Tin Prices Under Pressure as Myanmar Resumes Exports: Structural Tightness Remains

Myanmar tin exports resume but structural supply deficits persist. DRC emerges as strategic alternative with companies like Rome Resources near high-grade producer Alphamin.

- Tin shipments have resumed from Myanmar’s Wa State after a two-year suspension, introducing short-term downside pressure on global tin prices.

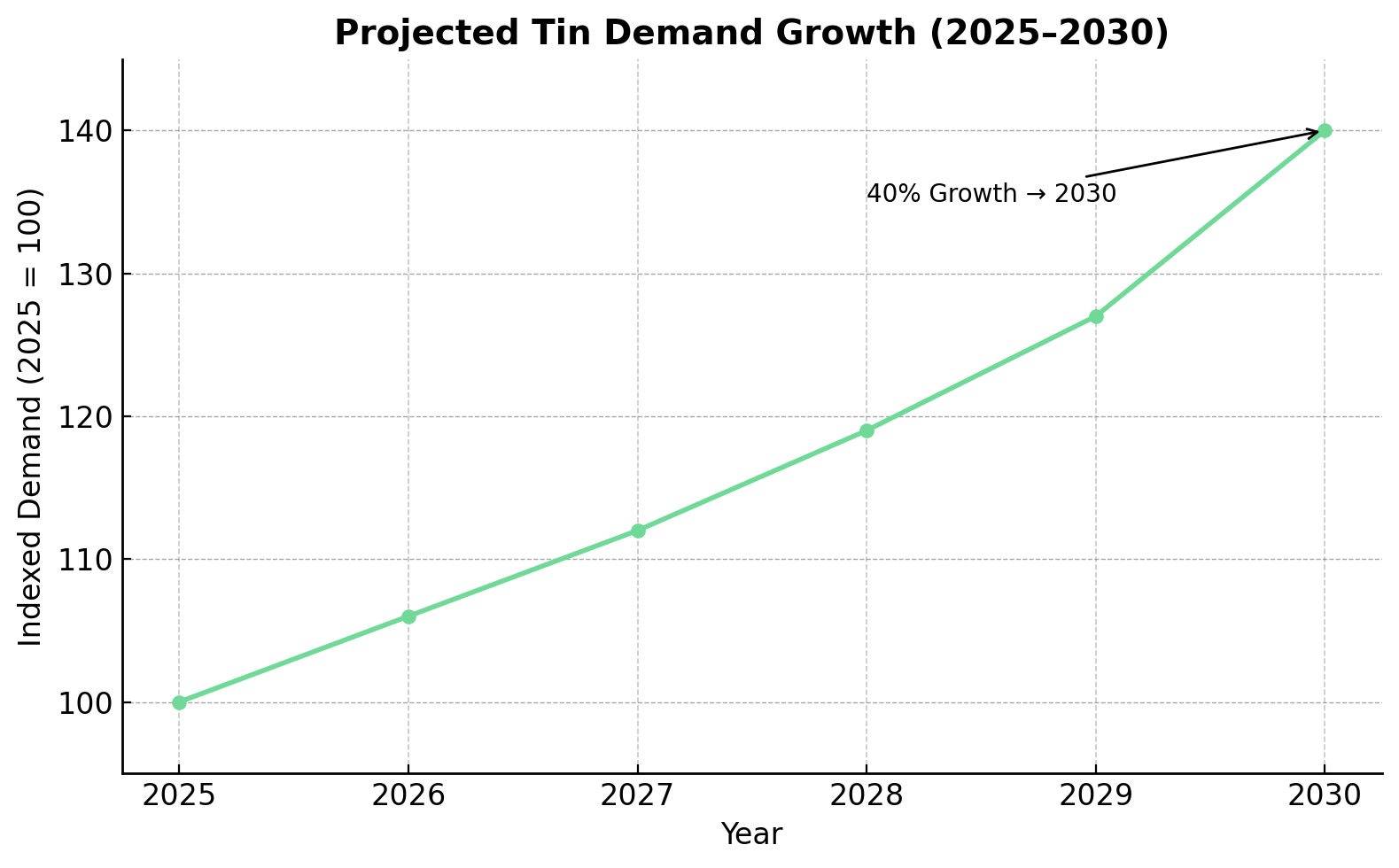

- Despite this development, the International Tin Association forecasts a 40% increase in tin demand by 2030, driven by electrification, semiconductors, and AI technologies.

- The tin market remains structurally fragile, with concentrated production in politically volatile jurisdictions such as Myanmar and Indonesia.

- Investors are increasingly turning to alternative jurisdictions like the DRC, where companies like Alphamin Resources and Rome Resources are developing scalable, high-grade tin assets.

- While prices may remain volatile in the short term, supply security, strategic sourcing, and development readiness are key factors guiding capital allocation.

The resumption of tin exports from Myanmar's Wa State in July 2025 has reintroduced volumes from a region that historically accounted for approximately 10% of global supply. While this re-entry temporarily eased spot market pressure, dropping tin prices 1.6% to US$32,775 per metric tonne, it has not altered the structurally tight long-term supply landscape that continues to define investment opportunities in this critical mineral sector.

Despite the Myanmar-driven price correction, July 2025 recorded an average tin price of US$33,610 per metric tonne, representing a 3.3% month-over-month gain that underscores persistent underlying bullish sentiment. The International Tin Association forecasts a 40% increase in tin demand by 2030, driven by electrification technologies, semiconductor applications, and artificial intelligence infrastructure requirements.

Supply Re-entry in a Fragile Market System

The tin market's response to Myanmar's export resumption highlights the sector's structural vulnerabilities rather than resolving them. Wa State's partial autonomy, ethnic governance framework, and historical volatility underscore the jurisdictional risks embedded in current supply chains. The region's two-year suspension demonstrates how localized political dynamics can generate disproportionate global price movements in a market characterized by thin physical stockpiles and minimal swing production capacity.

Market Response & Short-Term Price Action

London Metal Exchange data reveals the immediate market impact of Myanmar's return, with tin prices experiencing their steepest single-session decline in three months following the export announcement. However, the broader July performance suggests that fundamental supply-demand imbalances remain largely intact. Market participants continue to operate with limited inventory buffers, creating an environment where individual supply disruptions or resumptions generate outsized price volatility.

The tin market's structural thinness reflects years of underinvestment in new production capacity. Global tin exploration budgets remain below pre-2011 levels, constraining the pipeline of future supply additions. This dynamic creates a market where temporary supply additions, such as Myanmar's resumed exports, provide only short-term price relief without addressing longer-term supply security concerns.

Myanmar's Role & Wa State Governance Dynamics

Myanmar's tin production operates within a complex geopolitical framework where the Wa State maintains significant autonomy from central government control. This governance structure, while enabling continued mining operations during periods of national political instability, introduces unique supply chain risks that institutional investors increasingly factor into their commodity exposure strategies.

The Wa State's decision to resume exports reflects local economic priorities rather than national mining policy, highlighting how decentralized decision-making can create unpredictable supply patterns. For investors seeking reliable tin exposure, Myanmar's governance complexity reinforces the strategic value of alternative jurisdictions with more transparent regulatory frameworks.

Structural Demand Unmoved by Temporary Shocks

While prices responded to Myanmar's reopening, the longer-term supply-demand imbalance remains driven by technological supercycle fundamentals that position tin as a critical enabler of global electrification and digitalization trends.

Electrification, Semiconductors & Tin's Critical Role

Massachusetts Institute of Technology research identifies tin as the most critical metal for electrification technologies, emphasizing its irreplaceable role in high-temperature solder applications essential for electric vehicle batteries, solar photovoltaic systems, and advanced semiconductor packaging. The metal's unique properties, including corrosion resistance, low toxicity, and superior electrical conductivity, create limited substitution possibilities across these growth applications.

Tin demand growth of 40% by 2030, as projected by the International Tin Association, reflects the metal's integration into multiple secular growth themes. Electric vehicle production requires approximately 3-5 kilograms of tin per vehicle for battery management systems and charging infrastructure. Solar installations consume tin in both photovoltaic cell manufacturing and grid connection systems. Semiconductor applications, particularly advanced chip packaging for artificial intelligence processors, represent an emerging high-value demand segment with significant growth potential.

The Supply Pipeline Deficit

New tin production faces multiple development constraints that limit near-term supply additions despite elevated price levels. Complex metallurgical characteristics, particularly in polymetallic deposits, require sophisticated processing technologies that extend development timelines and increase capital requirements. Environmental, social, and governance considerations add additional permitting complexity, particularly in jurisdictions with heightened regulatory scrutiny.

Indonesia, Bolivia, and Myanmar, three major tin-producing regions, face distinct development challenges. Indonesian operations confront marine environmental concerns related to offshore mining activities. Bolivian projects navigate complex community consultation requirements and infrastructure limitations. Myanmar's political instability creates ongoing operational uncertainty for international mining companies.

Strategic Supply Chain Repositioning in the Global Tin Market

Geopolitical tensions and mineral diplomacy initiatives are reshaping sourcing strategies away from legacy producers toward jurisdictions offering greater supply security and strategic alignment with Western economies.

Mineral Diplomacy & United States Strategic Access Agreements

The United States has negotiated critical mineral access agreements in the Democratic Republic of Congo to reduce dependence on Chinese-controlled supply chains and politically volatile regions like Myanmar. These agreements position the DRC as a strategic alternative for tin, cobalt, and copper procurement, supported by improved regulatory frameworks and international development financing.

The DRC's emergence as a preferred sourcing jurisdiction reflects broader supply chain diversification strategies implemented by technology companies and defense contractors. Unlike traditional mining jurisdictions focused primarily on production economics, the DRC offers strategic alignment with Western security interests while maintaining competitive production costs.

DRC Emerges as a Tin Growth Corridor

Alphamin Resources exemplifies the DRC's potential as a high-grade tin production center. The company achieved fiscal year 2024 production of 17,324 tonnes, representing a 38% increase from the previous year. Earnings before interest, taxes, depreciation, and amortization reached US$274 million in fiscal year 2024, a 102% increase that demonstrates the operational leverage available to efficiently managed tin producers. Plant recovery rates exceeded target levels at 75%, indicating robust metallurgical performance across varied ore compositions.

Alphamin's fiscal year 2025 guidance of 20,000 tonnes positions the company as the world's highest-grade tin producer, with operations that deliver superior economics compared to traditional alluvial mining methods. The company's success validates the DRC's geological potential while establishing operational benchmarks for subsequent developments in the region.

Rome Resources, located approximately eight kilometers from Alphamin's operations, represents the next wave of tin development in the DRC's emerging mining corridor. The company's polymetallic assets contain tin, copper, and zinc mineralization within similar geological settings to Alphamin's Mpama South operations.

Rome Resources' drilling program has identified significant tin mineralization outside previously defined geochemical soil anomalies, suggesting broader mineralization potential than initially anticipated. Chief Executive Officer Paul Barrett notes the discovery's implications:

"The XRF analysis has shown considerable tin, and this lies outside the geochemical soil tin anomaly. We think there's considerable scope now for the northeast flank of Monte Agoma."

Capital Deployment & Project Differentiation in a Volatile Market

Despite favorable macro conditions, capital allocation remains highly selective. Investors focus on projects combining strategic jurisdiction, development readiness, and diversified commodity exposure to optimize risk-adjusted returns.

Financial Strength & Operational Execution

Rome Resources raised £8.2 million in 2024 through a reverse takeover and strategic placement, allocating approximately 49% of proceeds to drilling and resource development activities. The company operates three drilling rigs simultaneously to accelerate exploration progress and optimize geological understanding across multiple target areas.

Current metallurgical testing in Canada aims to assess processing flowsheets for polymetallic value extraction from the Monte Agoma prospect. The testing program addresses a critical development milestone by establishing optimal recovery methods for tin, copper, and zinc mineralization in a single processing circuit.

Project Milestones & Near-Term Catalysts

Rome Resources has engaged MSA Group to complete a Maiden Resource Estimate scheduled for September 2025, representing a major derisking milestone for the project. MSA Group's previous work on Alphamin Resources and other DRC projects provides relevant regional experience for resource modeling and mine planning activities.

The resource estimate will encompass tin, copper, and zinc mineralization across the Monte Agoma and Kalayi prospects. Early drilling results indicate tin zones exceeding 40 meters in width within structurally favorable geological settings, suggesting significant scale potential for resource definition.

Chief Executive Officer Paul Barrett emphasizes the resource expansion potential:

"What we're seeing now will only get bigger. We continue drilling and aim to put out an update with additional drilling and assays in September."

Jurisdictional Risk Premiums & Investor Repricing

The tin sector increasingly reflects jurisdictional bifurcation, with investors assigning valuation premiums to stability and strategic alignment considerations beyond traditional mining economics.

Risk Mitigation Through Strategic Geography

Myanmar's ongoing volatility illustrates the risks associated with overexposure to politically unstable jurisdictions. While the Wa State's export resumption provides temporary supply relief, the broader regulatory uncertainty surrounding Myanmar operations reinforces investor preference for alternative production centers.

The DRC's repositioning benefits from United States and Gulf state investment, improved permitting frameworks, and enhanced artisanal mining integration programs. International development organizations have supported infrastructure improvements and community development initiatives that strengthen the social license for large-scale mining operations.

Relative Valuation Uplift in Strategic Zones

Tin projects in the DRC increasingly attract institutional capital due to high-grade discovery potential, relatively low capital expenditure requirements, and supportive policy environments. The region's geological characteristics favor high-grade, hard-rock deposits that offer superior economics compared to declining-grade alluvial operations in Southeast Asia.

The United States-brokered access agreements provide additional investment security by establishing formal diplomatic frameworks for critical mineral procurement. These agreements reduce political risk premiums while creating preferential access conditions for Western technology companies requiring secure tin supplies.

The Investment Thesis for Tin

Strategic investors should view tin as a high-conviction, supply-constrained critical mineral with asymmetric upside potential driven by electrification demand growth and supply chain diversification imperatives.

- Supply-side fragility across Myanmar, Indonesia, and Bolivia exposes systemic vulnerabilities that create sustained price support despite temporary supply additions.

- Structural demand growth positions tin as a core enabler of electric vehicle adoption, solar energy deployment, and advanced semiconductor manufacturing.

- Jurisdictional shift toward the DRC creates investment opportunities in a high-priority zone for Western critical mineral procurement strategies.

- Operational delivery by companies like Alphamin demonstrates scalability and cost advantages available to efficiently managed hard-rock tin operations.

- Emerging discovery plays such as Rome Resources' assets offer proximity de-risking benefits and multi-metal optionality that enhances investment returns.

- Repricing catalysts including September 2025 resource estimates and United States critical mineral policy momentum may trigger broader institutional investor re-engagement with the tin sector.

Resilient Strategies in a Reshaped Tin Market

The resumption of Myanmar's tin exports has not altered the fundamental structural reality defining the global tin market. Supply remains concentrated in politically volatile jurisdictions, demand growth continues accelerating through electrification and digitalization trends, and investors increasingly prioritize supply security over production costs alone.

Companies positioned in strategic jurisdictions with operational clarity and resource depth represent the most attractive investment opportunities in this critical mineral transition. The next wave of capital deployment will favor organizations offering geopolitical alignment, metallurgical expertise, and development readiness, positioning firms like Alphamin Resources and Rome Resources at the center of this evolving investment landscape.

Analyst's Notes

Subscribe to Our Channel

Stay Informed