Weaker Dollar Dynamics & Copper's Price Resilience Amid China Uncertainty

Copper prices rally on weaker USD and tight supply, but China demand risks linger. Low-cost oxide projects with flexible development paths best positioned for volatility.

- Copper prices have rebounded toward record levels, supported primarily by a weaker US dollar, even as investors temporarily discount weak Chinese macro data.

- Tight physical supply signals, visible in LME inventory drawdowns and delivery activity, are reinforcing near-term price resilience despite demand-side uncertainty.

- Arbitrage-driven flows between the LME and Comex are distorting regional inventory balances, masking underlying supply tightness.

- China's property downturn and slowing industrial output remain structural risks, likely to reassert influence once FX tailwinds fade.

- Developers and explorers with low-cost oxide projects, permitting visibility, and capital discipline are better positioned to weather volatility and attract capital.

Currency Markets Are Driving Copper More Than Demand - For Now

Currency dynamics have emerged as the dominant force behind copper's recent rally, overshadowing traditional demand fundamentals and creating a pricing environment driven more by financial flows than industrial consumption patterns.

FX Sensitivity Dominates Near-Term Price Action

Copper's recent move higher reflects pronounced FX sensitivity, with a weaker US dollar improving affordability for non-USD buyers and lifting dollar-denominated commodities across the board. LME three-month copper is now trading near US$11,678 per tonne, close to recent record highs, underscoring how financial variables are currently outweighing physical demand signals in the pricing mechanism.

The speed of the rebound highlights copper's evolving role as a macro hedge against currency debasement and fiscal expansion rather than a pure industrial proxy. Institutional investors have increasingly turned to copper as a strategic allocation in portfolios seeking protection against monetary policy shifts, a trend that has decoupled price action from traditional demand drivers in the short term.

Volatility Expected Through Year-End

Near-term volatility remains elevated, with market strategists expecting choppy intraday trading into year-end and early Q1. The question facing investors is whether current price levels can be sustained once FX tailwinds diminish or whether the market will recalibrate toward demand fundamentals that remain ambiguous at best. Positioning data suggests that speculative interest has built significantly during this rally, increasing the potential for sharp reversals if sentiment shifts.

For producers and developers, the current FX-driven rally presents both opportunities and challenges. Strong copper prices improve project economics on paper, but financing decisions based on elevated spot prices carry meaningful risk if dollar strength returns. Prudent operators are using this period to advance permitting and development work while maintaining conservative assumptions in their financial planning.

Physical Supply Tightness Is Providing Structural Support Beneath Prices

While currency movements explain near-term price volatility, structural supply constraints are providing a more durable foundation for copper valuations, with visible tightness across global inventory systems and limited new mine supply reinforcing long-term bullish fundamentals.

