Logistics Failures Create 3x Salt Pricing Spreads as North America Imports 8-10 Million Tonnes Annually

North America's import-dependent salt market hit $300/tonne vs $100 contracted as logistics failures stranded supply at ports during 2026 demand spike.

- North America's 2026 road salt stockout resulted from domestic production unchanged since American Rock Salt opened in 2001, creating 8 to 10 million tonne annual import dependency representing 20% to 35% of consumption.

- Municipal liability frameworks legally require road de-icing in winter jurisdictions, creating non-discretionary demand, but spot market pricing in Detroit reached $300 per tonne during early 2026, compared to contracted rates near $100 per tonne as commercial driver shortages prevented delivery from ports to municipal stockpiles.

- Commercial driver shortages stranded thousands of tonnes at Newark and Baltimore ports, forcing Detroit municipalities without strategic reserves into spot markets where competition drove pricing from $100 per tonne contracted rates to $300 per tonne.

- Legacy salt producers face mounting environmental challenges, with governments enforcing stricter regulations to mitigate ecological impacts, and certain legacy assets remaining unsold specifically due to environmental risks. Projects leveraging clean energy and logistic advantage are positioned to replace the 8 to 10 million tonne annual import volume.

- Investment returns depend on all-in sustaining cost per delivered tonne, including trucking distance from port to municipal buyer, contract tenure that determines revenue visibility beyond single winter seasons.

A Break in a Low-Visibility Market

Industrial salt operates as a municipal utility input with consumption driven by winter weather severity and road network size rather than economic cycles. The winter of 2026 broke this stability when Detroit metro area spot markets reached $300 per tonne, while thousands of tonnes remained stranded at Newark and Baltimore ports, demonstrating that available supply could not reach buyers during peak demand.

Domestic mining capacity remained unchanged since 2001 when American Rock Salt in New York became the last major new underground salt mine to open in North America. Municipal procurement operates under statutory lowest-qualified-bid requirements with annual rebidding cycles that penalize suppliers who maintain off-season inventory. A commercial driver shortage prevented movement from ports to inland distribution points even when salt existed in storage.

Investment returns in industrial salt depend on all-in sustaining cost per delivered tonne including final-mile trucking from port to municipal buyer, multi-year contract tenure that determines whether revenue extends beyond single winter seasons, and regulatory compliance costs.

North America's 2026 Stockout Revealed System Failures

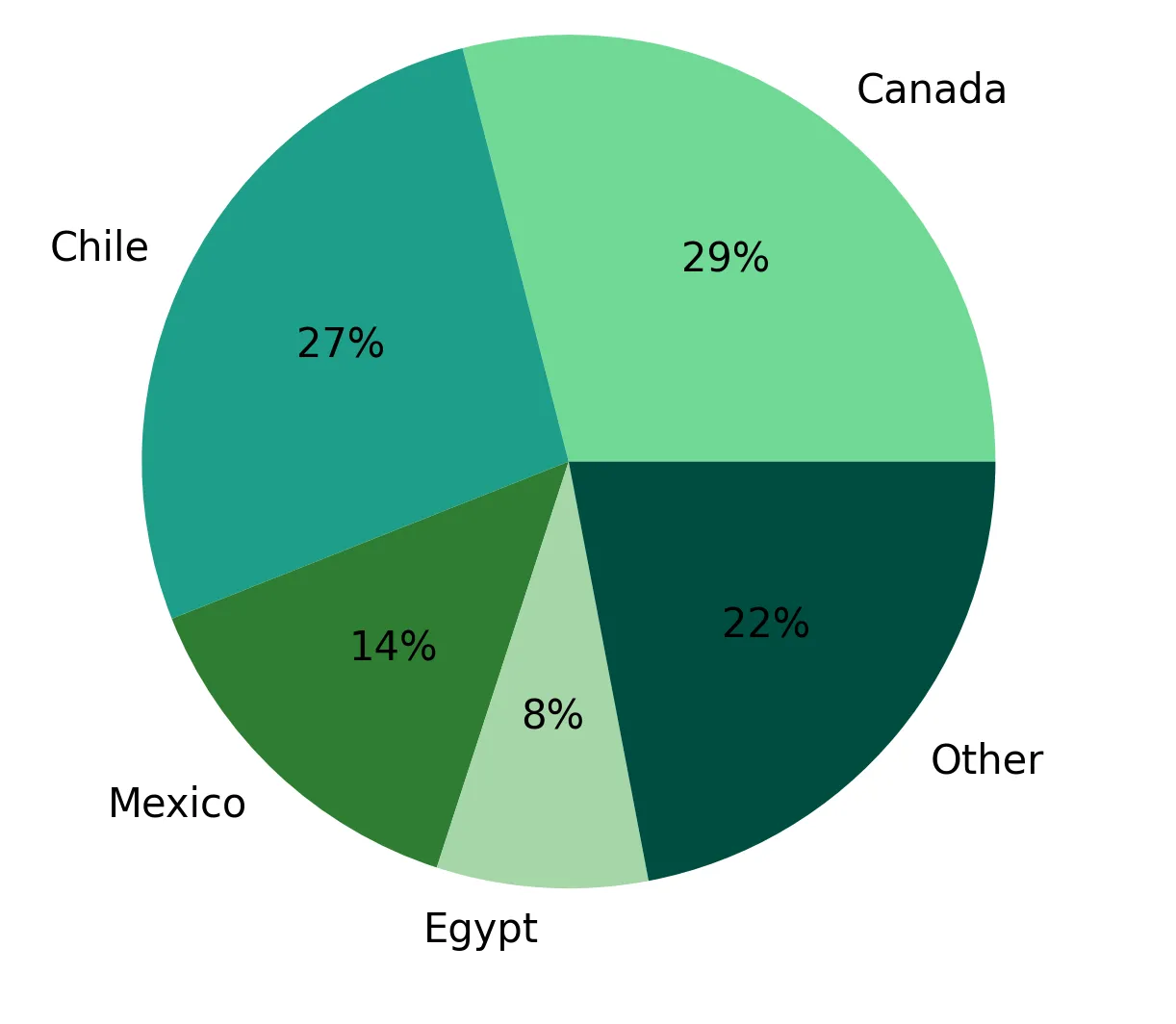

Domestic salt production capacity has not expanded since 2001 when American Rock Salt opened the last major new underground mine in New York. Mining sector capital over the past two decades flowed to lithium extraction, copper mining for electrical grid expansion, and gold as monetary hedge allocation. Industrial salt attracted minimal investment due to $100 per tonne pricing that generates lower returns per dollar of capital. This created 8 to 10 million tonne annual import dependency representing 20% to 35% of total North American consumptio, with United States import data from 2020 to 2023 showing Canada supplying 29%, Chile 27%, Mexico 14%, Egypt 8%, and other sources 22% by volume.

Municipal procurement operates under statutory lowest-qualified-bid requirements with annual rebidding that penalizes suppliers who maintain strategic reserves. This minimizes municipal expenditure during mild winters but fails when multiple cities enter spot markets simultaneously, demonstrated by Detroit metro area pricing reaching $300 per tonne in early 2026 compared to contracted rates near $100 per tonne.

Sodium chloride thermodynamics amplified waste. At 30 degrees Fahrenheit, one pound of salt melts 46.3 pounds of ice, while at zero degrees Fahrenheit the same pound melts only 3.7 pounds. Municipalities applying salt during sub-zero temperatures consumed inventory without achieving ice melting, accelerating stockpile depletion.

Environmental Liabilities Create Regulatory Risk Without Viable Substitutes

Studies during the 2025 to 2026 season found 61% of sampled freshwater locations in the Northeast exceeded Environmental Protection Agency thresholds for aquatic life. Chloride ions do not degrade in groundwater systems but accumulate in aquifers over decades, creating remediation liabilities.

Infrastructure damage imposes additional costs as every $100 spent on road salt causes $3,000 in corrosion damage to vehicles, bridges, and reinforced concrete structures. These costs fall on vehicle owners and infrastructure maintenance budgets but create political constituency for regulations that would cap chloride discharge.

Beet juice blends require 80% salt brine by volume and cost $1.70 to $1.85 per gallon. Sand prevents vehicle traction loss but does not melt ice and creates sewer clogging. Calcium chloride and magnesium chloride offer lower temperature effectiveness and reduced environmental impact, but cost premiums prevent widespread municipal adoption.

Municipal buyers face legal obligation to maintain passable roads, environmental regulations impose monitoring costs, but no substitute exists at cost parity with sodium chloride. Producers with electrified operations using renewable power gain regulatory preference as chloride limits tighten.

Atlas Salt Targets Import Displacement Through Logistic Leverage

Atlas Salt holds 95 million tonnes of reserves grading 95.9% sodium chloride with 868 million tonnes inferred resource according to the 2025 Updated Feasibility Study. The feasibility study reports all-in sustaining costs of $34.90 per tonne, selling prices of $118.40 per tonne, net present value at 8% discount rate of $920 million, and internal rate of return of 21.3%.

Public maps show the project site located 2 kilometers from Turf Point Port via enclosed ship-loading conveyor, 1.4 kilometers from the St. George's 66 kilovolt electrical substation, and bordering the Trans-Canada Highway. This indicates less than 3 days of shipping to Boston compared to more than 14 days from Egypt or Chile. This 11-day differential allows weather-responsive delivery during winter demand spikes when municipalities enter spot markets, capturing pricing premiums demonstrated by Detroit's $300 per tonne rates in early 2026 versus contracted $100 per tonne.

Nolan Peterson, Chief Executive Officer, highlights the project’s position against import dependency:

"We aim to supply de-icing road salt to the North American market and we will be the first new salt mine built in North America in 25 years… You have to remember the primary customer for our salt is cities and governments and they are legally obligated to purchase salt to de-ice roads for liability reasons."

Peterson emphasizes de-risked execution:

"We don't have metallurgical, block model, geology... Salt deposits are very easy to define and permitting is advanced on this project... we have an approved environmental assessment."

Newfoundland and Labrador's Environmental Minister released the project from provincial environmental assessment in April 2024 after two months of review. The project targets electrified operations powered by a hydroelectric grid connection, eliminating diesel generator emissions.

Risk Framework & Analysis Invalidation Conditions

Commercial driver shortages may persist despite new domestic production if wage rates for corrosive bulk hauling do not rise enough to attract sufficient drivers, preventing delivery during peak winter demand.

The investment thesis fails under four conditions: municipal procurement shifts to multi-year strategic stockpiling contracts that eliminate delivery-time advantages, governments impose strict chloride discharge caps requiring substitution regardless of cost, alternative de-icing technologies achieve $100 per tonne cost parity at city-scale volumes, or automation and driver wage increases solve commercial driver shortages and eliminate logistics bottlenecks.

The Investment Thesis for Salt

- Government buyers legally required to purchase de-icing materials create stable baseline demand, but rigid annual bidding systems that select suppliers solely on lowest price eliminate incentives to stockpile inventory, transforming predictable winter weather into unpredictable pricing events when delivery systems fail under stress.

- Import-dependent markets where 20% to 35% of supply travels by ocean freight become vulnerable to delivery timing advantages during severe weather, as demonstrated when suppliers able to deliver within days captured triple the pricing of suppliers requiring two-week shipping windows even when total available supply exceeded demand.

- Environmental monitoring revealing majority contamination in regional water samples creates regulatory momentum for discharge restrictions that impose new costs on existing high-emission operations while creating competitive advantages for suppliers using grid-connected renewable power that avoid emissions-tracking obligations and future carbon pricing exposure.

- Industrial commodities purchased by government buyers under legal mandates offer downside protection through non-discretionary consumption floors, but upside participation requires delivery infrastructure that functions during the exact conditions when procurement systems break down and spot market competition drives prices above long-term contract rates.

- Returns in logistics-constrained commodity markets separate along three measurable factors: production cost plus delivery cost to end buyer determines baseline profitability, contract length beyond single purchase cycles determines revenue predictability, and regulatory compliance positioning determines which cost structures face escalation versus which avoid new expense categories as environmental standards tighten.

The 2026 salt crisis demonstrates a broader investment principle: commodities with mandatory government consumption and delivery bottlenecks generate outsized pricing gains when driver shortages or port congestion prevent imports from reaching buyers. Investors evaluating industrial commodity exposure should prioritize suppliers with port proximity and trucking infrastructure over reserve size alone, as delivery constraints convert weather-driven demand spikes into 3x pricing premiums that annual procurement contracts cannot prevent during supply disruptions.

TL;DR

North America's 2026 road salt shortage exposed critical logistics failures when commercial driver shortages prevented delivery of imported salt from ports to municipalities, despite adequate supply existing at Newark and Baltimore facilities. Detroit spot market pricing reached $300 per tonne compared to $100 contracted rates. With domestic production unchanged since 2001 and annual imports representing 20-35% of consumption, municipalities without strategic reserves faced supply disruptions. Environmental regulations targeting chloride contamination—found in 61% of sampled Northeast freshwater locations—create additional pressure on legacy producers while favoring electrified operations using renewable power. Investment returns depend on all-in delivered cost including final-mile trucking, multi-year contract tenure, and regulatory compliance positioning.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

.jpg)

Stay Informed