The Silver Bull Market: A Strategic Analysis for Natural Resource Investors

Silver market bull run begins: Structural deficits, soaring industrial demand & undervaluation vs gold create generational investment opportunity

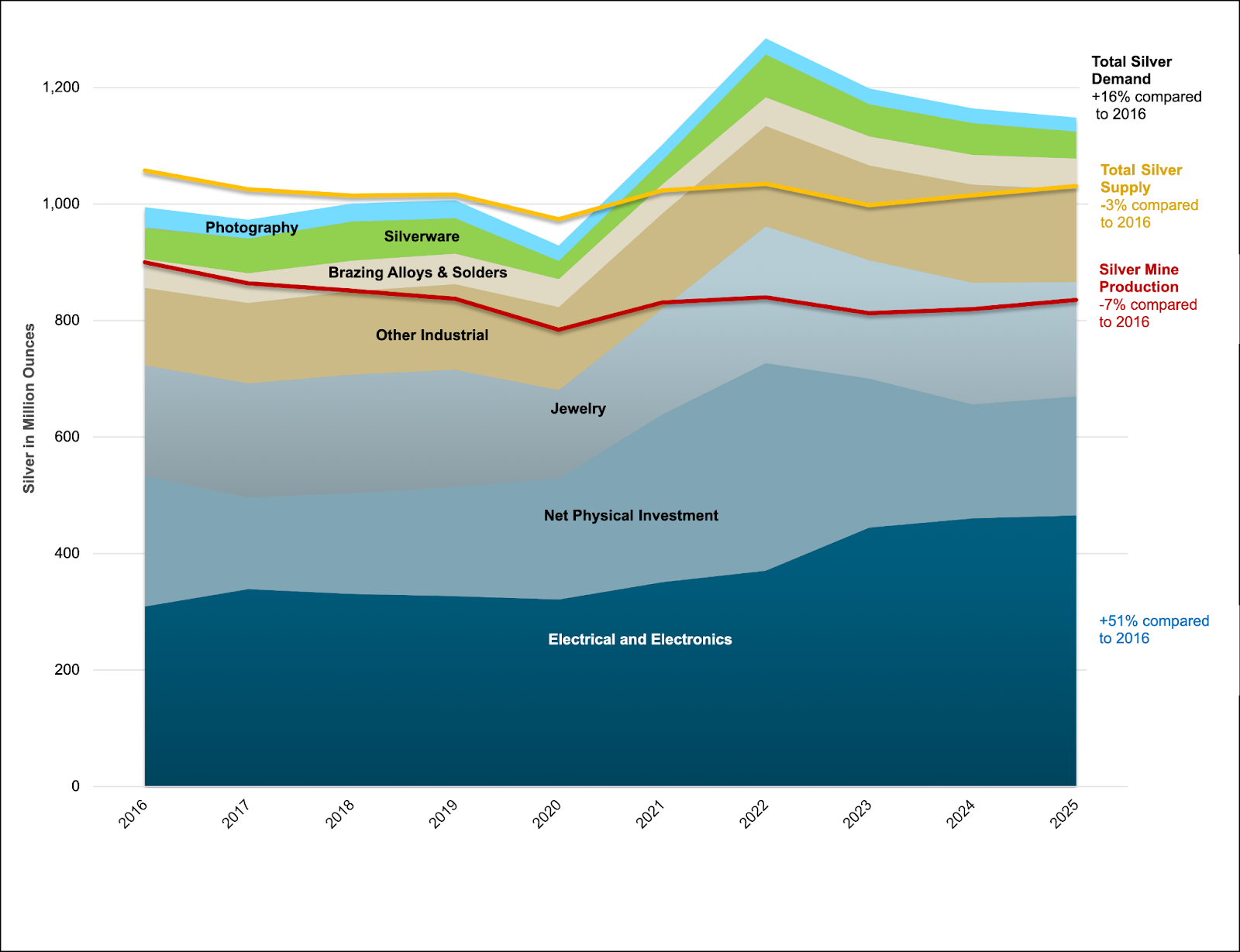

- The silver market has been in deficit for five years, with global demand exceeding supply by about 200 million ounces annually, while only 25% of silver comes from primary silver mines, making it difficult to increase production quickly.

- Industrial applications, particularly solar panels (photovoltaics), now account for 16-19% of global silver demand and are expected to continue growing, creating price-inelastic demand that competes with investment demand for limited supply.

- Silver appears undervalued relative to gold, with the current gold-to-silver ratio at 88:1 compared to the historical average of 65:1, suggesting potential for substantial price appreciation as the ratio normalizes.

- The silver mining stocks are experiencing consolidation with very few quality primary silver producers available globally (only 10 primary producers), creating opportunities for well-positioned companies to become new market leaders.

- Industry executives project silver prices moving through $40 and potentially testing previous highs of $50+, driven by the combination of supply constraints, growing industrial demand, and potential monetary system pressures creating what they believe could be a generational investment opportunity.

Silver Supply Deficit / Silver Demand vs supply

The mathematics of the silver market tell a compelling story. Dolly Varden Silver — which controls over 100,000 hectares in British Columbia's southern Golden Triangle, including five past-producing high-grade silver mines — has been advancing its Kitsault Valley Project with aggressive drilling and strategic acquisitions. The company's flagship Dolly Varden mine historically produced over 20 million ounces of silver at grades exceeding 1,000 g/t, while its Wolf deposit contains an inferred resource of 47.9 million ounces at 537 g/t silver. CEO Shawn Khunkhun outlines the stark reality: "For the last five years, we've been in deficit… we're mining about 850 million ounces a year, recycling another 150, but demand has been in excess of about 200 million ounces per annum."

This deficit becomes even more problematic when considering the structure of global silver production. "Only one out of four silver ounces comes from a pure silver mine," Khunkhun explains. "If the world said we need more silver, it's very difficult to go to the copper miner producing it as a byproduct and say 'increase your production.'"

Endeavour Silver, a mid-tier producer operating mainly in Mexico with additional growth coming from its new Peruvian asset Minera Colpa, expects to lift annual production from approximately 13 million to 20 million silver equivalent ounces by 2026 through its Taranera project ramp-up. The company operates three producing mines in Mexico — Guanaceví, Bolañitos, and Terronera — with a combined mineral resource base exceeding 130 million ounces of silver equivalent. CEO Brad Dickson confirms that "only about 30% of total production comes from a primary silver mine — they're not easy to find."

Vizsla Silver, advancing its flagship Panuco Project in Sinaloa, Mexico, from discovery to feasibility with the aim of becoming the world's largest single-asset primary silver producer, sees the scarcity issue as a key market driver. The company has delineated over 150 million ounces of silver equivalent in measured and indicated resources at its district-scale property, which covers 9,386.5 hectares in the prolific Sierra Madre Occidental. CEO Michael Konnert observes that "very few jurisdictions globally can support a silver primary mine of meaningful margin or grade… investors don't really understand how scarce and rare a profitable silver primary producer can actually be."

Industrial Demand: The Game-Changer

While silver has historically been viewed primarily as a precious metal investment, industrial applications are now driving unprecedented demand growth. GR Silver Mining, focused on its 100%-owned Plomosas Project in Sinaloa, Mexico — a 78 km² district-scale asset hosting both past-producing mines and high-grade exploration targets — is strategically positioned in a jurisdiction aligned with energy transition goals. The Plomosas district historically produced over 30 million ounces of silver and features multiple zones of mineralization across a 20-kilometer strike length, including the San Marcial deposit with its high-grade silver-lead-zinc mineralization. CEO and President Márcio Fonseca, highlights one key sector:

"Photovoltaics… 16% of global demand in 2023, expected to be about 19% in 2024 — Mexico is brilliantly positioned to participate in the energy transformation and decarbonization."

What makes this industrial demand particularly significant is its resilience and growth trajectory. Khunkhun observes that "a small decrease in photovoltaic demand is not going to offset the rise in silver… when one input decreases, Samsung comes out with a kilo silver battery that charges your car in under 10 minutes and gives you a range of 600 miles."

The geographical spread of this demand adds another layer of sustainability. "Demand is coming out of Russia, India, and China — and I don't see that slowing down," Khunkhun notes.

The Investment Paradigm Shift

Perhaps the most significant development in the current silver market is the competition between industrial and investment demand. Historically, investment flows have been the primary driver of silver's spectacular bull market moves. However, Khunkhun identifies a crucial difference this cycle: "Historically, whether you're a speculator or an investor… people come into silver for those bull markets — but this time industry is competing for half the supply."

This creates a fundamentally different dynamic where price-inelastic industrial demand provides a floor while investment demand can still drive explosive upside moves. As Konnert explains, "Silver sits at this crossroads of industrial growth and monetary anxiety… when that happens, the silver moves can be explosive and the silver equities can absolutely outperform their gold counterparts."

The changing investor base reflects this evolution. Dickson notes that "our shareholder base is changing because the company is changing… from a junior mid-tier to a mid-tier senior… generalists are coming in, moving from gold into silver." Konnert adds that "we definitely saw a new type of shareholder… a slight uptick of mainstream interest in silver and silver equities."

Fonseca from GR Silver emphasizes what sophisticated investors are seeking: "The market is on the hunt for companies with… cash flow, a development project two or three years out, and scalability. That complete package is what's rewarded."

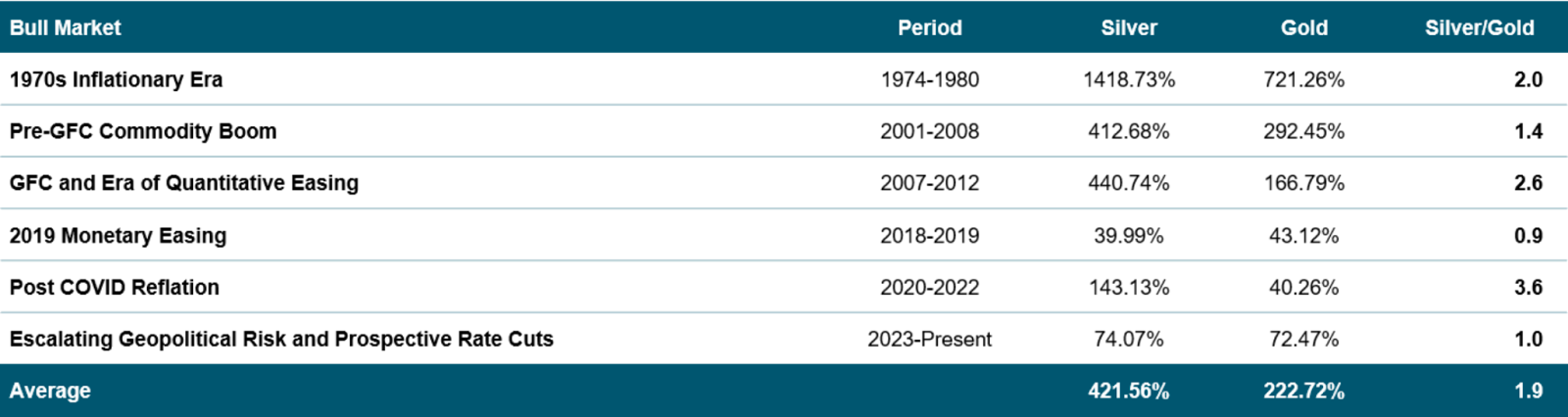

Valuation Opportunity: The Gold-Silver Ratio

From a relative valuation perspective, silver appears significantly undervalued compared to its historical relationship with gold.

Dickson points out that "We're sitting in an 88 to 1 silver to gold ratio… historically that's 65 to 1. In 2011… it got as close to 32 to 1. We're in that environment right now for silver."

Konnert believes this ratio will normalize: "We're still way out of whack… trending back down to a more reasonable level, that 60 to 1… every single time that gold has made a parabolic move, silver has lagged, then followed, and then outperformed."

This compression potential creates significant opportunities for producers. As Konnert calculates, "At $40 silver… typical silver producer ASIC near $20 — that's great margin… attractive to a broader group of investors."

Evaluating Silver’s Performance Versus Gold

Silver and gold are precious metals often used as hedges against inflation, economic uncertainty, and currency fluctuations. A key metric for comparing their relative performance is the gold-silver ratio, which measures how many ounces of silver it takes to buy one ounce of gold (calculated as gold spot price ÷silver spot price).

Current Gold-Silver Ratio: Approximately 87.9 (based on current spot prices of gold at ~$3,105.80 per ounce and silver at ~$35.34 per ounce). This is on the higher end of the modern historical range (typically50-80), suggesting silver is relatively undervalued compared to gold right now. Historically, the ratio has averaged around 60-70 since1915, with extremes like nearly 100:1 in 2020 during market volatility and as low as 20:1 in 1980.

2025 Performance Comparison:

Silver has outperformed gold year-to-date (YTD) in 2025,gaining about 31.45% compared to gold's 28.27% (based on ETF proxies SLV andGLD). As of early August 2025, silver was trading near $37.50 per ounce and had risen nearly 30% for the year, driven by strong industrial demand(e.g., in solar panels, electronics, and EVs).

However, over the past 1 year, gold has performed better, up 35.41% versus silver's 28.42%.

In the first half of 2025, silver gained 24.94%, building on momentum from prior years, while gold hit new record highs above $3,000 per ounce. Analysts expect silver to potentially continue outperforming gold in the second half of 2025 due to supply shortages and industrial uses, with some forecasts targeting $40+ per ounce for silver.

Overall, silver offers higher growth potential but with more volatility, while gold provides more stability. A balanced portfolio might include both for diversification.

Gold Trends

Gold has been on a strong upward trajectory in 2025, surpassing $3,000 per ounce and setting new records in major currencies. Drivers include central bank buying, geopolitical tensions, and inflation concerns. Today's price is up ~1.07% from the previous close, with a bullish outlook but potential resistance near $3,176 (52-week high equivalent).

Silver Trends

Silver has surged even more aggressively, up ~2.11% today and nearing its 13-year high from June 2025. Industrial demand (e.g., from green energy) and supply deficits are key factors. If trends continue, silver could test $40 per ounce by year-end, outpacing gold.

The Silver Squeeze Scenario

Market structure changes are setting up what some analysts call a potential "silver squeeze." Khunkhun explains that "freely traded inventories have been diminished, making the metal more sensitive to incremental buying."

The consolidation in the sector adds to this dynamic. Konnert notes that "the last three meaningful transactions in the entire silver space have been in Mexico… scarcity continues to increase."

Kootenay Silver, a Mexico-focused explorer with four silver discoveries totaling over 300 million ounces in M&I and Inferred categories, is advancing its Colombo Project in Chihuahua — a high-grade, wide-vein system with potential to exceed 100 million ounces. The company's portfolio also includes the La Negra, Promontorio, and Copalito projects, all located in prolific silver districts. The Colombo project features mineralization across a 6-kilometer strike length with individual veins ranging from 1 to 20 meters in true width and grades averaging over 200 g/t silver equivalent.

CEO Jim McDonald frames the upside: "Silver hasn't even caught up to the median gold ratio… our strong belief is that it will, and then go beyond it… industrial demand plus monetary demand is where you get the real slingshot effect of silver outperforming gold."

Historical Context

The silver market's historical performance during precious metals bull markets provides important context for current opportunities. Khunkhun observes that "people come into the silver space… for the moments where you enter a precious metals bull market and silver outperforms gold. It has in every previous precious metals bull market."

The key for investors is positioning ahead of these moves. McDonald emphasizes the importance of contrarian timing: "Buying at the bottom of the market is not easy… but we knew the metal price was going to go higher. It's really important to focus on being countercyclical."

Geopolitical Factors

The broader macroeconomic environment is creating additional tailwinds for precious metals. Dickson identifies the psychological component: "The uncertainty out there creates anxiety and that anxiety normally takes investment away from traditional assets… now you're getting into metals… everyone trying to secure their own metals for their own country."

He breaks down the dual nature of silver demand: "From the industrial side of silver… that's easy, that's supply-demand… The monetary side is psychological — belief in the US dollar and where it's going."

Mexico's position as the world's largest silver producer adds geopolitical considerations. Khunkhun notes that "Mexico is the number one silver producing nation… 70% of Mexican silver comes from open pits, and there's a reluctance to permit new operations. If those projects don't move forward, it could be quite problematic."

However, changing trade dynamics may be creating opportunities. Konnert suggests that "tariff issues between the US and Mexico have probably created a higher willingness for Mexico to permit mines like ours."

Strategic Asset Development & Corporate Positioning

The development strategies of leading silver companies reveal different approaches to capitalizing on the bull market thesis. Dolly Varden's strategy focuses on high-grade, underground assets in stable jurisdictions, with recent acquisitions including the Homestake Ridge project, which adds significant gold-silver potential to their British Columbia portfolio.

Endeavour Silver's multi-asset approach provides both production stability and growth optionality. The company's Terronera mine in Jalisco represents its newest operation, featuring mechanized mining methods and higher-grade mineralization that should improve overall unit costs and margins.

Vizsla Silver's district-scale consolidation strategy at Panuco represents one of the largest silver development projects globally. The company has identified over 500 targets across the property and continues to expand the resource base through systematic drilling programs.

GR Silver Mining's focus on the historic Plomosas district leverages existing infrastructure and geological knowledge while targeting both near-term production scenarios and longer-term resource expansion. The district's mineral endowment includes significant lead and zinc credits that could enhance project economics.

Kootenay Silver's asset-building strategy specifically targets creating value for eventual strategic buyers. The company's systematic approach to resource delineation across multiple projects provides optionality and scale attractive to larger producers seeking growth through acquisition.

Investment Strategy

For natural resource investors, the key is identifying companies positioned to capitalize on this cycle. Fonseca from GR Silver outlines what the market is seeking: "What the market wants right now is consolidation in the silver space… creation of companies with critical mass… a cash-flowing asset, a pipeline project, and exploration scalability. That complete package is what's rewarded."

The scarcity of quality assets creates opportunities for the right companies. Khunkhun sees potential for new market leaders: "There are only 10 primary silver producers, and many get less than 30% of their production from silver… I see an opportunity for a new go-to name in the sector."

For development companies, de-risking becomes crucial. McDonald explains: "You start to demonstrate you're going to have the size needed to support a mine build… the more you de-risk, the more value for a buyer."

Operational Excellence & Technical Advantages

The technical quality of silver projects becomes increasingly important as the market matures. Dolly Varden's high-grade underground assets offer operational advantages through selective mining of rich ore zones, potentially delivering lower capital intensity and higher margins compared to bulk tonnage operations.

Endeavour Silver's operational track record across multiple Mexican jurisdictions provides valuable experience in navigating permitting, community relations, and technical challenges. This operational expertise becomes particularly valuable as new projects advance through development phases.

Vizsla Silver's district-scale opportunity allows for phased development approaches, potentially reducing capital requirements while building operational experience. The company's technical team has identified multiple mineralization styles across the property, suggesting long-term production potential. GR Silver Mining's focus on proven geological districts reduces exploration risk while leveraging existing infrastructure and community relationships. The company's technical approach emphasizes both underground and open-pit scenarios, providing operational flexibility. Kootenay Silver's systematic resource development approach across multiple projects provides diversification of geological and operational risk while building scale attractive to potential acquirers.

Price Targets & Market Outlook

Industry executives are increasingly bullish on silver's price trajectory. McDonald projects that "we think silver's going through $40… once it does, it's going to test the old highs of $50 and beyond."

The consolidation theme extends beyond just price appreciation. Dickson believes that "in the primary silver space, there aren't that many assets available… scarcity in high-quality silver will keep driving consolidation."

These price projections are based not just on historical patterns but on fundamental supply-demand mathematics that appear increasingly favorable for silver. The combination of constrained primary supply, growing industrial demand, and potential investment flows creates a compelling setup for sustained price appreciation.

Risk Factors & Market Considerations

While the bull market thesis appears strong, investors should consider several risk factors. Regulatory changes in key producing jurisdictions, technological substitution in industrial applications, and broader economic conditions could impact silver demand and pricing.

Mexico's regulatory environment remains a key consideration for companies operating in the world's largest silver-producing nation. Recent policy changes and ongoing political developments require careful monitoring by investors and companies alike.

Operational execution risk remains significant in the mining sector. Companies advancing projects from exploration through development and production face numerous technical, financial, and operational challenges that can impact timelines and returns.

Market volatility in precious metals can be extreme, particularly for silver given its smaller market size and dual industrial-monetary role. Investors should prepare for significant price swings even within a broader bull market trend.

For Investors

The convergence of supply constraints, industrial demand growth, investment flow changes, and relative valuation opportunities suggests that the silver market is entering a new phase. Konnert captures the sentiment: "I think this is the beginning of what is more likely to be a sustained upward trend in the market… the early stages of a cycle for silver and gold."

For natural resource investors, the message is clear: silver represents both a defensive hedge against monetary uncertainty and an offensive growth opportunity driven by industrial demand. The companies that can successfully navigate this environment—those with quality assets, operational expertise, and strategic positioning—stand to deliver exceptional returns as this cycle unfolds.

The silver bull market thesis is built on fundamental supply-demand imbalances that appear likely to persist and intensify. The scarcity of primary silver producers, combined with growing industrial demand and potential monetary system pressures, creates a setup that could deliver sustained outperformance relative to other commodity sectors.

Investors who position themselves thoughtfully in this space, focusing on companies with proven management teams, quality assets, and clear development pathways, may look back on this period as one of the most compelling entry points in decades. The key is identifying the right companies at the right stage of development, with the operational expertise and financial resources to capitalize on what industry leaders believe could be a generational opportunity in the silver market.

Analyst's Notes

Subscribe to Our Channel

Stay Informed