Rising Copper Inventories & China's Smelter Surge Signal Near-Term Market Rebalancing

Copper prices ease as inventories rise and China expands smelting, but electrification demand and limited new supply keep the long-term copper outlook bullish.

- Copper's short-term correction reflects easing physical tightness, with exchange inventories rising more than 500,000 tonnes and Chinese refined production approaching record levels near 1.2 million tonnes per month.

- Macro headwinds, including a stronger US dollar, rising energy prices, and weaker Chinese import demand, are pressuring sentiment and pushing prices below the $13,000 per tonne threshold.

- Despite near-term softness, structural demand drivers remain intact, particularly electrification, electric vehicle adoption, grid expansion, and AI-driven power infrastructure.

- Long development timelines of approximately 17 years from discovery to production, combined with declining ore grades, constrain supply and reinforce forecasts of a potential 30% global copper deficit by 2035.

- Development-stage and exploration companies in established mining jurisdictions are attracting increasing investor attention, as infrastructure access, permitting progress, and strong project economics improve the likelihood of bringing new copper supply online

Macro Rebalancing in the Copper Market: Inventories Rise as Demand Signals Soften

After reaching record highs above $14,500/t in early 2026, copper prices have slipped below $13,000/t as rising inventories and macro pressures weigh on sentiment. Stocks across the LME, SHFE, and COMEX have increased by more than 500,000 tonnes this year, suggesting the tight physical market that supported the rally may be easing.

China, responsible for about 60% of global refined copper demand, continues expanding smelting capacity, with monthly output nearing 1.2Mt. A stronger US dollar, higher energy costs, and geopolitical tensions are also adding pressure to cyclical commodities.

Despite the pullback, the shift appears cyclical rather than structural. Inventory increases reflect short-term trade flows and seasonal demand, while long-term drivers, electrification, renewable energy, and digital infrastructure, continue to support copper demand.

China's Expanding Smelting Capacity Is Reshaping the Global Copper Supply Chain

China’s dominance in midstream copper continues to reshape global supply. Over two decades, it has accounted for more than 90% of global smelting capacity growth, increasing its share of refined output from about 15% in 2005 to roughly 50% today.

This expansion has created an unusual dynamic where record copper prices coincide with collapsing treatment and refining charges. In 2026, the benchmark between major miners and Chinese smelters fell to $0 per tonne, forcing smelters to rely more on by-product revenues from gold, silver, and sulphuric acid.

The imbalance reflects a structural bottleneck: smelting capacity is expanding faster than copper concentrate supply, while new mines take over a decade to develop and major discoveries remain scarce.

The Long-Term Copper Thesis Remains Intact Despite Short-Term Volatility

While near-term indicators suggest easing tightness, copper’s long-term outlook remains structurally bullish. Its high conductivity and durability make it essential for electrification, renewable energy, grid expansion, and energy storage. Electric vehicles alone require two to three times more copper than internal combustion vehicles.

Artificial intelligence is also emerging as a demand driver, as data centers require large investments in power and grid infrastructure. Wood Mackenzie estimates cumulative data center power investment could exceed $1 trillion globally by 2030.

Meanwhile, supply faces growing constraints. Ore grades have fallen about 40% since 1991, new mines are increasingly capital-intensive, and only about 5% of deposits identified in the past 35 years were discovered in the last decade. With development timelines averaging 17 years, supply may struggle to keep pace with demand.

Project Economics & Jurisdictional Stability Are Increasingly Central to Investor Allocation

Greater emphasis is placed on project economics, jurisdictional stability, and infrastructure access when assessing copper opportunities. Projects in established mining jurisdictions, particularly Chile, Peru, and parts of North America, benefit from mature infrastructure, regulatory frameworks, and skilled labor, reducing capital intensity and execution risk. Chile alone accounts for roughly 27% of global copper supply, with regions like Antofagasta hosting major operations such as Chuquicamata and Spence, supported by extensive power networks, ports, and specialized mining services that streamline project development.

Feasibility Validation & Construction Readiness

Within Chile’s established copper belt, Marimaca Copper, a development-stage company, is advancing the Marimaca Oxide Deposit in northern Chile. A definitive feasibility study outlined strong economics, including a post-tax NPV of about $1.1 billion and an IRR near 39%, placing the project among the more capital-efficient copper developments under review. Its oxide mineralization supports heap-leach processing with solvent extraction-electrowinning (SX-EW), producing copper cathodes directly and bypassing concentrate markets and smelting bottlenecks as refining capacity remains heavily concentrated in China.

Hayden Locke, President and Chief Executive Officer of Marimaca Copper, emphasized the significance of this milestone when discussing the study's outcome:

“The key milestone was delivering the DFS, which is the final piece of the puzzle before we transition into financing, detailed design, and engineering for the Marimaca oxide deposit. The study confirmed what we already knew: industry-leading capital costs, very competitive operating costs, and industry-leading returns on invested capital.”

With environmental approval already secured, the project has cleared one of the most significant regulatory hurdles that typically delay new mining developments. Combined with the region's mature infrastructure and access to experienced contractors, the project now sits firmly within the execution phase of the development cycle.

