Surging Demand from Manufacturing Recovery and Clean Energy Drives Copper Prices Higher

Surging demand from clean energy, EVs, and manufacturing recovery is driving copper prices higher. Supply constraints and miner expansions add to bullish outlook.

- Copper's superior electrical conductivity makes it a critical component for essential application in the renewable energy and electric vehicle sectors supporting the global transition to clean energy.

- A combination of supply constraints, including limited growth in refined copper production and tight scrap availability, along with recovering manufacturing activity globally, is propelling copper prices higher.

- Leading mining companies, such as BHP and Glencore, are actively increasing their copper production capacities to meet the rising demand from various industries. These strategic expansions demonstrate the miners' confidence in the long-term value and growth potential of the copper market.

- Market analysts present optimistic forecasts for copper prices, with projections ranging from $9,000 to $11,000 per metric ton by the end of 2025. These estimates are driven by expectations of continued supply tightness and robust demand growth across key sectors.

- Geopolitical risks, such as potential trade disputes and tariffs, introduce a degree of uncertainty in the copper market, which could lead to price volatility. Investors must remain vigilant and closely monitor these developments to make informed decisions and manage risk effectively.

Copper, a fundamental industrial metal, plays a pivotal role in various sectors, including construction, electronics, and transportation. The copper market presents a compelling case for investors, driven by a confluence of supply constraints, robust demand, and strategic industry developments.

Demand Drivers: Energy Transition and Economic Factors

The global shift towards renewable energy and electric vehicles (EVs) significantly boosts copper demand. Copper's superior electrical conductivity makes it indispensable in manufacturing EVs, power grids, and renewable energy infrastructure. UBS Global Research projects that copper prices could reach $11,000 per metric ton by the end of 2025, driven by supply tightness and a rebound in manufacturing demand. They estimate a 3.4% demand growth for the year, underscoring copper's critical role in the energy transition.[3]

