Solving The Junior Exploration Conundrum

Fitzroy Minerals targets cash flow by 2027 via Chile copper JV whilst exploring district-scale sulphide discovery at Bueno Retiro project adjacent to billion-dollar deposits.

- Fitzroy Minerals is advancing a near-term production strategy through a proposed heap leach partnership with Pucobre that could deliver more than 10 million pounds of annual copper attributable to the company by late 2027 or early 2028, creating a potential self-funding pathway for ongoing exploration.

- The Bueno Retiro project exhibits geological and mineralisation characteristics directly comparable to major IOCG systems in the Punta del Cobre district, including hematite stockwork and chalcopyrite assemblages similar to those found at Mantoverde and Candelaria.

- Recent drilling has confirmed significant sulphide discovery potential, with disseminated chalcopyrite encountered across 149-metre-plus intervals and a largely untested 3-kilometre by 2-kilometre IP anomaly offering substantial blue-sky tonnage upside.

- Fitzroy’s dual-track strategy of near-term oxide heap leach development alongside systematic sulphide drilling positions the company to bridge the structural funding gap faced by copper explorers while building exposure to district-scale mineral potential.

- Chile’s mining stability, favourable royalty regime for small-scale producers, mature infrastructure, and deep operational expertise provide a strong jurisdictional foundation for Fitzroy’s plan to advance Bueno Retiro toward production while expanding its sulphide footprint.

Why Copper Explorers Need New Financial Models

The copper exploration sector faces a structural challenge that has intensified as project development timelines extend and capital requirements escalate. Junior explorers typically burn through treasury funding in 12-18 month drilling campaigns, forcing repeated dilutive financings that erode shareholder value long before production revenues materialise. Fitzroy Minerals (TSXV:FTZ) is attempting to solve this conundrum through an unconventional strategy: securing near-term cash flow from a joint venture with established Chilean operator Pucobre whilst simultaneously also pursuing what could prove to be a district-scale copper discovery in Chile's historic Punta del Cobre mining region.

With copper prices facing structural support from electrification demand and constrained global supply, the timing for new copper discoveries has rarely been more compelling. Fitzroy's $103 million Canadian market capitalisation ($70 million USD) represents a modest entry point for investors willing to accept exploration risk in exchange for exposure to what CEO Merlin Marr-Johnson describes as geology "identical" to assets that underpin multi-billion dollar valuations for Capstone Copper and Lundin Mining.

Best Copper Exploration Stocks 2026: Chile's Enduring Advantages

Chile's position as the world's dominant copper producer stems from more than geological endowment. The country delivers 5.3-5.4 million tonnes of copper annually, representing almost a quarter of global production, and has maintained stable mining law since 1980 following denationalisation of the copper industry under the Pinochet regime. This regulatory stability persists despite recent political shifts, with mining reforms under the socialist Boric government focused primarily on increased royalty rates for producers exceeding 50,000 tonnes of fine copper annually and higher concession holding costs to encourage exploration investment.

Critically for junior miners like Fitzroy, operations producing less than 12,000 tonnes of fine copper per annum remain exempt from royalties, a significant economic advantage for smaller-scale heap leach operations.

"It is important to recognise that Chile is a proper mining country," Marr-Johnson emphasised. "There is a political shift to the right. The new candidate Kast is talking and acting like a president already and the congress and the chamber of deputies are already run by the centre right."

The Chilean Copper Commission's 2025 report projects $83 billion of investment flowing into Chile between 2024-2033, with over 75% directed toward copper projects. Yet this massive capital deployment is forecast to increase national production by merely 100,000 tonnes, from 5.43 million tonnes to 5.5 million tonnes, illustrating the extraordinary capital intensity now required simply to maintain output as mature operations deplete high-grade zones and mine progressively deeper ore bodies.

