Made In America | Revival Gold Targets Major Re-Rating as Mercur Moves Toward 2028 Construction

Revival Gold holds 6Moz of US gold at ~$30/oz with a clear path to 2028 construction - trading at a fraction of NAV in one of mining's most favourable jurisdictions.

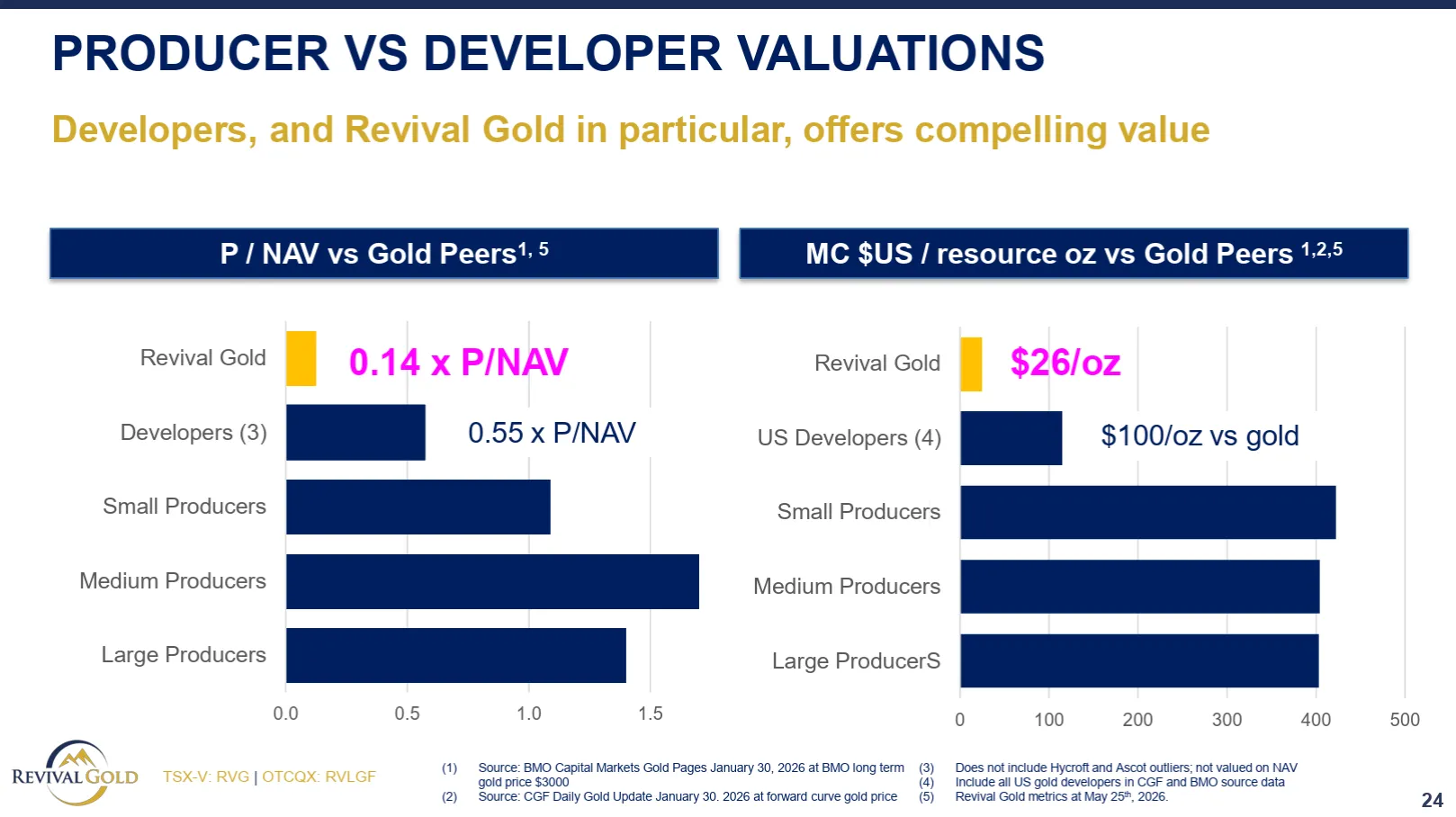

- Revival Gold is developing two US-based gold projects: Mercur in Utah and Beartrack-Arnett in Idaho, with a combined 6 million ounces of resource and approximately $1.3 billion in NAV against a current market cap of around $200 million USD.

- The Mercur project is the near-term production focus, targeting a preliminary feasibility study (PFS) by Q1 2027, a full feasibility study by end-2027, and a construction decision in early 2028, with projected free cash flow of $300–$350 million per year at current gold prices.

- The company is benefiting from significant regulatory tailwinds in the US, including 2023 amendments to the National Environmental Policy Act (NEPA), President Trump's "Unleashing American Energy" executive order, and a landmark 2025 Supreme Court decision clarifying NEPA as a procedural - not results-based - statute.

- Mercur is located on private land in Utah, placing permitting authority primarily at the state level under the Division of Oil, Gas, and Mining (DOGM), which significantly reduces federal permitting complexity and timeline risk.

- Management views Beartrack-Arnett as essentially unpriced in the current market cap, representing potential additional upside as exploration drilling extends the known mineralised structure at depth.

Made in America is a Crux Investor series profiling strategic and critical mineral developers with their primary asset or assets located within the United States. At a time when geopolitical risk, permitting reform, and domestic energy and mineral policies are reshaping where capital flows in junior mining, these are the companies built for this moment.

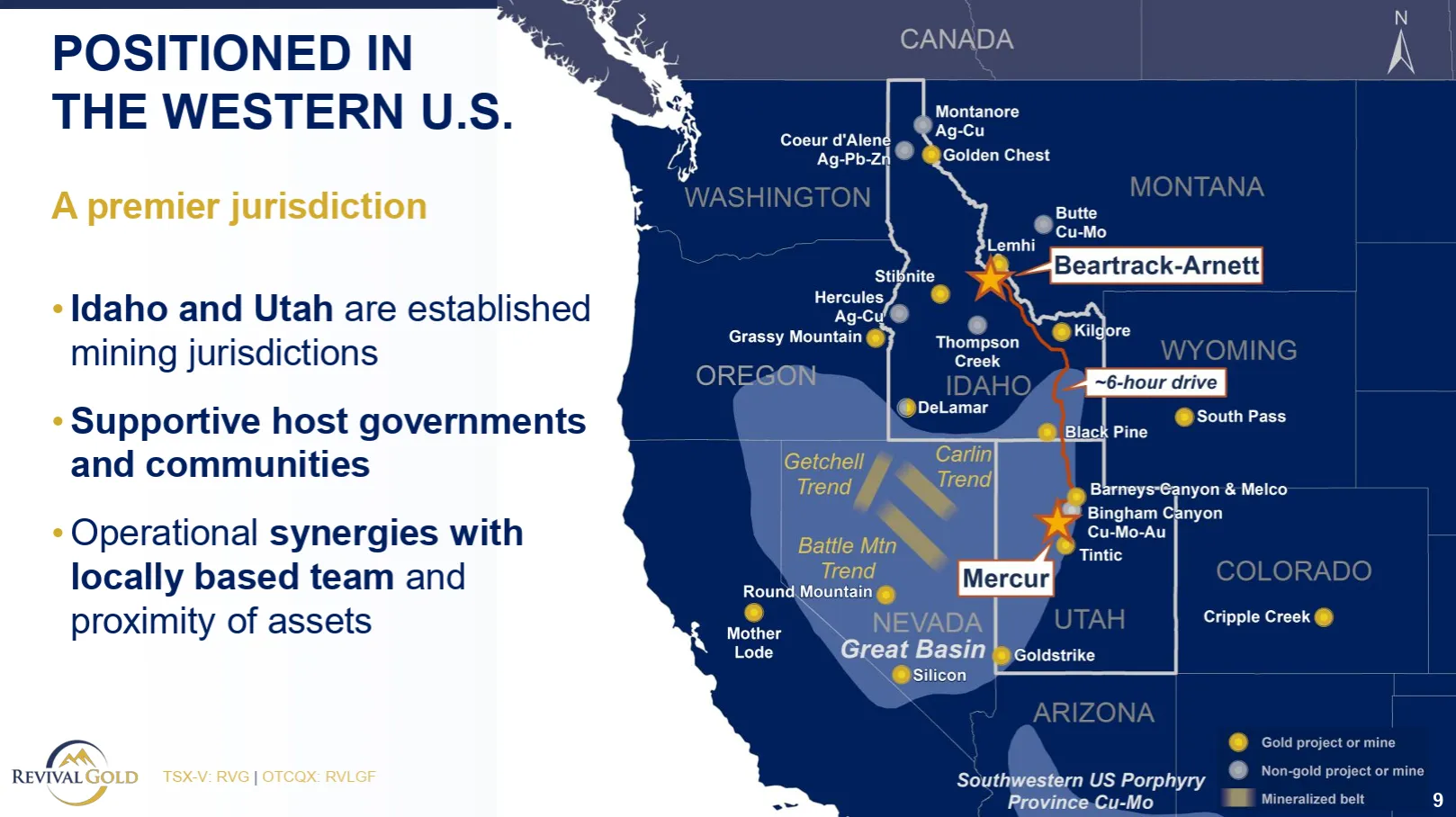

Utah and Idaho: Why These States Matter

Before examining the projects themselves, the jurisdictional context deserves its own treatment - because for a series defined by the American advantage in mining, not all US states are equal.

Utah is one of the most mining-friendly regulatory environments in the country. For projects situated predominantly on private land, the primary permitting authority is the Utah Division of Oil, Gas, and Mining (DOGM) - a state-level body with a long institutional history of working alongside large-scale extractive operations. Utah's mining heritage is deep: Bingham Canyon, operated by Rio Tinto's Kennecott subsidiary, is one of the largest open-pit copper-gold mines on earth, and has shaped a regulatory culture that understands what mine development looks like at scale. The proximity of Salt Lake City - a city of over 1.2 million people with an international airport, a university system, and an established industrial workforce - means that talent, logistics, and financial services infrastructure are all within reach. For a developer looking to compress timelines and manage costs, Utah's combination of private land permitting, institutional familiarity with mining, and urban infrastructure represents a genuinely rare package.

Idaho has its own distinct mining identity. The Silver Valley and Coeur d'Alene basin in the state's north are among the most historically productive silver and gold districts in North America, and Idaho's state-level mining statutes reflect a long co-existence between the regulatory framework and the resource sector. Beartrack-Arnett, Revival Gold's second project, sits on federal land, which introduces Forest Service engagement into the permitting process - a meaningful distinction from Mercur's state-led pathway. Management treats this difference explicitly: Beartrack-Arnett is the longer-horizon asset, and its federal land status is in part why it has not been elevated to primary development focus. That said, Idaho's mining heritage means the project exists within a state where resource development has political and cultural legitimacy that is not universally available across the US.

The contrast between the two projects - private land in Utah versus federal land in Idaho - is itself an instructive window into how Revival Gold has structured its development sequencing. Mercur first, with its shorter permitting pathway. Beartrack-Arnett as the optionality asset, carrying a completed preliminary feasibility study and active drilling, waiting for its moment.

The American Advantage: Jurisdiction, Permitting, and the Policy Shift

The regulatory environment for domestic US mining has changed materially in the past three years, and Revival Gold's project portfolio is positioned to benefit from every layer of that change.

At the state level, Mercur's location on predominantly private land in Utah means that the primary permitting authority is DOGM rather than federal agencies such as the Bureau of Land Management or the Forest Service. This is not a minor operational detail - it is a structural de-risking of the entire development timeline. Management reports a constructive working relationship with DOGM, and baseline study work for mine permitting is already underway, targeting completion by end-2027.

At the federal level, three developments have collectively produced what Debra Struhsacker, Revival Gold's Senior Adviser, describes as the most favourable US permitting environment in decades.

The first is the 2023 amendments to the National Environmental Policy Act (NEPA), which for the first time imposed statutory time limits on environmental assessments and environmental impact studies - a reform that had been sought by the mining industry for years and that directly addresses the primary mechanism by which permitting delays have historically been weaponised against resource projects.

The second is President Trump's "Unleashing American Energy" executive order, which explicitly classifies minerals alongside energy as a national security and economic priority, establishing a formal policy mandate for expedited permitting of domestic resource development.

The third - and arguably the most durable - is the 2025 US Supreme Court ruling in Seven County Infrastructure Coalition v. Eagle County, Colorado, which reaffirmed NEPA as a procedural statute rather than a results-based one, and granted federal agencies greater deference in project-specific permitting decisions. The practical effect is to significantly reduce the litigation surface area that has historically been used to stall mine permitting through the courts.

Struhsacker, who was formerly involved in permitting Kinross Gold's Buckhorn operation in Washington State, was direct about the significance of these changes and the market's failure to absorb them:

"Energy and mineral security are economic and national security. You can't have one without the other."

She added that what is happening at the state level at Mercur - a constructive, time-bound engagement with DOGM on private land - is exactly the kind of permitting pathway that the new federal framework is designed to support and replicate at scale. As more projects are permitted under the new framework, awareness and confidence among investors should increase. The investment community has not yet caught up.