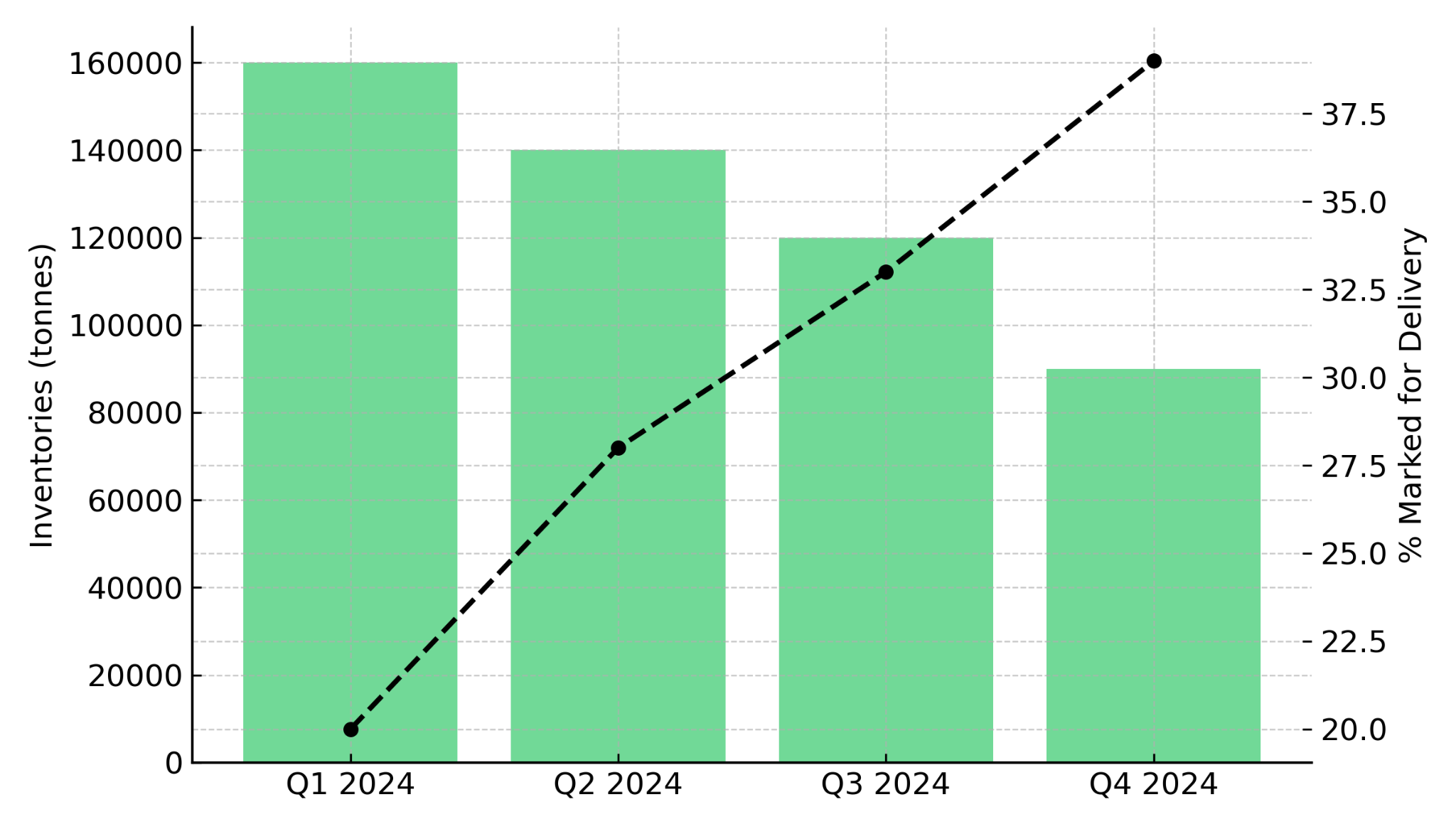

LME Inventory Drawdowns Signal Market Tightness

Beyond currency dynamics, physical supply constraints are providing a fundamental floor beneath copper prices. Approximately 39% of LME copper inventories are currently marked for delivery out, reducing immediately available supply and tightening the nearby market. Although headline inventories appear adequate, operational availability is considerably more constrained than surface-level data suggests.

Persistent supply concerns have been amplified by limited new mine supply globally, extended permitting timelines across key jurisdictions, and capital discipline following the last commodity downcycle. These constraints help explain why copper was able to reach record highs near US$11,952 per tonne earlier this year despite mixed macro data from China.

