Hedge Funds Cut Oil Exposure While Diesel Stayed 42% Above February, Signaling Refinery Constraints

Hedge fund selling pushed crude lower, but refinery constraints kept diesel 42% above February, raising mining fuel costs and delaying price relief.

- Hedge fund sales of 245 million barrels of Brent and WTI futures and options drove ICE Brent down $19.28/b to an average of $84.43/b in June, while WTI fell $16.72/b to $81.79/b.

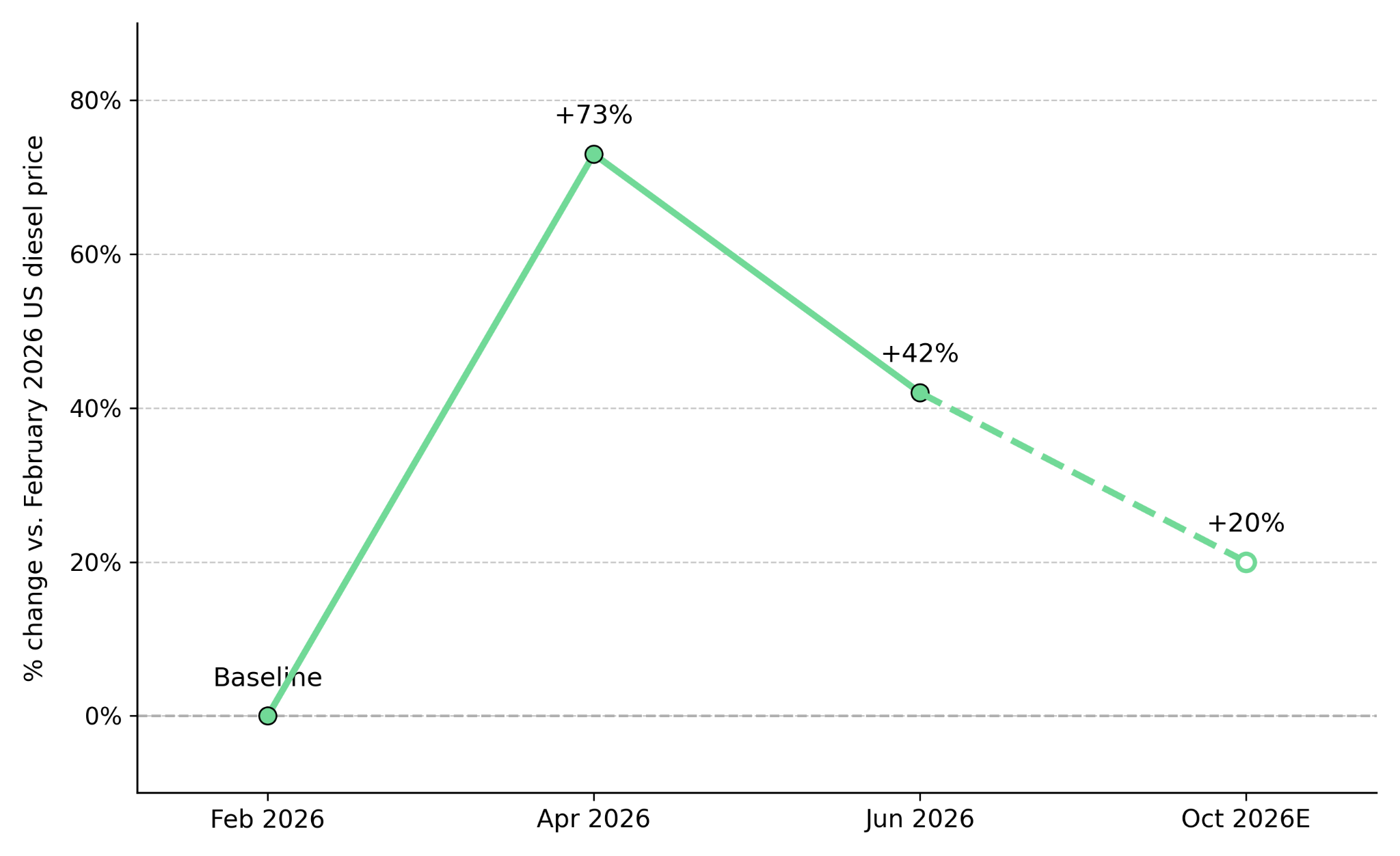

- US gasoil (diesel) averaged $121/b in June, 42% above February levels, while jet fuel averaged $127/b, 29% above February, showing refined fuel prices remained elevated despite lower crude prices.

