US Tariff Exemption Reshapes Copper Trade Flows & Triggers Sharp Market Repricing

US copper tariff exemption triggers 20% price drop, reshapes global trade flows. Strategic copper assets in Tier 1 jurisdictions gain investor focus.

- The August 1 US copper tariff exemption dismantled expected trade barriers, triggering a sharp price correction and volatility in global copper markets.

- The premium between COMEX and London Metal Exchange collapsed, erasing arbitrage-driven flows and recalibrating global copper trade routes.

- US domestic refining bottlenecks and import reliance highlight the strategic importance of accessible, low-emission copper assets in secure jurisdictions.

- Near-term risks include oversupply to US inventories, ongoing demand softness from China, and a potential future reintroduction of refined copper tariffs.

- Companies with scalable, low-cost oxide and sulphide deposits in politically stable regions - such as Chile, Spain, Canada - are well-positioned for rerouted capital and supply chain interest.

Trade Policy Reversal & the Shock to Copper Markets

On July 30, 2025, President Trump's administration unexpectedly clarified that refined copper imports would be exempt from the 50% tariff imposed on copper semis. While this averted immediate supply-side constraints, it triggered a violent market correction as arbitrage trades rapidly unwound. The exemption represents more than tactical policy adjustment - it signals a fundamental recalibration of US copper strategy amid growing supply security concerns.

COMEX copper surged to $5.80 per pound on July 23, driven by tariff expectations and speculative positioning. Prices then collapsed approximately 20% to $4.43 per pound post-exemption as of August 19. The COMEX-LME premium, which had expanded beyond 28% during peak speculation, rapidly compressed as arbitrage flows reversed direction.

Copper inventories surged across US warehouses as in-transit shipments originally destined for other markets flooded domestic facilities. This inventory build created additional downward pressure on prices while revealing the extent of speculative positioning that had accumulated ahead of the expected tariff implementation.

Supply Chain Reconfiguration & Strategic Uncertainty

The exemption shifted refined copper flows back toward LME-linked markets, replenishing global inventories and loosening regional spreads that had widened dramatically during the tariff speculation period. However, confusion around future policy direction creates structural uncertainty for global producers, particularly with potential phased tariffs in 2027-2028 remaining a possibility.

This policy whiplash mirrors the 2018 aluminum tariff experience, where initial market disruption gave way to gradual supply chain adaptation. However, the lack of meaningful downstream copper processing buildout in the US raises questions about the long-term efficacy of reshoring via trade barriers alone.

Copper Demand & Supply Realignment in a Two-Zone World

The refined copper exemption signals not merely a tactical trade adjustment, but a pivot toward regionalized supply chain blocs. The US appears to be forming a "Pan-American copper corridor" while China consolidates Asia-Pacific flows, fundamentally altering global trade patterns and investment priorities.

US copper demand could expand from current levels of 1.5-1.6 million tonnes annually to 2.3-2.5 million tonnes with domestic smelting capacity expansion—creating multi-year investment opportunities for feedstock suppliers. This demand growth represents one of the most significant structural shifts in global copper markets since China's industrialization phase.

Chile, Peru, and emerging Africa-Asia smelting hubs are re-orienting export strategies to capture these evolving trade flows. Copper producers in jurisdictionally secure, ESG-compliant regions stand to benefit from demand previously served by imports from politically sensitive sources.

Strategic Case Study: Marimaca Copper

Marimaca Copper's positioning exemplifies the advantages available to strategically located producers. The project, located in Chile, sits just 25 kilometers from Mejillones port, providing exceptional export optionality to copper-hungry trade partners including the US market.

Chief Executive Officer Hayden Locke of Marimaca Copper explains their processing advantage:

"The company's focus is on high acid soluble mineralization that delivers better recoveries than at Marimaca through our integrated processing approach"

The project's measured and indicated resource of approximately 900,000 tonnes copper, with definitive feasibility study completion due in 2025, positions it advantageously for long-term demand from US and European Union buyers prioritizing low-carbon intensity supply sources.

Near-Term Volatility & Tactical Positioning for Investors

The unwinding of speculative copper flows created an acute but likely temporary dislocation, now transitioning into a new risk-adjusted equilibrium. This period offers tactical positioning opportunities for investors willing to navigate increased volatility in exchange for exposure to structural themes.

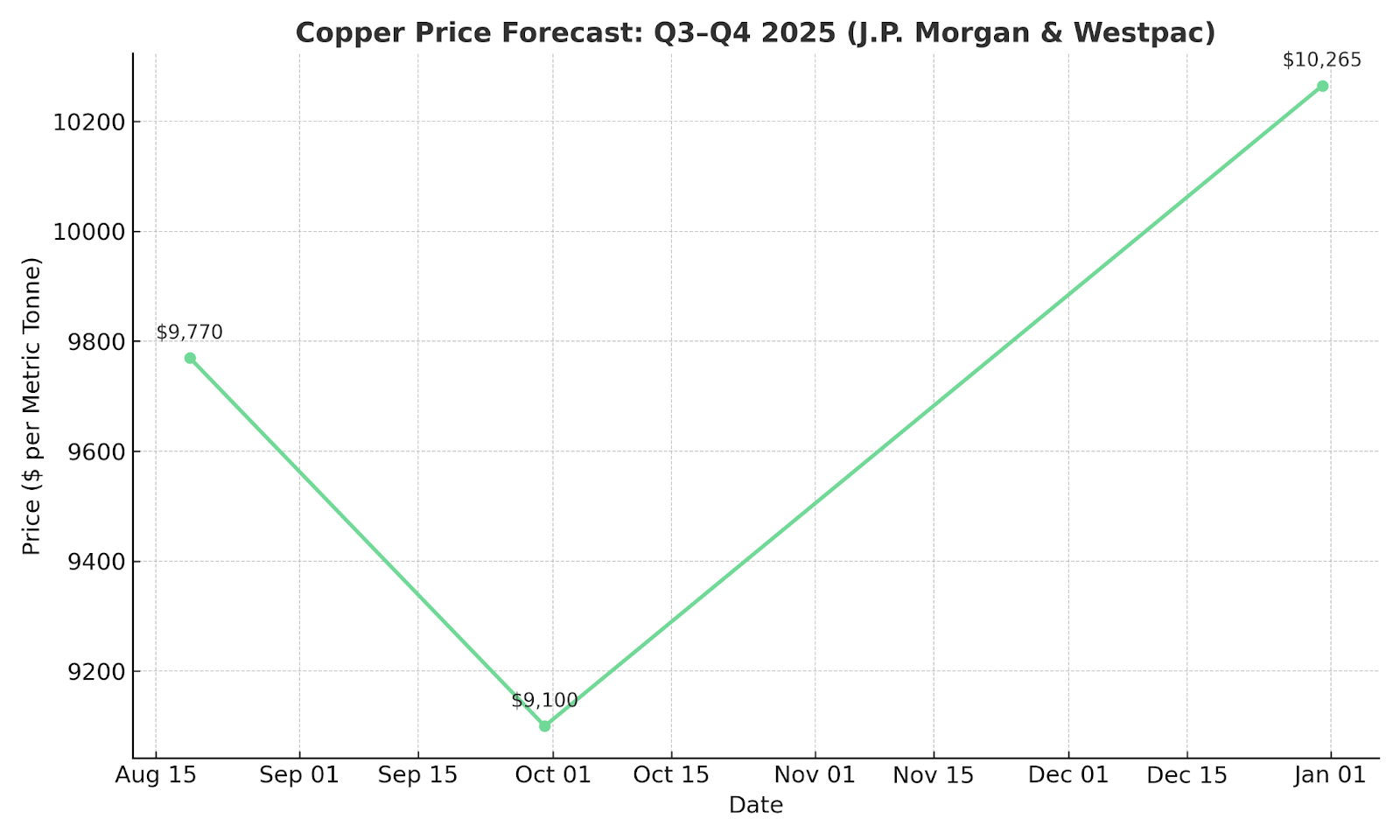

Record COMEX warehouse builds suggest potential near-term oversupply conditions, with possible re-exports to global markets as inventory levels normalize. J.P. Morgan and Westpac forecast near-term softness to approximately $9,100 per metric tonne in Q3 before recovery to $10,265 per metric tonne in Q4, reflecting this temporary supply-demand imbalance.

The gold-to-copper ratio divergence may indicate tactical trading opportunities, with potential mean reversion plays emerging for sophisticated commodity traders. This ratio historically reverts during periods of macro uncertainty, suggesting copper's relative undervaluation may prove temporary.

Strategic Case Study: Fitzroy Minerals

Fitzroy Minerals' oxide-dominant Buen Retiro IOCG system offers low-capital expenditure optionality as US manufacturers prioritize feedstock diversity. The project's recent drilling results, including spectacular intersections exceeding 800 meters of continuous mineralized trend, demonstrate the scale potential available in established mining jurisdictions.

Over 12,000 meters of drilling planned for 2025, combined with potential asset acquisition from Pucobre, creates a partially de-risked exploration model with multiple value catalysts.

Chief Operating Officer Gilberto Schubert of Fitzroy Minerals describes their approach:

"Fitzroy Minerals is focused on scalable oxide resources that fit emerging green and reshored supply trends."