Oxide Projects Offer Faster Path to Production

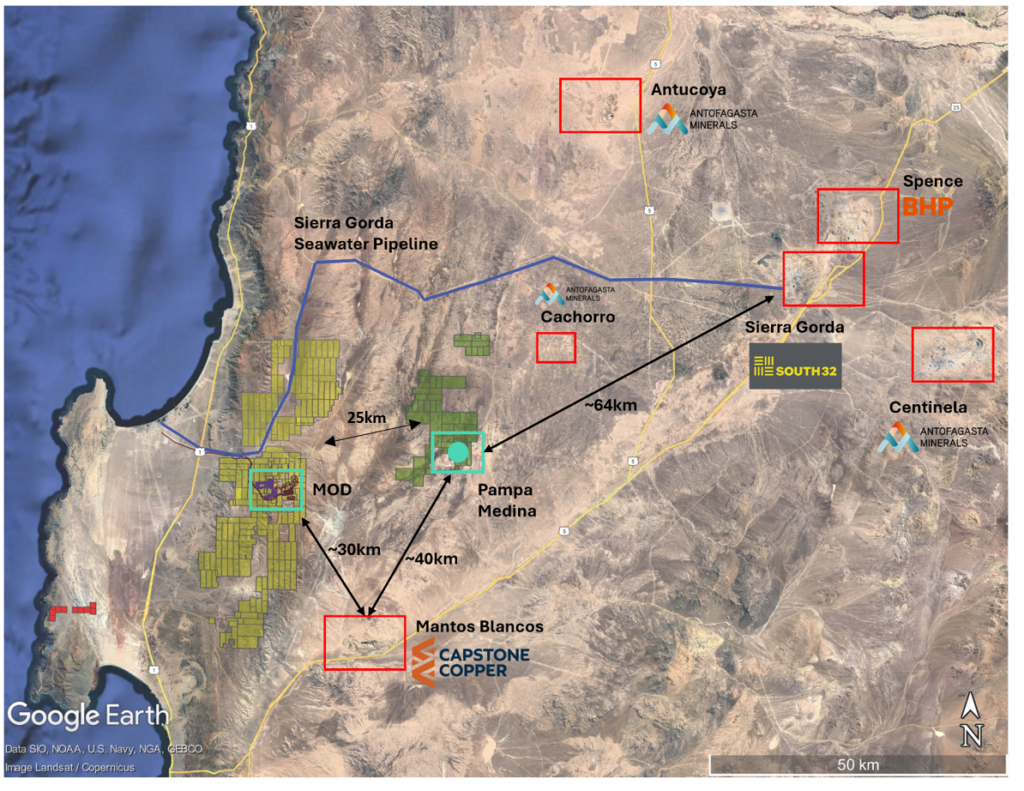

In this environment, developers with low-strip, heap-leach oxide projects can respond more quickly to supply gaps than large sulphide megaprojects requiring multi-year construction timelines. Marimaca Copper, operating in Chile's established copper corridor, exemplifies this positioning with its oxide-focused development strategy that offers lower capital intensity and reduced execution risk compared to conventional sulphide operations.

Recent drilling results have reinforced the scale potential of oxide resources that can be brought to market efficiently. Hayden Locke, Chief Executive Officer of Marimaca Copper, highlights the significance of recent intercepts:

"The oxide intersection which was nearly 50 metres at 2% in a broader zone of 160 metres at 1%. That is a material extension to the oxide envelope and certainly higher grade than what our current interpretation of the block model is."

Chile's Established Infrastructure Reduces Development Risk

Chile's position as the world's largest copper producer provides significant advantages for developers operating within established mining districts. Marimaca benefits from proximity to existing infrastructure, including power, water, and transportation networks, which materially reduces capital requirements and shortens development timelines compared to greenfield projects in frontier jurisdictions.

The regulatory framework in Chile, while evolving, remains fundamentally supportive of mining development, with established permitting processes and technical expertise throughout the supply chain. For investors evaluating copper developers, jurisdictional advantages can be as important as geological endowment, particularly in volatile commodity price environments where execution risk becomes a primary consideration.

Arbitrage Flows Are Distorting Inventory Signals Across Global Exchanges

Regional inventory imbalances driven by arbitrage trading are creating misleading signals about global copper availability, with headline stock figures masking underlying tightness and introducing additional complexity for investors attempting to assess true market conditions.

Regional Stock Imbalances Mask Underlying Tightness

While LME inventories are tightening, Comex stocks have risen to record highs, creating an apparent contradiction in global supply signals. This divergence is driven by price differentials rather than end-use demand, as the LME-CME arbitrage has incentivized physical copper to flow into the US market, temporarily inflating visible stocks on domestic exchanges.

These flows do not represent new supply entering the system; rather, they reflect opportunistic repositioning that can reverse quickly if spreads narrow. The current inventory configuration increases short-term volatility and mispricing risk, as headline figures provide a misleading picture of underlying availability.

Trade Policy Adds Regulatory Uncertainty

US trade policy remains a wildcard in this equation. Refined copper is currently exempt from a 50% import tariff, but policy remains under review, adding regulatory uncertainty to cross-border flows. Any policy shift could trigger rapid inventory rebalancing and corresponding price volatility. Investors should focus on global availability metrics and mine supply trajectories rather than regional inventory snapshots.