- Global refinery throughput is about 5 mb/d below the 2025 average, keeping diesel and jet fuel prices elevated despite lower crude prices.

- OECD commercial oil stocks fell 21.8 mb to 2,770 mb in May, 48.6 mb below the five-year average, signaling tight physical oil supplies despite lower crude prices.

- The Wall Street Journal reported that the Strait of Hormuz "won't go back to normal," consistent with OPEC data showing ICE Brent averaged 33.5% higher in 1H26 than in 2H25 before June's speculative selloff.

Backwardation Signals Physical Oil Supply Remained Tight

The OPEC Monthly Oil Market Report said ICE Brent fell $19.28/b to average $84.43/b in June, while NYMEX WTI dropped $16.72/b to $81.79/b, marking the sharpest monthly decline since the geopolitical risk premium emerged in early 2026. Hedge fund and money manager sales of 245 million barrels of Brent and WTI futures and options drove the selloff, reducing ICE Brent net long positions by 80%.

Brent, WTI, and Oman forward curves remained in backwardation through June, with prompt barrels trading above forward delivery, indicating physical oil supplies remained tight despite the futures selloff. OECD commercial oil inventories fell 21.8 mb to 2,770 mb in May, leaving stocks 48.6 mb below the five-year average and 185.8 mb below the 2015-2019 average.

Strait Disruptions Reduced Refinery Throughput, Delaying Lower Fuel Prices

The Strait disruption cut Middle Eastern crude arrivals into Asia in the first quarter of 2026, reducing global refinery intakes by 7.3 mb/d from pre-crisis levels in April, the largest monthly decline of the year. Global refinery intakes remain about 5 mb/d below the 2025 average, limiting diesel and jet fuel output and delaying inventory rebuilding.

US gasoil (diesel) averaged $121/b in June, 42% above February levels, while jet fuel averaged $127/b, 29% above February. The Wall Street Journal reported that the Strait "won't go back to normal," while OPEC data showed lower East-West product flows kept fuel supplies tight and VLCC rates on West Africa-to-East routes 160% above year-ago levels in June.

Geopolitical Conflict Outlasted Market Positioning, Keeping Oil Risk Elevated

Hedge funds' combined ICE Brent and NYMEX WTI net long positions fell to their lowest level since January 2026 by the week ending June 30, showing futures markets were pricing in de-escalation despite no confirmed supply recovery. Iran struck US facilities in Gulf states over the weekend and declared the Strait of Hormuz closed, while President Trump reinstated a naval blockade and pledged to keep the Strait open "for a fee," leaving the conflict unresolved.

The OPEC Reference Basket fell $24.80/b to $89.75/b in June 2026, but its 2026 year-to-date average remained $93.67/b versus $72.04/b for full-year 2025, showing the June selloff reversed only part of this year's oil price gains.

Elevated Diesel Prices Increase Mining Costs, Exposing Unhedged Producers

US gasoil averaged $121/b in June, 42% above February levels, keeping fuel costs elevated for open-pit mines, haulage-intensive copper and iron ore operations, and drill-and-blast programs. Producers without fuel hedges in place before January 2026 are likely to report higher Q3 2026 operating costs because gasoil prices remained well above February levels even after crude prices fell.

Mining operations with access to cost-competitive grid electricity can reduce diesel cost exposure, while open-pit truck fleets without an alternative power source remain fully exposed to diesel prices of $121/b. State-subsidized producers in parts of the Middle East and Africa can offset higher diesel costs, while producers in unsubsidized markets, including Australia, the Americas, and most of Africa, absorb the full increase.

Fuel Supply Recovery Will Determine When Mining Costs Decline

Refinery throughput, not crude prices, determines when diesel prices decline. With refinery throughput still about 5 mb/d below the 2025 average, Brent at $84.43/b alone cannot bring diesel prices lower. In the base case, Strait tensions remain at current levels, refinery throughput recovers during Q3 2026, and diesel and jet fuel prices fall to 15% to 25% above February levels by October 2026.

In the bear case, another Strait closure would lift US jet fuel above $170/b, 78% above February levels, and US gasoil to nearly $148/b, 73% above February levels. That would raise airline and mining fuel costs back to April peaks within 30 to 60 days. The EIA Weekly Petroleum Status Report remains the key indicator to monitor, with US distillate inventories 37.7 mb below the five-year average. Three consecutive weekly inventory draws would indicate diesel supplies are tightening, while three consecutive builds would indicate refinery throughput is recovering.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed