The Salt Deficit: Navigating North America’s US$2.6 Billion De-Icing Market (3/3)

North America's $2.6B de-icing salt market rewards retail channel access over bulk volume. Retail premiums reach 10x municipal pricing, reshaping producer valuations.

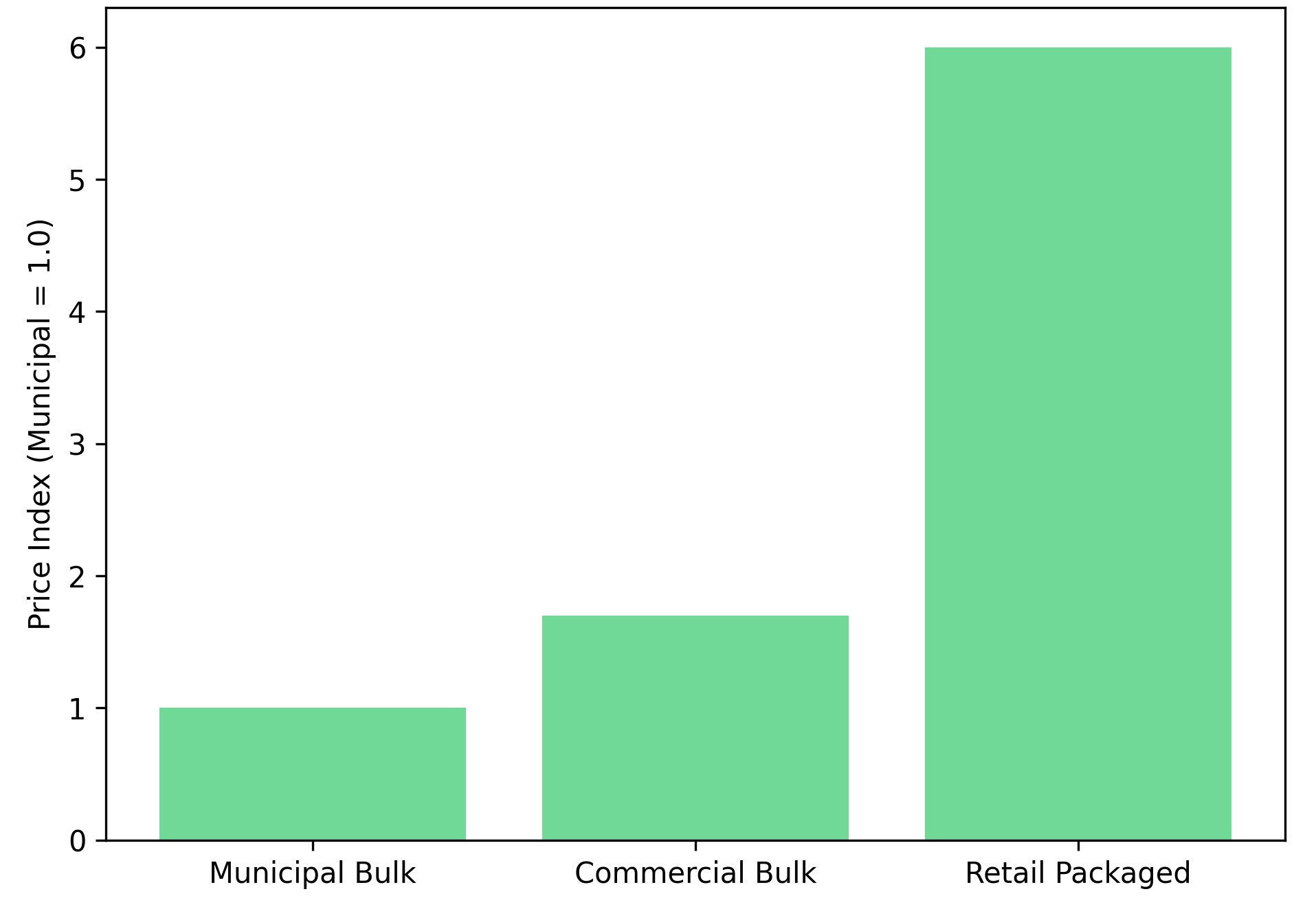

- Pricing power in salt is no longer volume-driven, as the North American market has structurally split into bulk, commercial, and retail regimes, with retail pricing up to 10 times municipal contracts.

- Margin expansion now depends on mix rather than tonnage, with producers able to shift 20% to 30% of sales into packaged retail, materially changing EBITDA and cash flow durability.

- ESG considerations are becoming economic filters rather than branding exercises, as low-carbon mine design and logistics are increasingly influencing procurement outcomes across both public and retail channels.

- Distribution access represents the true bottleneck, with the ability to monetize retail premiums depending less on geology and more on partnerships with established consumer-facing distributors.

- This reframes salt from a utility commodity into a differentiated infrastructure product, with implications for valuation, capital allocation, and strategic optionality.

From Utility Commodity to Margin-Stratified Market

For decades, salt has been analyzed through a single framework: lowest-cost production wins. The industry was understood as volume-driven, with pricing determined by mine-gate costs and transportation economics. Municipal contracts were awarded to the bidder offering the most tonnage at the lowest delivered price.

That analytical framework no longer explains the margin dispersion emerging across North American salt producers. While bulk deicing salt remains the foundation, stable, predictable, safety-critical, a parallel market structure has developed where pricing bears little relationship to traditional cost benchmarks. This bifurcation reflects structural changes in how salt reaches end users, how value is captured across the supply chain, and increasingly, how procurement decisions are influenced by factors beyond delivered cost per ton.

Salt assets can no longer be evaluated solely on all-in sustaining costs and annual throughput capacity. The ability to access higher-margin channels, segment customer bases, and participate in downstream economics now determines cash flow quality and valuation resilience.

The Three Pricing Regimes Defining North American Salt Economics

The North American salt market operates across three distinct pricing regimes, each characterized by different contracting mechanisms, margin profiles, and competitive dynamics.

Municipal & State Bulk: Volume Without Alpha

The largest volume segment remains municipal and state government contracts, typically structured as annual tenders for quantities exceeding 100,000 tons. In the United States, these agreements are often governed by the 80/120 supply rule, which requires contractors to deliver between 80% and 120% of the contracted tonnage depending on seasonal severity.

Procurement is almost entirely price-driven. Municipalities issue requests for proposals with detailed specifications, and contracts are awarded to the lowest qualified bidder. This dynamic caps margin upside and favors producers with low operating costs.

Nolan Peterson, Chief Executive Officer of Atlas Salt, describes the strategic trade-off in a November 2025 interview:

"We chose for feasibility study purposes the most conservative market, which is the bulkiest, lowest margin market, and that's deicing road salt. It is low risk because you're selling to governments, you're selling to cities, and the demand is well understood and stable."

Commercial Bulk: Stability Without Pricing Power

Mid-sized commercial contracts represent an intermediate segment, typically negotiated directly with private operators and industrial users. Contract sizes average approximately 10,000 tons annually. This segment offers improved revenue predictability compared to spot sales while maintaining some flexibility, though margins remain constrained.

Retail Packaged Salt: Where the Economics Break Away

The retail segment operates under entirely different economics. Packaged salt sold through consumer-facing channels commands prices that diverge dramatically from those of bulk equivalents.

Margin Mix as a Strategic Variable

Because retail volumes carry margins several multiples higher than bulk, shifting 20% to 30% of production into packaged channels can materially alter EBITDA composition and free cash flow predictability.

Why Channel Mix Changes the Financial Profile

A producer entirely dependent on municipal contracts experiences margin compression when bulk pricing declines, with limited ability to offset through volume growth. Conversely, a producer with diversified channel access can maintain or expand EBITDA even during bulk market weakness.

Free cash flow predictability improves with retail exposure because consumer demand exhibits seasonality different from that of municipal procurement. Retail purchases are often event-driven, triggered by immediate weather forecasts, rather than contractually scheduled, creating natural diversification in cash flow timing.

Pure bulk producers trade at discounts typical of industrial commodity businesses. Producers with credible retail access command valuations more consistent with consumer-adjacent or infrastructure businesses, where recurring revenues and channel partnerships support higher multiples.

Operational Reality Check

Accessing retail economics requires packaging infrastructure, brand development, logistics coordination, and relationships with established distributors. Shelf space is finite and controlled by retailers with sophisticated procurement standards. Most salt producers lack the capital or expertise to build retail capabilities organically.

ESG as an Emerging Factor in Procurement Decisions

Environmental, social, and governance considerations are beginning to influence procurement outcomes in select jurisdictions. While the extent remains uneven, early adopters are establishing frameworks that advantage suppliers demonstrating lower carbon intensity.

The Shift Toward Decarbonization Mandates

The City of Denver provides a concrete example. In 2020, Denver launched an Environmentally Preferred Procurement program that incorporates greenhouse gas emissions into scoring frameworks for municipal contracts. While price remains the primary selection factor, the program introduces point systems that favor suppliers with lower carbon footprints.

Retail brands face parallel pressures regarding Scope 3 emissions, those embedded in purchased goods and services. Procurement teams are beginning to request emissions data from suppliers and, in some cases, prioritizing lower-carbon sources.

Low-Carbon Operations as Competitive Positioning

Atlas Salt's Great Atlantic Salt project in St John's, Newfoundland, demonstrates this approach. The project is designed as an all-electric mine utilizing Newfoundland's abundant hydroelectric power, a battery electric vehicle fleet, and an enclosed overland conveyor system. According to Atlas Salt's August 2024 ESG Report, projected Scope 1 greenhouse gas emissions total only 79 tonnes per year.

Distribution as the Hidden Constraint in Retail Salt

Retail premiums exist not because salt becomes chemically superior when packaged, but because distribution access is scarce and relationship-dependent.

Why Geology Alone Cannot Unlock Retail Premiums

Retail distribution is a logistics-dense, relationship-driven business. Shelf space is allocated based on brand recognition, supply reliability, and the ability to support marketing initiatives. Product must be packaged to retail specifications, delivered on predictable schedules, and supported with promotional capital.

Most salt producers lack both the operational infrastructure and the commercial relationships to access retail channels independently. Building these capabilities organically requires capital investment in packaging facilities, dedicated sales teams, and multi-year relationship development.

Strategic Partnerships as a Margin-Access Mechanism

An alternative approach involves partnering with established distributors that already possess retail relationships and logistics networks. Atlas Salt announced a memorandum of understanding with Scotwood Industries in August 2024. The non-binding agreement targets volume distributions of 1.25 to 1.5 million tonnes per year of packaged salt and contemplates a profit-share mechanism.

This structure allows Atlas Salt to leverage Scotwood's established distribution capabilities and strategic network of packaging facilities. The company's 2025 Updated Feasibility Study incorporated an updated sales mix prioritizing these higher-margin packaged sales.

Building retail distribution capabilities organically requires significant capital and time. Peterson describes the partnership approach:

"We have an MOU with one of them called Scotwood Industries right now. They're the largest distributor of packaged retail deicing salt. But there are other distributors that we are actively courting and they're courting us as well to see what the potential is to do business together."

Asset Longevity & Retail Credibility

Retail buyers prioritize supply security differently than municipal procurement officers. While municipal tenders emphasize near-term price competitiveness, retail partnerships require confidence in multi-decade supply continuity.

Why Retail Buyers Care About Mine Life

Long reserve life provides retail partners with assurance that supply relationships can extend across decades without requiring alternative sourcing. Atlas Salt's Great Atlantic Salt project holds probable reserves of 95.0 million tonnes at 95.9% sodium chloride, supporting an estimated mine life of 24.3 years based on the 2025 Updated Feasibility Study. The wider resource includes 383 million tonnes of indicated resources and 868 million tonnes of inferred resources.

Long-term cash flow visibility underpins retail partnership credibility. Peterson quantifies the project's financial profile:

"The NPV is 920 million Canadian, the IRR after tax 21.3%. And most importantly the thing we like to focus on is the after-tax free cash flow, which is 188 million a year every year on average for the 25-year mine life."

Strategic Geography & Logistics

The Great Atlantic Salt project is located approximately 2km from the Turf Point Deep Water Port on Newfoundland's west coast, with access to the Trans-Canada Highway. This positioning provides access to densely populated northeastern markets while maintaining export optionality.

Domestic production offers measurable advantages over imported supply in both cost and delivery time. Peterson quantifies the differential:

"Our port proximity and our presence in Newfoundland allow us to move the same types of boats that foreign salt does to the same markets in 15 to 20% or sometimes even less the time and the cost, and that gives us huge advantage for shipping and delivery."

Reduced shipping distances compared to imported salt, which primarily originates in Chile, Egypt, Italy, and Morocco, offer both cost and environmental advantages. North American salt markets rely on imports for 20% to 35% of demand, according to Project Blue and United States Geological Survey data.

The structural supply-demand imbalance in North American salt markets creates opportunities for new domestic producers. Nolan Peterson, CEO of Atlas Salt, describes the scale of import dependence:

"What you find is that in North America there is a salt shortage year-over-year when you're balancing domestic production versus domestic needs. So we've had to supplement to the tune of 30 to 40% of our salt needs from other jurisdictions. Egypt and Chile primarily come to mind."

Capital Markets Implications: Re-Rating Through Mix, Not Metal

Salt developers are frequently mispriced because investors apply commodity producer frameworks to assets that increasingly function as differentiated infrastructure plays.

How Investors Typically Misprice Salt Developers

Discounted cash flow models typically assume homogeneous pricing across production volumes, implicitly treating all tons as economically equivalent. This approach systematically undervalues projects that can access higher-margin channels. The error compounds when sensitivity analysis focuses exclusively on bulk pricing and volume assumptions.

Over-emphasis on near-term production metrics also obscures the strategic value of long reserve life. Investors often prioritize speed to production over asset longevity, missing the credibility advantages that multi-decade reserves provide in retail partnerships.

What Changes When Retail & ESG Are Credible

When investors recognize credible retail access and ESG positioning, confidence in forward EBITDA quality improves. Visibility into higher-margin sales reduces perceived commodity exposure and lowers required discount rates.

While salt remains exposed to weather variability and economic cycles affecting municipal budgets, retail exposure provides natural diversification. Consumer purchasing patterns differ from municipal procurement cycles, and retail margins are more resilient during economic downturns due to non-discretionary demand.

The Investment Thesis for Salt

The case for North American salt exposure reflects structural market evolution rather than cyclical commodity dynamics.

- Retail channel access introduces pricing leverage without proportional capital intensity, allowing producers to capture premiums that are structurally insulated from bulk market volatility.

- Non-discretionary deicing demand underpins cash flow resilience across economic cycles, as public safety mandates prevent municipalities from deferring winter road treatment regardless of budget constraints.

- ESG considerations are beginning to influence procurement outcomes in select jurisdictions, particularly among public sector buyers and retail brands focused on Scope 3 emissions reduction.

- Distribution partnerships mitigate execution risk associated with retail market entry while preserving upside optionality, allowing producers to focus capital on mining operations while participating in downstream economics through profit-sharing arrangements.

- New, permitted North American supply addresses structural import dependence in eastern markets, where transportation costs and carbon intensity favor domestic production.

The evolution of the North American salt market is not about higher demand; it is about where margins are earned and who is positioned to capture them. Retail pricing and emerging ESG-driven procurement dynamics in select jurisdictions are reshaping the sector's economic hierarchy, rewarding producers that think beyond bulk tonnage and lowest-cost bids.

This shift reframes salt from a defensive utility exposure into a margin-selective infrastructure asset, where distribution access, carbon positioning, and asset longevity increasingly influence valuation outcomes. Understanding this evolution is critical to accurately pricing the next generation of North American salt producers.

TL;DR

The North American salt market has evolved beyond simple volume economics into three distinct pricing regimes: municipal bulk, commercial, and retail packaged salt. Retail channels command premiums of up to 10 times bulk pricing, meaning producers can materially improve EBITDA and cash flow durability by shifting even 20-30% of sales into packaged retail. Distribution access—not geology—represents the true bottleneck for capturing retail margins, favoring strategic partnerships with established distributors. ESG considerations are emerging as procurement factors in select jurisdictions, with low-carbon operations providing competitive positioning. This structural shift reframes salt from a utility commodity into a margin-differentiated infrastructure asset where channel access, carbon positioning, and reserve longevity increasingly drive valuations.

FAQs (AI-Generated)

Retail salt commands premiums up to ten times bulk pricing not because of chemical differences, but because distribution access is scarce and relationship-dependent. Shelf space at major retailers is finite, requiring brand recognition, supply reliability, packaging infrastructure, and promotional support that most producers cannot build organically.

Select jurisdictions are incorporating carbon intensity into procurement scoring. Denver's 2020 Environmentally Preferred Procurement program, for example, awards points to suppliers with lower greenhouse gas footprints. Retail brands are also increasingly requesting emissions data as part of Scope 3 reduction initiatives.

Retail distribution requires logistics networks, packaging facilities, established retailer relationships, and marketing capabilities that mining companies typically lack. Strategic partnerships with established distributors allow producers to access retail premiums without building these capabilities organically.

Pure bulk producers trade at discounts typical of commodity businesses, while producers with credible retail access command valuations closer to consumer-adjacent infrastructure companies. Shifting 20-30% of production into retail channels can materially alter EBITDA composition and free cash flow predictability.

Retail buyers prioritize multi-decade supply continuity over near-term price competitiveness. A long reserve life provides assurance that supply relationships can be extended without requiring alternative sourcing, making it a key credibility factor in establishing retail partnerships.

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

.jpg)

%20(1).jpg)

Stay Informed