Quadruple Silver Demand Growth Within the Decade Depict Fundamentals Beyond Supply Dynamics

Silver faces 206M oz deficit as solar/EV demand surges while 70% byproduct supply stays inelastic. Companies report high-grade discoveries, strong margins.

- The silver market faces an unprecedented structural crisis with a projected 206 million ounce supply deficit in 2025, marking the eighth consecutive year of market imbalance driven by fundamental mismatches between industrial consumption and constrained mine output.

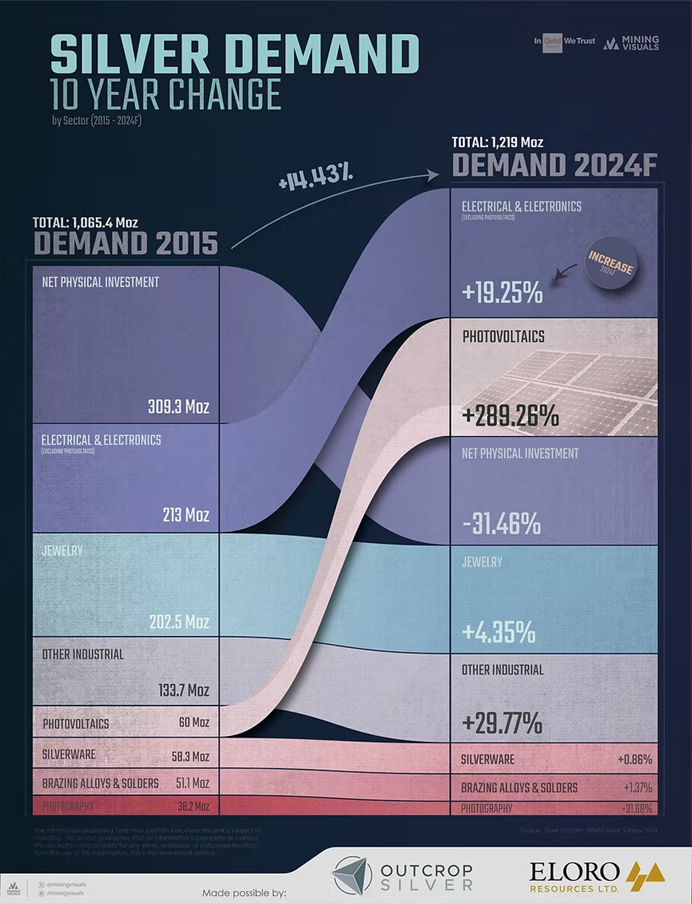

- Industrial demand has transformed dramatically due to the green energy transition, with solar photovoltaic production representing nearly 400% growth from 2015 vs 2024 that extends across electric vehicles, 5G infrastructure, and grid modernization projects.

- Supply constraints persist because approximately 70% of global silver production comes as a byproduct of base metal mining operations, creating inelastic supply response where traditional price signals cannot stimulate rapid production increases even at decade-high prices near $38 per ounce.

- Mining companies are achieving operational excellence through cost reductions, high-grade discoveries, and strategic development approaches that position them to capitalize on sustained demand growth while maintaining competitive advantages in rising cost environments.

- Jurisdictional considerations have become critical for silver investment success, with established mining regions like Mexico experiencing improved regulatory environments while strategic mineral recognition drives policy support for domestic production and secure supply chains.

The silver market is experiencing a fundamental transformation driven by unprecedented industrial demand growth coinciding with structural supply limitations. This confluence of factors has created what industry analysts describe as the most compelling silver investment environment in decades, characterized by persistent supply deficits, inelastic production response, and accelerating consumption from critical green energy technologies.

Industrial Demand Acceleration from Green Energy Transition

The green energy transition has fundamentally altered silver's demand profile, creating secular consumption growth that extends well beyond traditional cyclical patterns. Solar photovoltaic production has emerged as the dominant industrial driver, consuming 232 million ounces in 2024 compared to just 60 million ounces in 2015, representing nearly 400% growth in less than a decade.

The International Energy Agency projects massive increases in global solar capacity, supported by U.S. Inflation Reduction Act credits and European Union Green Deal funding, ensuring sustained silver consumption through the 2030s. Unlike cyclical industrial applications, these green energy demands represent permanent shifts in global energy infrastructure with limited substitution potential. Silver's role extends across multiple simultaneous technology adoptions. Electric vehicle production, charging infrastructure, 5G telecommunications, and grid modernization projects all require significant silver content per unit, creating compounding demand pressure as these technologies scale simultaneously.

Critically, green energy applications demonstrate reduced price sensitivity compared to traditional industrial uses. Solar manufacturers and electric vehicle producers prioritize supply security and performance over marginal cost differences, maintaining steady consumption even during price volatility period which distinguishes silver from other industrial metals where demand typically declines at elevated price levels.

The Deepening Supply-Demand Imbalance

Silver markets are approaching a critical inflection point with projected supply shortfalls that dwarf previous cycles. The silver market faces a 206 million ounce supply deficit in 2025, representing the eighth consecutive year of market imbalance. This structural deficit reflects not a temporary disruption but a fundamental mismatch between growing industrial consumption and constrained mine output.

The core challenge stems from silver's unique production profile, where approximately 70% of global output comes as a byproduct of base metal mining operations focused on copper, lead, and zinc. This production structure means that traditional price signals alone cannot stimulate rapid supply increases, creating persistent pricing pressure even as silver approaches decade highs near $38 per ounce. Mining companies are adapting their strategies to capitalize on this environment.

Santacruz Silver exemplifies operational resilience through diversified asset portfolios and flexible sourcing strategies. Despite temporary challenges at the Bolivar mine, the company maintained revenue stability through strategic ore sourcing and efficiency gains across multiple operations. The company reported Q2 2025 revenues of $73.3 million with gross profits of $25.3 million, representing a 59% year-over-year increase.

Executive Chairman and CEO Arturo Préstamo emphasized the company's strategic positioning:

"Our second quarter results reflect the strength and stability of Santacruz's business model. We achieved solid revenue growth and significantly improved profitability, with net income and adjusted EBITDA both showing substantial gains."

The company's cash cost per silver equivalent ounce of $19.48 represents a 10% decrease year-over-year, demonstrating operational improvements even amid challenging market conditions. This cost performance, combined with strengthened balance sheet positions, provides substantial operating leverage to silver price appreciation.

Development in Growth Strategies

Silver development companies are implementing innovative strategies to address supply constraints while positioning for sustained demand growth. These companies represent attractive investment opportunities through their combination of near-term production capabilities and district-scale resource potential.

Vizsla Silver demonstrates how advanced development projects can capitalize on current market conditions. The company's Panuco Project in Mexico hosts 361 million ounces of silver equivalent resources with a PEA showing AISC of $9.40 per ounce and post-tax net present value of $1.1 billion. CEO Michael Konnert emphasizes the importance of expedited development:

"The faster we can get into cash flow the better and once we're in that construction period it is a relatively short construction period following that we'll be producing 20 million ounces of silver equivalent in those first two years as per the preliminary economic assessment."

The company's total cash is now over $200 million after a recent $100 million financing positions Vizsla to advance through construction without dilutive equity raises during critical development phases. This financial strength provides significant advantages in current market conditions where capital access remains challenging for many development projects.

GR Silver Mining has implemented a compelling dual-asset approach combining near-term revenue generation with significant exploration upside with two complementary assets within a 5-kilometer radius in Mexico's established silver districts. The Plomosas historic underground mine maintains existing permits, infrastructure, and 7.4 kilometers of developed tunnels, while the San Marcial discovery area offers substantial expansion potential with current resources representing only 20% of identified geophysical anomalies.

GR Silver's C$13.8 million financing reflects growing investor appetite for silver companies demonstrating clear production pathways alongside substantial resource expansion potential. CEO Marcio Fonseca notes improved operating conditions:

"I go to Mexico pretty much every month and I've been doing business in Mexico for more than 20 years. We have seen many cycles but recently with the new government I've seen a more favorable and more positive environment for the development of mining projects."

The company's bulk sampling and pilot plant strategy addresses investor demands for earlier cash flow while building toward larger-scale operations leveraging existing infrastructure to minimize development risks and capital requirements typically associated with greenfield projects.

Interview with Marcio Fonseca, President & CEO of GR Silver Mining

High-Grade Discovery Success

Avino Silver and Gold's recent drilling results at La Preciosa demonstrate the quality of silver deposits being developed in Mexico's established mining districts. The company reported intercepts of 1,638 g/t silver over 7.90 meters, including exceptional grades of 15,352 g/t silver over 0.37 meters, significantly exceeding current resource model averages.

President and CEO David Wolfin highlighted the discovery's significance:

"We are delighted to report excellent grades on all four holes at La Preciosa. The intercept grades are significantly higher than the average grades outlined in our current resource, highlighting the potential we aim to capture by using underground mining methods."

These results demonstrate how established mining districts continue yielding high-grade discoveries despite extensive historical exploration. The company's integration of new geological understanding with modern mining techniques creates opportunities to unlock previously unrecognized value in proven terrains.

Americas Gold & Silver exemplifies this trend through operational optimization at their Cosalá Operations, which are positioned to deliver approximately 2.5 million ounces annually by 2026. The company maintains exceptionally low all-in sustaining costs of $10.80 per ounce while achieving 80% silver revenue exposure by 2025, creating significant leverage to silver price appreciation. The company's recent drilling at the Galena Complex identified high-grade extensions of the 149 Vein, with intercepts including 24,913 g/t silver and 16.9% copper over 0.21 meters. CEO Paul Andre Huet emphasized:

"The identification of this high-grade copper-silver-antimony extension to the 149 Vein is an exciting development that builds on our ongoing success in unlocking additional value at the Galena Complex."

Silver mining companies are achieving operational improvements that enhance margins while building production capacity. These operational advances create competitive advantages in rising cost environments while demonstrating management teams' ability to execute complex development programs.

Jurisdictional Considerations and Resource Security

Jurisdictional diversification has become increasingly important for silver investors as resource nationalism and trade tensions affect global supply chains. Mexico remains the world's largest silver producer, hosting eight of the fourteen largest silver districts globally, but recent policy changes have created opportunities for companies with established positions.

GR Silver Mining benefits from Mexico's improved regulatory environment for underground operations. CEO Marcio Fonseca's extensive Mexican experience provides valuable insights:

"We expect silver to continue to outperform, but there will be some volatility and we believe that's important to define a project that can really survive through different cycles because a mine project is probably seven to ten years of mine life."

Resource scarcity extends to jurisdictions capable of supporting profitable silver mining operations. Vizsla Silver and Endeavour Silver CEOs emphasized that high-quality silver deposits primarily exist in Mexico and Peru, limiting options for companies seeking growth opportunities. In a panel discussion, Konnert observed:

"There's really one or two - Peru & Mexico. I'd say Mexico, of course, is the main one there. It's the number one producer of silver in the world."

Mexico experienced permitting difficulties for new open-pit operations under the previous AMLO administration created supply constraints despite the country's dominant market position. With the current administration under President Claudia Scheinbaum, industry leaders note improvements observing more constructive engagement from Mexican authorities regarding mining permits and operations.

Michael Konnert, CEO of Vizsla Silver & Dan Dickson, CEO of Endeavour Silver

This jurisdictional expertise becomes particularly valuable as silver achieves recognition as a strategic mineral for energy security. Countries increasingly view reliable silver supply chains as critical for electric vehicle adoption and solar deployment, creating policy support for domestic production and strategic partnerships with allied nations.

The Investment Thesis for Silver

- Structural Supply Deficit: Target companies with existing production capacity or advanced development projects that can respond quickly to sustained demand strength, as new primary silver development faces 7-10 year lead times

- Industrial Demand Growth: Focus on companies with exposure to solar, electric vehicle, and semiconductor supply chains, as these sectors demonstrate sustained consumption growth with limited price sensitivity

- Cost Structure Advantage: Prioritize producers with all-in sustaining costs below $15 per ounce and development projects demonstrating sub-$12 operating cost profiles to maximize margin expansion during price appreciation

- Resource Quality and Scale: Invest in companies controlling district-scale mineralization in established silver provinces, particularly those with underground mining potential offering higher grade and longer mine life profiles

- Jurisdictional Diversification: Balance portfolio between established silver-producing regions (Mexico, Peru) and stable jurisdictions (United States, Canada) to optimize resource access while managing regulatory risks

- Financial Positioning: Select companies with strong balance sheets, adequate development funding, and management teams with proven track records in silver development and operations

- Exploration Leverage: Consider companies with substantial untested anomalies or district consolidation opportunities that provide option value for resource expansion beyond current defined resources

- Environmental and Social Governance: Prioritize companies with demonstrated community engagement, environmental remediation components, and sustainable mining practices that reduce permitting and operational risks

Silver's investment proposition in 2025 centers on unprecedented structural scarcity meeting accelerating industrial adoption across critical green energy technologies. The combination of inelastic supply response, sustained deficit conditions exceeding 200 million ounces annually, and growing institutional recognition of silver's dual industrial-monetary characteristics creates compelling opportunities for investors seeking exposure to both defensive positioning and growth-oriented allocation.

Companies with established production capabilities, advanced development assets in stable jurisdictions, and management teams capable of executing complex projects in challenging markets are positioned to benefit substantially from this fundamental repricing of global silver markets.

Analyst's Notes

Subscribe to Our Channel

Stay Informed