Highest Helium Grade Recorded in North America: Pulsar Helium's Minnesota Project as the Domestic US Solution | Made In America

Pulsar Helium holds a high-grade primary helium discovery in Minnesota at a time when 45% of global supply is offline and domestic demand is surging.

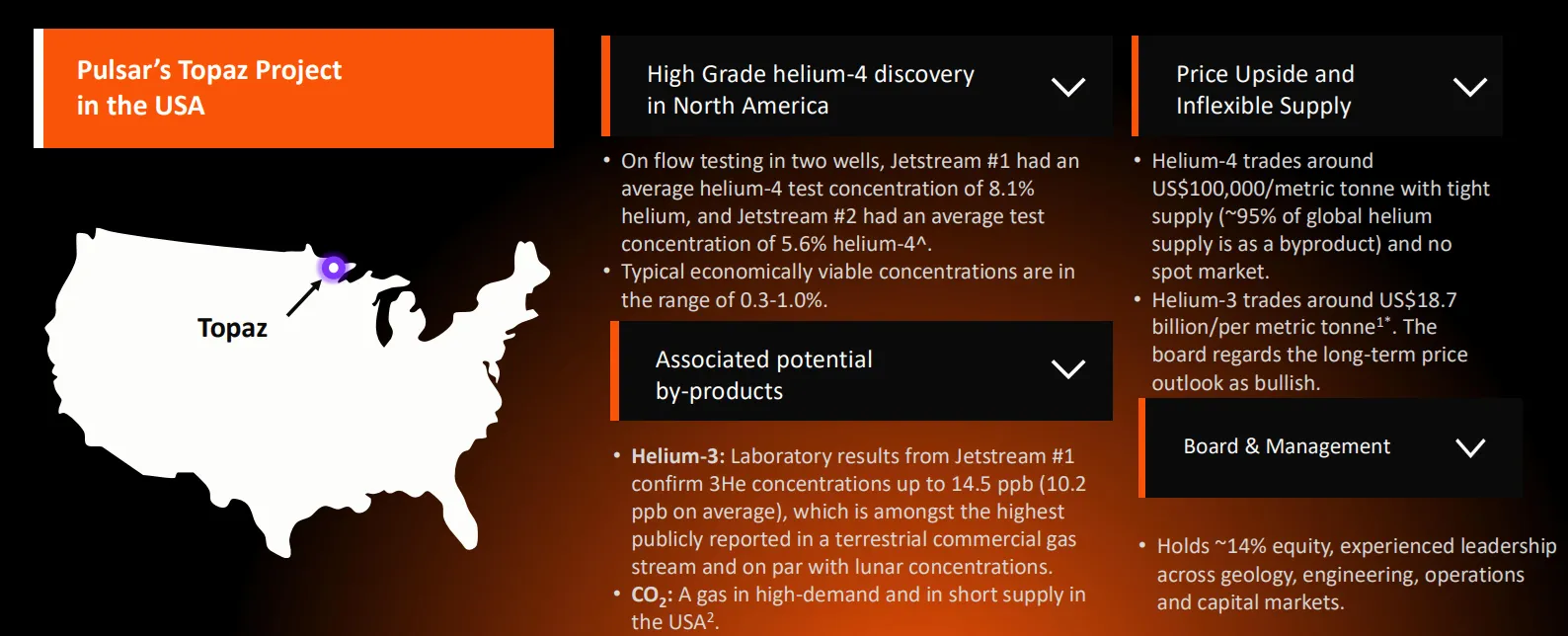

- Pulsar Helium is developing the Topaz project in northern Minnesota, a primary helium resource averaging 8.1% helium concentration across seven drilled wells making standalone commercial extraction viable without dependence on natural gas volumes or pricing.

- Geopolitical disruption has removed approximately 45% of global helium supply from the market, with the closure of the Strait of Hormuz cutting Qatar's export route and Russia introducing export controls, creating a supply deficit with no short-term self-correcting mechanism.

- Minnesota finalised its helium-specific operational regulations in June 2026 wherein legislation is built largely on the work Pulsar has conducted at Topaz thus removing a material non-geological risk from the project's development timeline and establishing a clear regulatory pathway to production that did not previously exist.

- The company has engaged Chart Industries to analyse the project's gas composition and begin designing a bespoke helium processing facility, while also confirming the presence of Helium-3 at Topaz, a rare isotope on Earth with applications in quantum computing and fusion research.

