US Crude Draws & Middle East Risks Keep Oil Above $85, Pressuring Mining Margins

Eight US crude draws and Middle East supply risks keep oil above $85, increasing fuel costs and margin pressure for unhedged mining companies.

- US crude inventories fell 9.12 million barrels in the week ended June 5, marking an eighth consecutive weekly draw, while gasoline stocks fell 1.19 million barrels. Lower inventories reduce the market's ability to absorb new supply disruptions, supporting oil prices at current levels.

- Brent held at $91.36 per barrel and WTI at $88.10 per barrel on June 10 after US forces struck Iranian targets following the downing of a US Apache attack helicopter. ING commodity strategists target higher oil prices in Q3 if Middle East supply disruptions continue during the seasonally stronger demand period.

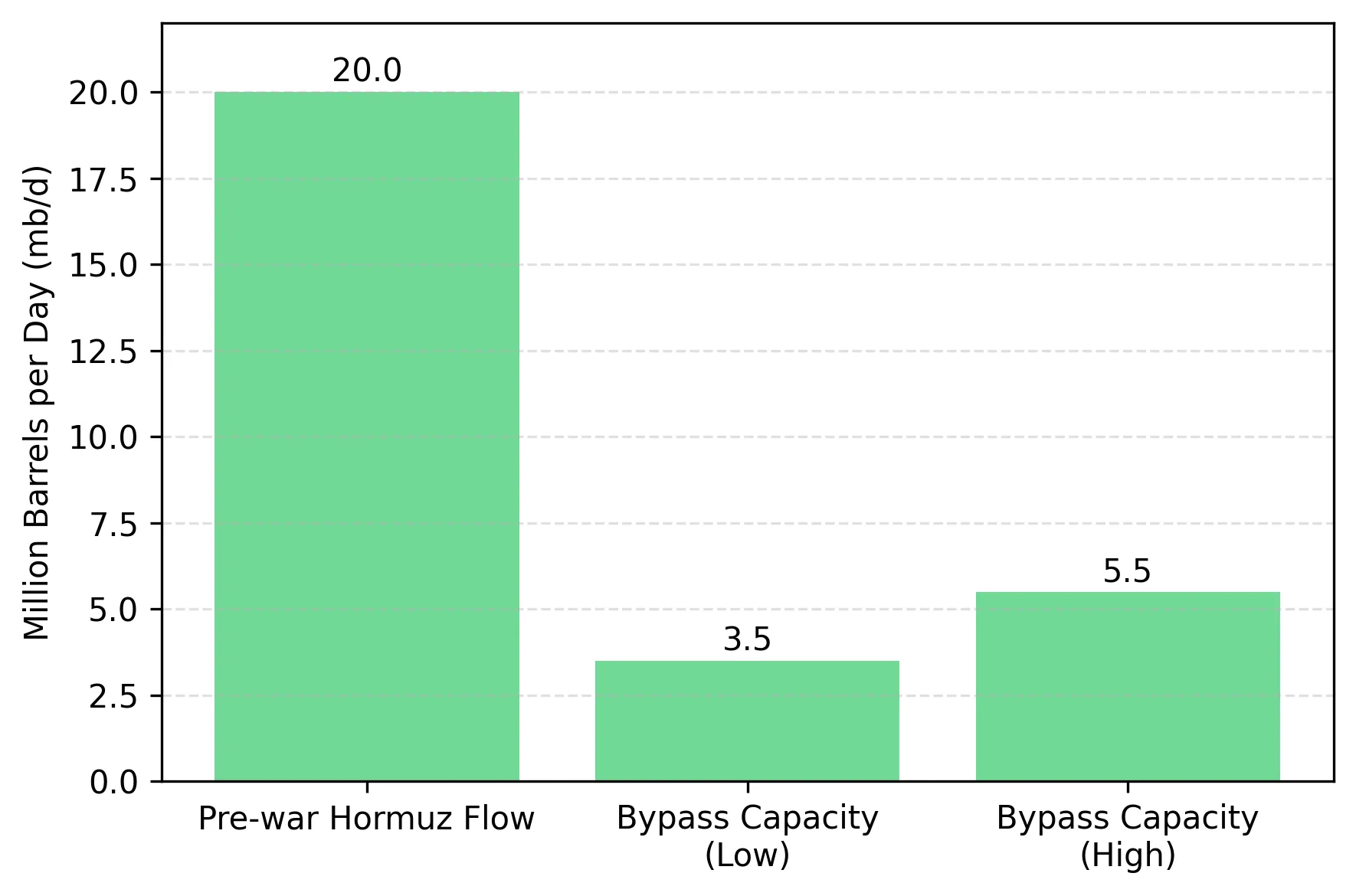

- Tehran continues blocking most Hormuz shipping and has threatened to resume full hostilities if Israel attacks Hezbollah; bypass capacity through Saudi Arabia's East-West pipeline and the UAE's Fujairah terminal remains capped at 3.5-5.5 mb/d versus 20 mb/d of pre-war Hormuz flow, leaving a supply gap with no identified solution before 2027.

- Japan's wholesale price index hit a three-year high of 6.3% in May as higher energy prices flowed through to businesses; the same cost pressure applies to mining operations that buy dollar-priced diesel from global markets and lack a local fuel alternative.

- US May CPI data releases June 11 at 8:30 AM ET; a print above consensus could support further Fed rate hikes, keep the dollar strong with DXY at 99.95, and reduce the exchange-rate benefit that helps offset higher energy costs for non-US mining operators reporting in local currencies.

US-Iran Escalation & Shrinking US Inventories Increase Oil Supply Risk

Brent fell 9 cents to $91.36/barrel and WTI fell 10 cents to $88.10/barrel after US forces struck Iranian targets following the downing of a US Apache attack helicopter, an incident President Trump had vowed to answer. The market response suggests investors are treating the conflict as an ongoing supply risk rather than a series of isolated events, helping keep oil prices near current levels.

US crude stocks fell 9.12 million barrels in the week ended June 5, the eighth consecutive weekly draw, while gasoline inventories declined a further 1.19 million barrels. The US has supplied additional crude and fuel to Asia and Europe throughout the Iran war; after eight consecutive inventory draws, the market has less capacity to absorb another supply disruption without higher oil prices.

Eight Consecutive Crude Draws Leave Oil Markets More Exposed to Supply Shocks

Eight consecutive inventory draws increase the likelihood that new supply disruptions will have a larger impact on oil prices. When inventories were higher, oil prices could absorb geopolitical shocks more easily as tensions eased. The 9.12 million barrel draw ending June 5 leaves the market with less inventory to offset another supply disruption at current prices. LSEG oil analyst Emril Jamil said ongoing geopolitical tensions and declining inventories continue to support oil prices.

Current ceasefire efforts remain stalled ahead of Q3 because Iran has tied any extension to conditions Israel has refused to accept. Tehran has threatened to resume full hostilities if Israel attacks Hezbollah, a condition Israel has refused to accept and one that has stalled ceasefire negotiations. Even if Hormuz traffic increases, bypass capacity through Saudi Arabia's East-West pipeline and the UAE's Fujairah terminal remains capped at 3.5-5.5 mb/d versus 20 mb/d of pre-war Hormuz flow, leaving a 14.5 mb/d supply gap. The UAE's West-East pipeline, the only planned infrastructure that could increase bypass capacity, is not scheduled to come online until 2027.

Middle East Supply Risks Keep Brent Near $90 While Escalation Threatens $100 Oil

ING commodity strategists said ongoing Middle East supply disruptions support higher oil prices if they continue into the third quarter, when seasonal oil demand is typically stronger. Commonwealth Bank of Australia economist Harry Ottley assessed the conflict as moving toward de-escalation, but that view came before additional US airstrikes and Iran's retaliatory strikes on a US base in Jordan and 21 Gulf targets.

US-Iran military exchanges remain limited, Hormuz traffic improves, and Brent remains in an $88-$95/barrel range through Q3 2026, keeping energy costs above levels assumed in many mining companies' Q3 budgets. If Iran targets Saudi or UAE pipeline infrastructure, including assets previously struck in April, reduced export capacity could push Brent above $100/barrel within 10 trading days and increase diesel costs by 10-14% for unhedged mining operations relative to current cost guidance.

A ninth consecutive inventory draw above 7 million barrels in the EIA Weekly Petroleum Status Report would indicate inventories continue to tighten and support current oil prices through Q3.

Higher Oil Prices & Unhedged Fuel Exposure Pressure Mining Margins

Open-pit gold and copper producers that rely heavily on diesel face margin pressure when WTI remains above $85/barrel. Diesel accounts for 15-25% of all-in sustaining costs at large open-pit operations, making it the highest variable cost after labour. Producers that set 2026 cost guidance before the Iran war face higher operating costs at current oil prices. Operations in West Africa and Southeast Asia face greater fuel-cost exposure because diesel is dollar-priced and often lacks local supply alternatives or state subsidies.

The key difference is whether a producer can hedge fuel costs or delay discretionary mine development activity. A producer with fuel hedges covering Q3 delivery at or below current Brent prices can lock in fuel costs even if oil rises above $100/barrel. A producer without hedges that cannot defer Q3 pre-stripping or major development drilling faces the full margin impact of higher fuel costs, because reducing activity could shorten mine life or breach production covenants under project finance agreements.

Available information does not yet indicate whether Brent remains in an $88-$95/barrel range or rises above $100/barrel. Investors should identify mining companies with unhedged fuel exposure and review management's Q3 hedge coverage disclosures before increasing positions in energy-intensive producers at current valuations.

US-Iran Ceasefire & Hormuz Reopening Could Reduce Oil Price Support

WTI at $88.10/barrel remains above the oil-price assumptions used in many mining companies' cost guidance before the Iran war, increasing fuel costs for operations that buy diesel against global crude benchmarks. Eight consecutive inventory draws support WTI above $85/barrel by reducing the crude available for export while meeting domestic demand.

A confirmed US-Iran ceasefire and the reopening of Hormuz to unrestricted commercial traffic would remove a key source of support for current oil prices, with the impact likely to emerge within two to three weeks. Without a ceasefire and a reopening of Hormuz, WTI is unlikely to fall below $85/barrel unless global oil demand weakens or additional export capacity becomes available before 2027.

The EIA Weekly Petroleum Status Report for the week ended June 5 will show whether recent inventory declines continued into a ninth consecutive week. A draw of 7 million barrels or more would indicate inventories continue to tighten, while builds of 3 million barrels or more for two consecutive weeks would suggest weaker demand and reduced support for current oil prices. US May CPI will also influence oil-market sentiment; an above-consensus core reading could support further Fed rate hikes, keep the dollar strong, and reduce the exchange-rate benefit that helps offset higher energy costs for non-US miners.

Analyst's Notes

Subscribe to Our Channel

Stay Informed