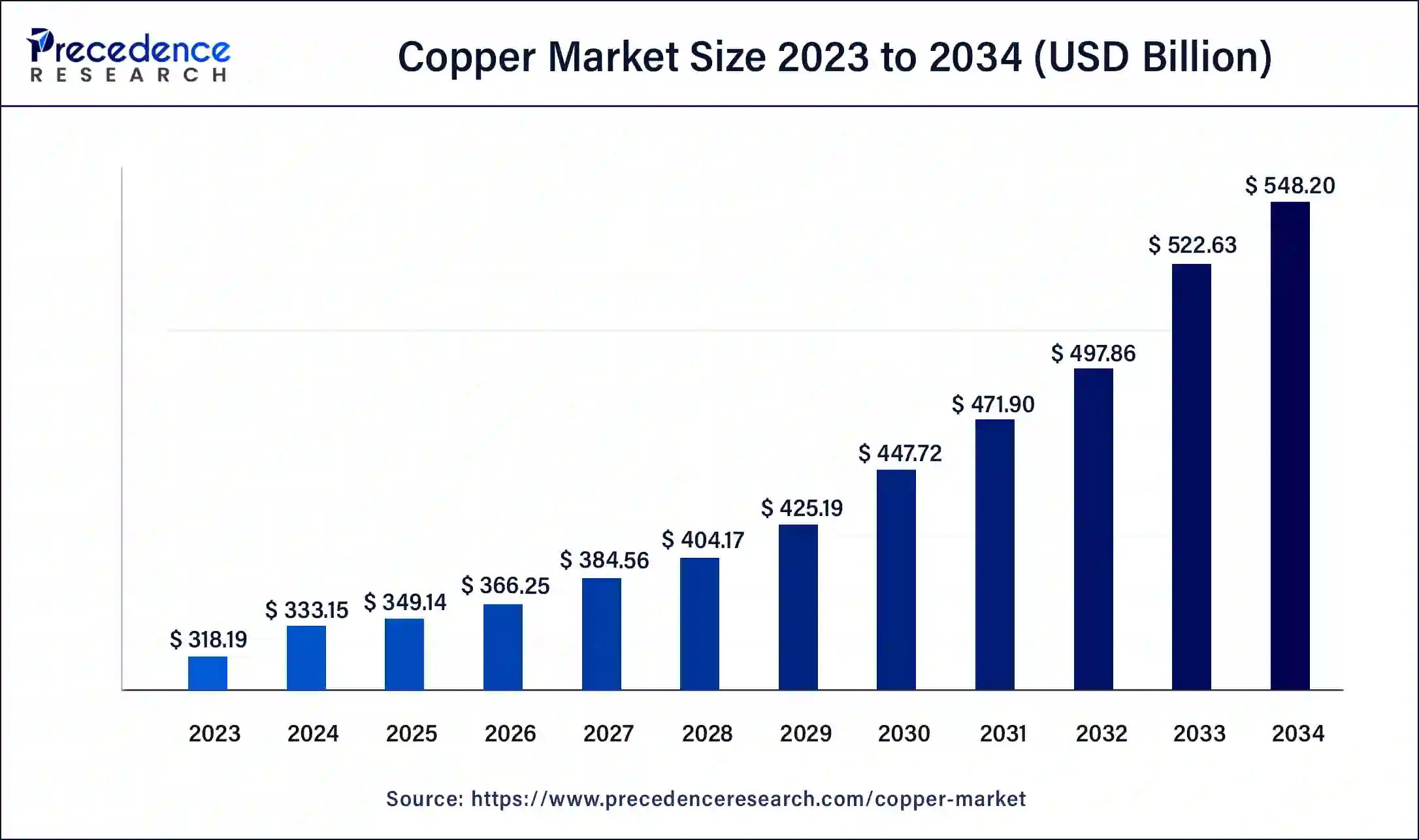

The global copper market size is expected to reach around $350 billion in 2025, expanding at a CAGR of 5.11% from 2024 to 2034.[4]

However, the market faces uncertainties, including potential U.S. trade tariffs under President-elect Donald Trump's administration, which could impact metals-intensive industries. Despite these concerns, China's increased copper imports suggest an economic rebound, contributing to a 4% price rise since early January 2025. This positions copper as the top performer among London Metal Exchange base metals.

Market Outlook and Price Projections

Analysts present varied forecasts for copper prices in 2025. UBS anticipates prices reaching $11,000 per metric ton, citing supply constraints and increasing demand.

Conversely, Bank of America has adjusted its forecast to an average of $9,438 per metric ton, a 12% reduction from previous estimates, due to rising geopolitical tensions and potential trade disputes.

This divergence highlights the market's sensitivity to global economic policies and geopolitical developments.

Copper Production Dynamics

Major mining companies are actively increasing copper production to meet the escalating demand. BHP, the world's largest mining company, reported a 10% rise in copper production over the past six months, primarily due to a 22% increase from its Escondida operations in Chile. This expansion aligns with BHP's projection of a 70% surge in copper demand by 2050. Despite challenges in other segments, BHP remains committed to enhancing its copper assets, including a planned $10 billion investment in Escondida over the next seven years.[2]

Similarly, Glencore, a leading miner and commodity trader, has expressed openness to mergers and acquisitions that bolster shareholder value, emphasizing its position as a top copper producer.[1] This strategy reflects a broader industry trend of consolidating resources to secure copper supply amid rising demand.

Kincora Copper

Kincora Copper's pivot to an asset-level funding model aligns with the copper industry's renewed interest in funding junior explorers to replenish project pipelines. By partnering on 5 of its 12 projects, Kincora has secured up to $60M in funding commitments, demonstrating the value major miners see in promising copper exploration projects. With $3-3.5M spent on partner-funded drilling in 2024 and the potential for $5-10M in 2025, Kincora is well-positioned to benefit from rising copper demand and prices. CEO Sam Spring highlights this industry shift:

"What you're increasingly seeing is relatively generous deals where those majors are willing to give the junior quite an attractive scenario and actually fund that risk of making a discovery."

Almadex Minerals

Almadex Minerals' assembling of a portfolio of 6 early-stage porphyry projects in the Western U.S. in 2024 capitalizes on the region's immense geological potential and stable jurisdiction, key factors for major miners seeking new copper resources. By applying its proven exploration methodology focused on detecting buried porphyry deposits, Almadex is working to make the new copper discoveries needed to meet surging demand from electrification and clean energy.

The company's unique in-house drilling capability provides cost-efficiency and flexibility to rapidly test targets. CEO Morgan Poliquin underscored the opportunity in the context of challenging markets:

"We're starting to see a little change in that and I think there's a little bit more confidence in the copper sector and an increasing recognition of its necessity."

Kavango Resources

Kavango Resources made significant strides in 2024 to advance its dual-focused portfolio of near-term gold production in Zimbabwe and district-scale copper exploration in Botswana. Securing £6.5M in funding and increasing production at its Zimbabwean gold projects has positioned Kavango to be self-funding as it ramps up copper exploration in the highly prospective Kalahari Copper Belt, where majors like Rio Tinto and BHP are also active. With a 5,000m drilling campaign confirming the presence of copper mineralization and identifying 15 high-priority targets, Kavango offers exposure to a potential new copper district in a region that is drawing increased attention from the industry.

Kodiak Copper

Kodiak Copper's upcoming maiden resource estimate for its MPD copper project in British Columbia is a significant milestone that could highlight the company as an attractive investment opportunity in a market hungry for new copper resources. MPD's geological similarities to nearby producing mines and multi-zone porphyry potential suggest the project could develop into an important copper asset as demand surges from global electrification trends.

CEO Claudia Tornquist emphasized the potential for a re-rating, noting

"I think for us there is a good prospect that we'll really see some appreciation and that this will be a good year for our shareholders."

Chairman Chris Taylor also captured the compelling copper macro setup, stating:

"I always remember when I got involved in the business, a friend of mine who's quite clever with the markets always said to me 'You're always one drill hole away with porphyry copper systems from a $100 million market cap', and he's absolutely correct."

Pan Global Resources

Pan Global Resources' plans for an aggressive 2025 exploration program aiming to delineate a 100 million tonne copper resource reflect the urgency to develop new copper supply. The company's Spanish projects offer outstanding discovery potential in a low-risk jurisdiction with a rich mining history. The main focus on expanding the La Romana discovery and drill-testing 5 adjacent targets at the Escacena Project could demonstrate a significant new copper district as the world faces a supply deficit. The copper market's robust fundamentals, driven by electrification and decarbonization, increase the strategic value of Pan Global's portfolio.

Marimaca Copper

Marimaca Copper's extensional drilling success at its Mercedes target in Chile aligns with the copper industry's intensifying search for new supply to meet projected demand growth from electrification and clean energy. From a recent drill result, the high-grade oxide mineralization starts from just 8m depth (as highlighted by a drill hole of 68m at 0.64% CuT) which demonstrates potential to meaningfully extend the mine life of the flagship Marimaca development project.

With the encouraging results from Mercedes, Marimaca Copper has now shifted its exploration focus to drilling the greenfields Sierra de Medina target, follow-up drilling along strike from the recently acquired Pampa Medina deposit, and completing a resource estimate and preliminary economic assessment for Pampa Medina

Chakana Copper

Chakana Copper's new discoveries at the Soledad project in Peru, including the high-grade copper-gold-silver Estremadoyro breccia pipe and Mega-Gold porphyry targets, showcase the potential for multi-deposit copper districts to help fill the looming supply gap. Despite copper's essential role in decarbonization, a lack of new mine development and declining grades necessitate new discoveries.

Chakana's approach of targeting high-grade, near-surface mineralization for a potential low-cost, high-margin operation is well-suited to the inflationary cost environment. Chakana holds 6.7 million tons of resource in high-grade breccias and believes to expand this to 10 million ton high-grade resource starting at surface in their promising location. With 52 of 80 identified breccia targets still untested, Chakana Copper's Soledad offers exposure to ongoing discovery potential.

The Investment Thesis for Copper

Investors considering copper should note the following:

- Supply Constraints: Limited growth in refined copper production due to low treatment and refining charges, coupled with tight scrap availability, may lead to supply deficits.

- Demand Growth: The accelerating adoption of renewable energy and electric vehicles is expected to drive substantial copper demand.

- Strategic Industry Moves: Major mining companies are expanding operations and exploring mergers and acquisitions to secure copper resources, indicating confidence in the metal's long-term value.

- Economic Indicators: China's increased copper imports and anticipated global economic recovery, particularly in manufacturing, support a positive demand outlook.

- Geopolitical Risks: Potential trade disputes and tariffs could introduce market volatility, necessitating careful monitoring by investors.

Conclusion

Copper's strategic importance in the global economy, particularly in the context of energy transition and technological advancements, underscores its investment potential. While supply constraints and robust demand present opportunities for price appreciation, investors should remain vigilant of geopolitical and economic factors that may influence market dynamics. A balanced approach, considering both the promising fundamentals and potential risks, is advisable for those looking to invest in the copper market.

References:

- Denina, Clara, and Desai, Pratima (January 2025). Reuters. Glencore Open to Deals as Investors Brace for More Mining M&A

- Fildes, Nic (January 2025). Financial Times. BHP Boosts Copper Production as Miners Race to Meet Growing Demand

- Acharya, Navamya (January 2025). Investing.com. Copper to be Key Driver of Price Gains Among Industrial Metals in 2025: UBS

- Precedence Research (July 2024). Copper Market Size, Share, and Trends 2025 to 2034

- Home, Andy (January 2025). Reuters. Copper's Early-Year Rally Leaves Investors Unimpressed

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

Stay Informed