Lithium Prices Test Three-Month Low as Mine Restarts Raise Supply: Structural Shift or Temporary Reset?

Lithium prices hit a three-month low as mine restarts boost spodumene supply, while strong Chinese battery production offsets growing market pressure.

- Lithium carbonate fell to CNY 154,000 per tonne, its lowest level since March, signaling continued pressure on lithium prices as lower feedstock costs filter through the supply chain.

- Platts assessed its SpodIX benchmark at $2,200/mt CIF China, down $270/mt from the previous week, lowering the price incentive for higher-cost spodumene producers.

- Mineral Resources restarted its Bald Hill spodumene mine after idling it since November 2024, targeting its first shipment in Q1 FY27.

- China's power and energy storage battery production reached 191.7 GWh in May, up 55.2% year over year, supporting lithium demand despite rising mine supply.

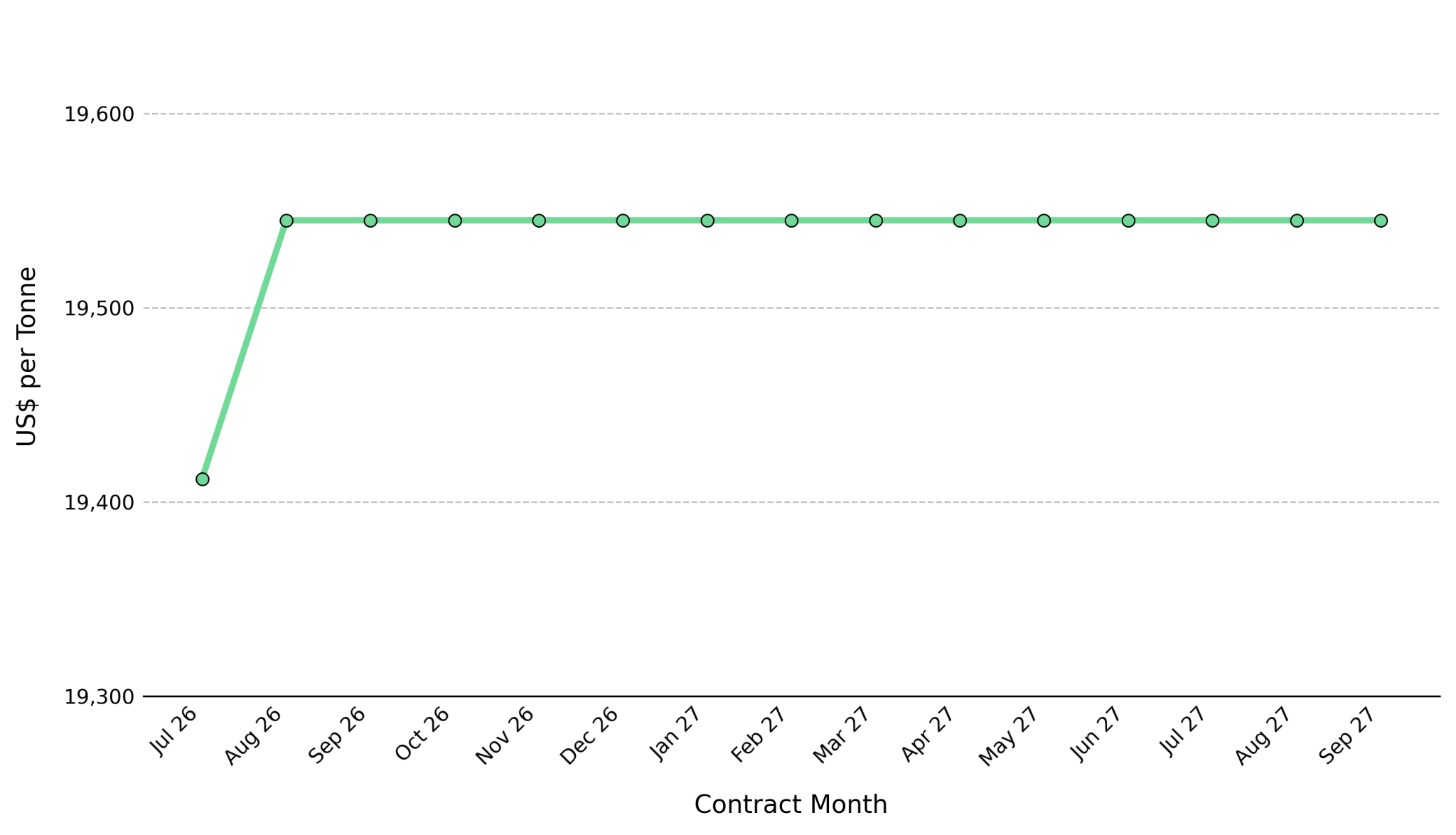

- The LME Lithium Hydroxide CIF (Fastmarkets MB) forward curve remains near $19,545/tonne from August 2026 through September 2027, indicating the market expects new mine supply to arrive on schedule.

