Fed Rate Expectations Lift Gold-Silver Ratio to 70:1 Despite Six Straight Annual Silver Deficits

Fed rate expectations lifted the gold-silver ratio to 70:1 as six straight silver deficits kept supply tight. PCE and Treasury yields are key catalysts.

- Silver fell 1.4% to $57.84 per ounce while gold rose less than 0.1%, pushing the gold-silver ratio to 70:1 near its two-year high.

- About 58% of silver demand comes from industry, making it more sensitive to growth data than gold.

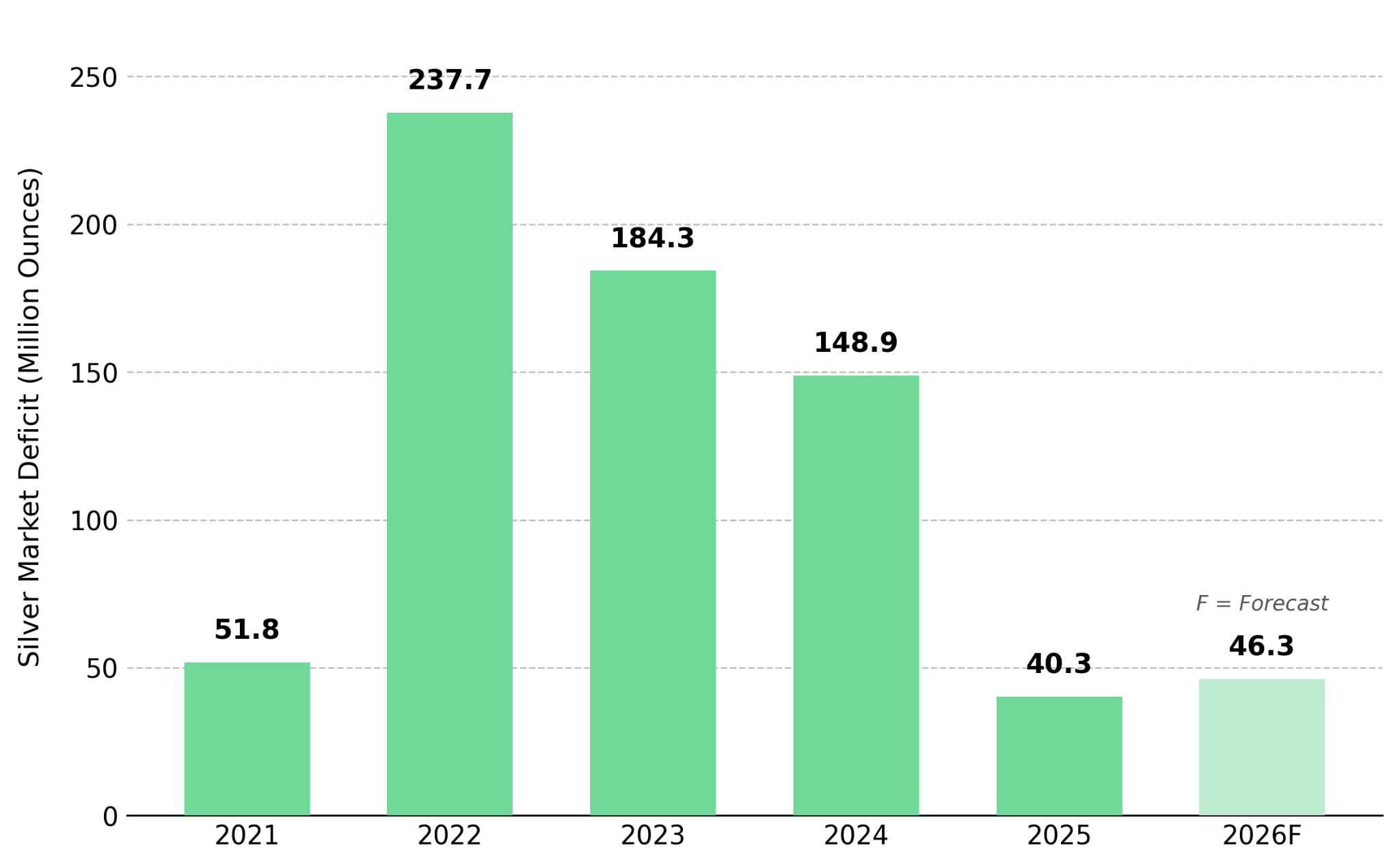

- The Silver Institute reports a sixth straight annual deficit of 46.3 million ounces, with 762 million ounces drawn from above-ground inventories since 2021, equal to about nine months of global mine supply.

- J.P. Morgan targets $81 per ounce for silver, implying a gold-silver ratio near 50:1 at current gold prices, versus the LBMA consensus of $79.57.

- A Fed hold followed by a softer-than-expected PCE print would likely narrow the ratio, while renewed September hike expectations would keep it near current levels.

Fed Rate Expectations & Gold-Silver Ratio: Why the Gap Widened

Silver fell 1.4% to $57.84 per ounce while gold rose less than 0.1%, pushing the gold-silver ratio to 70:1. The gap remained in place as silver traded near $57.00 while Brent crude held above $85 a barrel on renewed US-Iran tensions, and spot gold eased toward $4,035 after briefly trading above $4,050.

Although 70:1 remains within the historical range of about 30:1 to 127:1, the move shows the two metals responding to different demand drivers rather than an unusually stretched valuation. Silver remains more exposed to rate-sensitive industrial demand, while gold continues to draw support from central bank purchases and institutional buying.

Industrial Demand & Tight Supply: Why Silver Responds Differently Than Gold

Silver is more exposed to economic growth than gold because about 58% of its demand comes from industrial applications, including solar panels, semiconductors, EV components, and medical devices.

AI data centers are adding to that demand through silver paste used in high-temperature silicon carbide chips, while gold relies mainly on central bank purchases and institutional holdings. CME FedWatch prices a July Fed hold at about 90%, but 44% September hike odds and Brent crude above $85 continue to pressure silver's industrial outlook.

Fed Policy & Silver Outlook: What Could Move the Gold-Silver Ratio Next

Mine supply cannot respond to changes in interest rate expectations over a few weeks. Bunker Hill Mining's Idaho restart took six years after its 2020 ownership change, highlighting the long lead times needed to add new supply. With the market still facing a 46.3-million-ounce annual deficit, one restart is unlikely to shift the physical balance.

Base case: A Fed hold followed by a softer-than-expected PCE reading could narrow the gold-silver ratio into the low 60s, broadly supporting J.P. Morgan's $81 silver target.

Bear case: If September hike odds rise above 50% and Brent crude stays above $85, weaker industrial demand could keep the ratio at or above 70:1 through the September Fed meeting.

Fed Expectations & Silver Exposure: Why the Long-Term Thesis Still Holds

The setup affects physical or ETF-backed silver, silver mining stocks such as Bunker Hill Mining, and relative-value strategies that depend on gold and silver moving together. Those strategies came under pressure as the two metals diverged by more than one percentage point over two sessions.

Even so, a 1.4% daily decline does not change a market that has recorded six straight annual deficits and 762 million ounces of inventory drawdowns since 2021. The move reflects shifting rate expectations rather than stronger physical supply. CME FedWatch prices a July Fed hold at about 90%, making the PCE inflation report and updated September hike odds the next key catalysts.

Monitor PCE, Treasury Yields & Fed Odds Before Increasing Silver Exposure

The gold-silver ratio is likely to remain elevated while Brent crude stays above $85 a barrel and CME FedWatch prices September rate-hike odds at about 44%, supporting gold relative to silver.

Before increasing silver exposure, monitor three indicators: the PCE inflation report, September Fed rate-hike probabilities, and the 10-year Treasury yield. A Fed hold followed by a softer-than-expected PCE reading, combined with a sustained decline in the 10-year Treasury yield below 4.60%, would improve the outlook for silver and could narrow the gold-silver ratio from current levels.

If September rate-hike odds instead move above 50% or Treasury yields continue to rise, silver could remain under pressure despite its sixth consecutive annual supply deficit. Tracking these macro signals alongside the physical supply picture provides a more reliable framework for adjusting silver exposure than focusing on daily price movements alone.

Analyst's Notes

Subscribe to Our Channel

Stay Informed