Interview with Hugh Agro, President, & Debra Struhsacker, Senior Advisor

The Mercur Project: A Carlin-Type System in Utah

Mercur is Revival Gold's primary development asset. Located in Tooele County, Utah, the project sits on a 7,800-hectare land position and features a Carlin-type mineralisation system - the same geological framework that underpins some of North America's most productive gold mines, including Nevada's Goldstrike operation. The project area spans approximately 15 kilometres of strike in the main mineralised belt and benefits from proximity to significant geological neighbours, including Bingham Canyon, one of the world's largest copper-gold deposits.

The project has a brownfield character. Historical underground mining on the site dates to the 1800s and early 1900s, and Barrick Gold subsequently operated both a heap leach and a mill targeting sulphide horizons. Revival Gold acquired the asset through an option-earn agreement on terms suited to a junior, and has since consolidated the surrounding land package - including a neighbouring parcel formerly associated with Homestake Mining.

The first phase of development is an open-pit heap leach operation. At current gold prices, management projects the operation could generate $300 to $350 million in annual free cash flow. Drilling to date has been concentrated in the top 100 to 150 metres from surface, and Agro noted that Carlin-type systems are well-documented for their depth potential, pointing to high-grade discoveries at depth by companies such as Barrick at Cortez and Fourmile.

Infrastructure That Compresses the Timeline

A distinguishing feature of Mercur is its infrastructure profile. The site already has an energised power line, paved road access, and a confirmed water source - all significant de-risking elements ahead of a feasibility study. These are not incidental conveniences; in the context of a junior mining development, the absence of any one of them can add years and tens of millions of dollars to a project timeline.

The location compounds the advantage, as Agro notes:

"Location's key to the development of a project like Mercur. We're within 60 minutes of an international airport at Salt Lake City. We've got a town of 35,000 people less than half an hour away from us and that's a great source of staff for the project."

The project team is being assembled with a local-first approach that reflects this geography. Tim Barnett, the site-lead at Mercur, is a Utah resident who has managed 14 mine commissionings globally. The chief engineer, John Meyer, is a former Barrick professional based in Salt Lake City who is closely familiar with the region. This is not a management team parachuted in from elsewhere - it is a team embedded in the state where the project sits.

From Drill Results to a Construction Decision

Revival Gold's technical programme at Mercur is currently focused on the work required to advance to a preliminary feasibility study (PFS) by the end of Q1 2027. This includes approximately 18 kilometres of planned drilling in 2026, encompassing resource expansion, geotechnical work, and combination drilling. The company currently has two drill rigs operating at Mercur and anticipates a third shortly.

Metallurgical test work is also underway. Twenty columns are currently under leach, aimed at optimising the heap leach recovery plan. This work feeds directly into the engineering parameters of the PFS.

Following the PFS, the company intends to move into a full feasibility study before reaching a construction decision in early 2028.

Beartrack-Arnett: The Underappreciated Asset

Beartrack-Arnett in Idaho is Revival Gold's second project. It already carries a completed PFS and sits on existing infrastructure - a meaningful head start relative to most junior assets at a comparable stage. Unlike Mercur, however, Beartrack-Arnett involves federal land and therefore requires engagement with the Forest Service alongside state permitting processes. This is why it sits behind Mercur in the development queue, and why management treats it primarily as an optionality asset rather than an active development focus.

Management's view is that the project is currently unpriced in the company's market capitalisation - essentially a free call option for investors who buy the stock on the Mercur thesis.

Revival Gold is currently drilling one of its deepest holes to date at Beartrack-Arnett - approximately one kilometre downhole - to test the depth extension of a mineralised structure already confirmed over 5.5 kilometres of strike. Results are expected within months.

"I really don't think there's much if any value in our stock today reflected from the Beartrack-Arnett project in Idaho. And we see this as a huge opportunity for our investors."

Capital Markets and Valuation Context

Agro characterised the company's current valuation at approximately $30 per ounce of gold in the ground, compared to producing peers that trade at significantly higher multiples. He indicated that closing even a portion of that gap as de-risking milestones are achieved through the PFS and feasibility study could imply a doubling or tripling of the current per-ounce rating within six to eight months.

