Helium’s Price Surge Resets Global Supply Priorities and Elevates Strategic Asset Values

Helium prices surge 400% to $97K/mt as supply shortages & US export controls reshape global markets. Australian developers positioned for premium valuations.

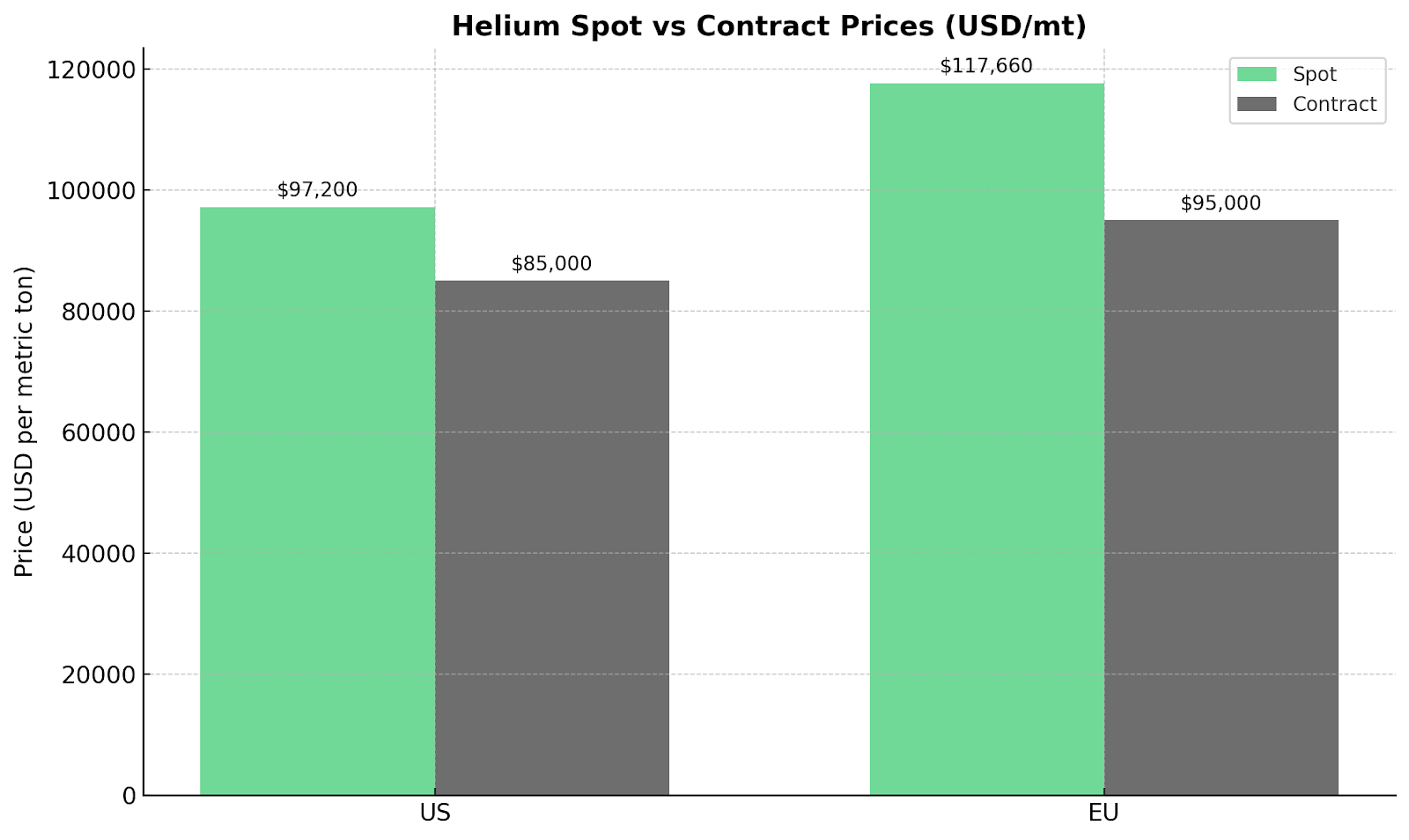

- Helium prices have surged ~400% in 2025 to ~$97,200/mt in the U.S. and >$117,000/mt in Europe, driven by supply shortfalls and surging high-tech demand.

- Supply chain fragility is amplified by geopolitical disruptions, U.S. export controls, and reliance on byproduct output from natural gas fields.

- Strategic reclassification of helium in the U.S. is shifting buyer behavior toward long-term contracts and politically stable supply sources.

- Developers like Georgina Energy in Australia are positioned to benefit from scarcity pricing, low-risk jurisdictions, and resource scale.

- Volatility in spot pricing offers tactical trading opportunities, while structural deficits support long-term capital allocation to helium projects.

Helium's Strategic Repricing in 2025

From Niche Gas to Strategic Material

Helium's unique physical properties—inertness and ultra-low boiling point—underpin its irreplaceable role in semiconductors, aerospace, magnetic resonance imaging, and quantum computing. The United States designation of helium as a strategic material introduces export restrictions, tightening global supply and forcing international buyers to secure alternative sources or pay premium prices for domestic production.

Historical market cycles from 2017, 2019, and the current 2025 spike demonstrate that price surges are prolonged when supply shocks align with demand growth. Unlike previous episodes where temporary production increases could moderate prices, the current shortage reflects structural constraints in byproduct-dependent supply chains and geopolitical restrictions on major producing regions.

The shift from opportunistic buying to long-term supply contracting represents a fundamental change in market dynamics. Industrial users previously relied on spot markets for flexibility but now prioritize supply security over cost optimization. This behavioral change supports sustained pricing power for producers in stable jurisdictions, particularly those with development-stage projects capable of scaling production over multi-year timelines.

Supply Disruption & Demand Acceleration

Geopolitical Risk & Supply Chain Fragility

Geopolitical risks and ongoing shipping disruptions continue to underline the interdependence between liquefied natural gas flows and helium availability. Major helium-producing facilities in Qatar and Algeria operate as integrated complexes where LNG production disruptions immediately impact helium output. Russian supply reductions due to sanctions and delays at the Amur facility limit new capacity additions, while geopolitical tensions in Eastern Europe threaten existing supply routes to European markets.

Over 90% of global helium output is byproduct-based, making supply inelastic in the short term. Natural gas producers optimize operations for methane extraction and LNG production, with helium recovery as a secondary consideration. This structure creates bottlenecks when demand exceeds the byproduct yield from existing gas processing facilities, requiring new capital investment and multi-year development timelines to meaningfully increase supply.

Demand Catalysts in Technology & Medicine

Semiconductor fabrication expansions in the United States, Taiwan, and South Korea are increasing helium intensity across the industry. Advanced chip manufacturing requires ultra-pure environments where helium's inert properties prevent contamination during critical processing steps. Each new fabrication facility represents a multi-decade helium demand commitment, with consumption patterns that remain stable regardless of semiconductor price cycles.

Growth in magnetic resonance imaging installations across emerging markets adds incremental demand from the healthcare sector. Space exploration and defense contracts contribute additional consumption, particularly for applications requiring helium's unique cooling properties in extreme environments. Quantum computing development, while still nascent, represents a potential demand catalyst with exponential growth characteristics should the technology achieve commercial viability.

Pricing Dynamics & Market Structure

Spot vs Contract Market Divergence

Spot market premiums in Europe trade 20-25% higher than United States levels, reflecting supply chain constraints and limited alternative sources for European industrial users. Long-term contract prices lag spot market movements but offer stability to producers with forward sales programs and buyers seeking predictable input costs for multi-year projects.

Geographic arbitrage opportunities exist between United States, European Union, and Asia-Pacific supply chains, though transportation costs and regulatory restrictions limit the effectiveness of cross-border trading. The strategic material designation in the United States creates additional complexity for international arbitrage, as export licenses may be required for large-volume transactions.

Volatility & Arbitrage Opportunities

Seasonal maintenance shutdowns at major processing facilities and liquefied natural gas flow shifts amplify short-term volatility in regional markets. These predictable disruptions create trading opportunities for sophisticated participants with storage capabilities and flexible supply arrangements. However, the limited number of major suppliers and high barriers to entry in storage infrastructure restrict participation to established industry players.

Chief Executive Officer Anthony Hamilton of Georgina Energy contextualizes the market dynamics:

"Our whole concept is to sell at the wellhead to mitigate infrastructure costs. The off-taker is responsible for putting a plant there."

Case Study: Stable Jurisdiction Leverage in Helium

Australia's Emerging Role in Strategic Gas Supply

Australia's political stability, established infrastructure, and existing liquefied natural gas footprint position it as a premium helium jurisdiction for international buyers seeking supply security. The Northern Territory and Western Australia offer infrastructure synergies through existing roads, rail networks, pipelines, and the Darwin processing plant that reduce development costs and timeline risks for new helium projects.

The Australian government's commitment to critical minerals development and streamlined permitting processes provides regulatory certainty that contrasts favorably with emerging markets where policy changes can significantly impact project economics. This jurisdictional advantage becomes more valuable as industrial users prioritize supply security over marginal cost savings.

Georgina Energy: Scale, Scarcity & Catalysts

Georgina Energy represents the investment thesis for helium development in stable jurisdictions through its tier-one resource scale and strategic positioning. The company's Hussar EP513 project demonstrates potential in-situ value of $55 billion for combined helium and hydrogen resources, while the Mount Winter EPA155 resource upgrade in May 2025 increased helium and hydrogen resources by 15%.

Operational advantages include proven gas flows from existing wells, an off-take strategy designed to avoid major infrastructure capital expenditure, and plans for a hydrogen-powered purification plant to reduce operating costs. The wellhead sales approach transfers infrastructure risk to off-take partners while preserving margin capture for Georgina Energy.

Market timing aligns with regulatory milestones, as drilling permits for Hussar and approval for Mount Winter are expected in 2025. Re-entry drilling and seismic work have been completed, positioning the company to commence development activities upon regulatory approval. The Northern Territory government's infrastructure incentives and Australia's $110 billion national infrastructure plan provide additional support for project development.

Chief Executive Officer Anthony Hamilton notes the economic validation of the resource:

"We announced the scoping study on the 25th of February which was done by a highly respected group, with the revenue potential for Hussar between 7.3 million to 28 million USD per annum depending on production rates."

Capital Formation & Investment Positioning

Funding Windows in Strategic Commodities

High-price environments attract early-stage capital to helium projects, but investors increasingly focus on de-risked jurisdictions with established regulatory frameworks and infrastructure access. The shift from green hydrogen investment hype toward blue hydrogen and nuclear-powered hydrogen positions helium similarly as a critical enabler commodity with strategic importance beyond current applications.

Capital market sentiment favors projects with proven resources, clear development pathways, and off-take arrangements that reduce market risk. The premium valuation commanded by stable jurisdiction projects reflects investor recognition that regulatory and infrastructure risks often outweigh marginal resource quality differences in investment returns.

Mergers & Acquisitions and Off-take Trends

Original equipment manufacturers and semiconductor producers are exploring direct project stakes to secure long-term supply arrangements outside traditional commodity markets. Long-term off-takes with pricing floors are gaining prevalence as industrial users prioritize supply security and producers seek financing certainty for capital-intensive development projects.

Strategic partnerships between developers and end users create alignment around development timelines and specification requirements that traditional commodity trading relationships cannot provide. These arrangements become more valuable as helium's strategic importance increases and alternative supply sources become constrained.

Regulatory & Environmental Considerations

Environmental, Social & Governance in Helium Development

Helium production demonstrates a lower environmental footprint compared to traditional hydrocarbon extraction, with minimal carbon dioxide emissions in processing operations. Integration with renewable energy sources or hydrogen-powered operations enhances the environmental, social, and governance profile of development projects, appealing to institutional investors with sustainability mandates.

The byproduct nature of most helium production means environmental impacts are primarily associated with underlying natural gas extraction rather than helium-specific operations. This characteristic provides regulatory advantages in jurisdictions where hydrocarbon development faces increasing scrutiny, as helium recovery can be positioned as value optimization rather than additional resource extraction.

Regulatory Certainty as Competitive Edge

Australia's clear permitting frameworks reduce timeline risk compared to emerging markets where regulatory changes can significantly impact project development schedules. Established environmental assessment processes and transparent approval criteria provide predictability that enables more accurate project finance modeling and reduces contingency requirements in development budgets.

Risk Factors for Investors

Overreliance on liquefied natural gas-linked supply sources creates vulnerability to upstream disruptions that may not directly relate to helium demand fundamentals. Potential new mega-projects, particularly in regions with large natural gas reserves, could alter supply balances if development timelines accelerate beyond current industry expectations.

Substitution risk exists in certain technological applications where hydrogen cooling in magnetic resonance imaging or alternative inert gases in semiconductor manufacturing could reduce helium consumption. Price volatility affects project financing assumptions and may require more conservative development approaches or additional hedging arrangements to maintain investment returns.

The Investment Thesis for Helium

- The investment case for helium centers on structural supply deficits created by the byproduct nature of production that limits rapid capacity increases. Strategic reclassification in the United States and buyer preference for stable jurisdictions support premium pricing for projects in low-risk geographies like Australia.

- Demand diversity across semiconductors, healthcare, aerospace, and emerging quantum computing applications creates multi-decade demand visibility that supports long-term capital allocation.

- Project readiness through proven gas flows, infrastructure access, and near-term development positions developers for revaluation as helium pricing reflects strategic commodity characteristics rather than traditional commodity market dynamics.

- Development timelines aligned with multi-year demand growth trends provide revenue visibility that supports project financing and strategic partnerships with end users.

- Risk-adjusted growth potential through resource expansion or merger and acquisition activity offers additional upside for investors in established developers with proven resource bases and regulatory approvals.

Strategic Gas in a Repriced Market

Helium's transformation from industrial gas to strategic material reflects broader themes of supply chain security and technological dependence on specialized inputs. The combination of supply fragility, geopolitical risks, and structural demand growth creates asymmetric upside opportunities for well-positioned projects in stable jurisdictions.

The repricing of helium markets validates investment strategies focused on resource scarcity, jurisdictional stability, and strategic importance to critical industries. For institutional and sophisticated retail investors, the helium sector offers exposure to these macro themes through companies with proven resources and clear development pathways.

Market dynamics favor developers who can navigate regulatory requirements, secure off-take arrangements, and optimize operations for high-value production. The strategic importance of helium ensures continued policy support and industrial interest, supporting valuations that reflect scarcity premiums rather than traditional commodity market metrics.

Analyst's Notes

Subscribe to Our Channel

Stay Informed