US-China Supply Dependencies Reduce Tail Risk and Re-rate Non-Chinese Rare-Earth Midstream

US-China supply dependencies reduce geopolitical tail-risk while administrative tightening creates sustained premiums for non-Chinese rare earth midstream.

- Supply dependencies between semiconductors and rare earths moderate extreme policy risks while China's administrative tightening through monthly reporting and imported feedstock quotas creates sustained ex-China pricing premiums and structural scarcity.

- Reduced tail-risk supports lower discount rates for non-Chinese midstream assets while persistent scarcity premiums favor funded separation/recycling platforms over traditional mining projects with extended development timelines.

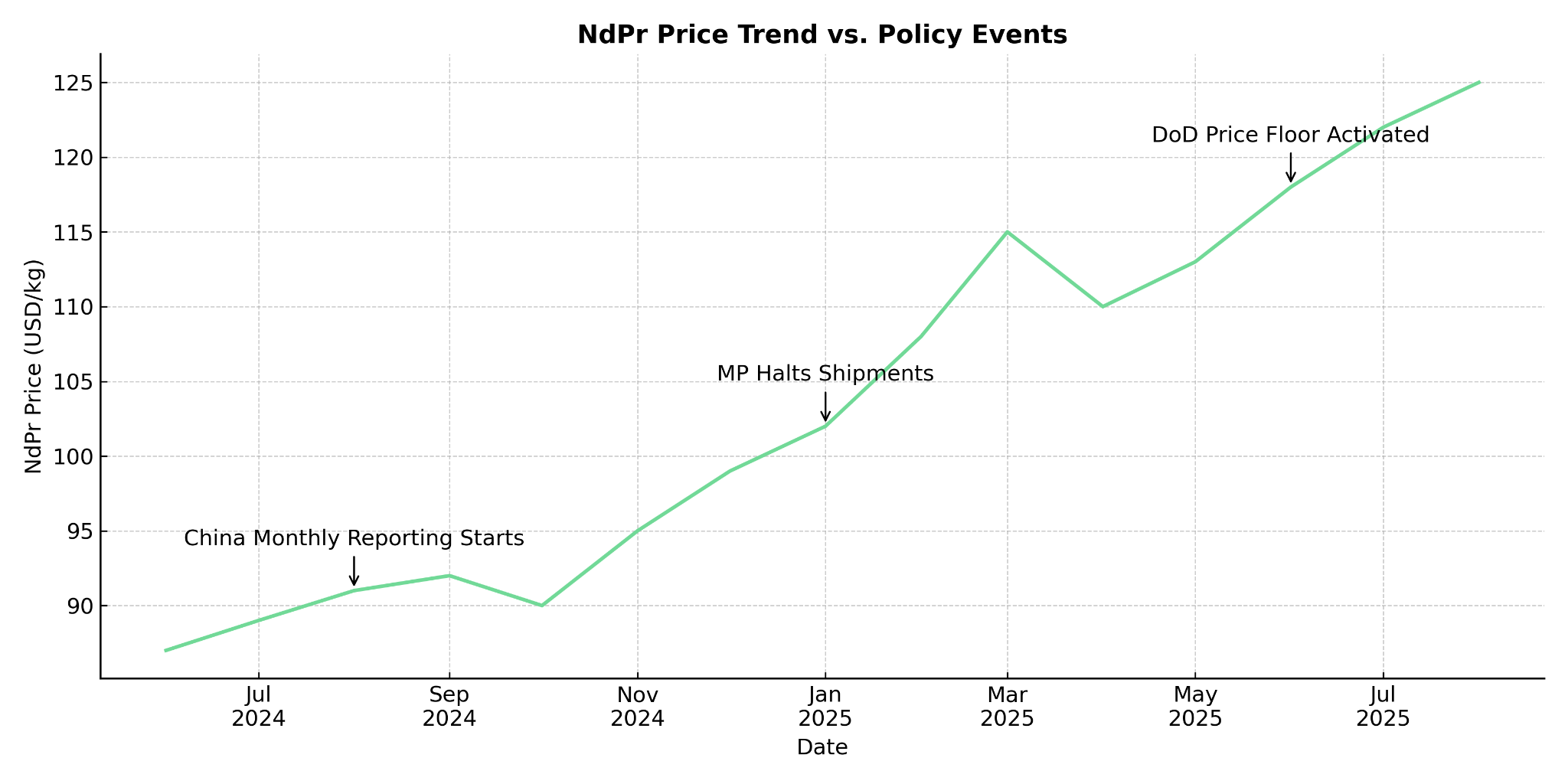

- NdPr reached two-year highs in late August as the US DoD's $110/kg price floor provides a new valuation baseline for qualifying projects and improves project finance terms through downside protection mechanisms.

- Pensana's funded Longonjo MREC pathway, Ionic Rare Earths' 99.9%+ recycled oxides, Ucore's RapidSX™ Louisiana facility, and Namibia Critical Metals' JOGMEC-backed xenotime HREE deposit exemplify strategic positioning within this environment.

- Prefer midstream integration, policy alignment, HREE exposure, and execution visibility while using milestone-based allocations tied to construction progress, grant awards, and commissioning schedules.

Supply Dependencies Create Moderated Risk Environment

The US-China rare earth relationship reflects broader supply chain interdependencies that constrain extreme policy measures. Washington requires reliable access to separated rare earth oxides for defense and energy transition applications, while Beijing depends on advanced semiconductor technology and manufacturing equipment controlled by US allies. These mutual dependencies create natural limits on escalation while allowing for administrative tightening that supports domestic industries.

China's approach has evolved toward administrative enforcement rather than dramatic export bans. Monthly reporting requirements implemented in August extend oversight to imported feedstock, creating compliance-driven supply constraints that support domestic Chinese producers while maintaining plausible engagement with international markets. This framework enables sustained ex-China pricing premiums without triggering wholesale supply chain abandonment.

Recent NdPr price action demonstrates how quickly administrative measures can tighten balances. Prices reached two-year highs following MP Materials' suspension of China-bound shipments, highlighting how projects positioned for non-Chinese separation can capture persistent pricing arbitrage. Pensana Plc’s Longonjo development in Angola exemplifies this approach, with Chairman Paul Atherley emphasizing the company’s strategic positioning:

"We are now in discussions with parties who have got separation capacity ex-China and that would be a very very important step if we were able to do that to create the non-Chinese supply chain"

Re-rating Implications for Ex-China Assets

Supply dependency dynamics reduce binary geopolitical risk while preserving structural scarcity premiums for non-Chinese origin materials. This environment supports lower discount rates for ex-China midstream projects while maintaining positive price spreads that justify higher capital costs outside China.

Administrative Tightening Supports Sustained Premiums

China's August measures demonstrate how administrative controls can achieve supply management objectives without policy announcements. Extended quotas covering imported feedstock and mandatory monthly traceability reporting create systematic constraints on export flows. The new framework requires companies to upload production and distribution data by the 10th of each month, enabling real-time supply chain monitoring.

These measures favor domestic Chinese operations through policy-stabilized input costs while systematically constraining ex-China availability. Import-dependent processors face increased compliance costs and potential feedstock restrictions, creating structural advantages for integrated non-Chinese operations. Projects with demonstrated product quality and supply chain transparency benefit from buyers' willingness to pay premiums for assured access.

HREE Scarcity Amplifies Valuation Impact

Heavy rare earth supply constraints create particularly acute premiums given Myanmar's conflict-related disruptions and limited alternative sources. This scarcity supports projects with xenotime mineralogy in stable jurisdictions. Namibia Critical Metals' Lofdal deposit represents this positioning, with the development team highlighting the strategic value of non-conflict HREE sources. s. The project targets a significant heavy rare earth deposit, as Darren Campbell, President of Namibia Critical Metals, highlights:

“We are developing the Lofdal heavy rare earth project in Namibia, one of the largest deposits of dysprosium and terbium outside of China. We are partnered with JOGMEC, the Japanese government agency, and are moving towards delivering a pre-feasibility study by the end of this year.”