- With production-ready well drilling scheduled to commence in September 2026, an independent resource update underway, and an economic assessment being prepared, Pulsar Helium is targeting 2027 with concrete production guidance

Pulsar Helium (TSXV:PLSR) is developing the Topaz helium project in northern Minnesota at a moment when geopolitical disruptions has removed approximately 45% of global helium supply from the market. With high-grade primary helium, confirmed helium-3, a supportive regulatory environment, and a US engineering partner already engaged, the company is advancing toward a production decision in a commodity that underpins semiconductor manufacturing, medical imaging, and quantum computing.

The Strategic Case for Domestic Helium

The United States is the world's single largest consumer of helium. It is a commodity whose importance is largely invisible to the general public but is an irreplaceable input in semiconductor fabrication, MRI scanning, space launch systems, and an emerging generation of quantum computing infrastructure. Demand for helium is projected to double by 2035, driven primarily by growth in chip manufacturing and high-performance computing.

The supply picture has deteriorated sharply. More than 95% of the world's helium is produced as a byproduct of natural gas processing, which means output cannot be increased on demand. Qatar has historically supplied approximately 35% of global helium, Russia contributes a further 10%. Together with US domestic sources, these three jurisdictions have underpinned global supply for decades.

The architecture is now under severe stress with the conflict in the Middle East has closed the Strait of Hormuz to container shipping, cutting Qatar's export route. The CEO of QatarEnergy has indicated that the production facility could take three to five years to return to full operation. Meanwhile, Russia has introduced export controls. The combined effect is that roughly 45% of global helium supply is currently offline, with no near-term mechanism for replacement given the byproduct nature of conventional production.

Against this backdrop, Pulsar Helium is developing what it believes to be a large-scale primary helium resource in the United States, one whose output would flow directly to US end users without the transit vulnerabilities, long-term take-or-pay contract structures, and single-point-of-failure risks that have historically defined the global helium trade.

Topaz Project: A Primary Resource in a Byproduct World

In a primary resource, helium is the principal economic driver of extraction. In a secondary or byproduct resource which is the majority of global production, helium is separated from natural gas streams whose economics are dictated entirely by gas prices and gas demand. This structural difference means that a primary producer can respond to helium market conditions directly, offering end users a degree of flexibility that the current supply chain cannot.

Topaz is located in northern Minnesota and was identified following an accidental discovery during nickel and copper exploration drilling when a drill hole encountered gas that tested at one of the highest helium concentrations in recorded history between 10-12%. Pulsar Helium was founded on the basis of that discovery and listed via IPO in the third quarter of 2023.

The company has since drilled seven wells across the project area, all of which have encountered gas, with current results averaging 8.1% helium concentration. To place that figure in context: Qatar's helium concentration runs at approximately 0.04% at which the operation is economic because it processes an enormous volume of natural gas with helium as a recoverable fraction. At 8.1%, Topaz operates in an entirely different grade regime, one that makes primary extraction commercially viable without needing natural gas volumes to justify it.

Helium-3: An Unexpected Addition

A more recent development has added a further dimension to the Topaz project. Laboratory testing including analysis by two US federal government laboratories has confirmed the presence of Helium-3 (3He), an isotope of helium with applications that extend well beyond those of the more common Helium-4.

Helium-3's primary applications are in quantum computing, where its ability to reach temperatures lower than conventional Helium-4 allows for greater processing stability, and in advanced fusion energy research where it functions as a potential fuel. The current price point for Helium-3 is approximately $18.7 million per kilogram, a figure that reflects not a true market price but rather the cost of inter-agency government transfers since no commercial market for helium-3 currently exists.

CEO Thomas Abraham-James was measured in how he framed this development, noting that Helium-4 production remains the company's operational priority:

"The priority for us is to get the Helium-4 up and running and to get that into operation. The helium-3, I would look at that as very much the cherry on top of the cake and certainly something that we want to realise, but at the moment it is not the absolute priority of the company."

The commercial pathway for helium-3 requires additional technical work. Six separation processes are known at laboratory scale, none of which have been demonstrated commercially. The US Department of Energy has already begun funding companies to develop lunar Hhelium-3 extraction technology, a data point that frames the domestic alternative Topaz may represent.

Interview with Thomas Abraham-James, President & CEO of Pulsar Helium Inc.

Minnesota: Regulatory Certainty as a De-Risking Event

One of the less-discussed risks in resource development is the legislative and regulatory framework within which a project operates. For Pulsar Helium, operating in a state with no prior history of gas production meant that the regulatory environment had to be built from scratch. In 2024, Minnesota legislated that helium was a commodity subject to state regulation. In early June 2026, the associated operational regulations were finalized. This removes what had been a genuine area of uncertainty for the project's development timeline.

The state of Minnesota has created a regulatory pathway that did not previously exist doing so on the basis of work Pulsar has carried out at Topaz. Abraham-James described the significance directly:

"To get new legislation in purely on the back of the work that Pulsar has been doing in such a short period of time is quite phenomenal support and I think that also goes to highlight the non-hazardous nature of helium, the small footprint, but also just the overall requirement that the nation has for more sources of helium."

This mirrors a broader pattern visible across US resource development. For Pulsar, the completion of Minnesota's helium regulations represents the removal of a key non-geological risk.

US Partnerships and the Domestic Supply Chain

Pulsar has aligned itself with Chart Industries, a multi-billion-dollar company specializing in the engineering, design, and fabrication of industrial gas facilities, with particular expertise in cryogenic applications. Chart operates a major fabrication plant in Minnesota, close to the Topaz project site. The company is currently analyzing Topaz's gas composition and downhole data to begin designing a project-specific helium processing facility.

The company has also recently appointed a new president with an industrial gas background, strengthening the relationships with potential end users that will be central to the project's commercial development. Dialogue with US federal and state government bodies is ongoing.

The United States has the engineering expertise, the manufacturing capacity, and the supply chain required to build a helium production facility without recourse to offshore contractors. For a project explicitly positioned as a domestic supply solution, the alignment of the engineering partnership with the project's geographic and political rationale is commercially coherent.

Path to Production

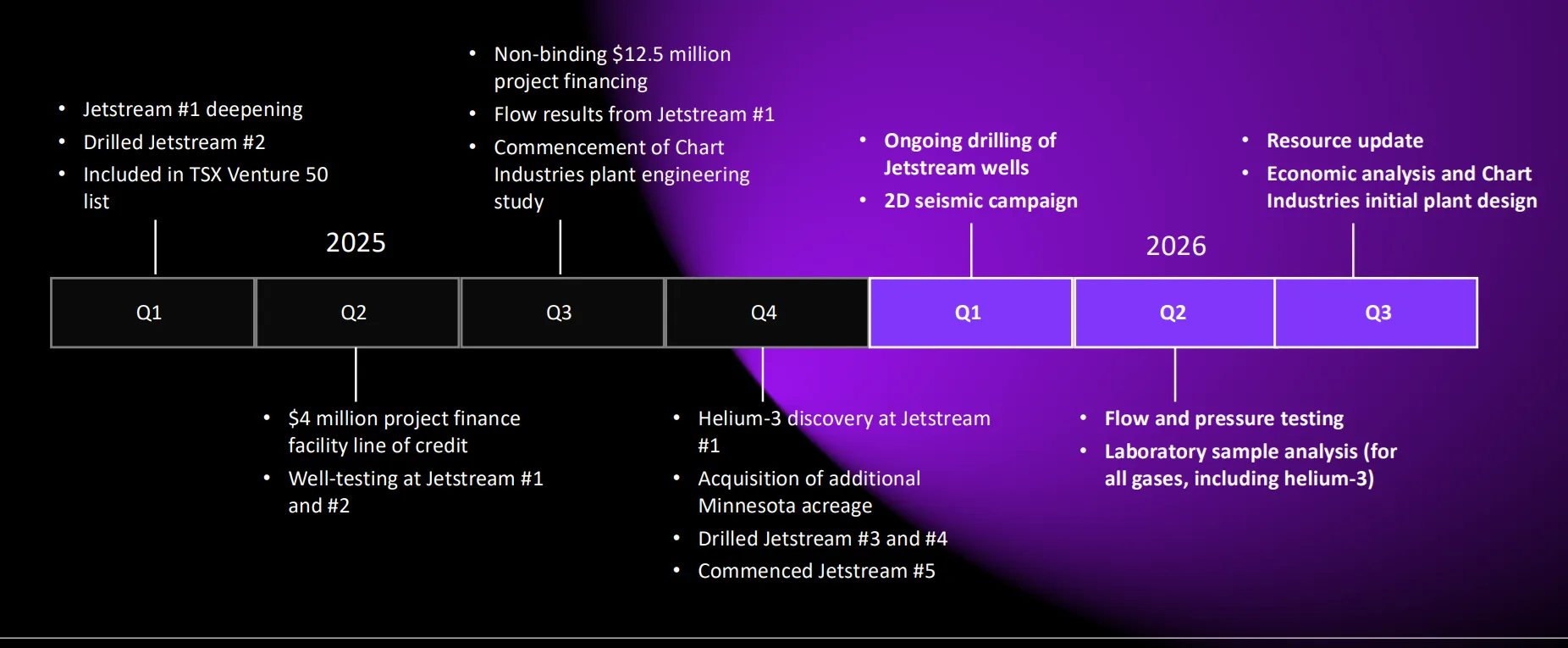

Pulsar Helium is planning to drill 2-4 additional production-ready wells beginning in September 2026. Unlike the five exploration wells recently completed, the production-ready wells can be directly incorporated into a processing facility and will provide the data required to build a meaningful production model. The results of that drilling programme, combined with the resource work being conducted by an independent US firm and the facility design work underway at Chart Industries, are intended to support a resource update and economic assessment that allows the company to enter 2027 with concrete production guidance.

The company has stated its intention that by 2027, the narrative will have shifted from exploration and derisking to potential production timelines and guidance.

The Investment Thesis for Pulsar Helium

- Primary resource in a byproduct world: At 8.1% average helium concentration, Topaz is economically viable as a standalone helium operation and not dependent on natural gas volumes or natural gas prices. This is a structural commercial advantage that fewer than a handful of projects globally can claim.

- Supply crisis is not short-term: With 45% of global supply offline and 3-5 years recovery timeline for the damaged production facilities, the supply deficit is not a transient event. Investors should assess Pulsar against a sustained period of elevated helium prices and rationed supply.

- US jurisdiction premium: Topaz is located in the United States, the world's largest helium consumer. Domestic production avoids the transit losses, shipping bottlenecks, and container integrity issues that affect imported liquid helium. It also benefits from the political and policy tailwind of the US government's formal designation of minerals as a national security priority.

- Regulatory derisking complete: Minnesota's finalization of helium regulations in 2026 removes a material non-geological risk that has weighed on the project's development timeline. The regulatory pathway to production now exists.

- Geological confidence: Seven wells drilled, seven gas encounters. The 100% success rate across a geographically diverse drill programme, stepping out in multiple directions over several miles, and provides meaningful confidence in the scale and continuity of the resource.

- Helium-3 optionality: The confirmed presence of Hhelium-3 at Topaz is not priced into any current economic assessment and represents potential additional value that cannot yet be quantified but that is strategically significant given the US government's investment in Helium-3 applications.

- Near-term catalysts: Production-ready well drilling commencing September 2026; independent resource update and Chart Industries facility design work expected to support an economic assessment targeting potential production guidance by 2027.

Macro Thematic Analysis

The global helium market is undergoing a structural dislocation that differs in important ways from typical commodity supply shocks. Helium cannot be synthesized at commercial scale. It cannot be substituted in its primary applications as semiconductor fabrication requires helium; MRI machines require liquid helium; space launch systems use helium as a pressurizing agent. And because more than 95% of global production is a byproduct of natural gas processing, supply cannot be increased in response to price signals the way it can in most commodity markets. When a major production node goes offline, the market has no self-correcting mechanism available at short notice.

With Qatar's infrastructure damaged, the Strait of Hormuz closed, and Russia's exports restricted, US customers are already reporting allocations of 50% of their typical orders and paying premiums on top of that. The semiconductor fabs in Taiwan, South Korea, and Japan that depend on helium appear to be absorbing a disproportionate share of available US supply, with domestic customers experiencing the shortfall.

This is the environment in which Pulsar Helium is advancing Topaz toward production. The broader policy context reinforces the commercial case. The US government's formal designation of critical minerals including helium as a national security priority reflects an awareness at the federal level that the existing supply chain is geopolitically fragile. The Department of Energy is already funding helium-3 extraction research. State-level frameworks, as demonstrated by Minnesota's 2026 regulations, are being built specifically to support domestic helium production.

As Abraham-James concluded the opportunity of helium:

"I would say that it is probably one of the most strategic commodities I've ever worked on in my life, and I think that its business case is only improving as technology advances."

For a company like Pulsar, holding a high-grade primary helium resource in the US at the moment that framework is being assembled, the thematic alignment is direct.

TL;DR

Pulsar Helium is developing a primary US helium resource grading 8.1%, more than 200 times the concentration of Qatar's operations, and at a moment when 45% of global supply has been knocked offline with a three-to-five-year recovery timeline. Seven wells drilled, seven gas encounters. Minnesota's helium regulations finalised June 2026. Chart Industries engaged for facility design. Helium-3 confirmed on site. Production-ready drilling starts September 2026, with an economic assessment and resource update to follow. The US government has formally designated helium a national security priority. The market for domestic supply has never been more urgent and Pulsar is the only listed primary helium developer in the United States advancing toward a production decision right now

Analyst's Notes

Subscribe to Our Channel

Stay Informed