China’s Rare Earth Export Controls and the Repricing of Supply Chains: What It Means for Western Producers and Investors

China's Nov 2025 rare earth export controls will restrict key processing equipment and heavy elements, disrupting global supply chains and accelerating Western localization.

- China's November 2025 export controls on rare earth processing equipment and heavy rare earth elements mark a major escalation in critical minerals geopolitics, disrupting global supply security.

- The new measures restrict the export of key machinery and heavy rare earth elements including holmium, erbium, thulium, europium, and ytterbium, potentially creating multi-quarter supply bottlenecks and tighter downstream markets.

- The policy underscores systemic risk for magnet supply chains, intensifying the Western push to localize separation, recycling, and refining capacity.

- Companies positioned in jurisdictions with supportive critical mineral frameworks, notably the United States, United Kingdom, Canada, Namibia, and Angola, stand to gain strategic premium and accelerated funding access.

- The rare earth element sector enters a new bifurcated phase with constrained Chinese exports on one side and rising Western industrial policy support on the other, redefining valuations across the rare earth element value chain.

The Policy Shift: China's November 2025 Export Controls

On October 9, 2025, China's Ministry of Commerce and the General Administration of Customs jointly announced new export control measures targeting rare earth elements, lithium batteries, and diamond technologies. These controls became effective November 8, 2025, and are enforced under China's Export Control Law, citing national security and non-proliferation commitments.

This marks Beijing's most comprehensive rare earth element-related policy since the 2010 quotas that triggered a World Trade Organization dispute. The new measures restrict not only raw materials but also core processing and separation equipment, a move designed to prevent technological leakage and preserve China's dominance in the rare earth element value chain.

The policy reflects a strategic shift from volume control to capability control, targeting centrifuges, vacuum furnaces, extraction tanks, and rare earth separation systems under export codes 2B902 and 1C914. The consequence is immediate. The West faces a structural deficit in midstream refining technology, prompting renewed urgency for domestic processing investments and technology transfer partnerships. Mark Chalmers, Chief Executive Officer of Energy Fuels, frames the rare earth urgency:

"If the United States wants to reshore the ability to be independent of China particularly on rare earth or reduce dependency on Russia we have a facility in the United States that's constructed permitting operating to do that."

From Trade Measures to Scarcity: Understanding What's Controlled

Unlike prior restrictions limited to oxide exports, the new controls extend to machinery essential for rare earth element separation, purification, and alloy production. Separation and purification equipment now subject to export licenses includes centrifugal extraction equipment, extraction tanks with mixing chamber volumes between 0.5 and 14.2 cubic meters, and intelligent continuous impurity removal and precipitation equipment for ion-adsorption rare earth ores with daily leaching solution processing capacity equal to or exceeding 5,000 cubic meters.

Metal production equipment under control encompasses specific equipment and electrolytic cells for rare earth metal electrolysis, vacuum induction reduction furnaces, and vacuum carbon tube furnaces. Permanent magnet equipment essential for high-performance magnets includes rare earth permanent magnet vacuum induction strip casting furnaces, hydrogen decrepitation furnaces, airflow mills, specialized forming presses, automatic hot pressing equipment, and vacuum sintering furnaces with cooling times equal to or less than 20 minutes and heating temperatures between 500 and 1,200 degrees Celsius.

The inclusion of heavy rare earth element compounds, holmium, erbium, thulium, europium, and ytterbium, signals Beijing's intent to defend its dominance in high-coercivity magnet alloys used in electric vehicle motors, turbines, and defense electronics. Each technical item translates to a bottleneck risk for Western supply chains. Without equivalent machinery, even mined concentrate cannot progress into value-added oxides or metals, prolonging the midstream dependency on China.

Paul Atherley, Chairman of Pensana Plc, underscored the complexity of the separation challenge in April 2025:

"The next step in the process is the tricky one, called separation. And typically we'll have sort of 27 steps to take to produce a range of products… We are now in discussions with parties who have got separation capacity ex-china and that would be a very important step to create the non-Chinese supply chain."