Recycling pathways offer alternative access to separated heavy rare earths without mining lead times or geopolitical exposure. Managing Director Tim Harrison of Ionic Rare Earths notes increasing demand for recycled HREE oxides:

"If you want to make a magnet to go into high-end applications whether that be electric vehicles, wind turbines or military defense you also need the despros and that's why we've had a lot of inbound inquiry on the materials that we're making."

Price Discovery and Policy Support Create New Valuation Framework

Two parallel developments are establishing higher valuation baselines for non-Chinese rare earth assets. Market-driven price discovery has pushed NdPr to two-year highs, demonstrating supply-demand imbalances that persist beyond short-term disruptions. Policy support through the US DoD's $110/kg NdPr price floor creates downside protection that improves project economics and financing terms.

The DoD price guarantee operates as a contract-for-difference mechanism that reduces cash flow volatility for qualifying projects. This structure particularly benefits US-based separation facilities where operational costs can be benchmarked against assured revenue streams. Ucore Rare Metals’ Louisiana Strategic Metals Complex benefits from this framework, with Chief Executive Officer Pat Ryan emphasizing the competitive timeline:

"By mid-26 we're looking to have that stage one of the Louisiana plant commissioned and start to deliver product to the western world"

The company's RapidSX™ technology offers capital and operational advantages aligned with policy support trends. The closed-system design requires approximately one-third the space of conventional solvent extraction while addressing environmental considerations increasingly factored into project finance decisions.

Midstream Focus Captures Value Creation

Rare earth value concentration has shifted decisively toward separation and oxide production rather than mining operations. Technology choices between conventional solvent extraction and next-generation separation methods determine capital intensity, processing flexibility, and product quality specifications. Recycling operations offer immediate access to separated oxides while avoiding mining permitting and development risks.

Successful companies emphasize pathways to separated oxides rather than resource tonnage. Pensana's strategic approach centers on producing mixed rare earth carbonate (MREC) that enables non-Chinese separation processing. Chairman Paul Atherley explains the commercial logic:

"We've actually designed the project to go all the way down to produce a mixed rare earth carbonate which is a midstream product which can then be sent to doesn't necessarily have to go to China can go somewhere else to be turned into an oxide and ultimately a metal"

Recycling technologies provide direct access to high-purity oxides without mining development timelines. onic Rare Earths, through its Ionic Technologies subsidiary, highlights that its patented technology, developed at Queens University Belfast (QUB), offers first mover capability for individual magnet rare earth recycling, separating 99.9% plus magnet rare earth oxides (REO) to enable the energy transition, electric vehicles, advanced manufacturing, and defence.

Investment allocation should prioritize midstream platforms with feedstock flexibility, established processing technology, and policy alignment through grants, tax advantages, or offtake agreements.

Valuation Methodology Adjustments

Supply dependency dynamics require adjusted analytical frameworks that account for reduced tail-risk alongside sustained operational premiums. Lower probability of extreme policy disruption supports reduced equity risk premiums for qualified ex-China projects, particularly where government backing provides additional downside protection.

Project finance assumptions can incorporate more stable base-case scenarios given policy floor mechanisms like the DoD's NdPr price guarantee. Sensitivity analysis should emphasize basket pricing, impurity penalties, and currency exposure while de-emphasizing binary geopolitical scenarios.

Re-rating opportunities focus on separation/recycling platforms with measurable commissioning progress relative to resource-stage projects with extended development timelines. The defense procurement model established through the MP Materials partnership, which includes a $400 million equity investment and a $110/kg NdPr price floor from the US DoD. Chief Executive Officer Pat Ryan of Ucore emphasizes this industry evolution:

"The need to have that rare earth permanent magnet so they can keep their supply chain running at a defined price is much more advantageous than being puppeteered by China as I mentioned"

Portfolio Allocation Framework

Core portfolio exposure (1–2%) should target midstream separation/recycling operations with funded construction, policy support, and 2025–27 production timelines. Satellite positions can access HREE-focused projects with strategic partnerships and clear feasibility study schedules.

Position sizing should correlate with milestone achievement including grant awards, construction commencement, first feedstock processing, and initial on-spec oxide deliveries. Monitor China vs. ex-China price spreads as indicators of administrative policy effectiveness and supply chain stress levels.

Geographic diversification merits increased attention given sustained policy support across multiple jurisdictions. Ionic Rare Earths demonstrates this approach through operations spanning the UK, Brazil, and Uganda, accessing different grant regimes while maintaining operational flexibility across regulatory environments.

Quarterly Monitoring Protocol

Track administrative policy implementation including Chinese license issuance cadence, monthly reporting compliance, and any preferential treatment mechanisms for selected counterparties. Monitor EU CRMA funding announcements and project qualification status updates.

Price monitoring should focus on China vs. ex-China differentials for NdPr and Dy/Tb, MREC-to-oxide conversion rates, and oxide purity specifications from active operations. Industrial metals pricing services increasingly report separate indices for Chinese vs. Western-origin materials.

Operational progress indicators include construction advancement at funded projects (Pensana's Longonjo), grant decisions and initial recycled oxide shipments (Ionic's Belfast facility), facility commissioning progress (Ucore's Louisiana plant), and pre-feasibility study completion (Namibia Critical Metals' Lofdal). ESG risk factors include Myanmar supply disruptions and supply chain traceability audit results.

Risk Assessment and Mitigation

Policy normalization represents the primary risk where improved US-China relations could compress ex-China premiums. Mitigate through diversified exposure across multiple jurisdictions and processing technologies, with offtake contracts indexed to regional price differentials.

Operational execution risk affects projects transitioning from feasibility to production, particularly regarding impurity control, reagent supply chains, and customer specification compliance. Require demonstrated pilot-scale processing and customer qualification before significant position sizing.

Heavy rare earth supply volatility continues given Myanmar's political instability and limited alternative sources. Prefer xenotime-hosted projects or recycling technologies with documented material provenance over ion-adsorption clay deposits in unstable regions.

European regulatory implementation poses execution risk given ambitious CRMA targets and potential conflicts with existing chemical regulations. Balance EU exposure with US and Japanese partnership opportunities where regulatory frameworks offer greater certainty.

The Investment Thesis for Rare Earths

- Supply dependency moderation reduces extreme tail-risk while preserving structural scarcity premiums that support ex-China project economics.

- Administrative enforcement creates sustained pricing support for non-Chinese separation capacity without dramatic policy announcements that could trigger retaliation.

- Policy floors and offtakes (exemplified by $110/kg NdPr pricing) provide downside protection that improves project financing and reduces equity risk premiums.

- Midstream value concentration favors separation/recycling platforms with established technology and near-term production over traditional mining projects with extended development timelines.

- HREE strategic importance warrants dedicated exposure given defense applications, limited supply sources, and recycling technology development.

- Jurisdictional diversification combined with supply chain traceability commands pricing premiums while reducing regulatory and geopolitical concentration risk.

- Government partnership models demonstrate how policy support can accelerate commercial viability and provide revenue certainty for qualifying projects.

- Execution visibility enables milestone-based allocation as projects advance from feasibility through construction to commercial operation.

Structural Premiums in a Moderated Risk Environment

US-China supply dependencies have created a more stable geopolitical framework while preserving economic incentives for supply chain diversification. Administrative tightening maintains structural scarcity without triggering wholesale supply disruption, supporting sustained ex-China pricing premiums. Policy mechanisms including the US DoD's NdPr price floor provide downside protection that improves project economics and financing terms.

Investment opportunities center on owning separated oxide production capacity through funded separation facilities, proven recycling technologies, and HREE-rich projects with strategic partnerships. Portfolio construction should emphasize milestone-driven allocation with disciplined monitoring of administrative policy implementation and market price differentials.

The resulting investment environment favors execution-focused companies over those dependent on geopolitical volatility for valuation support. Supply dependency dynamics have reduced extreme risks while preserving the structural imbalances that justify higher valuations for non-Chinese rare earth assets.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed