Indonesia's Crackdown on Illegal Tin Mining & the Structural Shock Reshaping Global Tin Supply

Indonesia’s crackdown on 1,000 illegal tin mines, plus disruptions in Myanmar and DRC, drives prices above $37,500/t amid supply crisis in critical tech metal.

- Indonesia's plan to shut down 1,000 illegal mines marks the most significant regulatory intervention in decades, potentially removing up to 80% of Bangka-Belitung's output from global tin supply.

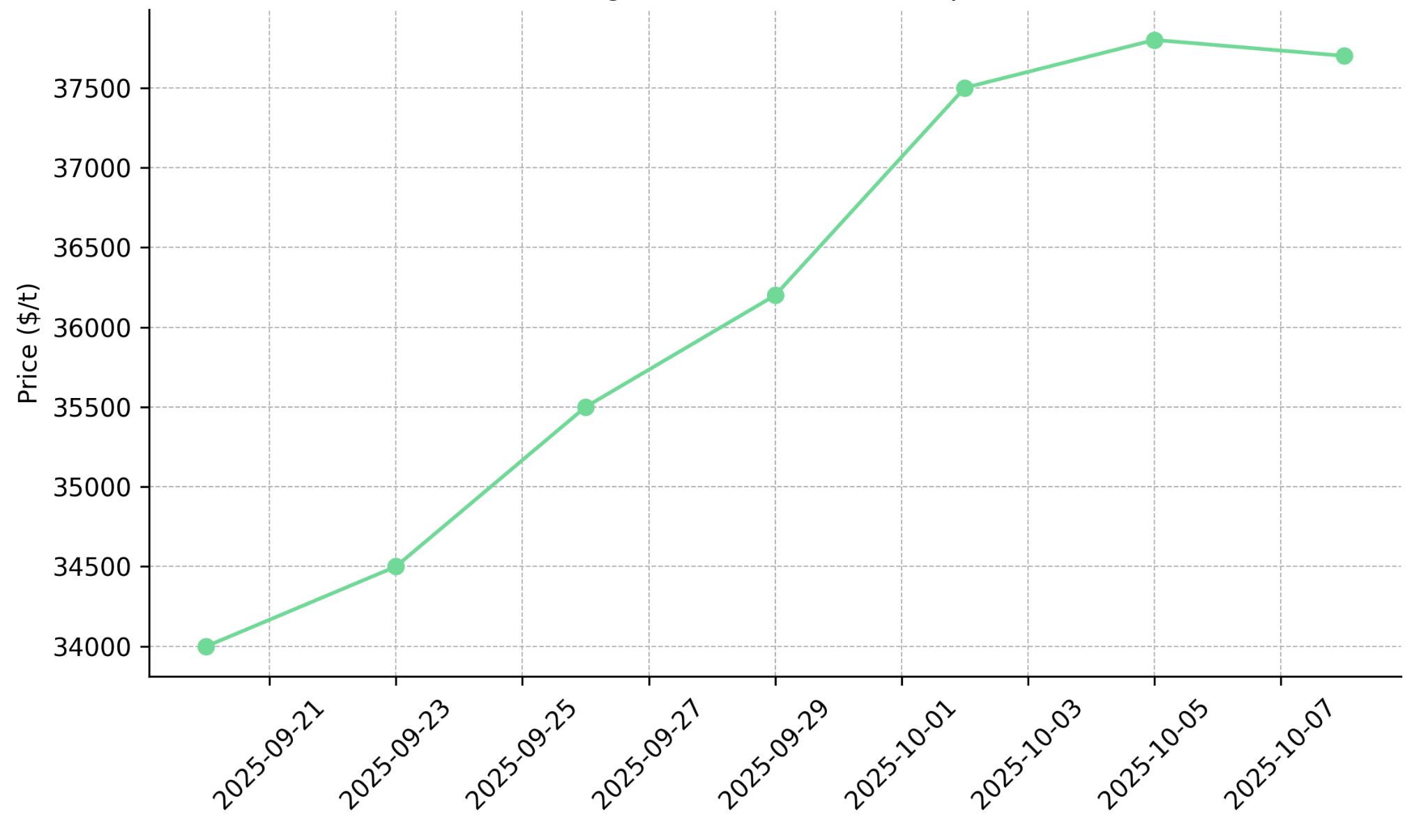

- Tin prices surged past $37,500/t in early October 2025, their highest level since April, as supply tightening flipped LME time-spreads into backwardation, signaling near-term scarcity.

- Supply disruptions extend beyond Indonesia: Myanmar's Man Maw mine remained offline as of October, and the DRC's North Kivu province continues to face security risks from M23 rebel activity.

- The crackdown highlights tin's geopolitical fragility, reinforcing its strategic role in electronics, EV batteries, and solar technologies amid accelerating energy transition demand.

- Rome Resources, an exploration-stage company operating in the DRC's tin belt near Alphamin's high-grade Mpama North mine, is working to capitalize on structural deficits through resource delineation in a proven mineralized corridor.

Indonesia's Sweeping Crackdown on Illegal Tin Mining

Indonesia, which accounted for the world's largest share of refined tin exports in recent years, has launched a sweeping regulatory intervention to curb illegal mining across its tin-producing islands of Bangka and Belitung. President Prabowo Subianto's announcement in late September 2025 to close 1,000 illegal mines marks a turning point for a sector long plagued by shadow production and blurred regulatory boundaries.

Historically, Indonesia's tin market liberalization in the late 1990s opened the door to uncontrolled small-scale mining. Over time, the line between official and informal producers eroded, with PT Timah (TINS.JK), the state-backed major, later accused of enabling black-market flows. Much of the country's tin originates from artisanal and small-scale miners, creating difficulty in distinguishing licensed operators from illegal ones. Some illegal operations consist of basic rafts deployed at night to dredge for tin in waters licensed to official sector operators, with the material then smuggled out on small boats.

The Indonesian Tin Exporters Association estimates that as much as 12,000 tonnes of tin are being illegally exported each year. Prabowo went further, stating that illegal operations may represent up to 80% of Bangka-Belitung's output, underscoring how deeply entrenched the issue has become. With PT Timah reporting a 32% year-on-year drop in ore production in the first half of 2025 due to competition from illegal miners, the government's crackdown not only aims to restore environmental control and tax compliance but also signals a new phase of market tightening that will likely reverberate across global tin supply chains.

The ongoing closure of illegal operations should in theory help the official sector lift production in compensation, although by how much and over what period remains highly uncertain. What is clear is that the regulatory intervention represents a fundamental shift in how Indonesia approaches tin sector governance after decades of increasingly loose oversight.

Market Mechanics: Prices Surge & Time-Spreads Signal Supply Stress

Following the crackdown announcement, London Metal Exchange three-month tin prices surged past $37,500/t in early October, the highest level since April, as traders priced in near-term supply shocks. The price reaction underscores the fragility of the tin supply chain, which remains dependent on a small number of large producers vulnerable to policy shifts and operational disruptions.

A key technical signal reinforced this tightening: the LME cash-to-three-month spread flipped from a $167 discount to a $105 premium, indicating acute scarcity and forced short covering. These backwardations are rare in tin markets and often mark periods of constrained physical availability, reflecting not just speculative positioning but genuine tightness in deliverable inventory.

Official export data validates the shift. Indonesia's refined tin exports plunged to a multi-year low of 46,000 tonnes in 2024, with the Indonesian Tin Exporters Association expecting only a modest rebound to 53,000 tonnes in 2025. Through the first three quarters of 2025, export volumes remained suppressed relative to historical norms. Such contraction represents meaningful tightening in a market where global annual refined tin demand typically ranges between 360,000 and 380,000 tonnes.

For investors, the significance is twofold: tight near-term supply has triggered immediate speculative inflows and elevated price volatility, while structural undersupply is forming as global inventories decline, threatening long-term cost inflation across semiconductor, solder, and EV sectors. The tin price surge of approximately 10% in late September and early October 2025 demonstrates that markets responded swiftly to the regulatory announcement and its implications for physical availability.

A Fragile Global Tin Supply Chain

Indonesia's crackdown is not an isolated event but part of a broader narrative of structural fragility within the global tin supply chain. Beyond regulatory intervention in Southeast Asia, two other major producing regions face persistent operational challenges that compound the market's supply vulnerability.

Myanmar: A Major Producer Still Offline

In Wa State, Myanmar, the Man Maw mine, once one of the world's largest tin producers, remained effectively offline as of October 2025, nearly two years after local authorities ordered a resource audit. While the mine has been described as preparing to reopen, the flow of tin raw materials over the border to China has remained minimal, suggesting the operation remains far from its pre-closure production rate.

Given Myanmar's complex political status and limited international oversight, a swift return to full production capacity appears unlikely. The extended absence of Man Maw from global supply chains has created a gap of tens of thousands of tonnes, contributing to the structural tightness now evident in LME pricing and inventory levels.

Congo: Persistent Instability in a Key Producing Region

In the Democratic Republic of Congo, tin production faces recurring disruption from regional conflict. Alphamin's Mpama North operation in North Kivu temporarily suspended activities in March 2025 due to M23 rebel activity in the region, though the company subsequently resumed operations. However, the security situation remains fluid. In a September 2025 CNN interview, one M23 leader adopted an uncompromising stance, and ongoing efforts by the United States to mediate the decades-old conflict in eastern Congo have yet to produce lasting stability.

These geopolitical disruptions emphasize a recurring theme: tin's geographic concentration risk. A handful of regions, Indonesia, Myanmar, and the DRC, account for most global output, meaning that localized shocks have outsized market consequences. As tin plays an increasingly critical role in the energy transition, from EV battery connectors to photovoltaic cell solder, the market's dependence on politically volatile jurisdictions could amplify volatility in future price cycles.

Tin's Strategic Role in the Energy Transition

Tin's demand profile is transforming. Once viewed primarily as a soldering metal for electronics, it is now categorized by institutions including the International Tin Association as a critical enabler of modern technologies. Its applications span semiconductors, EV batteries, and renewable energy infrastructure, where soldering, coating, and energy storage functions are indispensable.

The International Energy Agency projects global tin demand to rise sharply as green technologies scale, creating a structural imbalance against constrained mine supply. With few major development-stage projects in the pipeline, long-term supply forecasts point toward widening deficits through the end of the decade. This gap highlights why exploration-stage companies with access to high-grade, scalable deposits are increasingly viewed as strategic assets within diversified critical mineral portfolios.

The recent price surge reflects not just immediate supply shocks but a longer-term realization that tin's role in electrification and digitalization requires more reliable sourcing. As governments and manufacturers seek to secure critical mineral supplies, the premium placed on jurisdictionally stable, high-grade deposits continues to rise.

Emerging Opportunities: Frontier Exploration in the DRC's Tin Belt

Exploration-stage miner Rome Resources is advancing two tin projects, Mont Agoma and Kalayi, in the DRC's North Kivu province, operating in the same geological belt as Alphamin's high-grade Mpama North mine. Situated approximately 8 kilometers from Alphamin's operation, Rome's licenses lie within a proven mineralized corridor where decades of artisanal mining have demonstrated extensive tin, copper, and zinc mineralization.

Drilling conducted through 2024 and into 2025 intersected 12.5 meters at 1.06% tin, including higher-grade zones reaching up to 11.7% tin, providing geological validation for the district's exploration potential and demonstrating continuity with the broader tin system. The proximity to Alphamin's successful operation offers geological confidence, though it should be noted that Rome Resources and Alphamin operate as independent entities.

Rome Resources Chief Executive Officer Paul Barrett emphasized the comparability to Alphamin's geological setting:

"Clearly we are behind them because they're producing, but it's going to be a very similar story following through."

Resource Delineation Strategy

Operating in the DRC's relatively low-cost mining environment, Rome Resources is leveraging its experienced management team, led by Mark Gasson and advised by Klaus Eckhof, to delineate sufficient tonnage and grade to support future economic studies. The company's drilling campaign, which resumed following the March 2025 M23-related pause, continues to test high-grade extensions and parallel structures that could expand the resource base.

With artisanal mining confirming widespread mineralization across the license area, Rome Resources is systematically converting geological potential into drillable targets. The company is working toward defining a maiden mineral resource estimate, with ongoing drilling aimed at establishing the scale and continuity of mineralization required for project advancement.

Strategic Context Amid Supply Constraints

In the current macro environment, Rome Resources represents the type of high-grade exposure increasingly sought by investors looking to access tin supply growth outside the handful of established producing regions. With tin prices supported by both short-term scarcity and long-term structural demand trends, exploration-stage assets in proven geological belts offer potential leverage to sustained price strength.

The growing international interest in DRC critical minerals further validates the strategic positioning. Barrett noted a shift in institutional sentiment:

"I went to see the IRH guys in Abu Dhabi in December and they said “DRC, we're not bought into it yet”, but clearly they are now, and I think the US is getting involved as well. It's all positive actually for DRC critical minerals."

This sentiment shift reflects growing institutional interest in DRC critical minerals despite ongoing security challenges. While experienced operators like Alphamin have maintained production through periods of regional stability, the M23 situation remains fluid, and investors should carefully assess security risks alongside geological potential when evaluating frontier exploration assets.

Market Implications: From Policy Shifts to Investment Repricing

The cumulative effect of Indonesia's crackdown, Myanmar's production hiatus, and recurring disruptions in the DRC points toward a repricing of tin assets across the value chain. Investors are beginning to reassess the risk premiums embedded in tin equities, particularly those with high-grade exposure or demonstrated operational continuity.

With backwardation signaling near-term tightness and institutional buyers seeking long-term supply security, tin is emerging as one of the few metals simultaneously benefiting from both defensive and growth-driven demand. The metal's dual role, as a critical input for existing electronics manufacturing and as an enabler of future energy infrastructure, creates demand stability even amid macroeconomic uncertainty.

Equities aligned with reliable production or high-grade exploration potential in established tin districts may gain investor attention as the market recalibrates supply expectations. The sharp price reaction to Indonesian policy changes demonstrates how quickly capital can reprice scarcity, particularly in markets where supply concentration creates limited alternatives for end-users.

The Investment Thesis for Tin

- Regulatory tightening in Indonesia potentially removes a significant portion of shadow production, reinforcing long-term supply discipline and supporting higher equilibrium prices while reducing the structural oversupply that has periodically depressed market fundamentals.

- Persistent geopolitical risk in Myanmar and the DRC amplifies tin's scarcity premium, highlighting the value of diversified sources while demonstrating that operational disruptions in any major producing region can trigger immediate price responses and sustained volatility.

- Energy transition tailwinds, including EV, solar, and semiconductor growth, are expanding tin's strategic relevance within critical mineral portfolios as governments and manufacturers recognize the metal's indispensable role in electrification infrastructure.

- Exploration-stage assets in proven geological belts, such as Rome Resources' position in the DRC tin corridor, offers exposure to structural undersupply and regional geological continuity with established high-grade deposits, providing potential upside as scarcity premiums increase.

- Macro positioning reflects tin's combination of constrained supply and expanding demand, differentiating it from other base metals and warranting investor attention as inventories tighten and prices stabilize above $30,000/t with potential upside driven by both physical scarcity and strategic inventory building.

Tin's Rebound & Strategic Opportunity

The Indonesian crackdown exposes the fragile underpinnings of the global tin market, where a small number of mines and producing regions determine the fate of supply chains critical to modern technology. While regulatory tightening introduces near-term volatility, it may ultimately support a more transparent market structure that reduces the distortions created by decades of unregulated production.

For investors, this environment may favor companies capable of delivering credible grade, scalability, and operational continuity, attributes exemplified by Rome Resources' position in the DRC tin belt. The company's location within the same geological corridor as Alphamin's high-grade Mpama North mine, combined with drilling results demonstrating tin mineralization and an experienced management team, positions it to potentially benefit from the structural scarcity now evident across global tin markets.

As tin reasserts itself as a strategic enabler of electrification and digitalization, the current price strength reflects more than cyclical factors: it signals recognition that abundant, easily accessible tin supply is contracting, and the search for reliable new sources has intensified. The combination of regulatory reform in Indonesia, persistent disruptions in Myanmar, and ongoing security challenges in the DRC creates a supply environment where high-grade discoveries in proven geological districts may command increasing strategic value. For investors seeking exposure to this structural shift, exploration-stage assets with demonstrated mineralization and geological continuity to existing producers represent a potential avenue to capture upside from tin's evolving scarcity premium.

TL;DR

Indonesia’s unprecedented move to shut down 1,000 illegal tin mines represents the most significant regulatory intervention in decades, potentially removing up to 80% of Bangka-Belitung’s output from global supply. Combined with Myanmar’s Man Maw mine remaining offline and ongoing M23 rebel activity disrupting DRC production, tin prices have surged past $37,500/t, the highest since April 2025. The crackdown exposes critical vulnerabilities in global tin supply chains just as demand accelerates for semiconductors, EV batteries, and solar technologies. With LME time-spreads flipping into backwardation signaling acute scarcity, the structural deficit positions high-grade explorers in proven geological belts to benefit from long-term supply constraints and rising strategic premiums.

FAQs (AI Generated)

President Prabowo Subianto announced the closure of 1,000 illegal mines to restore environmental control, tax compliance, and support the struggling official sector after PT Timah reported a 32% production drop due to competition from illegal operators.

Up to 80% of Bangka-Belitung’s output may be affected, with an estimated 12,000 tonnes of tin illegally exported annually, creating significant supply tightening in a market where global demand ranges between 360,000-380,000 tonnes.

Myanmar’s Man Maw mine has been offline since late 2023, and the DRC faces recurring disruptions from M23 rebel activity in North Kivu province, where Alphamin temporarily suspended operations in March 2025.

Tin is essential for soldering in semiconductors, EV battery connectors, and photovoltaic cells in solar panels, making it indispensable for electrification and renewable energy infrastructure as demand accelerates.

Prices surged past $37,500/t in early October 2025, with LME spreads flipping into backwardation, a rare signal of acute scarcity, as markets price in both near-term shocks and long-term structural deficits.

Analyst's Notes

Subscribe to Our Channel

Stay Informed