Western Supply Chain Realignment Accelerates

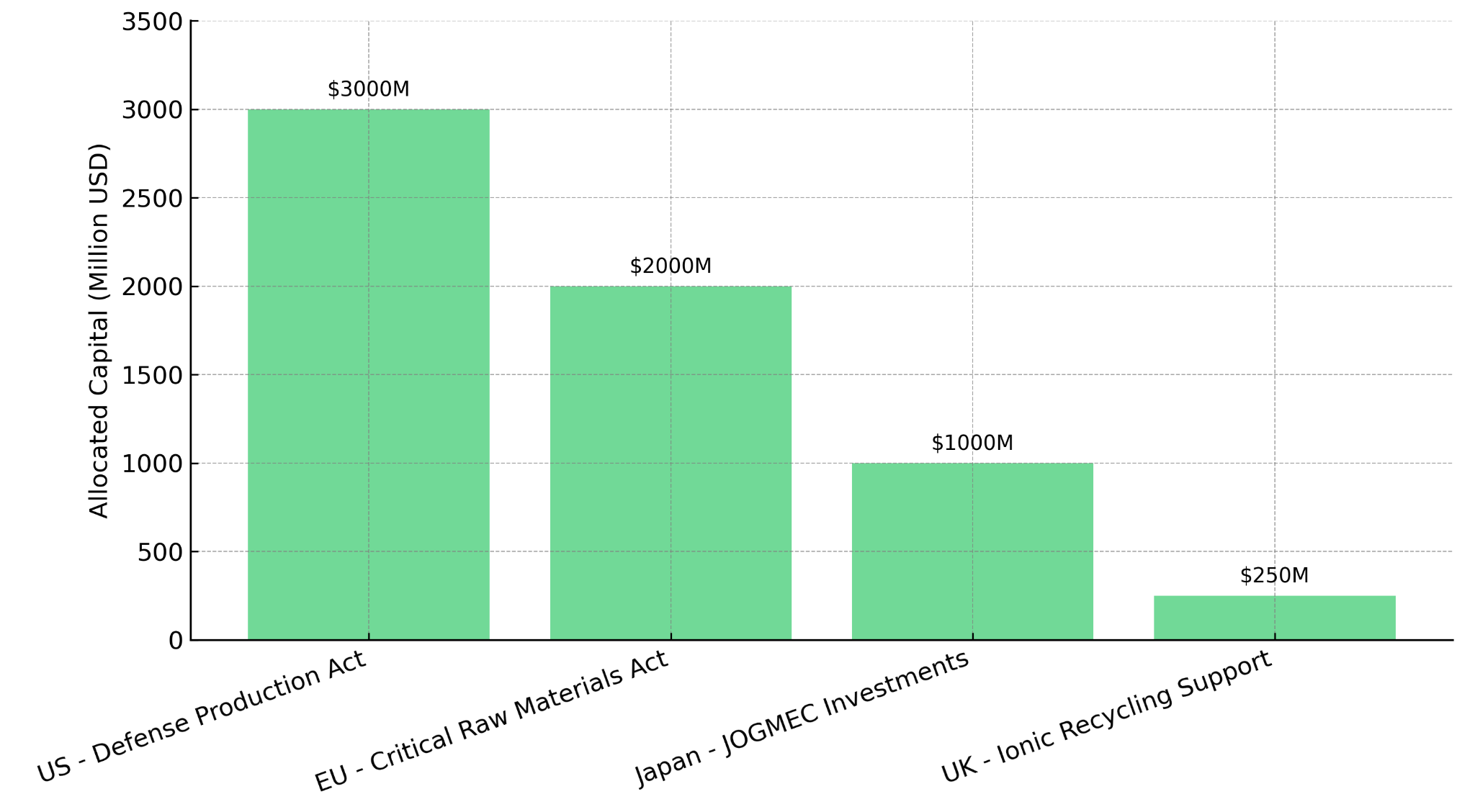

The export controls arrive amid unprecedented policy convergence across the United States, European Union, and allied jurisdictions. Each bloc is advancing legislative and fiscal mechanisms to derisk strategic mineral dependency. The United States Inflation Reduction Act and Defense Production Act have earmarked billions for rare earth element separation and magnet production. The European Union Critical Raw Materials Act mandates 15 percent domestic processing of strategic materials by 2030. The United Kingdom Critical Minerals Strategy supports domestic recycling and refining projects.

The result is an arms race to rebuild the rare earth midstream, where project timelines and technical partnerships now define valuation multiples. Ucore Rare Metals is advancing proprietary separation technologies to reduce Chinese dependency, targeting mid-2026 production at its Stage 1 Louisiana facility with support from United States government funding under the Defense Production Act.

Pat Ryan, Chairman and Chief Executive Officer of Ucore Rare Metals, highlighted the technological imperative in August 2025:

"We’re working on refining and processing that's currently 95 percent controlled by China. We're looking to bring it back to the western world."

Ionic Rare Earths leverages recycling and low-capex modular design to create parallel Western supply through its United Kingdom-based Ionic Technologies subsidiary, which achieved commercial-scale production of separated magnet rare earth oxides from recycled materials. Tim Harrison, Managing Director of Ionic Rare Earths, noted the policy-driven market bifurcation in September 2025:

"In the last 4 months since those export restrictions have been put in place we've been inundated on requests access to the dysprosium and terbium that we've been producing in our demonstration plant in Belfast and selling material now for example dysprosium at three times the price of Chinese quoted prices in Europe so there is appetite for this material and there is a bifurcation on pricing."

These represent early beneficiaries of the policy-driven localization premium now reshaping the rare earth element investment narrative.

Supply Disruption Mechanics & Market Tightness Outlook

Under China's new licensing regime, all exporters must declare rare earth element-related products as Dual-Use Items and obtain special permits. Customs can question the completeness, accuracy, and authenticity of declared information, and goods will not be released during the questioning period. This creates weeks-to-months delivery friction.

Analysts expect the pattern seen in graphite exports, where shipment volumes dropped 60 percent in the first quarter post-controls, to repeat in rare earth elements. The result is a temporary supply vacuum in heavy rare earth element markets. As Western separation facilities advance through 2026 and 2027, midstream capacity may offset part of the shortfall. However, investors should expect price volatility in dysprosium and terbium oxides through 2026, with premiums favoring Western-aligned supply.

The United States Department of Defense's recent establishment of a floor price of $110 per kilogram for neodymium-praseodymium in its agreement with MP Materials, representing a 70 percent premium to previous spot prices, has triggered corresponding price momentum in heavy rare earth elements. This floor pricing mechanism signals government willingness to absorb premium costs to secure non-Chinese supply.

Positioning Within the New Rare Earth Element Order

Energy Fuels restarted operations at the White Mesa Mill in Utah in early October 2025, the only fully licensed and operating conventional uranium processing facility in the United States with rare earth element separation capabilities. The company's dual uranium-rare earth element model diversifies revenue and hedges against commodity cyclicality. Shortly before October 9, 2025, Energy Fuels completed an oversubscribed $700 million convertible financing with Goldman Sachs as sole bookrunner, strengthening its balance sheet to advance both uranium and rare earth element production. As of June 30, 2025, the company reported zero debt and working capital of $253 million.

Ionic Rare Earths employs a dual-platform strategy through the Makuutu Project in Uganda and Ionic Technologies in the United Kingdom. The Belfast recycling facility achieved commercial-scale production and is recognized as the first Western producer of recycled, separated magnet rare earth oxides, distinguishing itself from other recyclers that produce powder alloys or mixed rare earth oxides requiring additional processing. The company completed a feasibility study in 2024 showing NPV of $502 million United States dollars, internal rate of return of 43.6 percent, and payback within 2.4 years. With modular buildout and magnet recycling scalability, Ionic offers exposure to low-capex, high-return processing aligned with European Union circular economy mandates.

Namibia Critical Metals has formed a joint venture with the Japan Organization for Metals and Energy Security, the Japanese government's resource security agency with an annual budget exceeding $10 billion United States dollars and a mandate to secure supply of natural resources for Japanese industry. The Japan Organization for Metals and Energy Security is earning up to 50 percent interest in the Lofdal heavy rare earth project and has currently earned 40 percent by spending approximately $17 million of the required $20 million Canadian dollars. The Pre-Feasibility Study, expected by the end of 2025, is fully funded by the remaining balance.

Darrin Campbell, President of Namibia Critical Metals, quantified the heavies’ significance in July 2025:

"Dysprosium currently sells at around $250 per kilogram and terbium trades at over $1,000 a kilogram so a multiple of value of the neodymium-praseodymium and the problem with these heavies is that there's just not very many of them economically found."

Campbell emphasized the urgency driving investment:

"There's definitely a renewed interest and focus and urgency on securing supply of heavy rare earth elements with the recent developments with China and the US over the last 5 months."

Pensana is advancing toward becoming a significant rare earth producer serving European markets, supported by the Angolan government and European Union strategic mineral policy frameworks. The company secured a conditional financing package in April 2025 led by the Angolan sovereign wealth fund, ABSA Bank, and the African Finance Corporation, structured with debt and equity components. As of October 2025, Pensana was mobilizing for construction at the Longonjo site in Angola and expected to begin drawing down the equity component of the financing shortly, targeting construction completion by the end of 2026 with full production well into 2027 following a six-month commissioning period.

Ucore Rare Metals is preparing for commercial deployment of its refinery facility in central Louisiana, located within a foreign trade zone. The company validated its proprietary Rapid SX technology through a commercial demonstration plant in Kingston, Ontario, operating for nearly 6,000 hours. Ucore received two grants from the United States Department of Defense totaling $22.4 million, an initial $4 million for technology validation and a subsequent $18.4 million for commercial deployment. The company raised $15.5 million Canadian dollars in October 2025 and is targeting Stage 1 production of 2,000 to 2,500 tons per annum of rare earth oxides by mid-2026.

Policy Alignment & Capital Allocation Shifts

The fragmented geopolitical supply chain has forced institutional capital to reprioritize jurisdictional safety over short-term cost advantages. Capital now flows toward projects with sovereign support, environmental, social, and governance validation, and midstream processing control. This reallocation dynamic parallels past cycles in uranium and lithium, where policy alignment became the strongest valuation catalyst.

Recent policy developments through 2025 underscore this capital reorientation. The United States government's establishment of floor pricing for neodymium-praseodymium and active funding of domestic processing facilities through the Defense Production Act demonstrates commitment to absorbing premium costs for supply security. The European Union's Critical Raw Materials Act mandate that 25 percent of rare earth supply come from recycling by 2030 creates regulatory tailwinds for companies like Ionic Rare Earths. Strategic partnerships such as the Japan Organization for Metals and Energy Security's heavy rare earth supply agreements signal international coordination to diversify away from Chinese dependency.

This represents an inflection point. Rare earth element equities will increasingly trade not just on grade or tonnage, but on policy leverage and supply chain integration, the new valuation metrics of critical mineral security.

The Investment Thesis for Rare Earth Elements

- China's export controls institutionalize midstream scarcity, particularly for heavy rare earth elements critical to electric vehicles and defense technologies, creating structural supply constraints that Western policy frameworks are attempting to address through significant capital deployment.

- Western government incentives including the Inflation Reduction Act, Critical Raw Materials Act, and Defense Production Act materially derisk domestic producers through direct funding, offtake agreements with floor pricing, and regulatory support, fundamentally altering project economics and supporting valuation multiples across compliant developers.

- Companies with multi-commodity exposure, such as Energy Fuels combining uranium and rare earth elements within integrated processing infrastructure, offer downside protection amid commodity volatility while maintaining exposure to policy-driven demand across multiple critical mineral categories.

- Recycling and proprietary separation technologies deployed by companies like Ionic Rare Earths and Ucore Rare Metals provide scalable, lower-capex entry points into constrained markets, with circular economy alignment offering additional regulatory advantages in European Union and United Kingdom jurisdictions.

- Projects advancing in the United States, United Kingdom, Namibia, and Angola benefit from demonstrated political alignment with resource security initiatives through 2025, including direct government funding, strategic partnerships with state agencies like the Japan Organization for Metals and Energy Security, and inclusion in critical mineral policy frameworks.

- Development timelines aligned with the 2026 to 2027 Western capacity buildout phase position near-term producers to capture premium pricing during the transition period, with heavy rare earth elements commanding prices three to four times Chinese quoted prices in non-Chinese markets as of late 2025.

- Jurisdictions demonstrating recent regulatory progress and permitting transparency reduce execution risk, with companies achieving major regulatory approvals, securing project financing, and advancing toward construction representing lower-risk exposure within the broader rare earth element development universe.

- Operational strategies incorporating government offtake agreements, floor pricing mechanisms, and strategic partnerships with end-users provide revenue visibility and downside protection during volatile commodity price environments, particularly important given the bifurcated pricing structure emerging between Chinese and non-Chinese supply chains.

The Reordering of Global Rare Earth Element Supply

China's November 2025 export controls formalize a new phase of global mineral realignment, one defined less by market economics and more by policy leverage. As processing technology becomes the critical chokepoint, investors must assess projects not only by grade and scale but by their role in the emerging non-Chinese ecosystem.

The rare earth element sector's valuation will increasingly reflect strategic autonomy premiums, mirroring dynamics already evident in uranium and battery metals. The United States Department of Defense's willingness to establish floor pricing 70 percent above market rates, combined with multi-billion dollar funding commitments across separation technology and processing infrastructure, signals that Western governments view rare earth element supply security as a national security imperative warranting significant fiscal support.

Geopolitical control of processing technology and midstream capacity equals control of value, and the companies securing government partnerships, achieving production milestones, and advancing separation capabilities through 2026 and 2027 will capture disproportionate upside as the bifurcated supply chain architecture solidifies.

TL;DR

China's November 2025 export controls on rare earth processing equipment and heavy elements represent a strategic shift from volume control to capability control, restricting centrifuges, vacuum furnaces, and separation systems essential for magnet production. This creates immediate supply bottlenecks for holmium, erbium, thulium, europium, and ytterbium, critical for electric vehicles and defense electronics. Western governments are responding with unprecedented policy support through the Inflation Reduction Act, EU Critical Raw Materials Act, and Defense Production Act, establishing floor pricing 70% above market rates and funding domestic separation facilities. Companies positioned in the US, UK, Canada, Namibia, and Angola with midstream processing capabilities are capturing premium valuations as the sector bifurcates into Chinese and non-Chinese supply chains, with heavy rare earths commanding 3-4x Chinese prices in Western markets.

FAQs (AI-Generated)

China restricted exports of rare earth processing equipment (centrifuges, vacuum furnaces, extraction tanks, separation systems) and heavy rare earth element compounds including holmium, erbium, thulium, europium, and ytterbium. This extends beyond raw materials to target the machinery essential for separation, purification, and magnet production.

Heavy rare earth elements are critical for high-performance permanent magnets used in electric vehicle motors, wind turbines, and defense electronics. They enable high-coercivity magnet alloys that maintain strength at extreme temperatures. Currently, 99-100% of commercial dysprosium and terbium supply comes from China.

The US, EU, and allied nations are deploying multi-billion dollar funding through the Inflation Reduction Act, Critical Raw Materials Act, and Defense Production Act. The US Department of Defense established floor pricing at $110/kg for neodymium-praseodymium (70% premium), while directly funding domestic separation facilities and processing infrastructure.

Companies with operational processing capabilities in Western jurisdictions, including Energy Fuels (US separation facility), Ionic Rare Earths (UK recycling plant producing separated oxides), Ucore Rare Metals (Louisiana refinery targeting mid-2026 production), Namibia Critical Metals (Japan partnership), and Pensana (Angola project with EU alignment).

As of late 2025, dysprosium and terbium from non-Chinese sources are commanding 3-4x the Chinese quoted prices in European and Western markets. This bifurcated pricing structure reflects supply security concerns and government willingness to pay premiums for strategic autonomy in critical mineral supply chains.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed