Lithium Proves Resilient Amidst U.S. Political Upheaval in an Electrified World

Trump Presidency on EV and Battery Metals Markets in the Linchpin of Surging EV and battery demand which positions lithium as a top investment theme. Near-term volatility, but an essential play on the global energy transition.

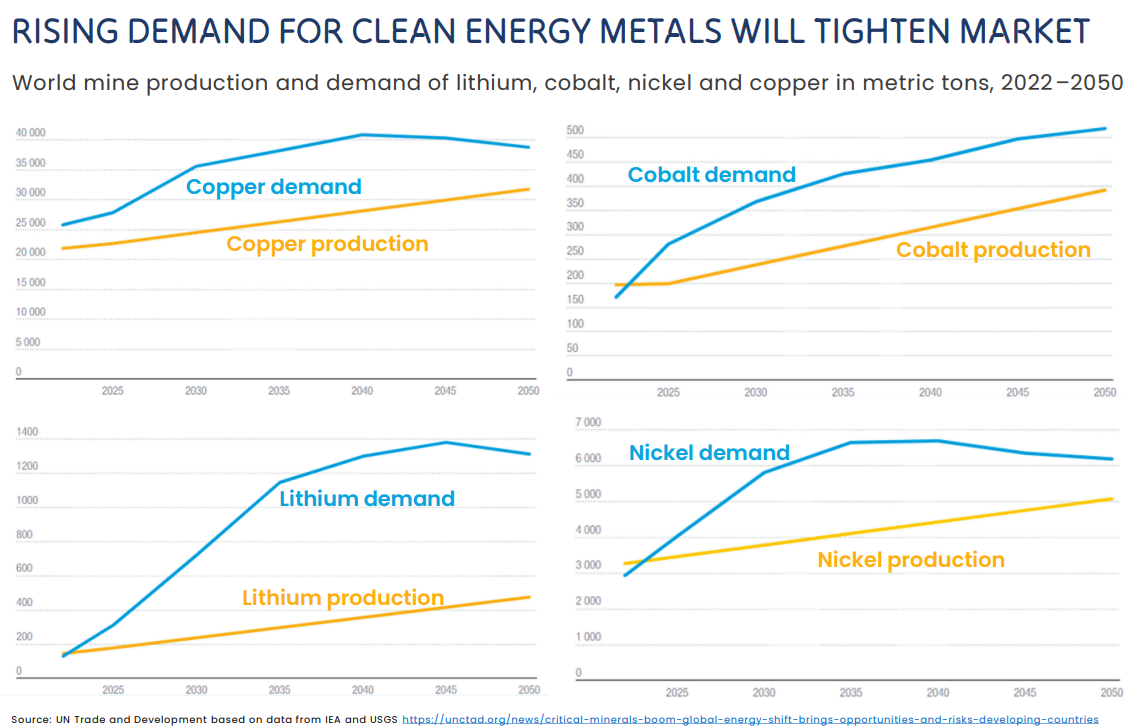

- Lithium demand is expected to soar 400% by 2030 due to rapid growth of electric vehicle and battery energy storage markets.

- Major lithium producers have signed multi-year supply agreements with EV makers like Tesla.

- Trump presidency could have significant implications for the electric vehicle (EV) sector and battery metals supply chains, taking a more ambivalent stance.

- Lithium prices hit record highs in 2022 but fell significantly in 2023-2024 due to oversupply as producers ramped up output. Prices stabilized and began trending upward in Q3 2024.

- Forecasts on lithium supply shortage start as early as 2025 as demand outpaces production from current and planned projects.

The global lithium market is poised for explosive growth in the coming years, driven by skyrocketing demand for lithium-ion batteries used in electric vehicles (EVs) and energy storage systems. As the world accelerates its transition to clean energy to combat climate change, lithium has emerged as an essential raw material underpinning this shift. For investors seeking exposure to the electrification megatrend, the lithium sector presents a compelling long-term opportunity.

Surging Demand from EVs and Energy Storage

Lithium-ion batteries have become the dominant technology powering the global EV revolution. Major automakers from Tesla to Volkswagen to General Motors are investing billions to electrify their fleets, while governments around the world are setting aggressive targets to phase out internal combustion engine vehicles. Global passenger EV sales more than doubled in 2021 to 6.6 million units, and are projected to hit 20.6 million units by 2025 and 54 million by 2040.

In addition to EVs, the stationary energy storage market is emerging as another significant source of lithium demand. Utilities and renewable energy developers are increasingly turning to large-scale battery storage to stabilize electric grids and support the integration of intermittent solar and wind power. Benchmark Mineral Intelligence expects lithium-ion battery demand to surge by 400% by 2030, reaching 3.9 Terawatt-hours.

Geopolitical Dynamics and Supply Chain Reshaping

China currently dominates the lithium-ion battery supply chain, accounting for 72% of global lithium chemical processing capacity in 2022.

"Should this new hard-rock supply come online, and at a sufficient grade quality and consistency, it could pose a challenge to incumbent producers who sit higher up on the cost curve," noted Adam Megginson, an analyst at Benchmark Mineral Intelligence.[1]

However, Western governments are taking steps to curb China's control and build out domestic supply chains. In 2024, Canada imposed a 100% tariff on Chinese EV imports, spurring China to file a complaint with the World Trade Organization. The U.S. has also levied steep tariffs on Chinese lithium-ion batteries and EVs, while offering incentives for domestic production through the Inflation Reduction Act. The European Union inked a critical minerals supply deal with Serbia in July 2024.

Potential Impact of Trump Presidency on EV and Battery Metals Markets

Whe the new US president-elect Donald Trump takes office on January 20th 2025, this could have significant implications for the electric vehicle (EV) sector and battery metals supply chains. While the Biden administration has implemented substantial subsidies and incentives to foster domestic EV and battery manufacturing, a Trump presidency might take a more ambivalent stance.

Uncertain Policy Support

- Trump has expressed skepticism about EV subsidies and tax credits, stating "Tax credits and tax incentives are not generally a very good thing" in an August 2024 interview. While he claims to be "a big fan of electric cars," he also supports gasoline and hybrid vehicles.

- Analysts believe Trump would find it challenging to fully repeal the Inflation Reduction Act (IRA) and other clean energy legislation. However, his administration could tighten regulations on qualifying EVs, limit tax credit eligibility, roll back emission standards, and scale down government fleet electrification commitments.

- Fastmarkets analysts estimate these policy changes could reduce U.S. EV sales by 5% by 2034 compared to current projections.

Elon Musk's Influence

- Despite Trump's past criticism of EVs, his relationship with Tesla CEO Elon Musk seems to have softened his rhetoric. Musk has endorsed Trump and appeared at his rallies, prompting the candidate to say "I'm for electric cars. I have to be, because Elon endorsed me very strongly."

- However, both Musk and Trump have criticized EV subsidies, even though Tesla has received billions in government support. Musk's controversial "voter lottery" also faced legal scrutiny for potentially violating election laws.

U.S.-China Tensions

- Trump may seek to reduce U.S. dependence on China for critical minerals processing and battery manufacturing to boost American competitiveness in EVs. Analysts believe he doesn't want to "lose to China" in this strategic industry.

- Stricter restrictions on Chinese imports could slow the pace of U.S. EV adoption in the near term by disrupting established supply chains. However, it could also spur more aggressive development of domestic mining and refining capacity.

Policy Recommendations

- Some experts suggest the U.S. should leverage Chinese expertise in battery manufacturing to accelerate its own capabilities, rather than trying to cut out China entirely.

- There are also calls for the IRA to allocate more funding directly to mining projects to secure upstream raw material supply. Shifting tax credits to focus more on driving consumer EV adoption and less on manufacturing restrictions could be more effective in the long run.

- Ultimately, a more pragmatic approach balancing cooperation and competition with China may be needed to sustain the U.S. EV sector's growth trajectory.

The election outcome's impact on lithium and battery metal demand will depend on the extent to which a new administration alters the EV industry's growth trajectory. A Trump presidency could introduce more uncertainty and potentially slow the demand curve's upward slope.

Lithium Producers Ramping Up to Meet Demand

Major lithium producers are moving aggressively to boost output and secure long-term supply agreements with EV and battery makers. Albemarle, the world's largest lithium company, plans to more than double its lithium carbonate equivalent (LCE) production to 225 kilotons by 2025. The company signed multi-year agreements in 2021 to supply lithium hydroxide to EV makers like Tesla and Lucid Motors.

China's Ganfeng Lithium, another top producer, is rapidly expanding with investments in projects across China, Argentina, Mexico and Australia. Ganfeng began supplying lithium to Tesla in 2022. Chilean mining giant SQM aims to grow its lithium carbonate capacity to 180 kilotons by late 2023, and also holds long-term contracts with Tesla and LG Energy Solution.

Electric Royalties

Electric Royalties (TSXV:ELEC) provides exposure to the lithium sector and broader electrification trend through a diversified portfolio of 40 royalties across lithium, vanadium, manganese, tin, graphite, cobalt, nickel, zinc and copper. The company's royalty model offers investors upside to rising metals prices and growth in the underlying assets while limiting downside risks. Electric Royalties' update highlights progress at several key lithium assets, including the Råna nickel-copper-cobalt project in Norway and Ruddy lithium asset in Ontario, Canada. As the lithium market grows to meet soaring battery demand, Electric Royalties is well-positioned to benefit from the industry's tailwinds through its royalty streams without the capital intensity of mining operations.

Nano One Materials

Nano One Materials (TSX:NANO) is commercializing an innovative "One-Pot" cathode active materials (CAM) manufacturing process that promises meaningful cost, energy, waste and emissions reductions compared to conventional methods. Nano One's technology is adaptable to lithium iron phosphate (LFP), nickel-manganese-cobalt (NMC), and other in-demand CAM chemistries. Its partnerships with major miners like Rio Tinto, leading cathode suppliers like BASF and automakers like Volkswagen validate the technology's potential. As battery-makers face pressure to reduce costs and improve their environmental footprints, Nano One provides a compelling licensing opportunity. The company's recent progress scaling up to commercial demonstration, expanding its intellectual property, and advancing towards a 4,000 tonnes per year LFP plant demonstrate it is on the cusp of initial commercialization.

James Bay Minerals

James Bay Minerals (ASX:JBY) is acquiring the advanced-stage, high-grade Independence Gold Project in Nevada, expanding its exposure from lithium to precious metals. Independence hosts a NI 43-101 compliant near-surface oxide resource of 334,300 ounces gold at 0.37 grams per tonne plus a high-grade underground resource of 796,200 ounces at 6.53 grams per tonne open for expansion. Nevada is a top-tier mining jurisdiction and the project's location next to majors like Barrick and Newmont reduces execution risk. With a low estimated capex and short timeline to initial production, Independence provides James Bay a near-term cash flow opportunity to complement its lithium growth pipeline. While on the surface a pivot from battery metals, the acquisition aligns with James Bay's strategy to acquire quality assets in attractive jurisdictions that can deliver shareholder value.

Lithium Price Volatility and Market Imbalances

Lithium prices have been on a rollercoaster ride over the past few years. Spot prices for battery-grade lithium carbonate in China hit an all-time high above $70,000 per tonne in 2022 amid the acute supply squeeze. However, prices have fallen sharply since November 2022 on increasing supply coupled with China's EV subsidy cuts and economic slowdown. Lithium carbonate values shed 22% to $10,019 in Q3 2024, a three-year low.

"We typically expect demand for lithium chemicals to be highest heading into Q4, as it tends to be the strongest quarter for EV sales. Given that feedstock supply upstream remains fairly strong, and chemicals supply in the midstream remains robust, we may not see much movement in prices to the end of the year," Megginson added.[1]

Looking ahead, the lithium market's long-term fundamentals remain intact despite near-term volatility. Benchmark expects supply deficits to emerge in the second half of the decade as demand continues to outpace production from current and new projects. This could send lithium prices back to record highs, benefiting established producers.

Key Investment Risks and Considerations

While the lithium growth story is compelling, investors must be aware of key risks. Lithium mining and processing can have significant environmental impacts, from greenhouse gas emissions to toxic waste. Growing scrutiny of sustainability issues across the EV supply chain could lead to stricter regulations and higher production costs.

Geopolitical risks are also important to monitor, especially U.S.-China trade tensions that could disrupt global battery supply chains. Investors should look for lithium companies with sustainable cost structures, strong balance sheets, geographically diversified assets, and secure long-term customer contracts. Given lithium's strategic importance, M&A and consolidation activities could also unlock shareholder value.

Conclusion

The global lithium market's growth trajectory is underpinned by the metal's critical role in the rapidly expanding electric vehicle and energy storage industries. Major lithium producers like SQM, Ganfeng Lithium and Livent are moving aggressively to expand production capacity, secure long-term supply agreements with automakers, and gain exposure to the most promising growth markets. The established players benefit from their low-cost operations, geographically diverse asset bases and strong customer relationships. However, the industry's long-term health also depends on a robust pipeline of new projects to meet projected demand.

Emerging companies like Nano One Materials, with its innovative cathode manufacturing process, Electric Royalties with its diversified royalty portfolio, and James Bay's solid lithium exposure in Tier One jurisdiction, provide unique investment exposure to the lithium value chain. Meanwhile, the expected increase in lithium-ion battery demand is driving mining activity in key producing countries like Australia, Chile and China, as well as potential new entrants like Canada, the US and Europe as the EV supply chain becomes more localized.

The Investment Thesis for Lithium

- Start building positions in well-established lithium producers with sound project pipelines, solid cost positions, and major long-term customer agreements.

- Invest in a diversified basket of lithium miners and refiners across geographies to mitigate geopolitical and single-asset risks. Consider lithium-focused ETFs.

- Given supply constraints, prioritize companies with projects slated to come online in the second half of the decade to capture lithium's next price upcycle.

- Closely monitor evolving U.S. and European policy incentives for domestic lithium production, which could benefit projects in those regions.

- Demand lithium players in your portfolio meet high ESG standards and have clear plans to minimize environmental footprints and improve sustainability.

The lithium sector offers a powerful secular growth story as the world charges ahead with vehicle electrification and renewable energy adoption. Near-term market imbalances may persist as the industry matures, but lithium's position as an irreplaceable ingredient in the clean energy transition is clear. For long-term investors, building a strategic position in key lithium producers and juniors, while closely tracking policy and technology shifts shaping the market, could generate robust returns as global demand takes off in the back half of the decade.

References:

- Williams, G. Investing News Network. October 2024. Lithium Market Update: Q3 2024 in Review

- Williams, G. Investing News Network. October 2024. Is Trump a Threat to US Electric Vehicle and Battery Supply Chain Growth?

- Benthan, J. Global Mining Review. April 2024. Addressing The Battery Market's Elephant In The Room.

- Pistilli, M. Investing News Network. September 2024. Where Does Tesla Get its Lithium?

Analyst's Notes

Subscribe to Our Channel

.jpg)

.webp)

Stay Informed