Oil Inventory Drawdowns & Gold Losses as Energy Inflation Drives December Hike Odds

Oil's inflation pass-through has trapped the Fed between a rate hike and a recession, and gold is pricing the wrong outcome for most retail investors.

- Global oil inventories fell by an average of 8.5 million barrels per day in Q2 2026, the largest drawdown since the COVID pandemic, keeping Brent crude near $94/barrel on June 5 despite progress in ceasefire talks.

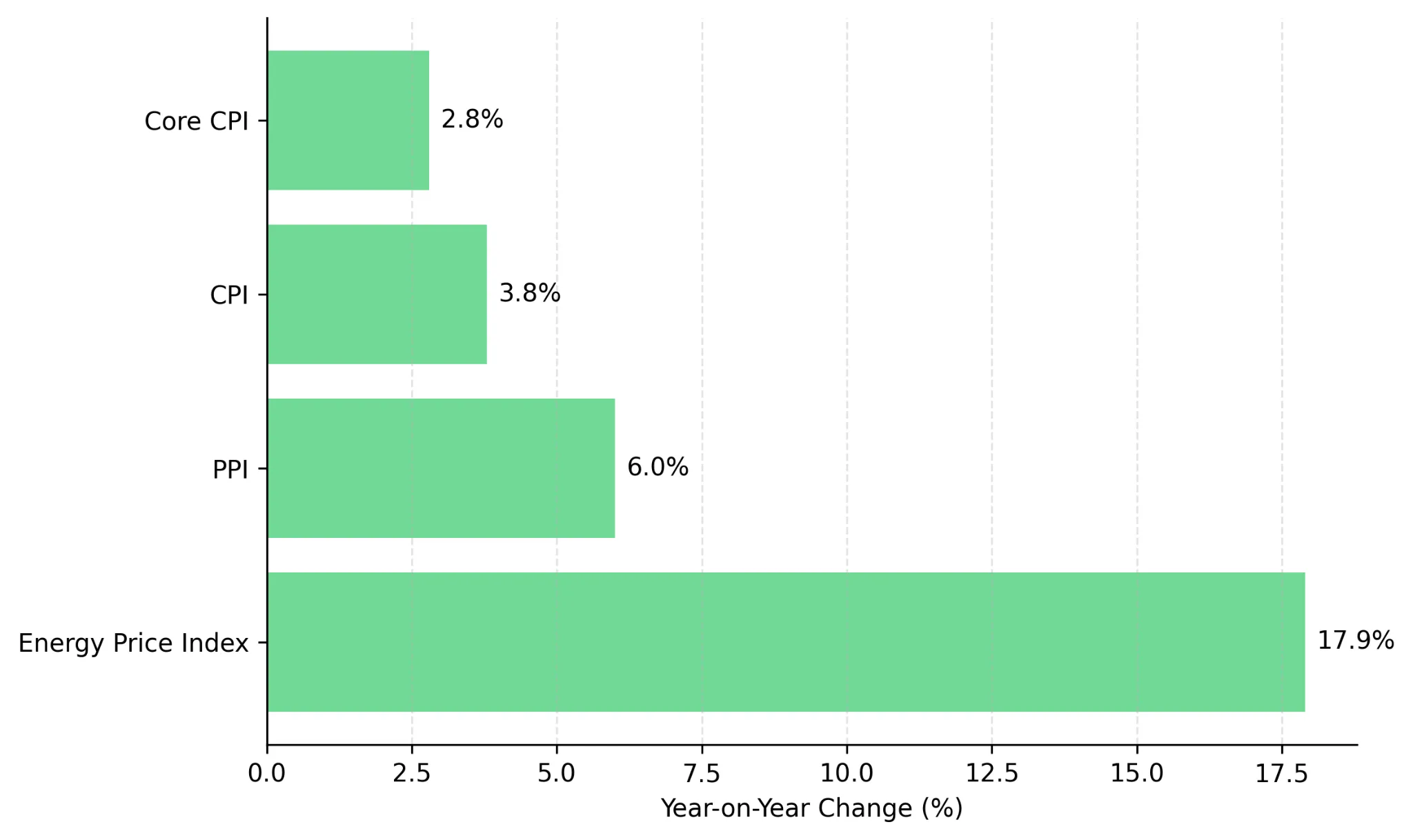

- With CPI at 3.8% year-on-year and PPI at 6%, the Fed kept rates at 3.50%-3.75% on April 29, while markets now price a 54.1% probability of a rate hike at the December 2026 FOMC meeting.

- Spot gold has fallen more than 10% from its January 2026 high near $5,595/oz to about $4,470 as higher oil prices have lifted inflation expectations and real yields, outweighing safe-haven demand.

- Saudi Aramco CEO Amin Nasser said that even if Gulf shipping lanes fully normalize today, oil market rebalancing will not be completed until 2027, extending inventory shortages that continue to support oil prices.

- May nonfarm payrolls, due at 8:30 a.m. ET on June 5, will influence expectations for a December Fed rate decision. A payrolls reading above 120,000 would increase the likelihood of a December rate hike and pressure gold toward $4,300, while a reading below 80,000 would increase recession concerns and could push WTI below the $88 support level identified by IG analyst Tony Sycamore.

Oil Inventory Drawdowns & Inflation Pressure on Gold and Bonds

During the week of June 2, oil retreated from recent highs, gold fell for a third consecutive week, and US equities reached record highs. The S&P 500 closed at a record 7,599.96 on June 2 despite rising oil prices. Spot gold traded near $4,470, below its 21-day moving average of about $4,565 and 50-day moving average of about $4,635, signaling continued short-term price weakness. Brent crude traded near $94/barrel on June 3, while WTI rose more than 6% for the week on progress in Gulf shipping-lane negotiations.

The US Energy Information Administration reported that global oil inventories fell by an average of 8.5 million barrels per day in Q2 2026 and that pre-conflict production and trade patterns are unlikely to normalize before late 2026 or early 2027, even as shipping lanes reopen. Delayed supply normalization increases the risk that higher energy costs continue feeding inflation, supporting higher bond yields and keeping pressure on interest-rate-sensitive assets such as gold.

Oil-Driven Inflation & Rising Fed Rate-Hike Risk

Oil affects financial markets primarily through inflation expectations and Fed policy rather than through direct energy costs. Brent crude averaged $117/barrel in April 2026, its highest monthly average since June 2022. Brent fell toward $94 in May, but inflation continued to reflect the earlier price spike. April CPI rose 3.8% year-on-year, core CPI reached 2.8%, and PPI increased 6%, its largest gain since December 2022. The energy price index rose 17.9% year-on-year and accounted for more than 40% of the CPI increase. Higher oil prices have fed through to inflation and bond yields, increasing pressure on interest-rate-sensitive assets.

The Fed kept rates at 3.50%-3.75% on April 29, citing elevated inflation partly driven by higher global energy prices. CME FedWatch data shows a 99.4% probability of no rate change on June 17 and a 54.1% probability of a 25-basis-point rate hike in December. Higher energy prices are keeping inflation above target, limiting the case for rate cuts while increasing expectations for further tightening. UCLA Anderson Forecast noted that headline CPI rose from 2.4% to 3.8% in two months and projected inflation could reach 4.5% year-on-year by the end of 2026, increasing the risk that rates remain higher for longer.

Delayed Oil Supply Recovery & Reduced Fed Rate-Cut Potential

Oil prices now depend more on inventory replenishment than on diplomatic developments, with supply recovery constrained by operational logistics. On Saudi Aramco's Q1 earnings call, CEO Amin Nasser said that even if the Strait of Hormuz reopened immediately, oil market normalization could extend into 2027. Delayed supply normalization increases the risk that energy-driven inflation remains elevated, limiting the scope for near-term Fed rate cuts.

The EIA Weekly Petroleum Status Report, published every Wednesday at 10:30 a.m. ET, provides the clearest indication of whether oil inventories are tightening or recovering. IG analyst Tony Sycamore says a weekly crude inventory draw above 4 million barrels is needed to keep WTI above its low-$80s support level. The next report is scheduled for June 11, 2026.

Higher Energy Costs & Margin Pressure Across Key Sectors

Higher energy costs are putting the greatest margin pressure on airlines, consumer discretionary retailers, and manufacturers with limited pricing power. US gasoline prices rose to $4.48 per gallon from $2.98 before the conflict, increasing transportation costs by about 50% and reducing margins across fuel-intensive industries. For investors in broad equity ETFs, the risk is concentrated in these sectors rather than in headline index performance, which remains supported by large technology stocks.

Utilities, healthcare companies, and essential food producers can often pass higher costs on to customers because demand remains relatively stable. Companies selling discretionary goods face greater margin pressure because higher prices can reduce demand. Rising energy costs can reduce both margins and revenue for discretionary businesses as consumers cut spending.

The June 5 payrolls report will influence the June 17 FOMC decision, leaving uncertainty around both interest rates and oil prices until those events occur. Positioning for a specific Fed outcome before the payrolls release carries elevated forecast risk. Investors can reduce exposure to energy-sensitive sectors such as airlines, chemicals, and logistics, while recognizing that gold faces two risks: higher rates that pressure prices and weaker growth that could reverse the decline.

Fed Policy Risk & Key Gold-Oil Price Levels

Cleveland Fed President Beth Hammack said on June 4 that additional policy tightening may be necessary if inflation remains elevated, while CME FedWatch data shows traders assign a greater than 50% probability to a 25-basis-point rate hike in December. A December hike probability above 50% favors domestically focused energy producers over non-yielding assets such as gold and silver and supports a cautious view on energy-intensive industrials. Silver has fallen about 20% since late February as higher oil prices increased inflation expectations and strengthened expectations for higher interest rates.

A weaker-than-expected payrolls report on June 5 and a dovish signal from Chair Warsh on June 17 would reduce expectations for further Fed tightening. If May nonfarm payrolls come in below 80,000 and Warsh omits rate-hike language from the June 17 statement, CME FedWatch could price December hike odds below 40%, a level associated with falling bond yields. Lower bond yields would support gold prices. UBS analyst Giovanni Staunovo said expectations for a weaker US dollar, lower real interest rates, continued central-bank buying, and US election uncertainty could support gold demand and lift prices toward $5,900/oz by late 2026. A weak jobs report would also increase recession risk, which could weigh on oil prices while improving relative support for gold.

Three indicators to monitor: May nonfarm payrolls on June 5, which will shape Fed rate expectations; the EIA Weekly Petroleum Status Report, where a crude inventory draw above 4 million barrels could keep WTI above $88; and CME FedWatch, where December hike odds above 60% would pressure gold while odds below 40% would support it. A close below $4,300 would increase the risk of a move toward $3,800 in gold.

Analyst's Notes

Subscribe to Our Channel

Stay Informed