Marvel Biosciences Advances Novel Treatment for Social Withdrawal in Autism and Depression

Marvel Biosciences develops MB-204 for autism/depression, outperforming approved drugs in trials. Phase 1 ready, $9M valuation vs $80M+ sector comps. Partnership likely pre-Phase 2.

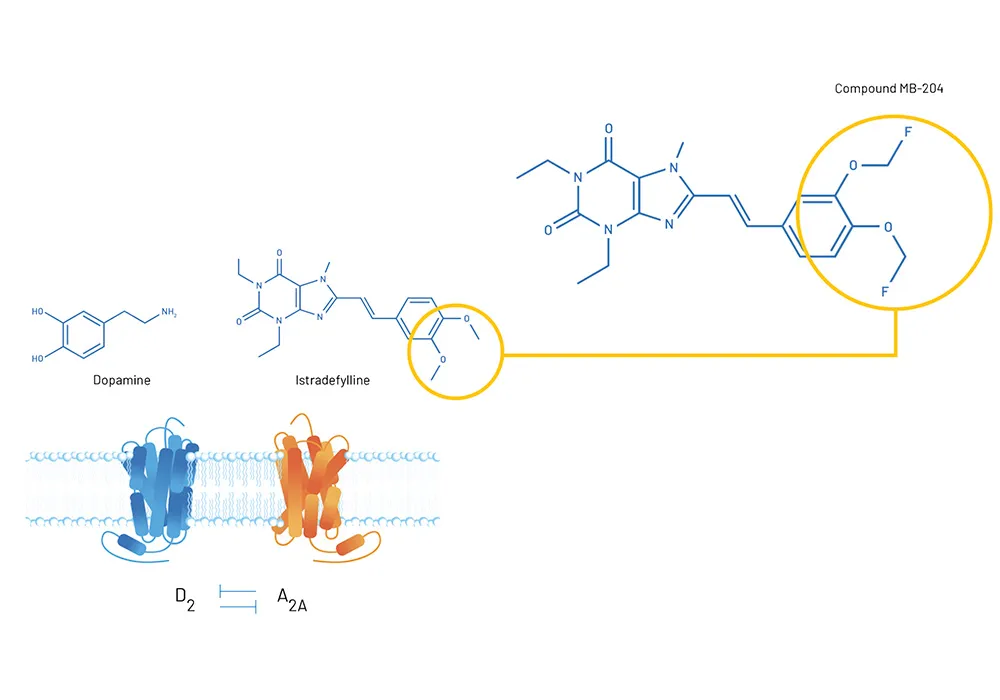

- Marvel Biosciences is developing MB-204, a first-in-class treatment targeting social withdrawal conditions in autism, depression, and Alzheimer's disease, based on a modified version of an approved Parkinson's medication

- Preclinical data shows the compound achieves rapid reversal of symptoms within one hour of oral dosing in animal models, outperforming trofinetide (the only FDA-approved drug for Rett syndrome) across multiple endpoints

- The company is preparing to enter Phase 1 clinical trials in Australia within 6-12 months, with composition of matter patents secured in China and Japan and additional jurisdictions pending

- Marvel is targeting orphan disease indications (Rett syndrome and Fragile X syndrome) first, where clinical success rates exceed 50% at Phase 3 and patient populations are well-defined and genetically homogeneous

- At C$9 million market capitalisation, the company trades at a significant discount to comparable neuroscience firms in Phase 1, with historical precedents showing neuroscience acquisitions typically occur before Phase 2 at valuations north of $80 million

Marvel Biosciences (TSXV:MRVL | OTC: MBCOF) represents a clinical-stage biotechnology company focused on developing treatments for social withdrawal disorders, an underserved therapeutic area affecting millions globally. The company's lead compound, MB-204, targets conditions characterised by social dysfunction including autism spectrum disorder, depression, and Alzheimer's disease. With autism prevalence rising to one in 36 children in the United States and depression affecting one in eight adults on antidepressants, the addressable market spans hundreds of billions of dollars in potential healthcare costs and lost productivity.

The company is led by Dr. Mark Williams, President and Chief Scientific Officer with nearly 20 years in biotechnology, and J. Roderick Matheson, CEO & Director with four decades of capital markets experience. Williams previously worked on a compound currently in Phase 3 trials for ischemic stroke that successfully reached NASDAQ listing, establishing a track record in advancing neuroscience assets through clinical development.

The Science: MB-204's Mechanism and Preclinical Performance

MB-204 is based on a known approved Parkinson's disease drug, providing the company with an established safety profile as a foundation for clinical development. The compound demonstrates what Williams describes as "essentially immediately active within an hour of oral dosing in animals" with "almost total reversal of symptoms in autism" across multiple endpoints. In genetically modified mouse models carrying autism-associated genes, untreated animals exhibit characteristic behaviors including social avoidance, self-grooming, and repetitive movements. Within one hour of MB-204 administration at doses lower than those used for Parkinson's disease, these animals display normalised social interaction, touching noses and paws with other mice, following other animals, and eliminating repetitive behaviors.

The compound's performance extends beyond autism models. In depression studies, MB-204 achieved approximately 90% reversal of depressive behaviors within one hour. Preliminary research also suggests potential benefits in Alzheimer's disease through effects on tau protein aggregation, though this application remains early-stage.

A critical differentiator emerged in head-to-head comparisons with trofinetide, the FDA-approved treatment for Rett syndrome. While trofinetide showed efficacy in one of several behavioral tests, MB-204 demonstrated superior results across all measured endpoints. More significantly, animals treated with MB-204 maintained behavioral improvements for two to three weeks after treatment cessation, suggesting semi-permanent neurological changes, whereas trofinetide benefits disappeared immediately upon stopping treatment.

Strategic Focus: Orphan Diseases as the Primary Path

Marvel's clinical strategy prioritises orphan disease indications, specifically Rett syndrome and Fragile X syndrome. This approach offers several advantages that Williams articulated clearly:

"Going after the orphan disease is the cleanest valuation we can get."

Orphan diseases provide well-defined, genetically homogeneous patient populations, making clinical trial design more straightforward and regulatory pathways clearer. Both Rett syndrome and Fragile X are monogenic disorders where single gene mutations drive the disease, allowing for more predictable preclinical-to-clinical translation.

Historical success rates support this strategy. Phase 3 clinical trial success rates exceed 50% for orphan diseases compared to lower rates in broader indications. Recent regulatory approvals in Rett syndrome and anticipated approvals in Fragile X provide validated clinical endpoints and regulatory precedents that Marvel can leverage, reducing development risk and timeline uncertainty.

The broader depression and Alzheimer's markets represent secondary opportunities. Williams acknowledged that "Alzheimer's is a graveyard for compounds" with only two antibody approvals after 20 years and hundreds of billions in investment, delivering modest disease-slowing rather than reversal effects. Depression, while a large market, presents patient heterogeneity challenges. The orphan disease focus allows Marvel to demonstrate proof-of-concept in well-controlled populations before potentially expanding to larger indications under partnership arrangements.

The Phase 1 Development Program

Marvel has completed manufacturing of clinical-grade material under current Good Manufacturing Practice (cGMP) standards and finished four-week Good Laboratory Practice (GLP) toxicology studies, meaning MB-204 is ready for immediate clinical entry. The company plans to conduct Phase 1 trials in Australia, benefiting from that country's efficient regulatory environment and 43% research tax credit.

The Phase 1 program will consist of single ascending dose (SAD) and multiple ascending dose (MAD) studies over six to 12 months in healthy volunteers. Williams noted the company has incorporated specific biomarker assessments to demonstrate target engagement in humans, creating an additional value inflection point. "Not only is the drug safe but it looks like it's doing what you want it to do in the patient pool," he explained, representing a critical validation step for pharmaceutical partners.

If Marvel proceeds independently to Phase 2, the company has designed efficient proof-of-concept studies. Williams estimates that within one month in a small population of Rett syndrome patients, the company could demonstrate clinical benefit, leveraging established endpoints from trofinetide's development program and FDA approval pathway.

Interview with Dr. Mark Williams, President & CSO, & J. Roderick Matheson, CEO of Marvel Bioscience

Building a Defensible Market Position

Marvel holds composition of matter patents in China and Japan, with additional jurisdictions expected imminently. Composition of matter patents represent the strongest form of pharmaceutical intellectual property, covering the molecule itself rather than just methods of use or formulation. This patent position is essential for pharmaceutical partnerships, as Williams noted:

"They want to see the composition of matter patents. It gives them a lot of confidence that if they took over development, they have full control of the compound."

The competitive landscape shows limited direct competitors. Trofinetide remains the only approved Rett syndrome treatment, generating meaningful commercial revenue but with limitations in efficacy and durability that MB-204 appears to address. In Fragile X syndrome, no treatments are currently approved, though several candidates are in development. Marvel's differentiated mechanism and preclinical performance position the company favorably against emerging competition.

The Path to Pharmaceutical Partnership

Marvel's business model aligns with neuroscience sector norms where large pharmaceutical companies have largely exited early-stage neuroscience research, preferring to acquire or partner on de-risked assets. Williams stated that

"roughly 70% of companies consummate some kind of business arrangement, a licensing, partnership, acquisition deal with a larger pharma before their phase two begins."

This creates a clear value realisation path for Marvel shareholders.

The company has identified and engaged in preliminary discussions with potential partners. Williams emphasised the preference for a single comprehensive partnership rather than fragmenting rights by indication or geography:

"MB-204 would be probably better with a single partner than it would be to try to sub it to various groups and so forth for various different indications."

Current Valuation Relative to Peers

Marvel currently trades at approximately $9 million CAD market capitalisation, which Matheson characterised as "certainly north of 30-35 million" below where comparable companies trade. Williams provided historical context: "Companies that have completed phase one data, I mean they can be certainly north of $80 million historically." Specific comparables include Mindset Pharma, acquired by Otsuka Pharmaceuticals for $80 million before Phase 2 entry, and Canadian firms NervGen Pharma and ProMIS Neurosciences, both in Phase 1 for Alzheimer's disease and trading north of $100 million with NervGen Pharma exceeding $300-400 million.

The valuation disconnect appears attributable to challenging junior capital market conditions during COVID-19, competition for investor capital from technology sectors, and limited investor awareness rather than fundamental scientific or commercial deficiencies. Matheson noted the company operates as a virtual organisation with minimal overhead, maintaining capital efficiency while advancing the asset.

The Risk-Reward Framework

Near-term catalysts include Phase 1 trial initiation, safety and biomarker data readouts, potential orphan drug designations, additional patent grants, and partnership announcements. Williams acknowledged that "funding has always been a chronic issue with companies of our size," suggesting potential equity financing needs to support clinical advancement absent partnership capital.

Key risks include Phase 1 safety findings, translation of animal efficacy to humans, clinical trial execution, competition from other Rett/Fragile X programs, and partnership negotiation dynamics. The company's reliance on external partnerships for Phase 2 and beyond creates business development execution risk, though this aligns with sector norms and preserves capital efficiency.

Macro Thematic Analysis

The neuroscience sector presents a compelling investment thesis driven by rising disease prevalence, unmet medical needs, and pharmaceutical industry dynamics. Autism diagnoses have increased dramatically, from rare occurrence to one in 36 children, creating urgent demand for effective interventions beyond behavioral therapy. Depression affects one in eight adults on medication, yet many current treatments show limited efficacy or significant side effects. Alzheimer's impacts one in three individuals over 75, with recent antibody approvals representing only modest progress after decades of failures.

Simultaneously, large pharmaceutical companies have substantially reduced internal neuroscience research, outsourcing early-stage innovation to biotechnology firms. This creates predictable acquisition pathways for companies demonstrating clinical validation, particularly in orphan diseases where regulatory paths are clearer and commercial exclusivity is protected. The combination of large addressable markets, limited effective treatments, and active pharmaceutical acquirers creates favorable conditions for investors in differentiated neuroscience assets with clinical-stage validation.

"We've gone head-to-head against trofinetide, the approved drug, and we've beaten it. So we feel very confident that this is the right path for us and everything else would just add additional incremental value." - Mark Williams, President & CSO

TL;DR: Executive Summary

Marvel Biosciences is developing MB-204, a rapid-acting treatment for social withdrawal disorders targeting autism, depression, and Alzheimer's disease markets worth hundreds of billions of dollars. The compound has demonstrated preclinical superiority over the only FDA-approved Rett syndrome drug and is ready for Phase 1 trials in Australia within 6-12 months, with composition of matter patents secured. At a $9 million CAD valuation, the company trades at a significant discount to $80+ million historical precedents for Phase 1 neuroscience assets, with 70% of sector companies completing partnership transactions before Phase 2.

FAQs (AI Generated)

Orphan diseases offer genetically homogeneous patient populations with validated endpoints, achieving >50% Phase 3 success rates versus lower rates in heterogeneous conditions. This strategy reduces clinical risk and accelerates partnership timelines.

MB-204 outperforms trofinetide across all behavioral endpoints in head-to-head studies. Critically, MB-204 produces semi-permanent improvements lasting 2-3 weeks post-treatment, while trofinetide benefits disappear immediately after cessation.

Approximately 70% of neuroscience companies complete deals before Phase 2, typically at valuations exceeding $80 million. Marvel targets this inflection point post-Phase 1 validation, when pharmaceutical acquirers gain safety and biomarker confidence.

Phase 1 initiation is immediate, with 6-12 month duration for safety and biomarker data. Partnership discussions occur throughout Phase 1, with historical deals consummating at this stage or shortly thereafter.

Australia offers efficient regulatory processes, high-quality clinical infrastructure, and a 43% research tax credit that significantly reduces net trial costs while maintaining data quality and FDA acceptability.

Analyst's Notes

Subscribe to Our Channel

Stay Informed