Mont Royal Resources' Updated PEA Confirms Ashram's Rare Earths Scale, PFS Targeted for H2 2026

Mont Royal Resources' updated Ashram PEA confirms a 30-year rare earths project with CAD$2.03B NPV, 22% IRR, and a path to Pre-Feasibility Study.

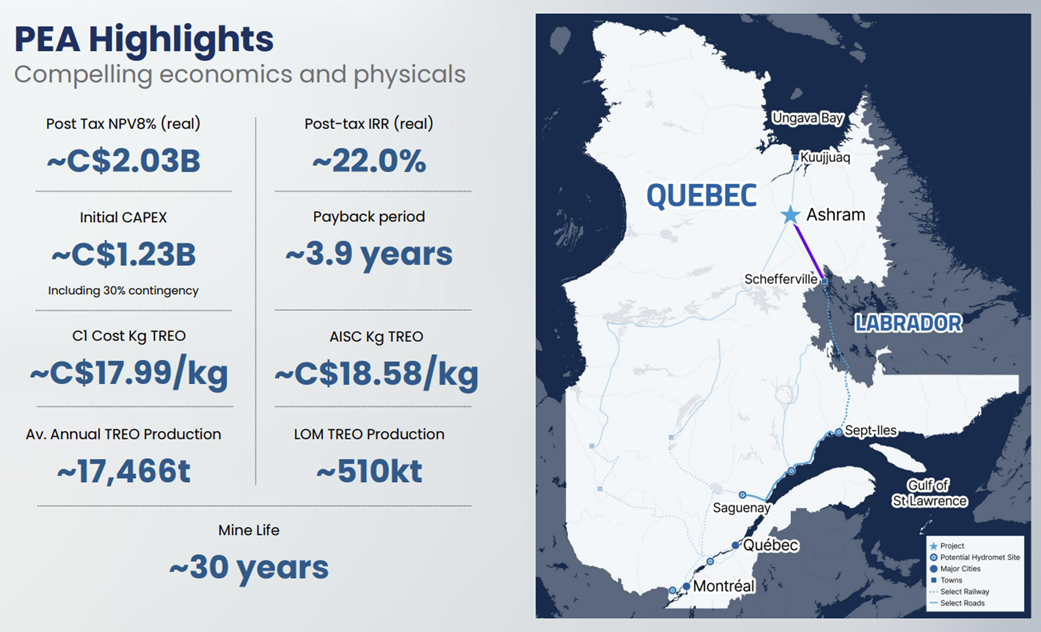

- The updated Preliminary Economic Assessment confirms Ashram as a large-scale, 30-year North American rare earths development, delivering a post-tax NPV8% of C$2.03 billion and a 22.0% post-tax IRR.

- Mont Royal filed the supporting NI 43-101 Technical Report confirming there are no material differences from the PEA results on previous reports.

- The Mineral Resource Estimate totals 204.3Mt (73.2Mt Indicated and 131.1Mt Inferred) grading approximately 1.9% TREO, with neodymium and praseodymium accounting for roughly 21% of the basket.

- Alongside the PEA, the company is engaging with the Naskapi Nation's independent access-corridor initiative and has begun a helicopter-supported gold till-sampling survey at its Northern Lights project, directly along strike from Benz Mining's Eastmain gold deposit.

- Initial capital cost is estimated at C$1.23 billion including 30% contingency, partly offset by an anticipated C$342 million in Clean Technology Manufacturing tax credits with a Pre-Feasibility Study targeted to commence in the second half of 2026.

Mont Royal Resources (ASX:MRZ, TSXV:MRZL) has spent the past month building the technical and social license case for its Ashram Rare Earths and Fluorspar Project in Nunavik, Québec by filing an updated Preliminary Economic Assessment, backing it with a formal NI 43-101 Technical Report, and progressing parallel exploration and community-engagement workstreams that speak to how the company is positioning itself in the race to build Western rare earth supply chains outside China.

The updated PEA released on June 2026 confirms Ashram as a long-life, large-scale development. China currently accounts for roughly 77% of global rare earth mine production and around 90% of separation capacity, a concentration that has pushed Western governments to prioritise alternative sources of magnet metals neodymium, praseodymium, dysprosium and terbium chief among them. Ashram's monazite-dominant mineralogy, with NdPr making up approximately 21% of total rare earth oxides (TREO), places it in a favourable position to supply that gap.

Ashram Financial Metrics

The PEA outlines a 30-year mine life supporting average annual production of approximately 17,466 tonnes of saleable rare earth oxide, including around 4,035 tonnes of NdPr oxide, roughly 100 tonnes of combined dysprosium and terbium oxide, and about 230 tonnes of yttrium oxide. At a real basket price of C$44.40 per kilogram of saleable REO, the project is forecast to generate life-of-mine revenue of C$24.6 billion and life-of-mine EBITDA of C$15.5 billion, an EBITDA margin of 62.7%.

On a post-tax basis, the project shows an NPV8 of C$2.03 billion, an IRR of 22.0%, and a payback period of 3.9 years from the start of production. Pre-tax figures are stronger still, with an NPV8 of C$3.44 billion and an IRR of 25.6%. Initial capital expenditure is estimated at C$1.23 billion, including a 30% contingency, with total life-of-mine capital expenditure of C$1.6 billion. The company also expects to benefit from approximately C$342 million in refundable Clean Technology Manufacturing Investment Tax Credits, incorporated into the post-tax cash flow model.

Project Overview

Ashram sits on Mont Royal's 100%-owned Eldor Niobium Project, roughly 130km south of Kuujjuaq, and is one of the largest monazite-dominant carbonatite-hosted rare earth deposits in North America. The updated Mineral Resource Estimate, using a net metal return cut-off of C$287/t defines 73.2Mt of Indicated Resources grading 1.89% TREO and 131.1Mt of Inferred Resources grading 1.91% TREO. The PEA's 30-year mine plan draws on only 25% of that resource, leaving considerable optionality for expansion, including the still-excluded BD-Zone and satellite targets such as Mallard within the wider Eldor carbonatite complex.

The development concept pairs an on-site concentrator at Ashram, producing a mixed rare earth concentrate at an average grade of around 30% REO, with a proposed hydrometallurgical processing facility in Saguenay, Québec, that would upgrade this concentrate into a saleable Mixed Rare Earth Carbonate. Mont Royal's Managing Director, Nicholas Holthouse, framed the update as a milestone for the project:

"It's a very long life project, 30 years, first 25% of the resource. It's one of those projects that does deserve that significant liquid capital that these larger hard rock projects do require to get up and running."

The company filed the NI 43-101 Technical Report underpinning the PEA, confirming there are no material differences between the reports as a procedural but necessary step under Canadian disclosure rules, given issuers must file within 45 days of an initial PEA disclosure.

Interview with Nicholas Holthouse, MD of Mont Royal Resources

Competitive Positioning

Ashram's positioning rests on more than resource scale. Its relatively simple monazite-bastnäsite-parisite-xenotime mineral assemblage is considered commercially favourable for metallurgical recovery, and the project sits in Québec, a Tier-1 jurisdiction with access to low-cost hydroelectric power, established logistics corridors via Kuujjuaq, and Canadian critical minerals funding programmes.

Holthouse explained the project's scalability going forward:

"What we are doing is doing a bit of a cost-benefit analysis on throughput versus CapEx, and seeing what winding that back a little further would do with regards to capex, but looking at opportunities also perhaps even coming back to the concentrate stage again only and working with partners to go into hydromet to reduce that capital cost storage."

Demand for magnet rare earths is projected to grow at a compound annual rate of 8-12% through 2050 driven by electric vehicles, wind turbines, robotics and defence applications, a structural deficit that Mont Royal is positioning Ashram to help fill, alongside potential fluorspar by-product value that could add further upside beyond the current base case.

Community and Regulatory Context

Project advancement in Nunavik requires ongoing engagement with Inuit, Naskapi and Innu communities. The company acknowledges a parallel, Nation-led initiative: the Naskapi Nation of Kawawachikamach's Nuuhchiimiiu Maaskinuw Project, a community-driven assessment of potential regional access corridor options. Mont Royal was explicit that this is an independent initiative it does not control, while noting its own continuing discussions with the communities involved in Ashram's development and in broader regional infrastructure planning which the company says is intended to build long-term relationships based on trust and mutual respect.

Catalysts Ahead

Beyond Ashram, Mont Royal holds a 75%-owned interest in the Northern Lights Minerals tenement package, a 536km² land position in the Upper Eastmain Greenstone Belt. The company announced a helicopter-supported till-sampling programme across the Chateaufort Property, designed to test gold potential using gold-grain dispersion analysis. The target area sits directly along strike from Benz Mining Corp's Eastmain gold project, which hosts a Mineral Resource of 1,005,000oz at 6.1g/t gold. Approximately 60 samples are planned across two sampling lines, with field work expected to wrap up in late July 2026, preliminary HH-XRF and pebble count data expected in August, and a full report including gold-grain counts due in the third quarter of 2026.

Investment Thesis for Mont Royal Resources

- Ashram's 204.3Mt resource and 30-year mine plan position Mont Royal among the larger advanced rare earth developers outside China, with a NdPr-weighted basket that aligns with structural Western demand for magnet metals.

- Updated PEA economics of C$2.03 billion post-tax NPV and 22.0% IRR, clear the bar for progression to Pre-Feasibility Study, targeted for H2 2026.

- Government support is a live tailwind: the project is expected to qualify for CAD$342 million in Clean Technology Manufacturing tax credits, and Canadian critical minerals funding schemes have expanded over the past 12 months.

- Funding risk is the key near-term overhang; approximately CAD$1.23 billion in initial capital will likely require some combination of equity, debt, government grants and strategic partnerships, with no committed sources yet in place.

- Community and Indigenous engagement outcomes including the independent Naskapi access-corridor initiative will influence the pace and shape of infrastructure planning; watch for updates as PFS work progresses through H2 2026.

- The Northern Lights gold till-sampling results, expected from August 2026, offer a near-term, lower-cost exploration catalyst distinct from the Ashram development timeline.

- Monitor the PFS scope for confirmation of the access-road cost-sharing arrangement and any formal off-take or strategic partnership announcements, both of which would materially de-risk the funding picture.

Macro Thematic Analysis

Rare earths sit near the centre of the critical minerals debate reshaping Western industrial policy. Magnet rare earths neodymium, praseodymium, dysprosium and terbium are essential inputs for electric vehicle motors, wind turbine generators, robotics, defence systems and consumer electronics, and demand is forecast to grow at 8-12% annually through 2050. Yet China's grip on the supply chain remains close to total: approximately 77% of global mine production and around 90% of separation capacity ran through Chinese facilities in 2025, leaving non-Chinese buyers exposed to concentrated supply and periodic export restrictions.

That imbalance has pushed governments across North America, Europe and allied economies to fund alternative sources of supply, from mine development to downstream separation and magnet manufacturing. Canada's federal and Québec provincial programmes including the Clean Technology Manufacturing Investment Tax Credit that Mont Royal expects to access for Ashram are part of that broader push, alongside similar initiatives in the United States and Australia.

Projects like Ashram matter to this picture not simply because of scale, but because of mineralogy: monazite-hosted deposits with high NdPr distribution and workable heavy rare earth content are comparatively rare outside China, and even rarer at a scale capable of supporting a multi-decade mine life. As Nicholas Holthouse put it when discussing the updated PEA, "This is a project that can have a meaningful and long-lived impact on the development of rare earth industries and technologies within Quebec, Canada, North America and Europe." Whether Ashram converts that resource potential into an operating mine will depend heavily on financing, permitting timelines, and the durability of government support as global rare earth markets continue to reprice around supply chain security rather than cost alone.

TL;DR

The updated Ashram PEA and its supporting NI 43-101 Technical Report give a fuller economic picture of a project with genuine scale: a 30-year mine life, a NdPr-weighted resource base, and post-tax returns that support progression to Pre-Feasibility Study later this year. At the same time, the company's handling of the Naskapi Nation's independent access-corridor initiative, and its continuing engagement with Inuit, Naskapi and Innu communities, will be an important marker of how smoothly infrastructure planning proceeds in a jurisdiction where Indigenous rights and modern treaties carry real weight. The Northern Lights gold till-sampling programme, though smaller in scale, offers a lower-cost, faster-turnaround catalyst that could add optionality beyond the core rare earths story. For investors, the near-term watch list is straightforward: PFS scoping decisions, any formal infrastructure or off-take agreements, and the outcome of the Chateaufort till survey expected from August 2026.

Frequently Asked Questions (FAQs) AI-Generated

Analyst's Notes

Subscribe to Our Channel

Stay Informed