Exploration & Near-Term Cash Flow Optionality

Fitzroy Minerals, an exploration-stage company, is advancing two copper projects in Chile: the Buen Retiro oxide system near Copiapó and the Caballos sulphide discovery along the Pocuro Fault Zone. Buen Retiro hosts shallow oxide mineralization with potential for low-capital heap-leach development, while Caballos represents a polymetallic Cu-Mo-Au-Re system that could provide valuable by-product credits. Together, the projects offer investors exposure to near-term development optionality alongside longer-term discovery upside.

Chief Executive Officer Merlin Marr-Johnson highlighted the company's exploration focus and discovery progress when discussing the strategy behind the Buen Retiro project:

“We are exploring for copper, and crucially we are finding copper. Our focus is firmly on the Buen Retiro flagship asset, which we believe has major discovery potential.”

Exploration projects in Chile’s established mining corridors can benefit from nearby infrastructure and producing mines if discoveries prove economic. Buen Retiro sits in the Punta del Cobre district alongside operations such as Lundin Mining’s Candelaria and Capstone Copper’s Manto Verde. As grades decline and capital intensity rises across the sector, discoveries with shallow mineralization and strong infrastructure access may gain strategic value as copper markets tighten.

Exploration Scale & High-Grade Discovery Potential

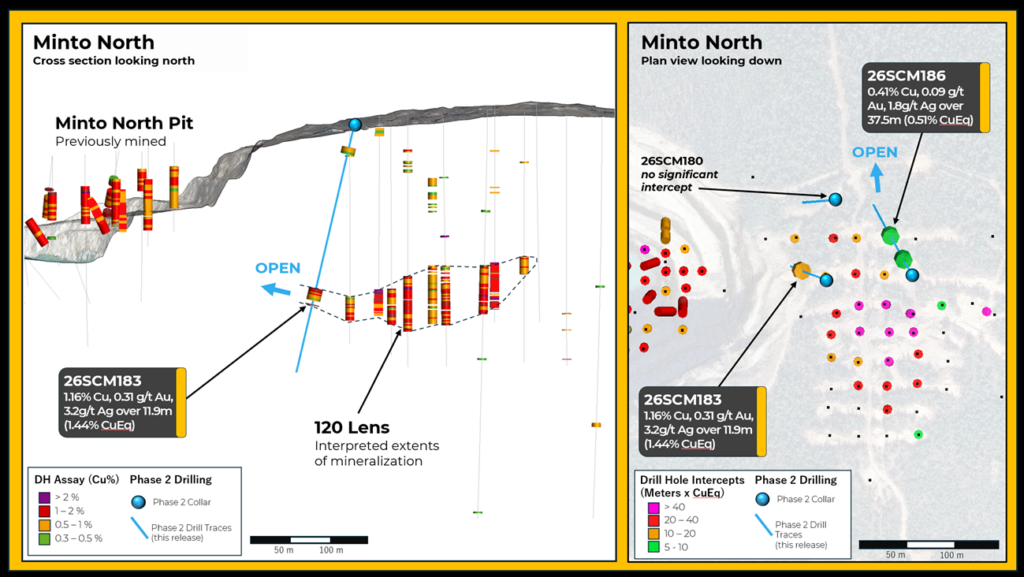

Abitibi Metals is advancing the B26 polymetallic copper-gold deposit in Quebec’s Abitibi Greenstone Belt, a VMS system recently expanded to 25.3Mt grading ~2.1% copper equivalent. The resource includes 13Mt indicated and 12.3Mt inferred, representing over 125% growth since 2023 and remaining open laterally and at depth. A fully funded 40,000-metre drill program in 2026 aims to expand the system toward a potential 30-50Mt scale.

Chief Executive Officer Jonathon Deluce highlighted the deposit’s growth potential when discussing the latest resource update:

“Since optioning the project, we’re up over 125% in terms of tonnage growth: 13 million tons indicated at 2.1% copper equivalent and 12.3 million tons inferred at 2.2%. One of the key questions from producers was, ‘How big can this get?’ Our thesis has been that this could very well be a 30 to 50 million ton deposit.”

Located about 7 kilometres from the former Selbaie mine, which produced roughly 60 million tonnes of polymetallic ore, the B26 project sits within one of Canada’s most established mining districts. As copper supply tightens, high-grade polymetallic systems in tier-one jurisdictions like Quebec may attract growing interest from producers.

Financing Cycles, Exploration Risk & Capital Allocation

Junior mining equities often show leveraged sensitivity to commodity prices, making them attractive during periods of structural supply tightness, but they also carry significant exploration and financing risk. Early-stage companies typically trade at discounts to project net asset value until resource estimates or economic studies demonstrate viability. As projects advance, valuation metrics such as enterprise value per pound of contained copper, resource grade, and metallurgical characteristics become key drivers.

During commodity downturns, exploration companies often raise capital at steep discounts, increasing dilution. In contrast, rising copper prices can trigger rapid re-ratings as investors anticipate future supply shortages.

A strong US dollar and higher interest rates can pressure commodity prices and increase financing costs for capital-intensive mining projects. In this environment, investors often favor diversified exposure across development stages, with lower-capex projects and those with established economics or permits generally attracting capital more easily.

The Investment Thesis for Copper

- Structural demand growth through electrification, electric vehicle adoption, renewable energy infrastructure, and AI-driven electricity demand is expanding copper consumption globally on a trajectory that current supply pipelines cannot satisfy.

- Supply constraints from declining ore grades, a shrinking pipeline of new discoveries, and permitting timelines extending up to 17 years restrict the pace at which new mines can be developed, reinforcing a widening structural deficit.

- Jurisdictional advantage in established mining regions, particularly Chile, provides projects with the infrastructure, regulatory frameworks, and skilled labor pools necessary to move from development to production with greater capital efficiency and lower execution risk.

- Capital efficiency through development projects featuring low capital intensity and strong project economics, including high internal rates of return and robust net present values, are better positioned to secure financing and advance through market cycles.

- Exploration optionality at the early-stage end of the spectrum offers leveraged exposure to future supply deficits, particularly where district-scale potential exists alongside near-term production pathways such as heap-leach joint ventures.

- Macro positioning supports copper as a strategic energy-transition metal, and even as near-term inventories normalize and prices consolidate, the long-term structural trends that drove the metal to record highs in 2026 remain firmly in place.

Copper's recent price pullback reflects a cyclical rebalancing rather than a structural shift in the market's long-term trajectory. Rising inventories, expanding Chinese smelting capacity, and softer short-term demand signals have temporarily eased the tight conditions that drove prices to record highs earlier this year. Yet the structural forces underpinning copper demand remain firmly in place. Electrification, renewable energy systems, and digital infrastructure all depend heavily on the metal, while supply growth faces mounting constraints from declining ore grades and lengthy development timelines.

Periods of market consolidation often provide entry points into companies advancing new copper supply in established mining jurisdictions. Development-stage companies with validated project economics, environmental approvals, and clear construction timelines, alongside exploration-stage companies with district-scale potential and near-term production optionality, represent the most direct means of accessing the structural copper investment thesis.

As the industry moves deeper into the energy transition, projects capable of delivering reliable copper production are likely to command increasing strategic value. The current market correction may prove less a warning sign and more a reminder of how difficult, and how valuable, it is to bring new copper supply online.

TL;DR

Copper prices have pulled back from record highs as inventories rise and China expands smelting capacity, signaling a short-term market rebalancing. However, the long-term outlook remains structurally bullish due to electrification, EV adoption, renewable energy, and AI-driven power demand, while supply growth is constrained by declining ore grades and 17-year mine development timelines. This dynamic is directing investor attention toward development and exploration companies in stable mining jurisdictions such as Chile and Canada, where projects with strong economics, infrastructure access, and scalable discoveries may play a critical role in meeting future copper demand.

FAQs (AI generated)

Copper prices have softened primarily due to short-term macroeconomic and supply-chain factors rather than a fundamental shift in demand. Exchange inventories across the London Metal Exchange, Shanghai Futures Exchange, and COMEX have risen significantly, indicating easing physical tightness. At the same time, China has increased refined copper production to near-record levels while macro headwinds, including a stronger US dollar, higher energy prices, and weaker Chinese import demand, have weighed on market sentiment. These conditions have pushed prices below $13,000 per tonne, signaling a temporary rebalancing after the strong rally earlier in 2026.

China’s smelting sector has expanded dramatically, accounting for more than 90% of global smelting capacity growth over the past two decades and producing roughly half of the world’s refined copper. This expansion has created a structural imbalance in the supply chain because smelting capacity is growing faster than copper concentrate supply. As a result, treatment and refining charges have collapsed, even falling to zero in some benchmark agreements. The situation highlights a critical bottleneck: while refining capacity continues to grow, the industry still requires new mines to supply the raw copper concentrate needed to feed those smelters.

Copper demand is expected to rise significantly as global energy systems electrify. Electric vehicles require two to three times more copper than internal combustion vehicles, while renewable energy projects, power grid expansion, and energy storage systems all rely heavily on copper components. In addition, artificial intelligence infrastructure and large data centers are creating new electricity demand, which requires expanded power generation and transmission networks. These structural trends are expected to increase copper consumption for decades, reinforcing forecasts of significant supply deficits in the future.

Because new mines take many years to develop, companies advancing projects today may become key future suppliers. Investors often look for development-stage companies with strong project economics, environmental approvals, and access to infrastructure, as these factors reduce execution risk and shorten development timelines. Exploration-stage companies can also offer significant upside if they discover large, scalable deposits in established mining districts. Together, these companies provide exposure to the long-term copper supply gap that many analysts expect to emerge over the next decade.

Junior mining companies can offer strong leverage to rising copper prices but also carry higher risk. Exploration results may fail to produce economically viable resources, and early-stage projects often require multiple financing rounds that can dilute shareholders. Market cycles also affect access to capital, with funding becoming more expensive during commodity downturns. Investors typically evaluate projects using metrics such as resource grade, contained metal, metallurgy, capital intensity, and jurisdictional stability to determine whether a project has a realistic path to development and production.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed