The Silver Investment Opportunity: Why 2025 Could Be the White Metal's Breakout Year

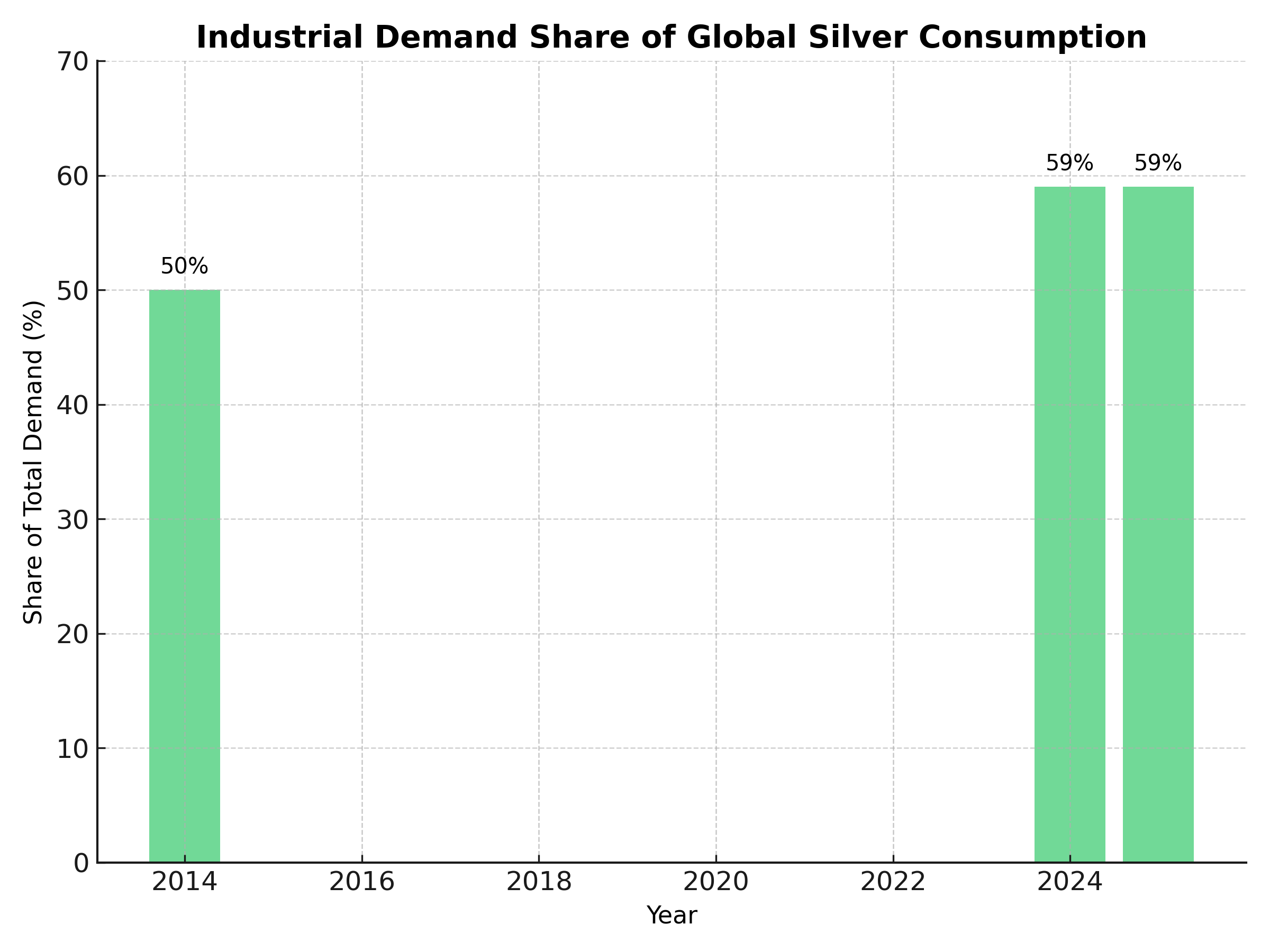

Silver faces historic supply deficit as solar/EV demand surges. Deutsche Bank targets $45/oz by 2026. Industrial consumption now 59% of total vs 50% decade ago.

- Silver is experiencing a historic supply-demand imbalance driven by industrial consumption growth and constrained production, positioning the metal for sustained outperformance with Deutsche Bank forecasting $45/oz by 2026.

- The silver market has recorded its fourth consecutive year of supply deficit, with industrial demand now representing 59% of total consumption—up from 50% just a decade ago, creating unprecedented market tightness.

- Industrial consumption surged 7% to 700 million ounces, also driven by strong demand from electric vehicle (EV) powertrain and charging infrastructure, fundamentally altering silver's demand profile.

- 72% of silver comes as a byproduct of other metals, supply cannot easily respond to this demand surge, constraining production despite elevated prices.

- In the first half of 2025, global silver-backed ETPs experienced significant net inflows, reaching 95 million ounces, marking renewed institutional interest.

- Deutsche Bank raised its silver forecast for 2026 to $45/ounce from $40/ounce, driven by expectations of weaker U.S. dollar and resumed Federal Reserve rate-easing cycle.

Introduction: Silver's Dual Identity Creates Unique Investment Opportunity

Silver's renaissance in 2025 stems from its unique position as both a precious metal and critical industrial commodity. Unlike gold, which remains primarily an investment asset, silver has become indispensable to the technologies powering the 21st century economy. This convergence of monetary asset properties with essential industrial applications creates fundamentally different market dynamics.

Silver bullion broke through the significant $35 per ounce resistance level early last month, reaching its highest price in a decade. However, unlike previous precious metals rallies driven primarily by monetary policy, today's silver bull market is underpinned by structural demand growth that appears sustainable regardless of macroeconomic conditions.

Global Industrial Demand & Solar Energy: The Foundation of Silver's Bull Case

The solar photovoltaic sector has emerged as silver's most dynamic demand driver, fundamentally altering the metal's consumption profile. Global silver demand reached 1.2 billion ounces in 2024, driven by the photovoltaic (PV) solar market which uses silver to make equipment such as solar panels.

In 2025, silver demand from the solar sector is projected to account for 14% of global demand, up from 5% in 2014. The technology shift toward more efficient solar cells continues to drive consumption despite efforts to reduce silver content per panel. The Silver Institute expects a 20% increase in the solar PV market this year alone.

Research suggests future constraints may be severe. The PV industry may require up to 14,000 tonnes of silver per year in 2030, with global supply being only 34,000 tonnes, indicating potential supply tightness ahead.

Electronics and Electric Vehicles: Sustained Demand Growth

Beyond solar applications, silver's unmatched electrical conductivity ensures its irreplaceable role in expanding technology sectors. The electronics and electrical sector represents silver's largest industrial application, consuming 445.1 million ounces in 2023—a remarkable 20% year-over-year increase.

Hybrid and EV production is expected to triple silver use in the auto sector by 2040, according to the Silver Institute. With global EV adoption accelerating and infrastructure deployment continuing, these applications create demand that grows with technological advancement.

Supply Challenges: Byproduct Dependency Constrains Production Response to Demand

The fundamental challenge facing silver markets is the metal's dependence on base metal production. 72% of silver comes as a byproduct of other metals, supply cannot easily respond to this demand surge, limiting producers' ability to respond to price signals.

Despite silver prices hovering near decade highs of approximately $38 United States Dollars per troy ounce, new primary silver production is lagging due to permitting delays, capital intensity, and declining ore grades. Even if silver prices rise sharply, major copper mining companies are unlikely to adjust their production plans, meaning a supply shortage could become a long-term structural issue.

Mine Supply Declining Despite Strong Prices

Contrary to typical commodity dynamics, silver mine supply has declined by 7% since 2016 despite stronger prices. This reflects the reality that new silver mining projects require substantial lead times, making supply response highly inelastic.

Mexico, the world's largest producer at 24.5% of global supply, faces regulatory uncertainties while Peru confronts operational disruptions. These geopolitical factors compound the structural supply challenges.

Vizsla Silver: Development-Stage Pure Play

Vizsla Silver represents leveraged exposure to rising silver prices through its Panuco District project in Mexico. The company targets becoming "the world's largest single-asset primary silver producer" with first silver production scheduled for H2 2027.

The project's economics demonstrate silver's profit leverage potential. Based on $26/oz silver, the 2024 PEA shows average life-of-mine production of 15.2 Moz silver-equivalent annually with all-in sustaining costs of $9.40/oz. This creates substantial operating leverage to silver price appreciation, with post-tax NPV of $1.14 billion and 86% IRR.

According to Michael Konnert, President and CEO of Vizsla Silver:

"Securing this debt financing mandate brings us one step closer to de-risking Panuco into production. Their support reflects the exceptional quality of Panuco and our team's ability to deliver. Together with the Company's current cash position, this debt facility is expected to fully fund the Panuco Project through to first silver production, and we remain firmly on schedule with this and other key de-risking milestones, positioning us to transition seamlessly into construction."

Vizsla has secured substantial funding capacity, including a $220 million debt facility with Macquarie, providing the financial foundation for development. With less than 30% of known vein targets drilled, the project offers exploration upside beyond the current 223 Moz measured and indicated resource.

Americas Gold & Silver: Production Leverage

Americas Gold & Silver exemplifies how established producers are adapting to this environment. The company's Cosalá Operations are optimized to deliver approximately 2.5 million ounces annually by 2026, supported by all-in sustaining costs of $10.80 per ounce and revenue alignment toward 80% silver exposure by 2025.

The company's transformation centers on revitalizing the Galena Complex in Idaho's historic Silver Valley, with management projecting restoration to over 5 million ounces of silver annually. Recent exploration has delivered exceptional intercepts, including 0.21 meters grading 24,913 g/t silver in the 149 Vein.

Paul Huet, Chairman & CEO of Americas Gold & Silver emphasized that:

"We're already mining one of the highest grades in the world. You look at who on the planet right now is mining silver at 400 gram. You'll find the list is less than five people. There are not many silver operators out there mining over 400 gram. We're over 400 gram."

This revenue profile makes the company uniquely sensitive to price upside driven by industrial demand acceleration.

Cerro de Pasco Resources: Unique Asset Profile

Cerro de Pasco Resources offers exposure to what management describes as "the world's largest above-ground metal resource" through tailings reprocessing in Peru. The Quiulacocha Tailings project contains an estimated 423 million ounces of silver equivalent across 75 million tonnes of material.

The business model provides advantages over traditional mining: extraction costs of only $1-2 per tonne, no drilling or blasting requirements reducing operating expenses by approximately 40%, and environmental benefits through acid water remediation.

"The silver market faces a persistent supply deficit, with demand exceeding supply for three consecutive years. In 2023, the deficit reached 184.3 Moz, one of the largest on record, and is expected to grow by 17% in 2024, driven by rising industrial consumption."

Internal projections suggest substantial value creation potential from reprocessing historic tailings rather than developing new mines, while also providing exposure to strategic metals including gallium and indium.

GR Silver Mining: Discovery-Stage Growth

GR Silver Mining represents a discovery-focused play concentrated in Mexico's Plomosas District, targeting resource expansion through aggressive drilling campaigns. The company operates a dual-asset strategy combining the historic Plomosas Mine area with the San Marcial resource area, both located in Sinaloa, Mexico.

The San Marcial project anchors the company's growth strategy with a current NI 43-101 resource of 68 million ounces silver equivalent. Management emphasizes that approximately 80% of intrusive-related anomalies remain untested, providing substantial exploration upside potential. Recent drilling has delivered encouraging results, including 75 meters grading 293 g/t silver equivalent and zones exceeding 1,000 g/t silver.

Marcio Fonseca, CEO of GR Silver explained:

"This hole brought up fresh information about the epithermal system, boiling textures that carry a lot of silver, kilos of silver. We discovered this situation through integrating geochemical data, geophysics, and structural geology, and it shows that only 20% of the anomaly's edge has been tested."

The company maintains a strong capital position with C$13 million cash as of September 2025, supplemented by C$13.8 million raised in bought deal financing in August 2025. This financial foundation supports the aggressive exploration program planned through 2026, including a 52-hole, 15,000-meter drill program that commenced in late 2025.

Investment Implications: Strategic Positioning Through ETF Products for Silver Outperformance

For investors seeking broad silver exposure, exchange-traded products offer liquid alternatives to physical ownership. With $40 billion in exchange-traded product assets under management and over 95 million ounces of inflows in 2025, institutional sentiment toward silver is accelerating at unprecedented levels.

The iShares Silver Trust provides investors with access to the silver price performance, using the London Bullion Market Association silver price as its benchmark, representing the largest physically-backed silver ETF. For leveraged exposure to silver mining companies, the Global X Silver Miners ETF offers access to diversified silver-focused producers.

Newer products like the Sprott Silver Miners & Physical Silver ETF combine physical silver holdings with mining equity exposure, providing a hybrid approach that captures both metal appreciation and potential operational leverage.

Market Structure Supports Sustained Outperformance

.png)

Market participants are beginning to recognize that silver's industrial demand is less price-sensitive than traditional commodity applications. Solar manufacturers and electric vehicle producers prioritize supply security and performance over marginal cost differences.

This dynamic distinguishes silver from other industrial metals where demand destruction typically occurs at elevated price levels. The essential nature of silver in technological applications creates more stable consumption patterns even during price volatility.

The University of New South Wales warns that solar industry growth could exhaust 85-98% of global silver reserves by 2050, creating long-term supply constraints.

The Investment Thesis for Silver

- Capitalize on Structural Deficits: Position in physical silver or silver ETFs to benefit from consecutive years of supply deficits, with continued shortfalls projected.

- Target High-Beta Silver Miners: Consider development-stage companies like Vizsla Silver if silver prices sustain above current levels, as operating leverage amplifies returns during bull markets.

- Focus on Jurisdictional Safety: Prioritize assets in stable mining jurisdictions given geopolitical risks in major silver-producing regions.

- Consider Hybrid Strategies: Allocate to ETFs combining physical silver with mining equity exposure to capture both metal appreciation and operational leverage without single-company risk.

- Monitor Industrial Demand Growth: Track solar installation data and EV adoption rates as leading indicators of sustained silver consumption growth beyond traditional investment demand.

- Prepare for Volatility: Maintain position sizing that accounts for silver's historical price volatility while recognizing current market structure differs from previous cycles.

Key Takeaways & Investor Implications

The silver market in 2025 represents a compelling investment opportunity driven by fundamental supply-demand imbalances rather than speculative positioning. Unlike previous precious metals rallies that relied primarily on monetary policy drivers, today's silver bull market is underpinned by structural industrial demand growth that appears sustainable across economic cycles.

With supply deficits deepening and demand intensifying across both industrial and investment channels, silver's bull market appears well supported. The combination of essential industrial applications, constrained supply response, and renewed investment interest creates conditions for sustained outperformance.

Investors should consider silver's unique position as both a monetary asset and critical commodity when constructing portfolios. The metal's industrial applications provide fundamental demand support while its precious metal characteristics offer portfolio diversification benefits. Given Deutsche Bank's upgraded price target of $45/oz by 2026 and the structural factors supporting continued demand growth, silver may offer attractive risk-adjusted returns.

The convergence of green energy transition, technology adoption, and supply constraints positions silver as potentially one of the best-performing asset classes in the current cycle. However, investors must prepare for volatility while recognizing that current market fundamentals differ significantly from historical precious metals cycles, potentially providing more sustained price support.

TL;DR

Silver is experiencing unprecedented supply-demand imbalances as industrial consumption, led by solar panel manufacturing, drives demand to record levels while mine production remains constrained. The metal has broken above key resistance levels for the first time since 2011. Deutsche Bank upgraded its 2026 price target to $45/oz, citing macro factors including weaker dollar expectations and Fed policy. Key investment opportunities include physical silver ETFs, silver mining companies with low-cost production profiles, and hybrid products combining physical silver with mining equity exposure. The structural shift toward industrial applications distinguishes this bull market from previous precious metals rallies driven primarily by monetary policy.

FAQs (AI Generated)

Silver's outperformance stems from its dual nature as both a precious metal and critical industrial commodity. While gold relies primarily on investment demand, silver benefits from surging industrial consumption, particularly from solar panel manufacturing and electric vehicle production. This industrial demand provides fundamental support beyond traditional monetary factors.

Investors can choose from several approaches: physical silver ETFs like iShares Silver Trust (SLV) for direct price exposure, silver mining ETFs like Global X Silver Miners (SIL) for operational leverage, or hybrid products like Sprott's offerings combining physical silver with mining stocks. Individual company exposure through firms like Vizsla Silver or Americas Gold & Silver offers higher potential returns but increased risk.

Deutsche Bank's upgrade to $45/oz for 2026 is based on fundamental factors including weaker dollar expectations, Fed rate cuts, and sustained industrial demand. While price targets are inherently speculative, the structural supply deficit and industrial demand growth provide stronger fundamental support than previous silver rallies that relied mainly on investment demand.

Key risks include silver's historical price volatility, potential supply response if prices rise significantly, regulatory uncertainties in major producing countries, and the possibility that strong equity market performance could reduce safe-haven demand. Additionally, most silver comes as a byproduct, making supply response unpredictable.

Unlike previous precious metals rallies driven primarily by monetary policy, today's silver market is supported by structural industrial demand that appears less price-sensitive. Solar manufacturers and EV producers prioritize supply security over cost, creating more stable demand patterns. However, sustainability depends on continued green energy adoption and industrial growth maintaining momentum.

Analyst's Notes

Subscribe to Our Channel

Stay Informed