$91.50 Uranium Term Prices Signal a Supply Deficit: Lasting Shift or One-Quarter Blip?

Uranium term prices are signaling a supply deficit before spot demand, with producer discipline, geopolitical risks, and capital allocation reinforcing the outlook.

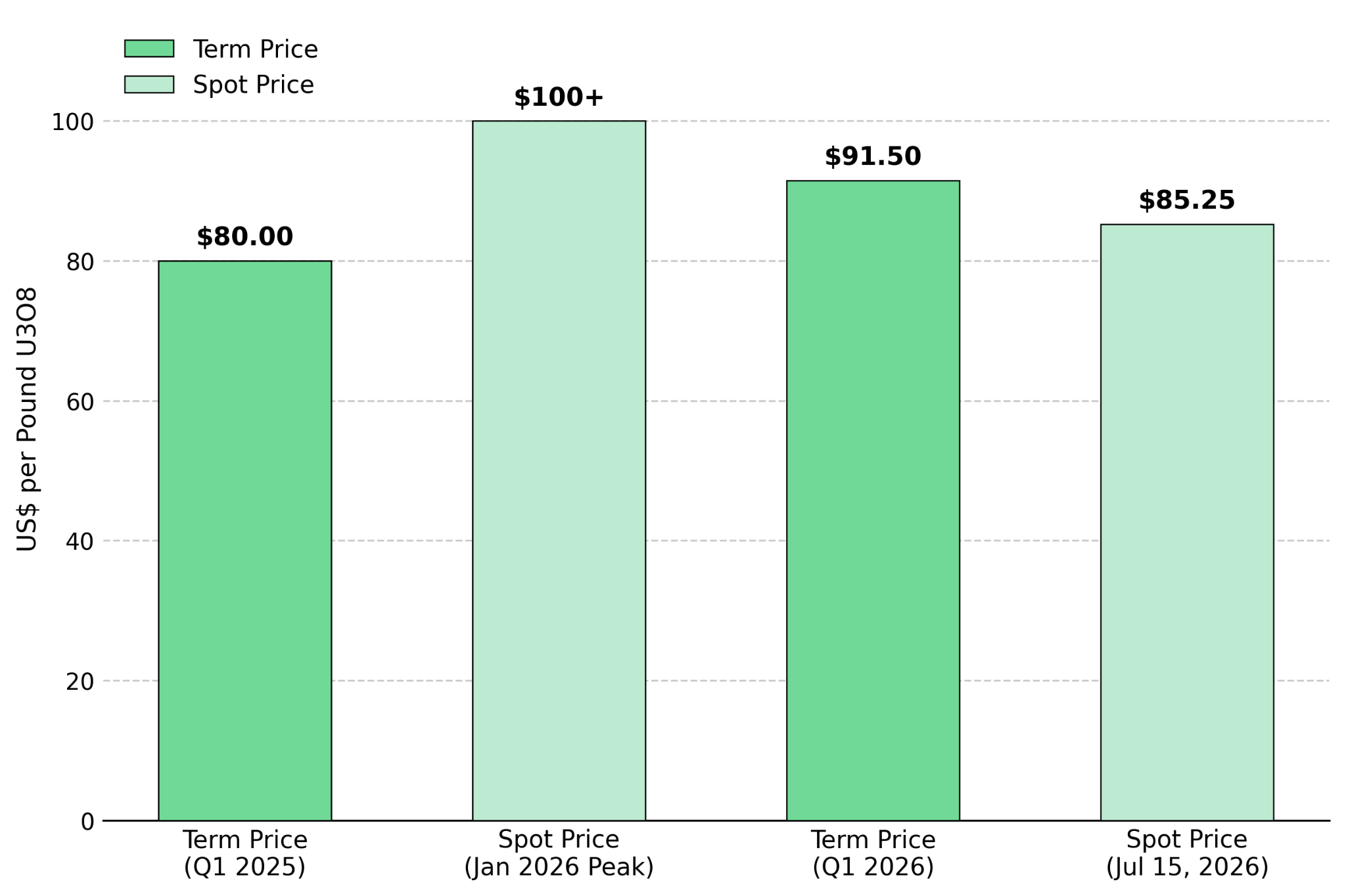

- Uranium's long-term contract price rose to $91.50 per pound U3O8 in the first quarter of 2026, up $11.50 from a year earlier according to Kazatomprom's first-quarter 2026 results, while the spot price has held between $84 and $87 per pound for more than three months, signaling tighter long-term supply expectations.

- The world's largest uranium producer cut 2026 output guidance by roughly 10%, choosing not to sell into current prices rather than signaling weaker demand.

- A sulfuric acid plant failure at a Saskatchewan processing mill halted production at the world's highest-grade uranium mine for 12 days, highlighting how Western uranium supply depends on a small number of processing facilities.

- Bank forecasts for 2026 range from $80 to $135 per pound, reflecting uncertainty over when the uranium supply deficit will tighten the market.

- Uranium companies at the production, development, and exploration stages allocate capital differently depending on how much evidence they require that the supply deficit will persist.

Utility Contracting Drives Higher Term Prices & Why Spot Uranium Has Yet to Confirm the Deficit

Uranium closed at $85.25 per pound on July 15, 2026, holding within an $84 to $87 range since April. That range remains well below the January 2026 spike above $100 per pound, which was driven largely by capital raising at the Sprott Physical Uranium Trust rather than utility demand. While the spot market has remained flat, long-term contract prices for uranium deliveries three to ten years ahead have continued to rise. Kazatomprom's first-quarter 2026 results put the long-term price indicator at $91.50 per pound, up $11.50 from a year earlier, while UxC reported some offtake contracts with ceiling prices of $140 to $150 per pound.

The split matters because the term and spot markets measure different sources of demand. Term prices reflect utilities locking in fuel purchases years ahead based on their long-term supply expectations. Spot prices reflect a thinner market driven more by fund buying than utility demand in recent quarters. When term prices rise while spot prices remain flat, utilities are signaling tighter future supply than the spot market alone suggests.

The key question is whether higher term prices reflect a lasting supply deficit or a temporary move that reverses if producers increase output in response to stronger contract prices. The analysis examines three factors: producer supply discipline, geopolitical risks across key uranium jurisdictions, and how producers, developers, and explorers are allocating capital in response to the same term-price signal.

Supply Discipline & Processing Constraints Tighten Uranium Supply

Kazatomprom, the world's largest uranium producer, cut its 2026 output guidance by roughly 10%, saying it would not return to full production because current demand does not justify higher output. That decision suggests producers see current contract prices as insufficient to justify higher output. Unlike a temporary outage, a voluntary production cut reflects a deliberate decision to limit supply, supporting the view that higher term prices are being driven by producer discipline rather than short-term trading.

The second development shows why supply discipline matters. Orano's McClean Lake mill in northern Saskatchewan, the only facility that processes ore from Cameco's Cigar Lake mine, shut down on June 29 after a sulfuric acid plant failure. With limited on-site ore storage, Cameco halted mining at Cigar Lake, the world's highest-grade uranium mine, until the mill restarted on July 11. Cameco maintained its 2026 production guidance of 17.5 to 18.0 million pounds U3O8 despite the 12-day outage, highlighting how a small number of Saskatchewan and Kazakh facilities support a disproportionate share of global primary uranium supply. When one of those facilities goes offline, little comparable processing capacity exists elsewhere to offset the disruption.

Operating Uranium Assets Generate Cash Flow Today & Enable Faster Growth

Producers are positioned differently from developers and explorers because they can monetize current uranium prices rather than wait to build new capacity. enCore Energy, a production-stage in-situ recovery (ISR) uranium producer in South Texas, illustrates how existing operations can expand capacity through phased investments instead of a single large capital project. Its Upper Spring Creek satellite ion exchange plant is being brought online in stages, feeding uranium-loaded resin into the existing Rosita Central Processing Plant instead of requiring a new standalone mill. ISR projects typically have lower operating costs and shorter permitting timelines than conventional hard-rock mines, allowing producers to expand output more quickly as long-term contract prices strengthen.

Energy Fuels illustrates another production-stage advantage: existing, licensed infrastructure. Its White Mesa Mill in Utah is the only operating conventional uranium mill in the US, with more than 45 years of permitted operating history. Uranium remains Energy Fuels' primary near-term cash flow, funding its expansion into rare earth separation and planned permanent magnet manufacturing through the acquisition of Vacuumschmelze.

Mark Chalmers, Chief Executive Officer of Energy Fuels at the time of the interview, was direct about where that revenue is coming from today:

"Uranium is now. We'll give guidance up to two and a half million pounds, and that's greater than anybody else in the United States. Really good cost structures, and prices are firming. So that is the revenue story right now."

Geopolitical Tensions Concentrate Uranium Supply & Strengthen the Case for Stable Mining Jurisdictions

Niger's government continues to assert its right to sell nationalized Somaïr uranium internationally despite an International Centre for Settlement of Investment Disputes tribunal order barring sales pending arbitration with Orano. Somaïr has historically accounted for roughly a third of Niger's uranium output. Any Nigerien uranium sold outside tribunal-approved channels creates traceability and contractual compliance risks for regulated buyers in the European Union, the US, and Japan, making this a supply-chain risk rather than simply a political dispute.

Russia adds another concentration risk to the uranium fuel cycle as Rosatom controls roughly 40% of global uranium enrichment capacity, while US import restrictions on Russian uranium products remain subject to waivers through January 1, 2028, leaving buyers dependent on temporary exemptions. Uranium has also become part of the broader US-China critical minerals rivalry after its addition to the USGS Critical Minerals List. The one-year US-China trade truce expires this fall, making it a key date for fuel-cycle supply chains if trade tensions escalate again.

Kazakh production discipline, the dispute in Niger, and Russia's waiver-dependent enrichment exports increase the value of uranium supply sourced outside those risks. In a market this concentrated, uranium supply from jurisdictions with stable permitting regimes and limited exposure to sanctions or nationalization risk is likely to command a premium. That backdrop helps explain why developers and explorers in jurisdictions such as Zambia and Canada are positioning differently around the same term-price signal.

Permitting Advances Ahead of Spot Demand & Why Uranium Developers Delay Construction

Development-stage uranium companies face a different decision than producers. Without operating infrastructure, developers must decide when to commit construction capital before stronger spot demand confirms the higher term-price signal.

Development Uranium Projects Expand Resources Before Committing Construction Capital

Atomic Eagle's Muntanga Uranium Project in Zambia has its Environmental and Social Impact Assessment approved on June 4, 2026, and the Office of the Vice President issued a No Objection to the Resettlement Action Plan. Management has said permitting alone will not trigger a construction decision. The 2025 feasibility study covers only the Muntanga and Dibbwi East deposits, excluding 44% of the company's current 58.8-million-pound resource base. Based on those deposits, it reported a post-tax NPV (8% discount rate) of US$243 million, a 20.8% IRR, a 3.5-year payback period, and operating costs of US$32.20 per pound.

Phil Hoskins, Chief Executive Officer of Atomic Eagle, said the company's capital sequencing reflects its expectation of a widening long-term uranium supply deficit:

"Everyone talks about a very obvious supply-demand imbalance that's opening up, and it's an imbalance that's going to continue over time. Roughly 150 million pounds is being produced at the moment on the supply side, and 200 million pounds is being consumed by the nuclear utilities. By 2040, that supply of 150 is going to drop to 50, based on current production, and demand will double to 400 million pounds."

Environmental Progress & Permitted Capacity Preserve Development Flexibility

IsoEnergy is following a similar strategy by preserving development flexibility rather than committing construction capital. Its Larocque East project in Saskatchewan's Athabasca Basin hosts the Hurricane deposit, which the company describes as the world's highest-grade Indicated uranium resource. In Utah, the permitted, past-producing Tony M Mine remains on standby under a toll-milling agreement with Energy Fuels, preserving restart capacity until market conditions justify new capital commitments.

Philip Williams, Chief Executive Officer of IsoEnergy, said the company's measured capital approach reflects a uranium supply deficit that does not depend on AI-driven electricity demand:

"All of the noise around AI doesn't really impact, to me, the work that we've done on the fundamental thesis. There's a supply deficit. When, exactly how much it is and when it really is, we can debate about that, but the deficit is real, and it's going to come and expand irrespective of how much new power comes on for what AI does and what data centers do."

Exploration Funding Signals Confidence in the Uranium Supply Deficit Before Spot Demand Returns

ATHA Energy raised US$63 million in the first quarter of 2026, led by Queens Road Capital, to fund a 20,000-meter drill program at its wholly owned Angilak Project in Nunavut while spot uranium prices remained flat and higher term prices were only beginning to emerge in producer disclosures. The company describes its 60.8- to 98.2-million-pound U3O8 exploration target at the Lac 50 corridor as conceptual rather than a defined mineral resource. Its 37.0-meter composite mineralized intersection at RIB North, the widest reported at the target, still requires additional drilling before it can support a classified resource. Financing a pre-resource project before stronger spot demand confirms higher term prices suggests specialist capital already sees the uranium supply deficit as credible.

Higher Term Prices Signal Tighter Uranium Supply & The Evidence Still Needed

Bank forecasts for 2026 range from $80 to $135 per pound, a $55 spread that reflects uncertainty over the timing and size of the uranium supply deficit. The wide forecast range suggests the market has not yet reached agreement on when tighter uranium supply will translate into higher prices.

The next several weeks should clarify whether higher term prices reflect a lasting supply deficit. Cameco's second-quarter 2026 earnings on July 30 will show whether the Cigar Lake outage affected full-year production guidance. Kazatomprom's operational update, expected in late July or early August, will show whether the company maintains, deepens, or reverses its production discipline. The Fed's July 29 rate decision could also influence uranium prices through its effect on the US dollar and real interest rates.

None of these events will resolve the spot-term split on their own. The gap will close either when utility spot buying returns and confirms tighter supply, or when another quarter of strong term contracting passes without higher spot demand, strengthening the case that utilities expect tighter supply ahead.

The Investment Thesis for Uranium

- Term prices provide a stronger indicator of future uranium supply-demand conditions than spot prices because they reflect utility contracting decisions made three to ten years ahead rather than thin, fund-driven trading activity.

- Supply discipline by the world's largest uranium producer strengthens the case for a supply deficit because a voluntary production cut reflects a deliberate decision to limit supply, unlike a temporary operational outage.

- Processing concentration increases supply risk, giving production-stage companies with existing, licensed infrastructure an advantage that new entrants cannot quickly replicate.

- Concentrated uranium supply in countries facing sanctions, nationalization disputes, or export restrictions increases the value of projects in stable mining jurisdictions.

- Capital allocation reflects each stage of the uranium development cycle: producers are monetizing current prices, developers are delaying construction while expanding project scale, and explorers are raising capital ahead of defining a mineral resource.

- The wide range in 2026 bank price forecasts shows analysts remain divided on when stronger term prices will be confirmed by spot demand.

The gap between uranium's spot and term markets will not close through price movements alone. It will close either when utility spot buying returns and confirms tighter supply, or when another quarter of strong term contracting passes without a comparable increase in spot demand. Cameco's earnings, Kazatomprom's operational update, and the Fed's rate decision will each provide new evidence over the next two weeks, but none will resolve the question on its own. None of the companies examined here is committing capital based solely on a uranium price forecast. Instead, each is aligning its capital commitments with a different level of confidence that higher term prices will eventually be confirmed by spot demand.

TL;DR

Uranium's term price has strengthened while the spot market remains flat, indicating utilities expect tighter long-term supply before that view is reflected in spot buying. Producer discipline from Kazatomprom, processing bottlenecks in Saskatchewan, and geopolitical risks across Niger, Russia, and the broader fuel cycle all support the deficit outlook. Companies are responding differently based on their stage of development, with producers expanding existing operations, developers delaying construction while advancing projects, and explorers securing funding before spot demand confirms the market. Upcoming updates from Cameco, Kazatomprom, and the Fed may provide additional evidence, but sustained utility spot buying remains the key confirmation signal.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed