Sharp Surge in Praseodymium-Neodymium Prices Signals Deepening Scarcity Premium in Rare Earth Supply Chains

NdPr prices surge 14% weekly, up 40% YTD as China export controls tighten supply. Western govt investment accelerates rare earth supply chain diversification.

- Praseodymium-Neodymium prices surged 13–14% in a single week, with oxide prices up over 40% year-to-date, underscoring structural supply strain and demand momentum in electrification.

- China's export controls and quota discipline continue to fragment the rare earth element market, creating ex-China scarcity premiums and accelerating efforts to build independent supply chains.

- Western government capital deployment through US$1 billion from the Department of Energy and the European Union Critical Raw Materials Act is reshaping the funding landscape for rare earth processing outside China.

- Energy Fuels' White Mesa Mill and heavy mineral sand partnerships position it as the only United States facility producing separated rare earth element oxides at scale, with near-term catalysts across NdPr, dysprosium, and terbium.

- Investor takeaway: NdPr's surge is a short-term price catalyst reinforcing the long-term structural thesis that diversified rare earth element supply chains are critical to capturing scarcity-driven returns.

A Rare Earth Price Spike That Matters

The rare earth element market witnessed an extraordinary price movement in late 2025 as praseodymium-neodymium oxide prices surged 13.6% in a single week, while NdPr alloy prices climbed 14%. This dramatic escalation brought cumulative year-to-date gains to over 40%, marking one of the most significant price movements in the traditionally stable rare earth complex.

The magnitude of this price surge stands in stark contrast to the typical behavior of rare earth element markets, where pricing tends to move incrementally due to supply chain opacity and limited spot trading. Unlike base metals or precious metals markets characterized by daily volatility, rare earth elements typically experience gradual price adjustments over months or quarters.

Investment Implications Beyond Short-Term Trading

For institutional investors, this price spike represents more than a short-term trading opportunity. The velocity and scale of the NdPr surge reflects underlying structural stress in supply chains that have operated under Chinese dominance for decades. As demand from electrification technologies accelerates and supply diversification efforts gain momentum, these price dislocations may become more frequent and pronounced.

The timing of this surge aligns with broader geopolitical realignments in critical mineral supply chains. Government initiatives across the United States, European Union, and allied nations are redirecting capital toward rare earth element projects outside China, creating new demand for Western-sourced materials even as traditional supply channels face increasing restrictions.

Demand from Electrification & Decarbonization

The surge in NdPr pricing reflects the fundamental role these elements play in permanent magnet motors that power electric vehicle drivetrains. Unlike copper coil alternatives, neodymium-based permanent magnets deliver superior power-to-weight ratios and energy efficiency that remain unmatched in high-performance applications. Each electric vehicle requires approximately 200-400 grams of NdPr depending on motor size and configuration.

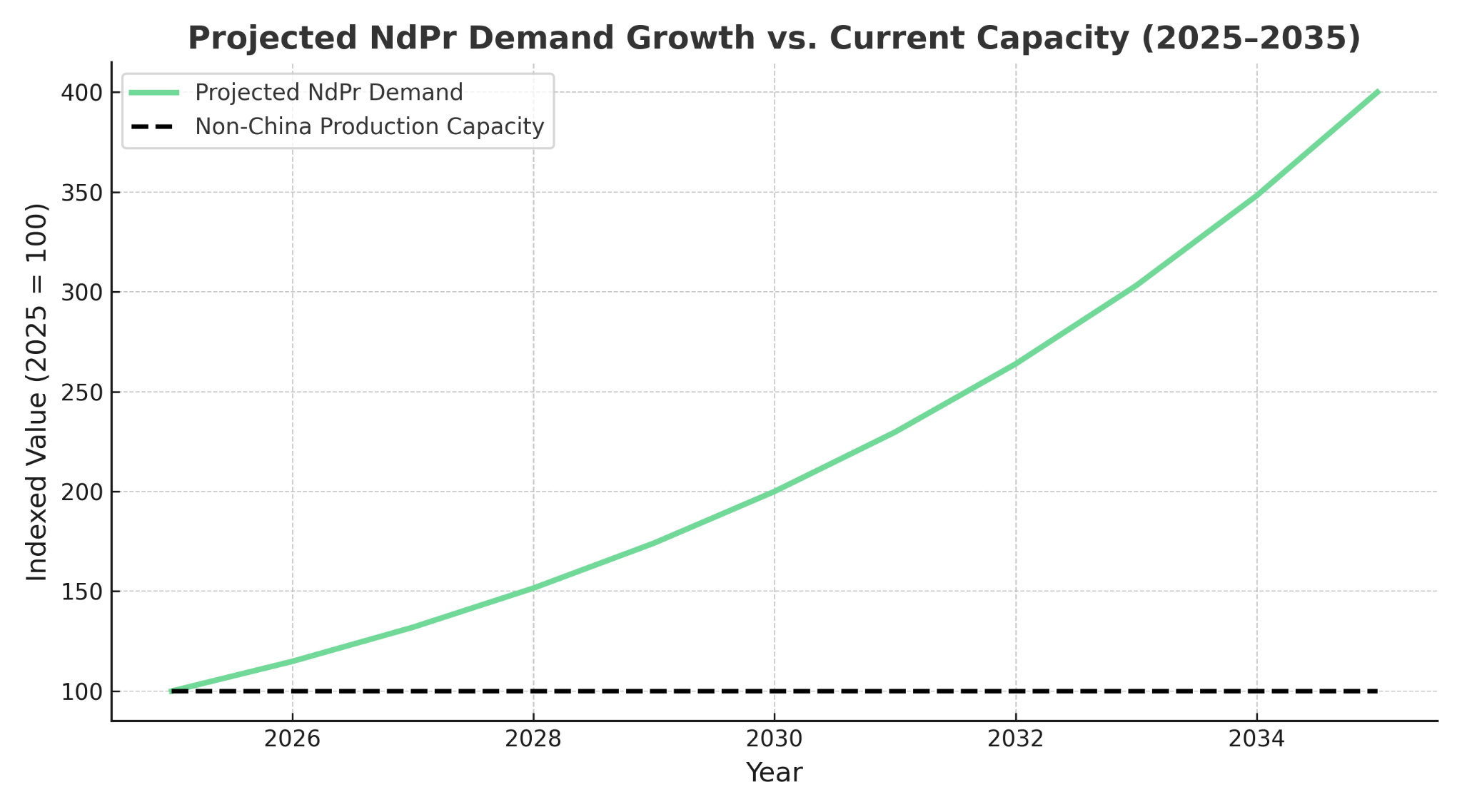

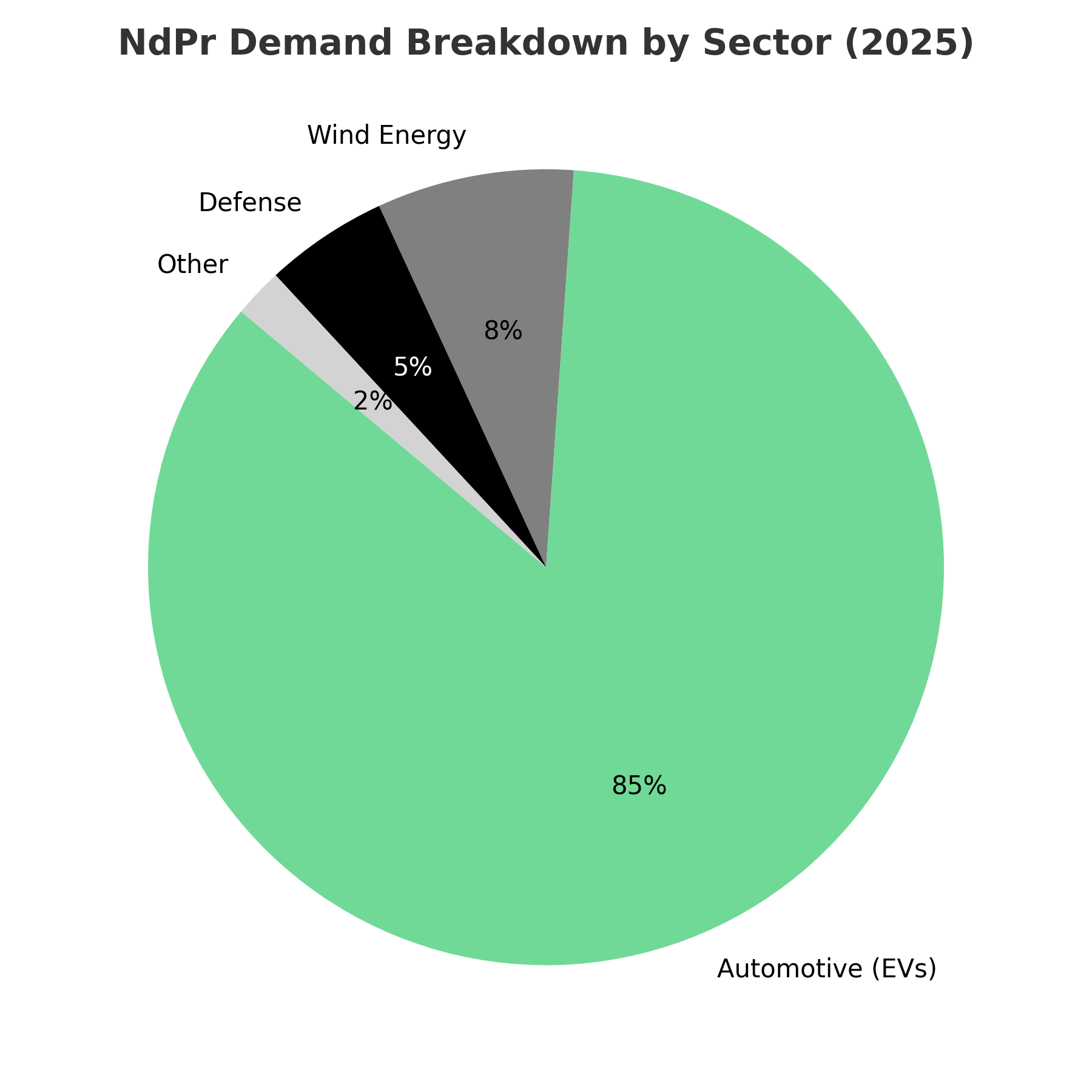

Global electric vehicle adoption continues to accelerate beyond initial forecasts, with International Energy Agency projections indicating 130 million electric vehicles on roads by 2030. This trajectory translates to cumulative NdPr demand growth of 300% over the next decade, far exceeding current production capacity outside China. The automotive sector now represents approximately 85% of total NdPr consumption, making electric vehicle penetration rates the primary driver of pricing dynamics.

Automotive manufacturers have explored alternatives to permanent magnet motors, including copper coil induction systems, but performance compromises in efficiency and weight have limited adoption in premium vehicle segments. Tesla's recent pivot back to permanent magnet motors in Model 3 production underscores the technical superiority of NdPr-based systems for mass market applications.

Wind & Renewable Energy Scale-Up

Beyond automotive applications, NdPr demand from wind turbine generators represents the second-largest consumption sector. Offshore wind installations, in particular, rely heavily on permanent magnet generators due to maintenance accessibility challenges in marine environments. Each offshore wind turbine requires 200-600 kilograms of rare earth elements, with NdPr comprising 20-25% of this requirement.

International Energy Agency and McKinsey forecasts project global wind capacity tripling by 2035, driven by government renewable energy mandates and declining installation costs. The offshore wind segment, which demonstrates higher rare earth intensity per megawatt of capacity, is expected to grow at compound annual growth rates exceeding 20% through 2030.

Strategic Demand for Dysprosium & Terbium Additives

While NdPr constitutes the bulk of rare earth demand by volume, dysprosium and terbium additives play critical roles in high-performance motor applications. These heavy rare earth elements enhance magnet coercivity and thermal stability, enabling operation in extreme temperature environments including aerospace and defense applications.

Defense applications, including fighter jet actuators and precision guidance systems, require dysprosium and terbium specifications that cannot be substituted with lighter rare earth elements. The Pentagon's establishment of strategic stockpile requirements and long-term supply agreements reflects recognition of these materials' importance to national security infrastructure.

Supply-Side Dynamics: China's Strategic Leverage

China's approach to rare earth element market management has evolved from production quotas to sophisticated export control mechanisms that create regional price divergence. July 2025 export quotas were issued with reduced transparency, while the April 2025 export license regime introduced restrictions on seven rare earth elements including NdPr, dysprosium, and terbium.

These export controls have effectively fragmented global rare earth markets, with Chinese domestic prices remaining relatively stable while ex-China pricing experiences significant volatility. The 40% year-to-date increase in NdPr pricing primarily reflects supply constraints outside China rather than fundamental production cost inflation.

Chinese rare earth production capacity remains substantial, with domestic consumption absorbing approximately 60% of total output. However, export restrictions have reduced international market liquidity, amplifying price responses to modest supply or demand changes. The resulting market fragmentation creates arbitrage opportunities for companies with processing capabilities outside China.

Myanmar & Opaque Supply Risks

Myanmar's rare earth production, concentrated in rebel-held territory within Shan State, represents a significant source of supply uncertainty. Heavy mineral sand operations in these regions operate outside formal regulatory frameworks, creating environmental, social, and governance risks for institutional investors seeking exposure to rare earth supply chains.

Recent escalation of conflicts in Myanmar has disrupted approximately 15% of global heavy rare earth supply, contributing to pricing pressure for dysprosium and terbium. The ethical implications of Myanmar-sourced rare earth elements have prompted several Western manufacturers to seek alternative supply sources, further constraining ex-China availability.

Scarcity Premiums Outside China

Rising ex-China scarcity premiums reflect investor preference for rare earth supply from stable jurisdictions with transparent regulatory frameworks. Projects in the United States, Australia, and Canada now command valuation premiums of 20-30% compared to equivalent deposits in higher-risk jurisdictions.

This jurisdiction premium has accelerated capital formation for Western rare earth projects, with government backing providing additional investment certainty through loan guarantees, tax incentives, and strategic partnerships.

Policy & Capital Flows: Governments Step Into the Market

United States Department of Energy & Industrial Policy

The United States Department of Energy's commitment of nearly US$1 billion to critical mineral supply chain development represents the largest government intervention in rare earth markets since the 1980s. This funding targets rare earth separation facilities, downstream processing capabilities, and strategic reserve purchases designed to reduce import dependence.

The Pentagon's establishment of a NdPr pricing floor at US$110 per kilogram for defense procurement contracts provides investment certainty for domestic production projects. This pricing mechanism, coupled with Buy America requirements for defense applications, creates a guaranteed market for United States-produced rare earth oxides regardless of Chinese pricing strategies.

Government Loan Guarantee Programs

Department of Energy loan guarantee programs have approved US$2.8 billion in conditional commitments for rare earth processing facilities, with additional applications under review totaling US$6.2 billion. These government-backed financing structures significantly reduce project development risk and enable private capital participation at scale.

European Union & Allied Initiatives

The European Union Critical Raw Materials Act establishes binding targets for member states to source 10% of rare earth consumption from domestic processing by 2030. This mandate, combined with US$8.3 billion in allocated funding, is driving investment in separation facilities across multiple European countries.

European Union-Australia cooperation agreements facilitate heavy mineral sand project development, with joint financing mechanisms supporting rare earth processing infrastructure in both jurisdictions. These partnerships leverage Australia's resource endowments with European processing expertise and market access.

Private Capital & Mergers and Acquisitions Activity

Capital formation in rare earth projects has accelerated dramatically, with private equity and strategic investors deploying US$4.7 billion across 23 projects in 2024-2025. Valuation premiums for companies with near-term production capabilities have increased 40-60% as supply scarcity becomes apparent.

Merger and acquisition activity reflects strategic positioning by downstream manufacturers seeking supply chain security. Recent transactions include major automotive manufacturers acquiring equity stakes in rare earth processing companies and permanent magnet producers establishing vertical integration through upstream acquisitions.

Company Case Study: Energy Fuels in Context

Energy Fuels operates the White Mesa Mill in Utah, representing the only United States facility currently producing separated rare earth element oxides at commercial scale. This 2,000 tonnes per day processing facility provides unique capabilities for rare earth separation using solvent extraction technology proven across uranium and rare earth applications.

The company's global heavy mineral sand project portfolio includes the Toliara Project in Madagascar, Donald Project in Australia, and Bahia Project in Brazil. These assets provide long-term rare earth feedstock security with combined measured and indicated resources exceeding 1.2 million tonnes of total rare earth oxides.

Energy Fuels' Pinyon Plain uranium mine serves as a revenue anchor, generating cash flow that supports rare earth development activities without requiring external financing. Current uranium production of approximately 300,000 pounds annually provides operational flexibility and balance sheet strength during rare earth market development phases.

Operational & Financial Positioning

The company achieved commercial-scale NdPr oxide production in 2024, with current qualification processes underway with multiple downstream customers. This production capability positions Energy Fuels as the sole domestic source of separated rare earth oxides available to United States manufacturers.

Chief Executive Officer Mark Chalmers, highlighted the company's progress in heavy rare earth separation technology.

"We have commercially produced NDPR and we are recovering DY and TB right now in the heavies."

Energy Fuels maintains US$210 million in liquidity with zero debt, providing financial flexibility for project development and market expansion. Ongoing uranium revenues support operating expenses while rare earth production scales toward full commercial capacity.

Near-Term Development Catalysts

The Donald Project in Australia approaches final investment decision in the second half of 2025, with full permitting completed and environmental approvals finalized. This heavy mineral sand project offers unique exposure to dysprosium and terbium, addressing the highest-value segments of the rare earth market.

Toliara Project development in Madagascar targets final investment decision in the first half of 2026, pending completion of financing arrangements and infrastructure agreements. The project's scale positions it among the largest rare earth development opportunities outside China.

Additional Project Pipeline & Strategic Opportunities

Bahia Project resource estimation completion is scheduled for 2025-2026, with initial metallurgical testing demonstrating favorable rare earth recovery characteristics. The project's proximity to existing infrastructure reduces development risk and capital requirements.

Chief Executive Officer Mark Chalmers emphasized the strategic value of heavy rare earth exposure:

"The one thing that we do have that I'm very proud of is that we have heavies in the Donald project that we have in Australia that is fully permitted."

Risk Factors & Investment Considerations

Rare earth element investments carry specific risks that require careful evaluation within portfolio construction frameworks. Permitting risks in Madagascar and Brazil could delay project development timelines, while regulatory changes in host countries may affect operating conditions or fiscal terms.

Market & Pricing Volatility

Pricing volatility risk remains elevated due to China's continued market influence and limited spot trading liquidity. Rapid price movements, while potentially favorable for producers, create earnings volatility that may not align with conservative investment mandates.

Operational & Technology Execution

Execution risk on separation technology scaling affects the transition from pilot-scale to commercial production. Technical challenges in heavy rare earth separation could impact project economics and development schedules.

Environmental, Social & Governance Scrutiny

Environmental, social, and governance scrutiny applies to both heavy mineral sand operations and uranium co-production activities. Institutional investors increasingly require comprehensive ESG compliance across all business segments.

The Investment Thesis for Rare Earths

- The structural case for rare earth element investment reflects multiple converging factors that create compelling risk-adjusted return opportunities:

- Structural scarcity emerges as NdPr demand growth of 300% by 2035 confronts a projected 30% supply shortfall based on current production capacity outside China.

- Geopolitical realignment accelerates as China's export controls drive ex-China scarcity premiums and government policies prioritize supply chain diversification across allied nations.

- Government backing provides investment certainty through the United States Department of Energy's US$1 billion commitment, Pentagon pricing floors of US$110 per kilogram for NdPr, and the European Union Critical Raw Materials Act funding mechanisms.

- Strategic positioning advantages companies like Energy Fuels that combine existing uranium revenue streams with rare earth separation capabilities and fully permitted project pipelines.

- Near-term catalysts including project final investment decisions and NdPr customer qualification processes de-risk development timelines and validate long-term demand projections.

- Operational resilience emerges through vertically integrated business models that control processing capabilities and maintain feedstock security across multiple jurisdictions.

- Market premiums for Western-sourced rare earth oxides create sustainable pricing advantages over Chinese competitors, supported by environmental, social, and governance requirements from downstream manufacturers.

Why This Price Spike Matters for Investors

The rare double-digit weekly surge in praseodymium-neodymium prices represents more than cyclical commodity volatility. This price movement validates long-term structural analysis that rare earth supply chains face fundamental scarcity as demand from electrification technologies accelerates beyond current production capacity outside China.

Supply constraints, government policy support, and accelerating demand creates investment conditions that favor companies with operational capabilities and strategic positioning in Western jurisdictions. Energy Fuels exemplifies this alignment through its combination of existing rare earth separation capabilities, government recognition, and project pipeline positioned in stable regulatory environments.

For institutional investors, the NdPr price surge reinforces the strategic necessity of rare earth exposure within portfolio construction. These materials are not cyclical commodities subject to traditional supply-demand balancing, but rather strategic inputs to technologies essential for energy transition and national security objectives.

The investment implications extend beyond immediate price appreciation to encompass the structural transformation of global rare earth markets. Companies positioned to capture value from this transition through operational excellence, strategic partnerships, and government support represent compelling opportunities for risk-adjusted returns in an environment of increasing resource nationalism and supply chain fragmentation.

Analyst's Notes

Subscribe to Our Channel

Stay Informed