The company is exploring debt financing options as a component of its capital structure for the construction phase, and management noted that lenders are actively seeking credit opportunities in well-located, low-geopolitical-risk projects. Equity and debt-like capital interest in US-focused gold developers is described as unusually strong - reflecting both the gold price environment and strategic interest from senior and intermediate producers seeking to expand domestic US production.

Execution as the Core Risk

Agro was direct in acknowledging that the company will ultimately be judged on execution. The 2026 priorities are completion of the 18-kilometre Mercur drill programme, finalisation of metallurgical test work, and delivery of the PFS on schedule. The 2027 priorities are completion of the full feasibility study and mine permitting. The construction decision follows in early 2028.

"We have the projects, we have the team, we have the funding. Our focus for the next few months is going to be on driving that drilling that's required at Mercur to underpin the PFS."

The Investment Thesis for Revival Gold

- US jurisdiction premium: Operating solely in Utah and Idaho - two mining-friendly states with long institutional histories of large-scale resource development -provides a risk profile that is increasingly rare at the junior level and increasingly valued by institutional capital allocating away from geopolitical risk.

- Regulatory tailwind: The combination of NEPA amendments, the Trump administration's domestic minerals executive order, and the 2025 Supreme Court NEPA ruling represents the most favourable US permitting environment in decades - a structural advantage not yet fully reflected in junior mining valuations.

- Brownfield advantage: Existing infrastructure (power, roads, water), historical mining data, and a private land position at Mercur compress both the timeline and the capital requirement between current status and a construction-ready project.

- Valuation gap: The company is trading at approximately $30/oz in the ground against a peer group of producers at significantly higher multiples, creating the potential for a material re-rating as development milestones are achieved.

- Capital-efficient path to production: The phase-one open-pit heap leach approach at Mercur is designed to minimise upfront capital, with projected free cash flow of $300–$350 million per year at current gold prices once in production.

- Exploration upside at depth: Mercur's drilling has been concentrated in the top 100–150 metres; Carlin-type systems are known for their depth endowment, meaning the existing resource may represent a fraction of the system's total potential.

- Beartrack-Arnett optionality: With a completed PFS and active deep drilling underway in Idaho, this second asset is, in management's view, essentially unpriced in today's market cap - additional upside at no incremental cost to investors entering on the Mercur thesis.

Macro Thematic Analysis

The United States is experiencing a convergence of economic, geopolitical, and regulatory forces that are reshaping how capital is allocated toward domestic resource development - and the effects are only beginning to reach the junior mining sector.

Gold above $4,500 per ounce has materially improved project economics across the board. But the more durable shift is structural: the formal designation of minerals as a national security asset by the US federal government, backed by executive action, legislative reform, and now Supreme Court precedent, represents a policy reorientation with no clear parallel in recent decades. For the first time since the modern environmental movement reshaped the regulatory landscape in the 1970s, bipartisan political support, streamlined permitting, and genuine public appetite for domestic resource development are aligned.

There is a useful analogy in the CHIPS Act and the Inflation Reduction Act - pieces of legislation that redirected hundreds of billions of dollars of private capital toward domestic semiconductor and clean energy manufacturing by changing the risk/return calculus through policy. The shift in US mining permitting is less fiscally dramatic but operates through the same mechanism: reducing regulatory risk for onshore producers relative to offshore alternatives, and signalling to capital markets that domestic resource development is a policy priority, not a policy obstacle.

Revival Gold's two-project portfolio in Utah and Idaho sits directly in the path of this thematic. The company operates in mining-friendly states, on largely private land, with a brownfield asset base that reduces both timeline and capital risk. As Debra Struhsacker observed, the investment community has not yet fully absorbed the scale of the recent regulatory change - which suggests the thematic tailwind has further to run before it is priced.

TL;DR

Revival Gold offers investors exposure to 6 million ounces of US-based gold resource at approximately $30/oz - a fraction of producing-peer multiples - with a defined path to a construction decision by early 2028. The Mercur project in Utah benefits from brownfield infrastructure, private land permitting under DOGM, and a regulatory environment that has materially improved following 2023 NEPA amendments, the Trump administration's domestic minerals executive order, and a landmark 2025 Supreme Court ruling. Beartrack-Arnett in Idaho, carrying a completed PFS and hosting active deep drilling, is effectively unpriced in the current market cap - representing additional optionality at no incremental cost to investors today. Both projects sit in states with deep mining heritage and institutional frameworks built around resource development - a jurisdictional foundation that is rarer than it looks at the junior level, and increasingly valued by the capital that matters.

Analyst's Notes

Subscribe to Our Channel

Stay Informed