Lower Spodumene Prices Push Lithium Carbonate to a Three-Month Low, Increasing Mine Supply Risk

Lithium carbonate fell to CNY 154,000 per tonne, its lowest level since March. Lower spodumene prices drove the decline as Platts assessed its SpodIX benchmark at $2,200/mt CIF China, down $270/mt from the previous week, while 5.5%-grade concentrate fell $247/mt to $2,003/mt CIF China, reducing feedstock costs for lithium producers.

Lower spodumene prices reduce the incentive to restart idled Australian mines. Mineral Resources restarted its Bald Hill mine after idling it since November 2024, while Core Lithium restarted its Finniss project. Those restarts are increasing supply, pushing spodumene prices lower, and raising the risk that additional mine restarts become uneconomic if prices continue to fall.

Rising Lithium Supply Meets Strong Battery Demand, Delaying a Price Recovery

Three developments are increasing lithium supply. Bald Hill restarted and is targeting its first shipment in Q1 FY27. CATL's Jianxiawo mine received approval to resume operations after a prolonged suspension. Mt Marion's owners approved a $490 million expansion, increasing annual spodumene concentrate capacity from 500,000 mt to 600,000 mt and adding future supply to the market.

Battery demand remains strong despite rising lithium supply. China's power and energy storage battery production reached 191.7 GWh in May, up 55.2% year over year. Chinese battery producers increased production and lithium purchases to defend market share despite slower EV order growth. Higher mine output is weighing on spodumene prices, while stronger battery production continues to absorb lithium supply, limiting downside pressure on the market.

Mine Restarts Delay New Lithium Supply, Extending Price Pressure Over Multiple Quarters

Mine restarts take time to translate into shipped volumes. Bald Hill is targeting its first shipment in Q1 FY27, about two to three quarters after restarting operations. That lag delays the supply impact, while producers typically expand output during higher-price periods and scale back production when prices weaken.

In the base case, Bald Hill begins shipments in Q1 FY27 as Mt Marion expands capacity to 600,000 mt per year, increasing spodumene supply and keeping downward pressure on the SpodIX benchmark. In the bull case, China's power and energy storage battery production remains above 191.7 GWh, absorbing the additional supply from Bald Hill and Mt Marion and pushing lithium carbonate back above CNY 154,000 during Q3 2026.

Lower Spodumene Prices Squeeze Mining Margins, Leaving Upstream Producers Most Exposed

Spodumene producers are more exposed to falling prices than downstream battery makers. Producers that rely on the spread between spodumene costs and lithium chemical prices face compressed margins because the SpodIX benchmark fell $270/mt and 5.5%-grade concentrate fell $247/mt in one week, while shipment volumes cannot adjust as quickly.

Mineral Resources restarted Bald Hill only after sustained lithium prices supported the decision, showing that mine supply responds to price strength with a lag. Because supply adjustments trail price movements, weekly spodumene assessments and monthly battery production together provide the clearest signal of whether supply or demand is driving lithium prices.

Mine Supply Delays & Stronger Battery Demand Could Lift Lithium Prices

Lithium carbonate remains near CNY 154,000 as sharp declines in spodumene prices and mine restarts at Bald Hill, Jianxiawo, and Finniss increased expected supply. That combination lowers raw material costs for battery producers while reducing revenue for spodumene producers.

Lithium prices would likely recover if Bald Hill's Q1 FY27 first shipment is delayed or Chinese battery production grows faster than May's 55.2% year-over-year rate. Either outcome would tighten spodumene supply, lifting the SpodIX benchmark above $2,200/mt CIF China and supporting higher lithium carbonate prices.

Weekly Platts spodumene assessments and the China Automotive Battery Innovation Alliance's monthly power and energy storage battery production figures will show whether May's 55.2% year-over-year battery production growth continued into June, indicating whether supply growth or battery demand is driving lithium prices.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed