New Pricing Paradigm: How Silver Miners Take Advantage of Low Costs and Financing Partnerships as Supply Shortfall Remain

Silver faces 184M oz supply deficit as industrial demand from solar/EVs surges. Producers show strong margins at $35+ prices with growth projects funded internally.

- Silver market fundamentals have shifted dramatically, with supply deficits reaching 184.3 million ounces and industrial demand from solar panels quadrupling since 2015, driven by renewable energy expansion and technological applications requiring silver's unique electrical conductivity properties.

- Multiple silver producers are demonstrating strong operational performance including Silvercorp Metals with $12 all-in sustaining costs amid $35+ silver prices, and companies like Kootenay Silver advancing high-grade Mexican projects with over 300 million ounces of silver equivalent resources.

- Industrial silver demand continues accelerating across critical sectors, particularly photovoltaics, electric vehicles, 5G infrastructure, and semiconductor applications, creating price-inelastic demand that supports higher price floors beyond traditional precious metals investment flows.

- Recent financing activity exceeds $100 million across multiple silver companies, including Vizsla Silver's $115 million raise, Americas Gold and Silver's $100 million debt facility, and systematic development programs targeting production expansion and resource growth in established mining jurisdictions.

- Silver prices have surged 134% since 2016 from $14 to $32 per ounce, with industry experts expecting continued appreciation toward $35-40 levels as supply constraints persist and the "new paradigm" for silver pricing reflects both monetary demand and irreplaceable industrial applications.

The silver market stands at a critical inflection point where traditional precious metals investment demand converges with accelerating industrial consumption driven by global electrification trends. Recent analysis of silver producers and market fundamentals reveals a compelling investment opportunity supported by structural supply deficits, expanding industrial applications, and favorable pricing dynamics. This assessment examines the evolving silver landscape through the lens of operational companies, market data, and industry developments that collectively signal a transformed investment environment for the white metal.

Fundamental Silver Market Shift

The silver market has experienced a fundamental transformation characterized by persistent supply deficits and expanding demand from multiple sectors. According to the World Silver Survey 2024, the market faced a supply deficit of 184.3 million ounces in 2023, representing one of the largest shortfalls on record. This deficit is projected to grow by 17% in 2024, driven primarily by rising industrial consumption that now represents a critical component of overall silver demand.

Silver's superior electrical conductivity and thermal properties make it irreplaceable in many advanced technologies, while its monetary characteristics continue to attract investment flows during periods of economic uncertainty.

The supply-demand imbalance reflects constraints on new mine development, which faces increasing regulatory hurdles, extended permitting timelines, and technical challenges. Industry analysis suggests a "skinny" project pipeline with limited new supply additions in the near to medium term, providing advantages to existing producers with established operations and proven technical capabilities.

Long-Term Growth: Industrial Application Demand

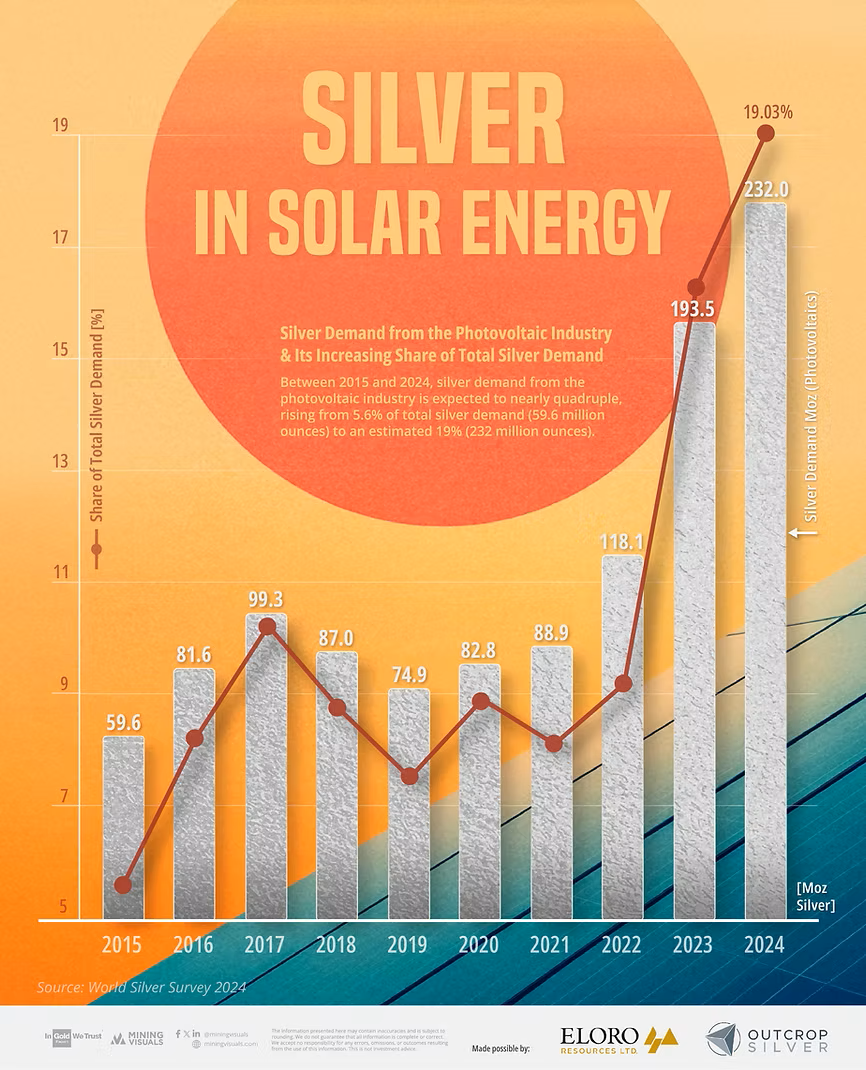

Industrial applications for silver continue expanding across critical sectors of the global economy, creating sustained demand that supports fundamental price appreciation. Photovoltaic silver demand has demonstrated particularly dramatic growth, quadrupling from 59.6 million ounces in 2015 to an estimated 232 million ounces in 2024. This expansion reflects the global transition toward renewable energy, where silver's unique properties are essential for solar panel efficiency and performance.

The renewable energy sector represents just one component of growing industrial silver consumption. Electric vehicle adoption requires significant silver content for electrical systems and battery technology, while 5G infrastructure deployment creates additional demand for telecommunications equipment. The semiconductor industry's expansion, particularly in advanced chip manufacturing, further increases silver requirements for electronic components and specialized applications.

These industrial applications create price-inelastic demand that provides fundamental support for silver prices beyond traditional precious metals investment flows where societal trends toward electrification and technology adoption create sustained industrial demand.

Silver Price Dynamics

Silver prices have demonstrated significant strength, climbing 134% from $14.01 in 2016 to $32.75 per ounce by early 2025. This sustained appreciation reflects the convergence of multiple factors supporting higher price levels, including supply constraints, industrial demand growth, and monetary diversification strategies among investors and institutions.

Industry management teams express optimistic outlooks for continued price appreciation based on fundamental supply-demand dynamics. McDonald from Kootenay Silver noted expectations for prices around $35 within a year, while Silvercorp's management believes the market has entered a new pricing paradigm where "we're unlikely to see prices trade below $30 and it's more likely that we see them touch $40."

While current economic studies use conservative pricing assumptions, mining executives expects higher prices for future studies:

"Silver came off a fairly long bottom that was $18-22. And only recently, just a little over a year ago, we broke out the bound range $22 to over $30. Our belief that in a year's time, you'll probably be talking something like $35." - Kootenay's CEO James McDonald

"Our view is we've been able to be profitable at much lower silver prices, but now that we've hit into this band, we're trading in that $35-36 range." - Silvercorp's President Lon Shaver

This price trajectory reflects recognition of silver's dual nature and the positive attributes of both investment fundamentals and industrial applications. The supply-demand imbalance that exists in silver creates multiple catalysts for price appreciation, particularly as above-ground inventory drawdowns continue and primary mine production struggles to keep pace with growing consumption.

The gold-silver ratio dynamics suggest additional potential for silver outperformance during precious metal bull markets. Historically mean-reverting around 16:1, the ratio remains elevated, indicating significant catch-up potential for silver prices relative to gold. This relationship provides additional upside leverage for silver investments during periods of precious metals strength.

Operational Merits Among Silver Producers

Leading silver producers have demonstrated remarkable operational resilience and cost management capabilities that position them favorably in the current market environment.

Silvercorp Metals exemplifies this operational excellence with all-in sustaining costs of just over $12 per ounce of silver production vs. current silver prices trading in the $35-36 range. The substantial margin provides significant cash generation capacity that funds growth initiatives without requiring external financing.

The company's nearly two-decade track record of profitable silver production from operations in China demonstrates proven ability to generate free cash flow even during periods of depressed silver prices. President Lon Shaver explained the company's strategic position:

"We've currently embarked on a growth project to grow and build the company and add new operating assets. Currently building a new mine in Ecuador and also continually on the hunt for new exciting opportunities."

The company is building a new mine in Ecuador targeting production commencement in 2027 represents strategic geographic diversification while maintaining focus on precious metals production. Construction activities are already underway, with management having signed the first of several major bid packages and progressing through road preparation and infrastructure development.

Kootenay Silver presents another compelling example of discovery and resource expansion potential in Mexico's prolific silver mining districts. The company's recently released 54 million ounce maiden resource at the Columba project demonstrates institutional-grade asset quality with exceptional grades of 284 grams per tonne silver. CEO James McDonald's experience founding Alamos Gold provides credibility for the company's development strategy, which focuses on advancing assets to preliminary economic assessment stage before selling to major mining companies.

The geological advantages at Columba include exceptional preservation within an old volcanic caldera setting, with drilling confirming mineralization extending to 540 meters depth. In addition, Kootenay Silver has seen political and regulatory developments for miners operating in Mexico. McDonald provided an update on recent improvements:

"Been a lot of positive statements and some positive action. So the direction is the temperature if you will has changed. It's a big improvement."

The change in federal government leadership has created a more favorable environment for mining companies, though continued monitoring remains essential.

Technological Innovation

Silver producers are implementing innovative extraction and processing technologies that enhance operational efficiency and reduce environmental impact. Companies processing tailings and historical mineral stockpiles benefit from significantly lower operational costs compared to traditional mining operations, with extraction costs often ranging from $1-2 per tonne versus $30-200 per tonne for underground mining.

Cerro de Pasco Resources exemplifies this approach with its Quiulacocha tailings project in Peru, which targets reprocessing of historical tailings containing an estimated 423 million ounces of silver equivalent. The company's submersible pump extraction system eliminates the need for traditional mining methods, operating without dust, noise, or explosives while providing environmental remediation benefits.

Drillings at Quiulacocha has confirmed average grades of 5.5 oz/ton silver equivalent, including valuable metals like gallium and indium. The project's potential economics demonstrate the viability of tailings reprocessing, with base case scenarios projecting significant profit margins based on conservative recovery assumptions and current metal prices.

These technological approaches provide competitive advantages through lower operational costs, reduced environmental impact, and access to resources that would be uneconomical through traditional mining methods. The environmental benefits of tailings reprocessing align with increasing focus on sustainable mining practices and circular economy principles.

Financing Activities and Capital Deployment

The silver sector has demonstrated strong access to capital markets, with significant financing activities within the past months supporting growth initiatives and development programs.

- Vizsla Silver completed a substantial $115 million financing to advance exploration and development of the Panuco Project and Santa Fe Project in addition to potential future acquisitions.

- Americas Gold and Silver secured a $100 million secured for a term loan facility to fund growth and development capital spending at the Galena Complex critical to our plans to increase development rates and tonnage mined, and reduce unit costs at Galena.

- Silver Tiger closed a $15 million bought deal financing for the El Tigre Project in Mexico.

- Santacruz Silver continues structured payments to Glencore under an Acceleration Plan. The plan is expected to generate US$40 million in savings and underscores the company’s commitment to financial discipline and long-term value creation. The strong relationship with Glencore highlights strategic priorities in Bolivia and beyond of Santacruz' portfolio

- Outcrop Silver announced funding partnership with Silver Mines for its Kramer Hills which claims covering approximately 48 km2 surrounding a patented claim covering the historic Shaherald oxide gold mine. Outcrop Silver highlights their strategy of unlocking value from non-core assets while focusing capital on expanding the high-grade Santa Ana silver project.

These transactions demonstrate multiple pathways for value creation and risk management within the silver sector. This financing activities reflects investor confidence in silver sector fundamentals and provides companies with resources to advance development projects during favorable market conditions. The structured approach to capital deployment, including milestone-based funding tranches, demonstrates disciplined financial management while maintaining operational flexibility.

The Investment Thesis for Silver

- Fundamental Supply-Demand Imbalance: Invest in silver during a period of structural supply deficits exceeding 180 million ounces annually, with limited new mine development and declining ore grades globally creating persistent shortfalls that support higher prices.

- Industrial Demand Growth: Position for accelerating silver consumption across renewable energy, electric vehicles, 5G infrastructure, and semiconductor applications, where silver's unique properties create price-inelastic demand that provides fundamental price support beyond traditional precious metals flows.

- Operational Excellence Access: Target established silver producers with proven cost structures below $15 per ounce all-in sustaining costs, substantial profit margins at current $35+ silver prices, and self-funding growth capabilities that eliminate dilution risks.

- Geographic and Asset Diversification: Focus on companies with operations across multiple jurisdictions, particularly Mexico's prolific silver districts, Peru's established mining regions, and emerging opportunities in Ecuador, reducing single-country political and operational risks.

- Strategic Metal Exposure: Seek silver producers with gallium, indium, and other critical metal byproducts that enhance strategic value and provide supply chain security benefits as China dominates production of these essential technology metals.

- Technological Innovation Benefits: Consider companies utilizing advanced extraction methods, tailings reprocessing technologies, and environmental remediation approaches that provide operational cost advantages and align with sustainable mining principles.

- Capital Market Access: Prioritize companies with demonstrated ability to access growth capital through debt and equity markets, enabling systematic development programs and strategic acquisitions during favorable market conditions.

- Price Leverage Opportunity: Capitalize on silver's historical outperformance during precious metal bull cycles, with the gold-silver ratio suggesting significant catch-up potential and multiple industry executives expecting $35-40 silver prices in the near term.

- Multiple Exit Strategies: Target junior developers with clear value realization strategies through asset sales to major mining companies, typically when resources exceed 75-100 million ounces and preliminary economic assessments demonstrate positive economics.

- Thematic Alignment: Align with global electrification trends, renewable energy adoption, and technology infrastructure development that create sustained industrial silver demand independent of monetary policy or economic cycles.

Investment Implications and Market Outlook

The convergence of supply constraints, industrial demand growth, and technological innovation creates a compelling investment environment for silver and silver-producing companies. The metal's dual nature as both a precious metal and critical industrial commodity provides multiple demand drivers that support sustainable higher price levels, while operational companies demonstrate strong cost management and growth capabilities.

Recent financing activity exceeding $100 million across multiple companies reflects investor confidence in sector fundamentals and provides resources for systematic development programs. The combination of established producers with low-cost operations and emerging developers with high-grade discoveries offers investors multiple approaches to silver market exposure, from stable cash flow generation to resource expansion potential.

The strategic importance of silver in renewable energy and advanced technology applications ensures continued industrial demand growth, while supply constraints from limited new mine development and declining ore grades support favorable pricing dynamics. Industry management teams' optimistic price projections toward $35-40 levels reflect recognition of these fundamental shifts and the establishment of a new paradigm for silver valuation.

Analyst's Notes

Subscribe to Our Channel

Stay Informed