Fitzroy Minerals Stock Analysis: The Bueno Retiro Project Portfolio

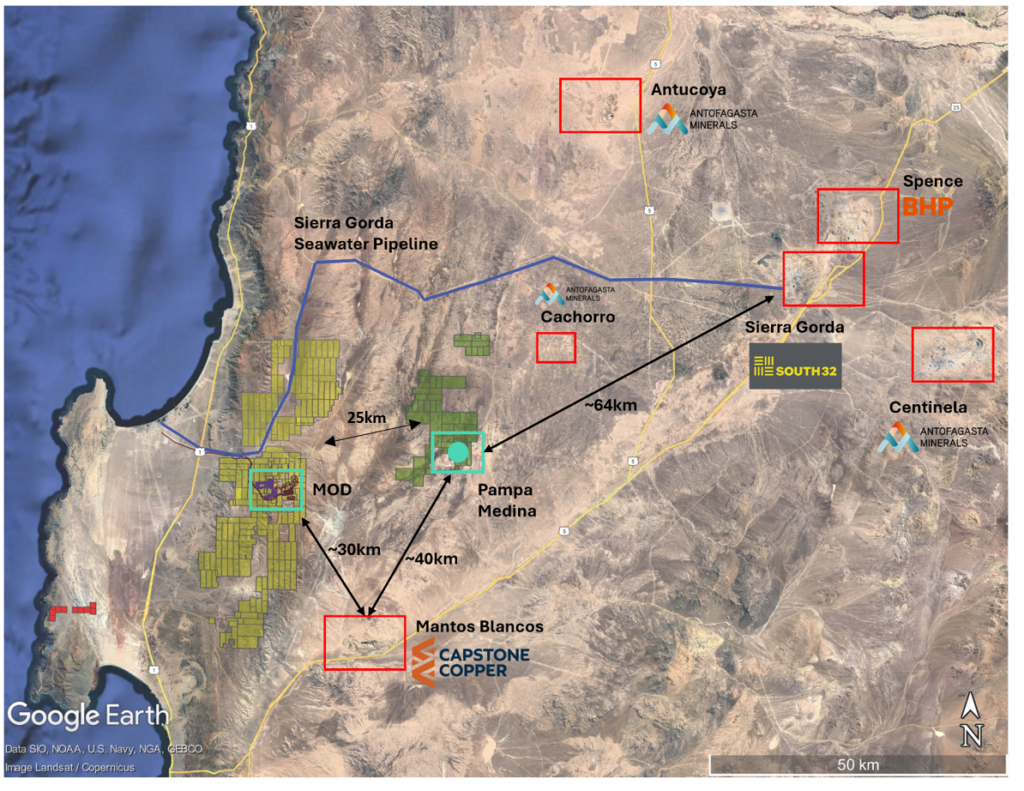

Fitzroy's flagship Bueno Retiro asset comprises multiple development opportunities within a single consolidated land package in the Atacama region, 35 kilometres from the coast and adjacent to established infrastructure including the Pan American Highway. The project sits within the Punta del Cobre district, which hosts Lundin Mining's Candelaria operation (600 million tonnes measured and indicated at 0.47% copper and 0.11 g/t gold) and Capstone Copper's Mantoverde operation (600 million tonnes at 0.46% copper and 0.1 g/t gold).

The Bueno Retiro site contains a historical mine previously operated by Pucobre, which trucked ore 30 minutes awy to their Planta Bío facility, an SX/EW plant operating since 1992 at a fraction of its 800 tonnes per month copper production capacity. This existing processing infrastructure forms the basis of Fitzroy's proposed heap leach joint venture, which could deliver attributable production of approximately 10 million pounds of copper annually to Fitzroy. At margin assumptions of $1-2 per pound, this would generate $10-20 million annual cash flow before capital allocation, transformational funding for a company currently holding $11 million in treasury with an additional $5 million expected from warrant and option exercises. This however is not the main play, it is merely a mechanism to address the eternal challenge for all explorers of how to fund drilling without continually diluting shareholders.

"We think that we may be able to structure a deal where we get close to 80 or 90% of capacity utilisation, using Buen Retiro material," Marr-Johnson explained regarding the Planta Bío arrangement. "So we're looking at attributable production of hopefully somewhere in the region of 10 million pounds of copper per annum or more attributable to Fitzroy coming through this plant and the mine operated by Pucobre."

The oxide mineralisation targeted for this near-term production scenario occurs in shallow zones across multiple areas of the property, with particular focus on the southwest area where drilling has established sufficient continuity for a starter pit over 800 metres of strike. Notable oxide intercepts include 135 metres at 0.73% copper and 110 metres at approximately 2% copper. The company is advancing a preliminary economic assessment focused on these oxide resources, with plans to complete a maiden mineral resource estimate and PEA by end of 2026, submit environmental impact declarations in Q2-Q3 2026, and potentially achieve production by late 2027, or early 2028.

Copper Mining Stocks with Upside: The Sulphide Discovery Story

Whilst the oxide heap leach project offers near-term cash flow visibility, the geological prize at Buen Retiro lies in the sulphide mineralisation that Fitzroy Minerals has begun systematically testing. The company's December 2025 news release reported visual results from holes 40, 41, and 42 revealed mineralisation styles directly comparable to the IOCG (iron oxide copper gold) systems that define the district's major producers.

Following a site visit to Capstone's Mantoverde and Lundin's Candelaria operations, Fitzroy's COO Gilberto Schubert was able to photograph core samples and conduct direct visual comparisons with Bueno Retiro drilling. The correlations proved remarkably consistent: hematite stockwork, chalcopyrite-hematite breccia, calcite-specularite-chalcopyrite assemblages, and late-stage low-temperature mineralisation styles all find equivalents in the Fitzroy core. Particularly significant is the la Farola style mineralisation, a late-stage overprint where Capstone recently delineated at approximately 50 million tonnes at Mantoverde for near-term production. Fitzroy encountered this identical style 2.5 kilometres away in a regional reconnaissance RC hole, with a 36-metre intersection including 5 metres at 1.33% copper on an 800-metre-long northeast-trending geophysical anomaly.

The main sulphide target comprises a 3-kilometre by 2-kilometre IP anomaly where initial drilling has intersected disseminated chalcopyrite across remarkably consistent intervals. Hole 40 encountered 60 metres of oxide mineralisation before entering sulphides; hole 41 and hole 42 continued the trend northward. Hole 3 at the southern extent delivered 21 metres at 0.4% copper and 0.1 g/t gold in sulphides, whilst all three holes contained disseminated chalcopyrite across 149+ metre intervals, suggesting potential for a bulk tonnage sulphide resource beneath the oxide cap.

"Each of these three holes has had intersections of disseminated chalcopyrite for over 149 metres," Marr-Johnson noted. "So we're pretty stoked about that, and I look forward to bringing results from those sulphide holes and others as we go ahead."

The company has drilled only four holes into this sulphide system to date, leaving the vast majority of the IP anomaly untested. For context, Candelaria contains reserves of 600 million tonnes in proven and probable categories, whilst Capstone's Mantoverde oxide reserves stand at 457 million tonnes at 0.29% copper. Marr-Johnson's assessment is direct:

"If we can find some shallow stuff - a few hundred million tons at 0.35 to 0.4% copper at around 0.1 grams gold - we are in business here at Fitzroy Minerals."

Top Copper Stocks Canada: Financial Position & Market Valuation

Fitzroy Minerals currently trades with a market capitalisation of approximately $103 million Canadian ($70 million USD), holding $11 million in cash with an additional $5 million anticipated from warrant and option exercises. The company's 12-month exploration budget must accommodate infill drilling for the oxide PEA, continued sulphide exploration at Bueno Retiro, geophysical surveys, metallurgical testing, engineering baseline studies, environmental permitting, and phase two work at the Caballos project.

This financial position reflects both opportunity and risk. The treasury provides adequate runway for the immediate drill programme and PEA completion, whilst the Pucobre joint venture, if successfully negotiated, could eliminate the need for significant equity dilution from 2028 onwards. However, the joint venture terms remain unfinalized, creating execution uncertainty around this cornerstone of the financial strategy.

The company's shareholder registry includes institutional investors and high-profile resource sector figures, most notably Craig Parry. Parry's track record includes C-Suites roles with Skeena Resources, IsoEnergy, NexGen Energy, Vizsla Silver, and Vizsla Copper through his Investa Capital platform. Parry has invested in Fitzroy at both 15 cents and 30 cents per share, providing project and market validation from an investor known for successful metals discoveries and building companies.

Retail investor interest has strengthened, with other prominent commentators highlighting the opportunity. As Merlin Marr-Johnson noted that when I was approached about selling a block of shares to institutions that I said no. As this may suggest, I and other notable existing shareholders are holding positions in anticipation of value creation from the drill bit rather than seeking liquidity at current valuations. Please note that I continue to buy stock in the option market.

Copper Investment Opportunities 2026: The Caballos Project & Portfolio Strategy

Fitzroy's second asset, the Caballos project, delivered the company's initial market attention with a high-grade discovery hole before subsequent drilling returned more modest results. Holes 2A, 3, and 5 produced grades "not as good as the first hole, which was a real zinger," according to Marr-Johnson's candid assessment. The company plans to complete geophysical surveys across the entire Caballos property using MMT to better understand subsurface architecture before committing to additional drilling.

Current drilling is underway at both Mule Hill and Chincolco zones within Caballos, with results pending. Marr-Johnson's approach to the project reflects appropriate risk management:

"We will be doing geophysics on Caballos and we will be coming to phase two work and probably drilling on Caballos. But there's just so much exciting stuff happening at Bueno Retiro that we cannot ignore it."

This allocation decision of prioritising Bueno Retiro over Caballos, despite Caballos delivering the initial discovery, demonstrates management discipline in concentrating capital on the asset with the clearest path to both near-term cash flow and district-scale discovery potential. For investors, the Caballos position represents portfolio optionality rather than the primary investment thesis.

Risks & Challenges for Junior Copper Miners

Several material risks warrant careful consideration. The Pucobre joint venture remains under negotiation, with no public disclosure of proposed commercial terms, ownership structure, capital contribution requirements, or timeline to definitive agreement. Any significant delay or unfavourable terms could materially impact the near-term cash flow thesis that distinguishes Fitzroy from peers.

Technical risk persists around the oxide resource estimate and PEA economics. Whilst management expresses confidence in delineating an 8-10 year mine life for the heap leach operation, the resource remains undefined with infill drilling ongoing. Metallurgical recoveries, leach kinetics, and capital cost estimates will determine project economics, with the PEA scheduled for completion by end of 2026.

The sulphide discovery, whilst geologically compelling, represents classic exploration risk. Three initial holes with consistent broad mineralisation provide encouragement, but grade, continuity, metallurgy, and ultimate resource tonnage remain unproven. The analogies to Candelaria and Mantaoverde are visual and geological; they are not yet economic. Converting geological similarity into economic similarity requires successful drilling across the 3km by 2km target area, a multi-year, capital-intensive undertaking.

Permitting risk, whilst reduced in Chile relative to many jurisdictions, remains present. The company anticipates submitting environmental impact declarations in Q2-Q3 2026, and hopes to replicate the 12-month approval timeline achieved by Marimaca Copper's oxide deposit. Any permitting delays would postpone the cash flow generation that underpins the financial model timeline.

Market risk cannot be ignored. Copper prices, whilst supported by structural supply constraints and electrification demand, remain subject to macroeconomic cycles, Chinese demand fluctuations, and potential supply responses from major producers. A sustained copper price decline would impact both the heap leach project economics and the strategic value of any sulphide discovery.

Chilean Copper Companies to Watch: Comparative Positioning

Fitzroy's USD$70 million market capitalisation positions the company at the junior end of the Chilean copper spectrum, orders of magnitude smaller than Capstone Copper's $9 billion valuation or Lundin Mining's $22 billion enterprise value. However, this scale differential reflects the vast difference between producing operations with established reserves and an exploration company with early-stage discoveries.

The key differentiators for Fitzroy include the proximity to existing processing infrastructure (reducing capital intensity), the advanced discussions with an experienced operating partner in Pucobre, and the geological validation provided by visual core comparisons to billion-dollar deposits within the same district.

The company's strategy explicitly targets the supply gap identified by major producers. BHP's guidance for Escondida, the world's largest copper mine, projects production declining from current levels of 1.0-1.3 million tonnes annually to approximately 1.0 million tonnes by 2030 despite a $5 billion capital investment program. This production plateau at mature operations, combined with increasing capital intensity for both greenfield and brownfield projects, creates market space for new production sources, particularly smaller-scale operations that can achieve cash flow without billion-dollar capital requirements.

Investment Thesis for Fitzroy Minerals

Value Proposition:

- Dual-track strategy separating near-term cash flow (oxide heap leach JV) from long-term discovery potential (sulphide exploration) addresses the explorer funding challenge whilst maintaining exploration upside

- District-scale geological validation through direct core comparisons to Mantoverde and Candelaria provides credible template for multi-hundred-million tonne sulphide potential at 0.35-0.4% copper grades

- Infrastructure advantage with existing processing facilities, established permitting precedents, and proximity to water sources reduces capital intensity and execution risk relative to greenfield remote projects

- Chilean jurisdiction benefits including stable mining law, no royalties below 12,000 tpa fine copper production, and 200-year mining history provide regulatory certainty unavailable in many copper-producing regions

- Experienced management and board including Craig Perry's involvement and Pucobre partnership provides operational expertise and market credibility for project advancement

Key Risks:

- Pucobre JV terms remain unfinalized with no public disclosure of commercial structure, potentially delaying or reducing expected cash flow generation

- Sulphide discovery remains unproven with only four holes completed across 3km x 2km target area; grade, continuity, and metallurgy require extensive additional drilling and testing

- Limited treasury of $11M cash plus $5M from warrants/options may prove insufficient for comprehensive drilling programmes across both Bueno Retiro and Caballos without additional financing

- Caballos disappointment following initial high-grade hole demonstrates exploration risk and potential for future drill results to disappoint market expectations

- Permitting and development timeline uncertainty with 18-24 month path to potential production dependent on successful PEA, environmental approvals, and JV finalization

- Copper price sensitivity as project economics for both oxide heap leach and potential sulphide development depend on sustained copper prices above marginal cost of production

- Market capitalisation reflects substantial execution risk with current USD$70M valuation requiring successful delivery on multiple fronts (PEA, JV, sulphide drilling) to justify further re-rating

Actionable Considerations:

- Monitor Q1-Q2 2026 for PEA results, maiden resource estimate, and formal announcement of Pucobre JV terms as key de-risking catalysts

- Assess sulphide drilling results from ongoing programme for consistency with initial holes showing 149+ metre disseminated mineralisation intervals

- Track warrant and option exercise rates as indicator of insider confidence and treasury strength for continued exploration

- Compare oxide heap leach economics once disclosed against peer projects in Chile to evaluate production cost competitiveness and margin sustainability

- Evaluate environmental permitting progress as measure of timeline confidence for 2027/2028 production scenario

Fitzroy Minerals represents a leveraged bet on copper supply constraints colliding with electrification demand, packaged within a financial structure designed to escape the perpetual capital-raising cycle that afflicts junior explorers. The Pucobre joint venture, if successfully negotiated, could deliver $10-20 million annual cash flow by 2028; sufficient to self-fund continued exploration of what may prove a district-scale sulphide system analogous to deposits supporting multi-billion dollar valuations for Capstone and Lundin Mining.

The geological validation is compelling: direct core comparisons confirm mineralisation styles identical to Candelaria and Mantoverde, whilst initial drilling has intersected broad zones of disseminated chalcopyrite across a largely untested 3km x 2km IP anomaly. However, investors must balance this blue-sky potential against execution risks spanning JV negotiation, oxide resource definition, sulphide drilling success, permitting timelines, and copper price sensitivity.

