Why Smart Investors Are Betting on Salt Supply Shortage

North America's salt supply gap creates investment opportunity. Atlas Salt's 4Mtpa project addresses import dependency with superior economics, ESG profile, and strategic location.

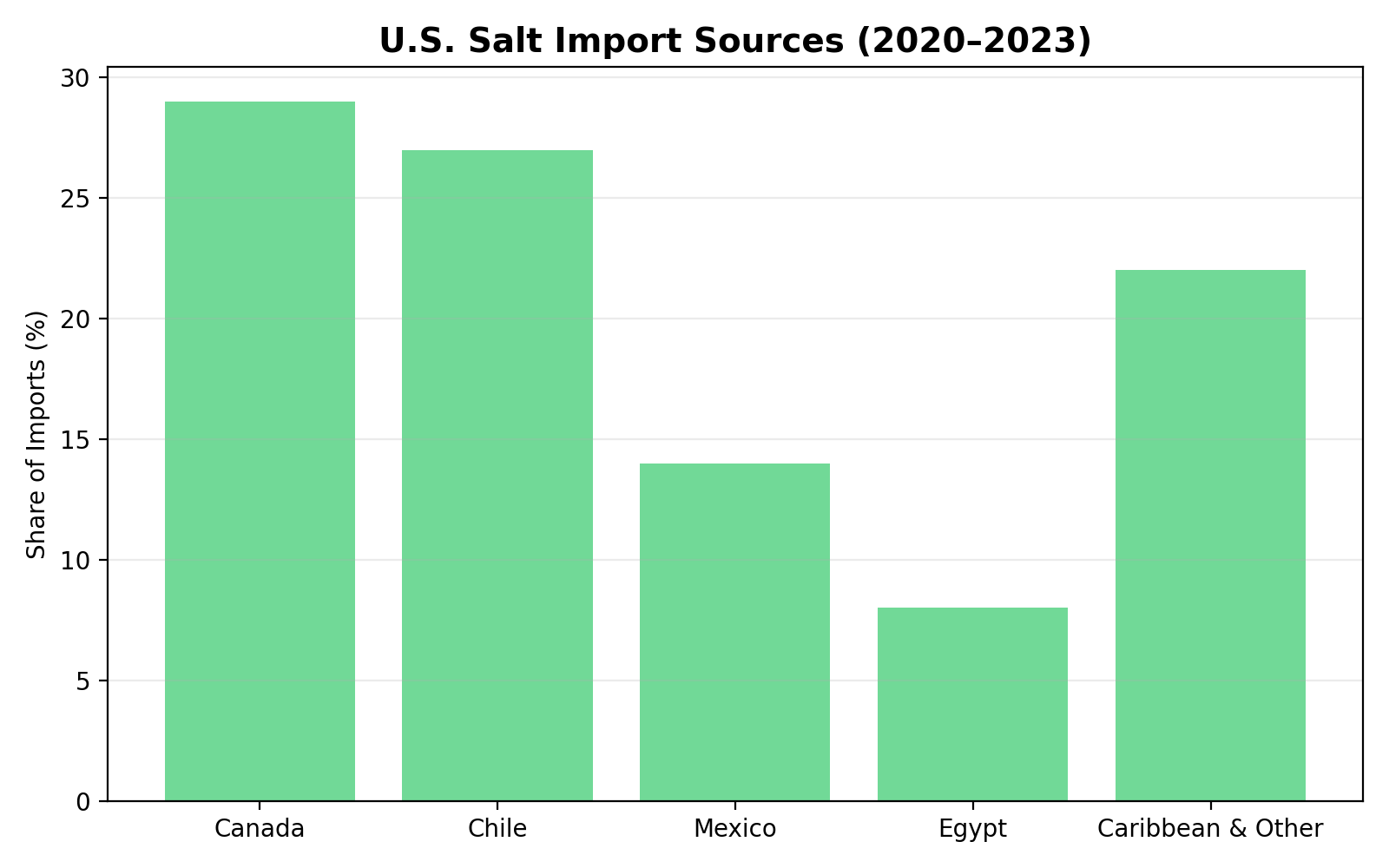

- North America imports 8-10 million tonnes per annum of de-icing salt despite being a major consumer market (28.5-36 Mt annual demand worth $2.3B-$2.9B). The U.S. imported 67.5 Mt of salt between 2020-2023, primarily from Chile (27%), Mexico (14%), Egypt (8%), and Caribbean sources (22%), creating long supply chains vulnerable to geopolitical disruption and exposing buyers to significant freight cost volatility.

- North America's salt mining infrastructure is demonstrably aging, with most major producing mines operating for 50+ years. Cargill's 2021 closure of the Avery Island mine removed 2.5 Mt/year of domestic supply from U.S. east coast markets, while environmental concerns have left Cargill's remaining New York and Cleveland assets unsold since 2023. No new salt mine of comparable scale to Atlas Salt's 4 Mtpa project has been developed in North America for nearly three decades, positioning new domestic supply as a strategic market advantage.

- Rock salt prices in the USA have demonstrated consistent growth at a 4.2% CAGR, rising from approximately $20/tonne in 2000 to $60/tonne in 2024. The global crude salt market is forecast to expand from $16.1B in 2025 to $23.2B by 2032 (5.2% CAGR), underpinned by essential industrial demand (chemical processing, water treatment), infrastructure requirements (de-icing), and agricultural/food processing applications that provide demand diversification and resilience.

- Recent M&A activity demonstrates institutional confidence in salt asset values, most notably German-based K+S's 2020 sale of Americas salt assets (Morton Salt, Windsor Salt) to Stone Canyon Industries for $3.2B, representing 12.5x 2019 EBITDA. This transaction established a valuation benchmark that significantly exceeds Atlas Salt's current enterprise value relative to its projected cash flows, suggesting material upside potential as the project advances toward production.

- Atlas Salt's shallow deposit (approximately 180m vs. 600m+ for legacy mines like Goderich), access to clean hydropower, all-electric operations, and proximity to major east coast markets (3 days shipping to Boston vs. 14+ days from Egypt/Chile) create compelling cost and ESG advantages. The project's scope 1 GHG emissions of just 79 tonnes/year, equivalent to four Newfoundland households, positions it among the lowest-carbon mining operations globally, aligning with institutional investors' increasing focus on sustainable commodity supply chains.

An Overlooked Essential Commodity at an Inflection Point

While lithium, copper, and rare earths dominate mining sector headlines, a far more fundamental commodity is quietly approaching a critical supply inflection point in North America. Salt is an essential material for road safety, chemical production, water treatment, and food processing. It faces structural supply constraints that have largely escaped investor attention despite favorable market dynamics and compelling project economics.

The North American salt market presents a paradox: robust and growing demand for a critical infrastructure commodity, coupled with aging production infrastructure, recent mine closures, and heavy reliance on imported supply from geopolitically distant sources. This supply-demand imbalance is creating investment opportunities in new domestic salt production, particularly as legacy mines face operational challenges and no comparable new projects have entered production in nearly three decades.

The global salt market reached approximately $26 billion in 2024, with North American de-icing salt consumption alone representing 28.5 to 36 million tonnes annually, valued between $2.3 billion and $2.9 billion. Yet North America imports 8 to 10 million tonnes per annum of de-icing salt to meet this demand, with the United States importing 67.5 million tonnes of salt between 2020 and 2023 primarily from Chile, Mexico, Egypt, and Caribbean sources. This dependency on distant suppliers creates vulnerabilities around freight costs, shipping logistics, and supply security. These concerns have intensified as legacy North American mines age and face environmental challenges.

Global Salt Market: Steady Growth Underpinned by Diversified Demand

.png)

The global crude salt market was valued at approximately $16.1 billion in 2025 and is forecast to expand to $23.2 billion by 2032, representing a compound annual growth rate of 5.2 percent. This growth trajectory reflects salt's role as an essential commodity across multiple end markets, providing demand stability that differentiates it from more cyclical commodities.

Salt production is highly concentrated geographically, with China, the United States, India, and Europe representing the largest producing regions. Between 2020 and 2024, global production has remained relatively stable at approximately 280 to 290 million tonnes per year, demonstrating the mature nature of the industry while highlighting limited capacity additions to meet growing demand.

Unlike commodities dependent on a single end-use sector, salt benefits from demand diversification across industrial, commercial, and consumer applications. Industrial usage, primarily chemical processing for chlorine, caustic soda, and soda ash production, represents the largest demand segment globally. De-icing applications constitute approximately 13 percent of the global salt market but represent a much larger proportion of North American consumption due to climate patterns and extensive road networks. Water treatment, oil and gas applications, agriculture, and food processing provide additional demand channels that support baseline consumption regardless of economic cycles. This demand diversification creates stability: while de-icing consumption varies with winter weather severity, industrial chemical demand remains consistent, and food processing and agriculture provide counter-cyclical support during economic downturns.

Rock salt prices in the United States have demonstrated consistent appreciation, rising from approximately $20 per tonne in 2000 to $60 per tonne in 2024, representing a 4.2 percent compound annual growth rate. This sustained price appreciation reflects underlying supply-demand fundamentals rather than speculative dynamics, as salt's bulk nature and relatively low per-unit value limit financial market participation. Price increases have accelerated in recent years as supply constraints have tightened, with North American buyers facing particular pressure due to import dependency and rising freight costs.

North America's Strategic Supply Challenge

North America's reliance on imported salt creates exposure to multiple risk factors that domestic production can mitigate. Between 2020 and 2023, the United States imported 67.5 million tonnes of salt, with Canada (29 percent), Chile (27 percent), Mexico (14 percent), and Egypt (8 percent) representing primary source countries. Shipping distances from Chile or Egypt to major North American east coast consumption markets exceed 14 days versus approximately three days from Newfoundland locations, introducing logistics complexity and freight cost exposure.

North America's existing salt production infrastructure is demonstrably aging, with most major producing mines having operated for 50 to 60+ years. Goderich mine in Ontario, North America's largest at 7 to 9 million tonnes per year capacity, began production in 1959 after being discovered in 1866. Cargill's 2021 announcement of closure for its Avery Island salt mine in Louisiana, which had operated since the mid-1800s, removed 2.5 million tonnes per year of domestic supply from U.S. east coast de-icing markets.

Perhaps most significantly for investors evaluating new salt projects, no new salt mine of comparable scale has been developed in North America for nearly three decades. American Rock Salt mine in New York, which opened in 2001, represented the newest significant capacity addition at more than 3 million tonnes per year production. This development gap reflects the capital intensity of underground mining projects, long permitting timelines, and until recently, sufficient existing capacity to meet demand growth. However, the combination of mine closures, aging infrastructure, and growing consumption has created a supply gap that existing operations cannot fill.

Atlas Salt: A Case Study in Strategic Development

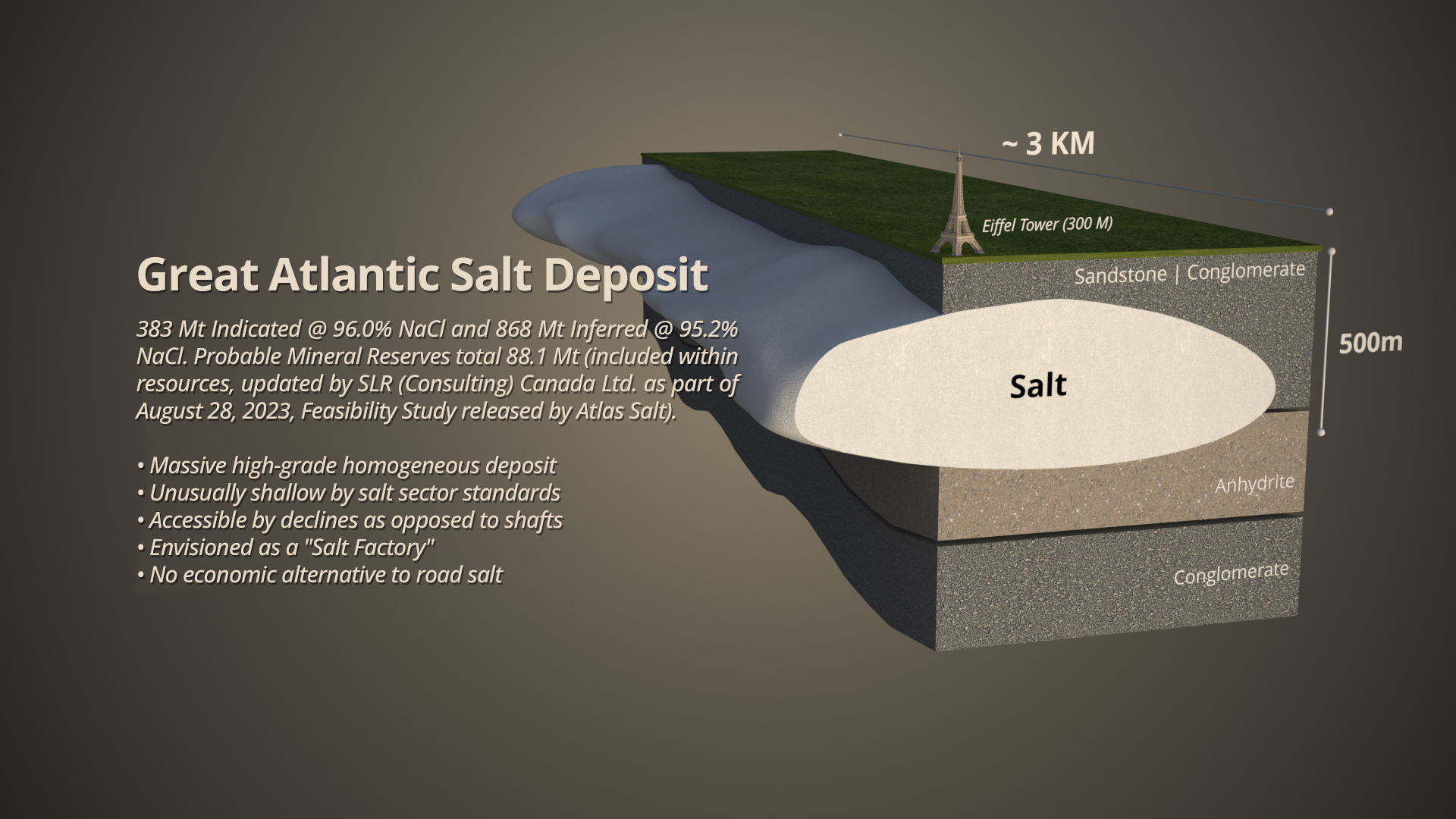

The Great Atlantic Salt Project in Newfoundland, Canada, exemplifies how new supply can address North American market needs while offering attractive project economics. The deposit hosts Probable reserves of 95.0 million tonnes at 95.9 percent NaCl grade, providing a 24.3-year mine life at planned production rates, with an additional 868 million tonnes of inferred resources at 95.2 percent NaCl grade that could support future production increases or mine life extensions.

"The deposit geometry allows for a compact, efficient site layout with consistent ore access and reduced development time. The shallow depth of approximately 180 meters from surface, compared to 600+ meters for legacy mines like Goderich, enables access via declines rather than costly shaft sinking, reducing upfront capital requirements and accelerating project development timelines."

Resource quality is critical for salt projects, as buyers specify minimum purity thresholds. The Great Atlantic deposit averages 95.9 percent NaCl across reserves, with significant concentrations of higher-grade material exceeding 98 percent NaCl, providing optionality to serve premium markets or blend production to meet varying customer specifications.

Atlas Salt's September 2025 Updated Feasibility Study demonstrated substantial improvements to project economics, outlining after-tax economics of $920 million NPV at an 8 percent discount rate, a 21.3 percent internal rate of return, and a 4.2-year payback period. Initial capital expenditure is estimated at $589 million, with total life-of-mine sustaining capital of $609 million, generating life-of-mine average annual post-tax cash flow of approximately $188 million. Operating costs of $28.20 per tonne shipped position the project competitively against both domestic producers and imported supply when logistics costs are considered.

The Updated Feasibility Study outlines a production profile reaching 4.0 million tonnes per year nameplate capacity. Target markets include Atlantic Canada, Quebec, and the U.S. east coast, which collectively consume 11 to 16 million tonnes per annum of road salt. The project's location provides significant logistics advantages: shipping time to Boston is approximately three days versus more than 14 days from Egypt or Chile.

Nolan Peterson, CEO of Atlas Salt mentioned their feasibility study:

"Atlas Salt is developing North America's first new salt mine in nearly three decades at a time when the continent faces growing import dependency and aging production infrastructure. The Great Atlantic project offers buyers secure, domestic supply with superior logistics and environmental performance compared to imported alternatives."

Sustainability considerations increasingly influence procurement decisions. Atlas Salt's environmental profile offers distinct advantages: all-electric operations powered by clean hydropower, no tailings or chemical processing, and minimal surface disturbance. A January 2024 greenhouse gas emissions study validated the project's scope 1 emissions at just 79 tonnes per year, equivalent to four Newfoundland households, positioning it among the lowest-carbon mining operations globally.

Investment Implications & Strategic Considerations

Recent merger and acquisition activity in the North American salt sector provides valuable valuation context. In May 2020, German-based K+S sold its Americas salt business including Morton Salt and Windsor Salt to Stone Canyon Industries Holdings for $3.2 billion, representing 12.5 times 2019 EBITDA. This transaction established a clear valuation benchmark for operating salt assets with established customer bases and cash flow generation.

Mining project valuations typically follow a predictable pattern of re-rating as development risks are retired and production approaches. Atlas Salt has achieved several key de-risking milestones: completion of an Updated Feasibility Study, environmental assessment release, and approval of an early works development plan. Remaining value inflection points include securing project financing, finalizing offtake agreements, and commencing construction activities.

From a portfolio construction perspective, salt exposure offers several attractive characteristics for resource-focused investors. The commodity's essential nature and limited substitution alternatives provide demand stability that contrasts favorably with cyclical base metals or technology-dependent battery materials. Supply dynamics further differentiate salt from more crowded commodity spaces, as the 30-year gap in new North American salt mine development creates a less competitive environment for well-positioned projects.

The Investment Thesis for Salt

- Atlas Salt's Great Atlantic project directly addresses North America's structural 8-10 Mtpa de-icing salt import dependency by providing strategically located domestic production. The project's Newfoundland location enables three-day shipping to major east coast markets versus 14+ days from Egypt or Chile, delivering significant logistics cost advantages and supply security for buyers.

- The September 2025 Updated Feasibility Study demonstrates after-tax NPV8 of $920M, 21.3% IRR, and 4.2-year payback on $589M initial capex. Operating costs of $28.20/tonne and all-in sustaining costs of $34.90/tonne generate $74.50/tonne margins at the base case price of $118.40/tonne, providing substantial margin safety.

- Key de-risking milestones include completion of the Updated Feasibility Study, provincial environmental assessment release, early works development plan approval, and strategic partnership agreements with industry leaders including Scotwood Industries, Sandvik, and Hatch.

- The 868 Mt inferred resource at 95.2% NaCl grade, excluded entirely from the current 24.3-year production plan, represents significant upside potential if converted to reserves, potentially supporting production increases beyond 4 Mtpa nameplate capacity or extending mine life.

- Scope 1 greenhouse gas emissions of just 79 tonnes/year position Atlas Salt among the world's lowest-carbon mining operations. All-electric operations powered by Newfoundland's clean hydropower grid create compelling advantages as government and institutional buyers increasingly prioritize low-carbon supply chains.

- Salt's essential infrastructure role, limited substitutes across applications, and diversified end-use markets provide demand stability uncorrelated to economic cycles, offering portfolio allocation opportunities for mining-focused investors seeking lower volatility exposure while maintaining growth potential.

The North American salt market presents robust fundamentals, structural supply constraints, and favorable long-term demand growth, yet limited investor attention compared to more headline-generating commodities. The investment case rests on demonstrable supply constraints as legacy mines age and close, import dependency creating strategic vulnerabilities, no comparable new production entering the market for three decades, and stable demand growth driven by infrastructure requirements and industrial applications.

Projects like Atlas Salt's Great Atlantic deposit exemplify how new supply can address market needs while generating compelling returns. The combination of high-quality resources, favorable geology enabling low-cost production, strategic location minimizing logistics costs, and strong environmental performance positions such projects to capture value as North American buyers seek alternatives to imported supply. The salt sector may lack the excitement of battery metals or precious metals, but for investors focused on sustainable cash flows, favorable supply-demand dynamics, and lower volatility, it merits serious consideration as portfolio diversification and strategic positioning.

TL;DR

North America faces a structural salt supply crisis driven by aging infrastructure, import dependency, and a 30-year development gap in new mine construction. The continent imports 8-10 million tonnes annually, with U.S. imports totaling 67.5 Mt from 2020-2023 primarily from Chile, Mexico, and Egypt. Legacy mines averaging 50+ years in operation face closure risks, exemplified by Cargill's Avery Island shutdown that removed 2.5 Mtpa from domestic supply. Atlas Salt's Great Atlantic project represents the first significant new North American salt mine in nearly three decades, offering 4 Mtpa production with superior economics ($920M after-tax NPV8, 21.3% IRR), strategic location enabling 3-day delivery to east coast markets versus 14+ days from overseas suppliers, and industry-leading environmental performance with just 79 tonnes/year scope 1 emissions. The investment opportunity combines defensive demand characteristics from salt's essential infrastructure role with favorable supply-demand dynamics, conservative pricing assumptions providing downside protection, and 868 Mt of expansion resources offering significant upside potential in an overlooked commodity sector.

FAQs (AI-Generated)

North America doesn't face an absolute salt shortage, but rather a domestic production deficit requiring significant imports to meet demand. The continent consumes 28.5-36 million tonnes annually of de-icing salt alone, yet imports 8-10 million tonnes per year to fill the gap. This deficit has widened due to aging mine infrastructure, recent closures like Cargill's Avery Island mine, and virtually no new major salt mine development over the past three decades.

Atlas Salt demonstrates superior economics with after-tax NPV8 of $920M, 21.3% IRR, and 4.2-year payback on $589M initial capex, exceeding typical mining project thresholds. Its strategic location enables three-day shipping to major east coast markets versus 14+ days from overseas suppliers. The shallow deposit depth eliminates expensive shaft sinking requirements, reducing upfront capital and accelerating development timelines.

Salt demonstrates exceptional demand stability due to its essential nature across diversified end-use markets with limited substitutes. Industrial chemical processing uses salt as primary feedstock for chlor-alkali production, while de-icing applications create non-discretionary demand driven by road safety requirements. The global crude salt market is forecast to grow from $16.1B (2025) to $23.2B (2032) at 5.2% CAGR.

Salt mining investments face construction execution risk, offtake concentration, weather variability affecting de-icing demand, financing risk, permitting delays, and competition from imports. Atlas Salt mitigates these through partnerships with industry leaders, diversified offtake strategies, conservative pricing assumptions, and environmental assessment completion.

Salt offers exceptional demand stability from essential applications, significantly lower price volatility than cyclical base metals or battery materials, limited new supply pipeline due to the 30-year development gap, and counter-cyclical demand characteristics providing recession resistance. However, it has lower per-unit values requiring higher volumes and less investor familiarity potentially limiting valuation multiples.

Analyst's Notes

Subscribe to Our Channel

Stay Informed