Silver's Continued Repricing in 2026: Monetary Volatility & Energy Transition Demand

Silver surged 150%+ year-on-year to $85.22 in March 2026, driven by supply deficits, industrial demand, and monetary volatility across key mining jurisdictions.

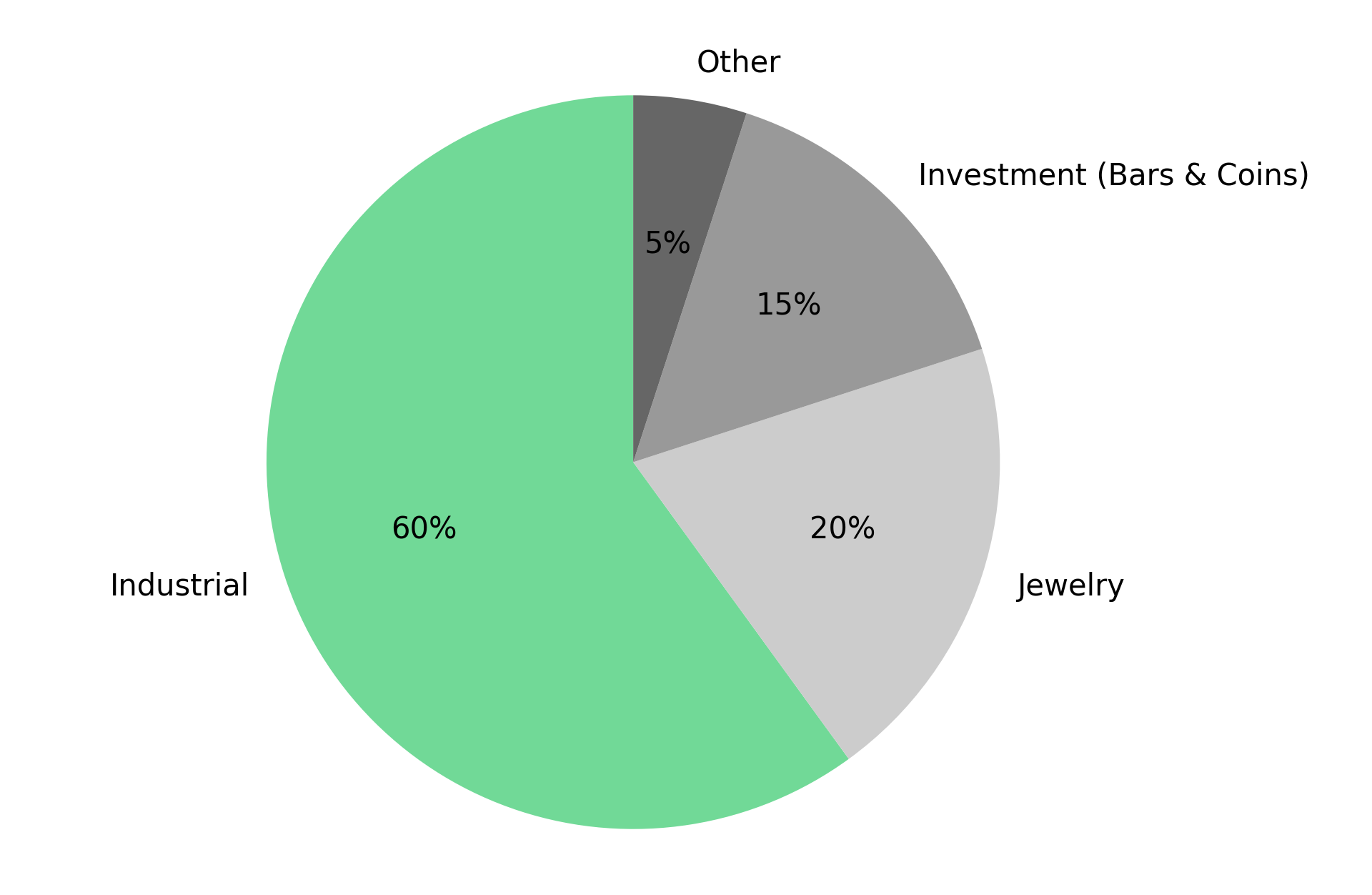

- Unlike gold, silver functions simultaneously as a precious metal safe haven and a critical industrial input, with roughly 60% of global demand tied to manufacturing sectors such as solar panels, electric vehicles, and data-center infrastructure.

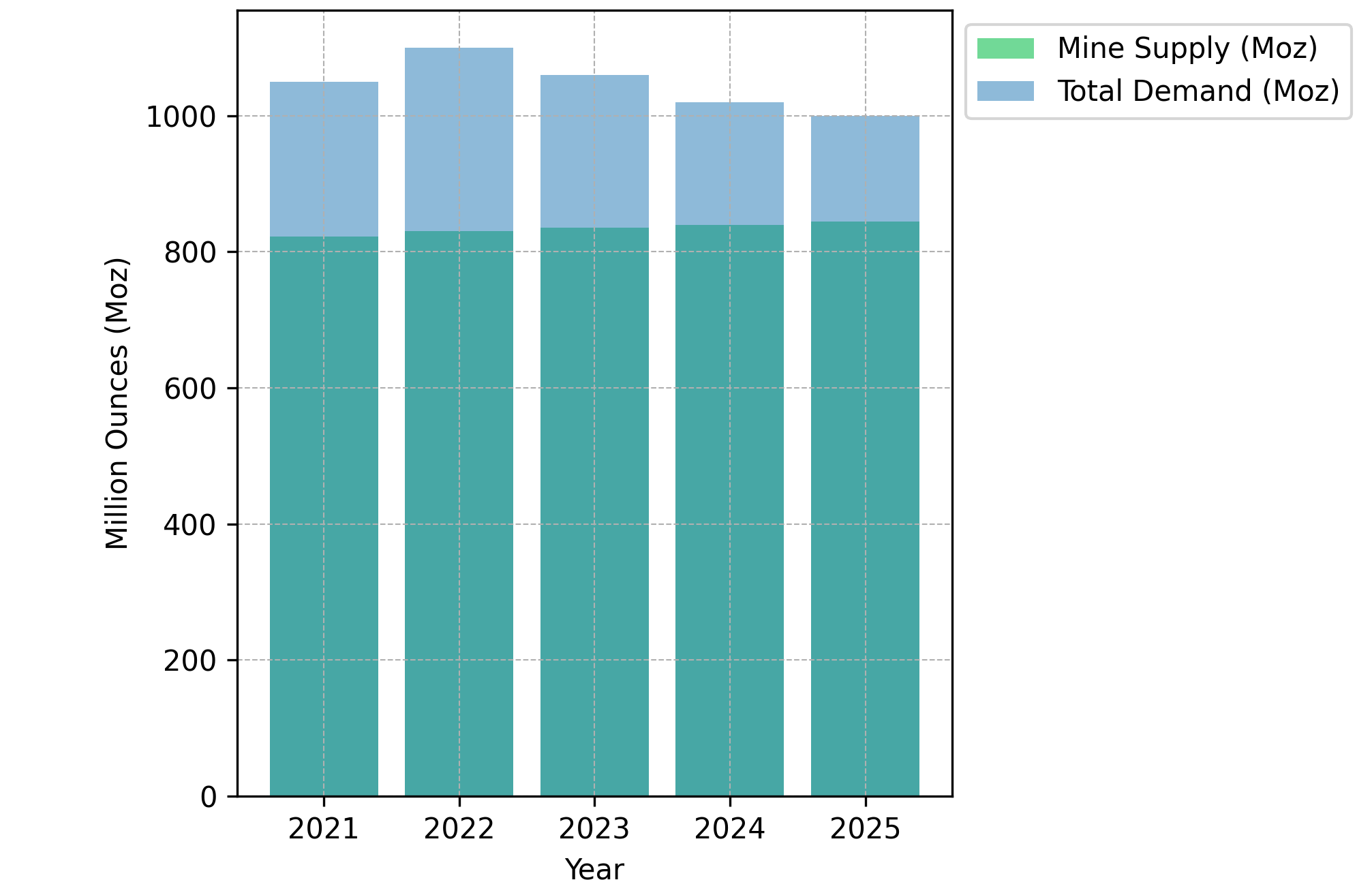

- Since 2021, the global silver market has recorded annual shortfalls ranging from 100 million to 250 million ounces against total mine supply of roughly 800 to 850 million ounces per year

- Approximately 70% of global silver production occurs as a byproduct of copper, lead, zinc, and gold mining, meaning higher silver prices alone cannot easily trigger rapid supply expansion.

- Monetary policy shifts, geopolitical tensions, and tariff discussions around critical minerals have triggered extreme price moves, highlighting silver's sensitivity to both safe-haven flows and industrial demand cycles.

- Mining companies positioned with high-grade resources, low costs, and operational catalysts may offer leveraged exposure. Projects with strong grades, low all-in sustaining cost profiles, scalable resources, and permitting visibility are drawing increasing investor attention as the market tightens.

Silver's Market Structure: Monetary & Industrial Demand

Roughly 60% of global silver demand originates from industrial applications, particularly sectors tied to electrification and digital infrastructure. Solar photovoltaic cells rely on silver paste for conductivity. Electric vehicles require silver in high-reliability electronics. AI-driven data centers increasingly depend on silver's thermal and electrical properties in power management systems. This dual identity creates a market dynamic that diverges sharply from other precious metals, producing a commodity that frequently exhibits greater price volatility than gold as two distinct demand regimes interact simultaneously.

Silver surged more than 130% during 2025, climbing from roughly $29 per ounce to over $70 per ounce, before spiking above $120 per ounce in early 2026 amid strong retail investment demand in Asian markets. Silver closed at $85.22 per ounce on March 11, 2026 - more than 150% higher year-on-year - underscoring the magnitude of the repricing underway.

Global Supply Constraints & the Structural Imbalance in Silver Markets

The investment narrative surrounding silver increasingly centers on a persistent and measurable imbalance: demand is outpacing supply, and structural characteristics limit the speed of any supply response.

According to J.P. Morgan Global Research, the silver market has recorded four consecutive years of deficits since 2021, with annual shortfalls ranging from 100 million to 250 million ounces against a global mine supply base of roughly 800 to 850 million ounces per year. Approximately 70% of global silver production occurs as a byproduct of base-metal mining in copper, lead, zinc, and gold, leaving silver output largely insensitive to silver price signals - what analysts describe as supply inelasticity. Developing new primary silver mines typically spans a decade or more from exploration through permitting, financing, and construction, meaning sustained price increases are generally required before new supply can materially close the deficit.

Industrial Demand From Energy Transition Technologies & the Thrifting Risk

While monetary factors influence short-term price movements, the energy transition has emerged as the dominant structural driver of long-term silver demand. Solar photovoltaic manufacturing represents one of the fastest-growing consumption channels, with silver's electrical conductivity and corrosion resistance making it essential for the metallization process within solar cells.

Historically, silver represented roughly 1.5% of the cost structure of a solar panel. Following the recent price surge, that share has reportedly increased to over 30% in certain manufacturing configurations, prompting manufacturers to accelerate thrifting efforts and experiment with alternative materials including copper and cadmium telluride thin-film. If silver prices remain elevated for extended periods, substitution technologies could partially offset the demand growth expected from solar deployment. Nevertheless, electrical systems across energy, transportation, and computing sectors have limited near-term alternatives to silver in critical applications.

Geopolitical Risk & Monetary Policy as Drivers of Silver Price Volatility

Short-term silver pricing remains highly sensitive to macroeconomic developments. Concerns over potential disruptions to oil shipments through the Strait of Hormuz, which carries roughly 20% of global oil flows, reignited inflation expectations across financial markets, illustrating how quickly sentiment can shift. On January 30, 2026, the nomination of Kevin Warsh as the next Federal Reserve chair triggered a sharp 27% decline in silver prices, according to J.P. Morgan Global Research - highlighting the commodity's acute susceptibility to macro policy shifts.

Unlike gold, silver lacks a consistent base of price-insensitive institutional buyers such as central banks. This absence of structural dip buying can amplify volatility during corrections. Silver's hybrid demand profile therefore not only creates upside potential during commodity cycles but also exposes the market to pronounced short-term fluctuations.

Mining Supply Responses Across Producers, Developers, & Explorers

As prices rise and deficits persist, the mining sector is responding through production expansion, project development, and exploration activity - each stage offering a distinct risk and return profile.

Production-Stage Operations & Critical Mineral Byproduct Optionality

Americas Gold & Silver is a primary silver producer operating the Galena Complex in Idaho and the Cosalá operations in Sinaloa, Mexico. The Galena mine recorded an average silver head grade of approximately 490 grams per tonne for full-year 2025, according to the company's March 2026 Corporate Presentation. At Cosalá, the EC120 mine reached commercial production in the fourth quarter of 2025, with an expected all-in sustaining cost of approximately $10.80 per ounce based on a pre-feasibility study filed on SEDAR.

The company announced a strategic joint venture with US Antimony on February 10, 2026, targeting antimony extraction from its existing concentrate stream - a critical mineral designated as strategic to US defense and industrial supply chains. Chief Executive Officer Paul Huet explained the Americas Gold & Silver’s operational structure:

"We will build a new refining structure, a leaching structure in the state of Idaho. On our land, next to our mill, we will have this new facility whereby all our concentrate will be leached through, and we will remove the antimony before we send it off... We own 51% of the JV, they own 49% of the JV."

The US government's Project Vault initiative, which has allocated $12 billion toward a domestic critical minerals stockpile, represents a potential institutional demand pathway. The company intends to work in collaboration with the government through that program, though no formal agreement has been publicly disclosed as of publication.

Development-Stage Projects & Tailings Reprocessing

Cerro de Pasco Resources is a development-stage company advancing the reprocessing of the Quiulacocha tailings deposit in Pasco, Peru. The deposit contains a historic estimate of 423 million ounces of silver equivalent, derived from historic metallurgical balances and not independently verified as a current mineral resource under NI 43-101 or JORC standards. Because the material is already above surface, the project avoids conventional drilling, blasting, and primary hauling costs, with extraction projected at roughly $1 to $2 per tonne based on internal projections not NI 43-101 compliant. Phase 1 drilling campaign assay results confirmed an average grade of 53.2 grams per tonne of gallium and 19.9 grams per tonne of indium, critical minerals increasingly relevant to semiconductor and defense supply chains. In May 2024, the company secured a Supreme Resolution granting land easement access to the El Metalurgista Concession, enabling its 40-hole drilling campaign to proceed.

Exploration-Stage Resource Growth & Permitting Frameworks

GR Silver Mining is advancing the Plomosas project in Sinaloa, Mexico, which hosts an NI 43-101 compliant resource of 134 million ounces of silver equivalent, 68 million ounces at San Marcial and 66 million ounces at Plomosas, effective May 3, 2023. The company has outlined a 20,000-metre step-out drilling program for 2026, with both an updated Mineral Resource Estimate and a maiden Preliminary Economic Assessment targeted for the second half of 2026.

Vice President of Corporate Development Daniel Schieber contextualized the discovery economics:

"Our discovery cost per ounce of silver is 17 cents. For every investor that is investing in GR Silver, when we put a dollar in the ground, we get about 5 ounces of silver out of that."

President and Chief Executive Officer Marcio Fonseca outlined near-term operational priorities:

"We are planning how we can be very aggressive in the first half of 2026, drill in six months, probably more than we ever drilled, with multiple drill rigs, and advance more towards the pilot plant by the second half of 2026."

Bulk sample test mining at Plomosas is scheduled to commence in 2026, serving both a metallurgical proof-of-concept function and a permitting advancement role ahead of pilot plant installation.

The Investment Thesis for Silver

- Supply deficits persisting since 2021 reflect a sustained imbalance between global demand and mine output with no near-term mechanism capable of rapidly correcting the gap.

- Inelastic supply dynamics, driven by the dominance of byproduct production across copper, zinc, lead, and gold operations, mean that silver prices alone cannot easily incentivize proportional increases in supply.

- Energy transition demand from solar photovoltaics, electric vehicles, and digital infrastructure continues to expand the industrial consumption base, even as manufacturers adapt to higher input costs through thrifting.

- Macroeconomic hedging behavior positions silver as a beneficiary of monetary uncertainty and geopolitical instability, adding a financial demand overlay to the structural industrial thesis.

- Operational leverage among mining companies with high-grade deposits, favorable all-in sustaining cost profiles, and critical mineral byproduct optionality may deliver amplified returns relative to spot price during commodity upcycles.

- Government critical mineral programs in the United States are beginning to create institutionalized demand pathways for domestic producers, introducing a potential new layer of price support for certain byproduct streams.

Silver's behavior as both a monetary metal and a critical industrial input places it at the intersection of energy transition infrastructure, geopolitical uncertainty, and shifting monetary policy expectations, producing periods of acute volatility while reinforcing the metal's long-term strategic relevance.

TL;DR

Silver has undergone a structural repricing, climbing from roughly $29 per ounce in early 2025 to $85.22 by March 11, 2026, more than 150% higher year-on-year. Four consecutive years of supply deficits, combined with inelastic byproduct-dominated mine supply, have created a gap that higher prices alone cannot quickly close. Industrial demand from solar photovoltaics, electric vehicles, and data-center infrastructure continues expanding even as manufacturers accelerate thrifting efforts. Macroeconomic triggers — Federal Reserve policy signals, Hormuz supply concerns, and critical mineral geopolitics — amplify short-term volatility. Mining companies with high-grade deposits, low all-in sustaining costs, and critical mineral byproduct optionality are drawing investor interest as the structural imbalance deepens.

FAQs (AI-Generated)

Silver surged more than 150% year-on-year by March 2026, driven by a combination of persistent supply deficits, surging industrial demand from solar and EV manufacturing, strong retail investment flows in Asian markets, and macroeconomic uncertainty prompting safe-haven buying. The metal's dual identity as both a monetary asset and critical industrial input amplified price moves beyond what either demand regime would produce independently.

Approximately 70% of global silver is produced as a byproduct of copper, lead, zinc, and gold mining, meaning silver prices alone cannot easily incentivize faster output. Developing dedicated primary silver mines typically takes a decade or more. Against a global mine supply base of roughly 800 to 850 million ounces annually, the market has recorded annual shortfalls of 100 to 250 million ounces every year since 2021.

Solar photovoltaic manufacturing is one of silver's fastest-growing consumption channels, relying on silver paste for electrical conductivity in solar cells. Electric vehicles and AI-driven data centers also depend on silver for high-reliability electronics and power management. While manufacturers are accelerating substitution and thrifting efforts as silver's share of panel costs has risen sharply, near-term alternatives in critical electrical applications remain limited.

Silver is acutely sensitive to monetary policy signals — the nomination of Kevin Warsh as Federal Reserve chair in January 2026 triggered a 27% single-session price decline, according to J.P. Morgan Global Research. Geopolitical developments affecting inflation expectations, such as concerns over Strait of Hormuz oil flows, can rapidly shift sentiment. Unlike gold, silver lacks a consistent base of price-insensitive institutional buyers such as central banks, which amplifies corrections.

Producers, developers, and explorers across the silver sector are expanding output, advancing projects, and deploying capital toward resource growth. Americas Gold & Silver is scaling production at its Galena and Cosalá operations while pursuing antimony byproduct extraction through a new joint venture. Cerro de Pasco Resources is advancing tailings reprocessing in Peru. GR Silver Mining has outlined an aggressive 20,000-metre drilling program for 2026, targeting a resource update and maiden economic assessment by the second half of the year.

Analyst's Notes

Subscribe to Our Channel

Stay Informed