China's Demand Weakness Has Not Disappeared—It's Been Deferred

The world's largest copper consumer continues to exhibit structural weakness across key demand sectors, with recent macro data confirming that China's economic challenges have not been resolved but merely overshadowed by near-term currency and supply dynamics.

Macro Headwinds Persist Across Key Consumption Sectors

China remains the world's largest copper consumer, and recent data points signal continued stress in key demand segments. Factory output growth has slowed to a 15-month low, new home prices continue to decline on a month-over-month basis, and property sector distress remains acute, as highlighted by developer Vanke's ongoing bondholder negotiations for onshore debt repayment.

Historically, sustained copper bull markets have required Chinese construction and infrastructure support, not just FX tailwinds. The market's current willingness to look through China weakness reflects short-term positioning dynamics rather than resolution of underlying demand concerns. If the dollar stabilizes or strengthens, China demand risks are likely to reassert downward pressure on prices.

Cost Discipline Critical in Uncertain Demand Environment

For project developers and investors, this backdrop reinforces the importance of cost positioning and capital discipline. Projects with high all-in sustaining costs or extended development timelines face elevated risk in a scenario where China demand fails to recover as anticipated. The consensus view that China will eventually stimulate its way back to growth has underpinned much of the recent speculative activity in copper markets, but the timing and magnitude of any recovery remain highly uncertain.

Market participants should also consider that China's copper demand composition is shifting. While traditional construction-related consumption faces structural headwinds from demographic changes and property sector deleveraging, demand from electric vehicles, renewable energy infrastructure, and grid modernization continues to grow. The net effect on total copper consumption will depend on the pace of transition between these demand drivers, creating additional forecasting complexity for investors and producers alike.

Volatility Favors Projects with Low Capital Intensity & Flexible Development Paths

In environments characterized by elevated price volatility and demand uncertainty, investors increasingly favor development projects offering operational flexibility, reduced capital exposure, and multiple pathways to value creation rather than large-scale, capital-intensive operations with extended construction timelines.

Joint Venture Models Reduce Capital Requirements

In volatile price environments, investors tend to favor projects with low initial capital expenditure requirements, short development timelines, and oxide or near-surface resources amenable to heap leach processing. These attributes reduce sensitivity to commodity price drawdowns and financing windows, providing operational flexibility that traditional large-scale sulphide projects cannot match.

Fitzroy Minerals represents an interesting case study in balancing near-term optionality with long-term exploration upside. The company's flagship Polimet project in Chile's Coastal Cordillera offers shallow oxide potential paired with deeper sulphide targets, providing multiple pathways to value creation depending on market conditions.

Near-Term Cash Flow as Strategic Differentiator

The company is pursuing a joint venture structure that could provide non-operated cash flow at minimal capital intensity, a differentiated model among early-stage copper explorers. Merlin Marr-Johnson, Chief Executive Officer of Fitzroy Minerals, outlines the near-term rationale:

"We are working on terms with Pucobre to do a heap leach joint venture that gives us the potential for near-term non-operated cash flow, which we think will distinguish us from many other explorers in the market… We're looking at maybe attributable production of hopefully somewhere in the region of 10 million pounds of copper per annum attributable to Fitzroy coming through this plant."

Meanwhile, exploration drilling continues to expand sulphide targets beneath the oxide zone, with recent intercepts including 21 metres at 4% copper and 0.1 grams per tonne gold in sulphides, indicating significant scale potential for longer-term development.

Dual Pathway Strategy Provides Optionality

Fitzroy's approach illustrates the value of dual-pathway development strategies in uncertain markets. The near-term oxide heap leach opportunity provides potential cash flow and project validation while exploration work continues on higher-value sulphide targets. This staged approach allows the company to respond to market conditions opportunistically, advancing the oxide component if copper prices remain elevated while preserving sulphide upside for longer-term development when capital markets are more receptive to larger-scale projects.

The flexibility inherent in this model reduces binary execution risk and provides multiple inflection points for value creation. For investors, this translates to reduced downside exposure while maintaining participation in exploration upside, a risk-reward profile that becomes increasingly attractive as commodity price volatility persists.

The Investment Thesis for Copper

- The current market environment presents both opportunities and risks for copper-focused investors. The following considerations frame the strategic case for selective exposure to copper developers and explorers positioned to benefit from structural supply constraints while managing downside risk from demand uncertainty.

- Weaker US dollar dynamics continue to support copper prices, benefiting USD-denominated project economics and improving financing conditions for development-stage companies. Tight global mine supply and limited permitting pipelines provide structural price support that extends beyond near-term demand fluctuations.

- Arbitrage-driven inventory distortions should not be mistaken for surplus supply, and investors should focus on underlying production and consumption trends. China demand risks remain unresolved, reinforcing the need for exposure to low-cost, flexible projects that can maintain margin discipline through price cycles.

- Developers with low all-in sustaining costs, heap leach optionality, and clear permitting visibility are better positioned to attract capital through periods of elevated volatility. Near-term cash flow strategies, including joint venture structures and non-operated production, provide differentiated risk-reward profiles for early-stage companies. Projects in established mining jurisdictions with existing infrastructure offer reduced execution risk and shorter timelines to production.

Copper's Rally Reflects Financial Forces, Not a Demand Reset

Copper's recent strength is best understood as a currency- and supply-driven rally rather than a clean signal of demand recovery. The weaker US dollar has provided near-term support, while physical supply tightness offers structural underpinning to prices. However, China's demand weakness has not been resolved; it has merely been deferred as a pricing consideration while financial flows dominate market dynamics.

Investors should expect continued volatility as FX trends, China data releases, and trade policy signals evolve through year-end and into 2025. The interplay between these factors will determine whether current price levels can be sustained or whether a correction toward more conservative demand assumptions is warranted. Inventory distortions add another layer of complexity, as headline figures provide an incomplete picture of underlying availability.

In this environment, project quality, capital discipline, and execution visibility matter more than headline price momentum. Copper remains strategically important to global electrification and infrastructure themes, and long-term supply constraints are well documented. However, near-term price action will be driven by financial factors that are difficult to predict with precision. Selectivity, emphasizing low-cost operators, flexible development pathways, and strong balance sheets, will define investment returns in the copper sector through this period of uncertainty.

TL;DR

Copper has rallied toward record highs near US$11,678/tonne, driven primarily by US dollar weakness rather than genuine demand recovery. Physical supply tightness—with 39% of LME inventories marked for delivery—provides structural price support, while arbitrage flows between LME and Comex are distorting inventory signals. China's demand weakness remains unresolved, with factory output at 15-month lows and property sector stress ongoing. These risks will likely reassert once FX tailwinds fade. In this volatile environment, investors should favor low-cost developers with heap leach oxide projects, clear permitting visibility, and flexible capital structures over large-scale sulphide megaprojects requiring extended timelines and heavy financing.

FAQs (AI-Generated)

Copper's rally reflects currency dynamics rather than demand recovery. A weaker US dollar has improved affordability for non-USD buyers, while physical supply tightness and limited new mine supply provide structural support. China's demand weakness has been temporarily deferred as a pricing factor while financial flows dominate.

Approximately 39% of LME copper inventories are marked for delivery out, meaning operational availability is considerably tighter than headline figures suggest. This reflects persistent supply constraints from limited new mine development, extended permitting timelines, and capital discipline across the industry.

Price differentials between exchanges have created arbitrage opportunities, incentivizing physical copper to flow into US markets. This repositioning inflates Comex stocks temporarily but does not represent new supply—these flows can reverse quickly if spreads narrow.

Low-capital-intensity projects with heap leach oxide resources, short development timelines, and clear permitting visibility offer reduced sensitivity to price drawdowns. Joint venture structures providing non-operated cash flow also differentiate early-stage developers in volatile markets.

Primary risks include US dollar stabilization or strengthening, failure of Chinese demand recovery, and potential trade policy changes affecting cross-border flows. If FX tailwinds diminish, prices may recalibrate toward weaker demand fundamentals.

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

Stay Informed