For risk-tolerant investors seeking copper exposure through Chilean jurisdiction advantages and district-scale discovery potential, Fitzroy's $70 million USD market capitalisation offers meaningful upside leverage if management successfully delivers the PEA, finalises the Pucobre partnership, and continues intercepting mineralisation across the sulphide target. The investment requires patience through 12-18 months of drilling and development work, with material catalysts anticipated throughout 2026 as resource estimates, economic studies, and additional drilling results emerge. The company's strategy explicitly addresses exploration's funding challenge - a potentially transformational approach if execution matches ambition.

Macro Thematic Analysis

The structural copper deficit taking shape across the 2025-2030 period stems from a collision between accelerating electrification demand and an extraordinarily capital-intensive supply response. The Chilean Copper Commission's 2025 report forecasts $83 billion of investment delivering merely 100,000 tonnes of additional annual production, from 5.43 million tonnes to 5.5 million tonnes nationally. This represents spending over $500,000 per incremental tonne of annual production capacity, illustrating why copper prices must materially re-rate to incentivise new supply.

BHP's Escondida operation epitomises the challenge: a projected $5 billion capital programme to maintain approximately 1.0 million tonnes annual production by 2030, representing a 20-30% decline from current output. As CEO Merlin Marjohnson noted:

"Capital intensity of new projects is rising... greenfield stays expensive but actually brownfield has got more and more expensive and that is a function of increased complexity, increased volumes as grades decline and increased depths as the big projects are being mined deeper and deeper and deeper."

This production plateau from tier-one assets creates market space for smaller-scale operations that can achieve cash flow without billion-dollar capital outlays. Heap leach projects targeting 10,000 tonnes annual production, below Chile's royalty threshold, offer particularly attractive economics in a rising copper price environment. The real copper price, measured against gold, has declined over 25 years despite nominal gains, suggesting substantial upside potential as physical supply constraints manifest in the late 2020s.

Fitzroy's strategy directly targets this opportunity: secure near-term production to fund exploration of a potential district-scale discovery whilst major producers struggle to maintain output from depleting ore bodies. If successful, the model could prove replicable across other junior explorers seeking to bridge the funding gap between discovery and development.

"Vast amounts of money is going just to maintain production. Metal prices have to rise as demand is strong... the coming crunch is actually driving value in existing companies and you can see that in companies like Capstone Copper and Lundin Mining."

From the author: I am a shareholder of Fitzroy Minerals, as noted in the company's investor presentation. I have not sold any shares and I continue to buy in the open market.

FAQ's (AI-Generated)

Fitzroy Minerals is targeting late 2027 or early 2028 for initial copper production from the oxide heap leach operation through its proposed joint venture with Pucobre. The timeline depends on completing the preliminary economic assessment by end of 2026, submitting environmental impact declarations in Q2-Q3 2026, receiving environmental permits (anticipated within 12 months following submission), and finalizing joint venture terms with Pucobre. The company plans approximately six months for construction once permits are secured. This production timeline is significantly faster than typical greenfield copper projects due to existing processing infrastructure at Pucobre's Planta Bío facility, which has operated since 1992 and currently runs below capacity. However, investors should note this timeline assumes successful completion of all regulatory, technical, and commercial milestones without material delays.

Fitzroy's Bueno Retiro project displays mineralisation styles visually and geologically identical to Capstone Copper's Mantoverde operation ($9 billion market cap) and Lundin Mining's Candelaria operation ($22 billion market cap), both located in the same Punta del Cobre district. Following a site visit to these operations, Fitzroy's COO photographed core samples showing hematite stockwork, chalcopyrite-hematite breccia, calcite-specularite-chalcopyrite assemblages, and late-stage low-temperature mineralisation—all of which have direct equivalents in Fitzroy's drilling. Particularly significant is the intersection of Rosella-style mineralisation (a late-stage overprint that Capstone recently delineated at approximately 50 million tonnes) located 2.5 kilometres away in a regional reconnaissance hole. Initial sulphide drilling at Bueno Retiro has intersected disseminated chalcopyrite across 149+ metre intervals in three consecutive holes, replicating the results of 21 metres at 4% copper and 0.1 g/t gold from teh bottom of hole 3, suggesting potential for bulk tonnage mineralisation across a 3km x 2km IP anomaly that remains largely untested.

Fitzroy is negotiating a heap leach joint venture with Chilean copper operator Pucobre that could deliver approximately 10 million pounds of copper annually attributable to Fitzroy by 2027/2028. At margin assumptions of $1-2 per pound, this would generate $10-20 million in annual operating cash flow—sufficient to self-fund continued exploration of the larger sulphide discovery potential at Bueno Retiro. This strategy directly addresses the structural challenge facing junior explorers, who typically exhaust treasury funding in 12-18 month drilling campaigns and face repeated dilutive financings. The joint venture would utilise Pucobre's existing Planta Bío SX/EW processing facility, which operates at a fraction of its 800 tonnes per month production capacity, significantly reducing capital intensity compared to building standalone processing infrastructure. CEO Merlin Marjohnson stated the company is "looking at maybe kind of attributable production of hopefully somewhere in the region of 10 million pounds of copper per annum attributable to Fitzroy coming through this plant and the mine operated by Pucobre." However, joint venture terms remain unfinalized, creating uncertainty around this cornerstone financial strategy.

Material risks include: (1) The Pucobre joint venture terms remain under negotiation with no public disclosure of commercial structure, ownership split, capital contribution requirements, or timeline to definitive agreement—any unfavourable terms or delays would impact the near-term cash flow thesis; (2) The sulphide discovery, whilst geologically compelling with consistent broad mineralisation in initial holes, remains unproven with only four holes completed across a 3km x 2km target area—grade, continuity, metallurgy, and ultimate resource tonnage require extensive additional drilling; (3) Limited treasury of $11 million cash plus $5 million from anticipated warrant/option exercises may prove insufficient for comprehensive programmes across both Bueno Retiro and Caballos without additional financing; (4) The Caballos project disappointed after initial high-grade results, demonstrating exploration risk and potential for future drill results to underwhelm; (5) Permitting and development timeline uncertainty with 18-24 month path to potential production dependent on successful PEA, environmental approvals, and JV finalization; (6) Copper price sensitivity as both oxide heap leach economics and sulphide development value depend on sustained copper prices above marginal production costs; (7) The current $70 million USD market capitalisation reflects substantial execution risk, requiring successful delivery across multiple fronts (PEA, JV, drilling) to justify further valuation re-rating.

Chile offers several structural advantages for copper development: (1) Stable mining law maintained since 1980 following denationalisation of the copper industry, providing regulatory certainty through multiple political cycles; (2) Operations producing less than 10,000 tonnes of fine copper per annum remain exempt from royalties—a significant economic benefit for smaller-scale heap leach operations like Fitzroy's proposed project; (3) 200 years of mining innovation and continuous copper production since the 19th century has created sophisticated local expertise, established supply chains, and proven operating techniques including leadership in block caving and chloride leaching for heap leach projects; (4) Infrastructure density in established mining districts like Punta del Cobre, including roads, ports, water access, and existing processing facilities, reduces capital intensity for new projects; (5) Chile delivers 5.3-5.4 million tonnes of copper annually (24% of global production), creating a mining-focused economy where copper represents 61% of export value; (6) Recent mining reforms focused on encouraging exploration through higher concession holding costs for inactive ground, improving asset availability for active explorers; (7) License reform in 2024 simplified permitting processes, with projects like Marimaca receiving environmental permits within 12 months. CEO Merlin Marr-Johnson emphasised: "Chile really is important to recognise that it is a proper mining country... stable constitution and stable mining law in fact the mining law has remained largely unchanged since 1980."

Note: These FAQs are AI-generated based on the provided transcript and article content. Investors should conduct independent research and consult with financial advisers before making investment decisions.

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

Stay Informed