The company's dual-jurisdiction exposure provides geographical diversification while maintaining operational focus in regions with established mining infrastructure and regulatory frameworks.

Project Readiness in a Global Copper CapEx Gap

The global copper development pipeline faces a severe capital expenditure gap, with insufficient new supply entering feasibility or pre-construction phases. Projects combining existing infrastructure, jurisdictional clarity, and resource scale increasingly represent strategic assets in a supply-constrained environment.

Structural Case Study: Gladiator Metals

Locatedin the Yukon, Canada, the Whitehorse Copper Belt's high-grade skarn mineralization aligns with structural demand for clean, high-grade, near-infrastructure deposits. This 35-kilometer copper belt offers exceptional infrastructure advantages, with highway access and proximity to Whitehorse city providing year-round operational capability and cost efficiencies.

Resource targets exceed 100 million tonnes at grades above 1% copper, with current drilling focused on Cowley Park, Little Chief, and Middle Chief prospects. The project's historical production record, including Hudson Bay Mining's extraction of 10-12 million tonnes at 1.5% copper and nearly one gram per tonne gold, provides geological confidence for resource expansion.

Chief Executive Officer & Director of Gladiator Metals Jason Bontempo highlights their operational advantages:

"Gladiator Metals' location and existing access enable a low-emission development strategy, without fly-in/fly-out complexity."

Long-Term Advantage: Jurisdiction & ESG Filters

Tier 1 jurisdictions increasingly attract capital due to escalating permitting risks in alternative locations, including recent challenges in Panama and ongoing instability in Democratic Republic of Congo. ESG-conscious investors favor producers utilizing renewable energy, seawater processing, and low-carbon methodologies—benefiting companies like Marimaca and Gladiator that prioritize sustainable development approaches.

Exploration Pipelines & Capital Reallocation

Copper junior companies with early-stage discoveries and visible catalysts are emerging as critical vehicles for capital rotation amid policy-induced macro disruption. These companies offer leveraged exposure to copper price recovery while maintaining optionality for resource expansion and strategic acquisition.

Catalysts & Capital Flow: Pan Global Resources

Pan Global Resources' positioning within Spain's Iberian Pyrite Belt enables multi-deposit exploration scale, aligning with historical regional mine models that have produced some of Europe's most significant base metal deposits. The company's Escacena and Cármenes projects both advance toward 100-million-tonne resource targets, with La Romana resource estimation due in H2 2026.

Recent gold discovery at the Providencia target within the Cármenes project adds significant value optionality, with initial drilling intersecting 46 meters of 1.1 grams per tonne gold. This discovery was unexpected, as historical mining focused exclusively on copper, cobalt, and nickel extraction without recognizing gold potential.

Induced polarization surveys and follow-up drilling indicate near-surface, bulk-mineable systems attractive to potential acquirers seeking advanced-stage projects with established infrastructure connectivity.

Exploration Cycles vs Investment Windows

Many copper junior mining companies remain undervalued due to broader risk-off sentiment in equity markets, despite structural alignment with long-term supply-demand fundamentals. Investors may benefit from pre-resource re-rating events, particularly as refined copper flows become increasingly regionalized and supply security gains prominence in corporate procurement strategies.

The Investment Thesis for Copper

The US refined copper exemption, while representing a tactical policy correction, underscores deep structural misalignments in the global copper market. These misalignments present unique positioning opportunities for investors willing to navigate near-term volatility in exchange for exposure to multi-year supply-demand themes.

- Refined copper exemption created significant market disruption, resetting price floors and eliminating arbitrage-driven speculation that had distorted regional pricing relationships.

- Inventory accumulation and trade route reconfiguration signal near-term volatility, but long-term demand for clean, traceable feedstock remains structurally bullish due to electrification and ESG requirements.

- Projects located in Tier 1 jurisdictions with established infrastructure access, low carbon intensity operations, and active exploration catalysts are optimally positioned to absorb redirected capital flows.

- Gladiator Metals offers near-infrastructure, shallow high-grade copper-gold mineralization in Canada, supported by strong First Nation partnerships and year-round operational capability.

- Marimaca Copper provides a low-strip ratio, low-carbon oxide development model with demonstrated scalability and advanced feasibility study completion.

- Fitzroy Minerals delivers high-risk, high-reward IOCG and porphyry exploration optionality across two established mining jurisdictions with complementary geological settings.

- Pan Global Resources combines exploration scale advantages with proximity to operating infrastructure within Spain's premier base metal belt, enhanced by unexpected gold discovery potential.

The US decision to exempt refined copper while targeting semi-finished products reveals a broader recalibration of copper policy and supply security priorities. As trade routes evolve, price signals adjust, and demand migrates regionally, investors must reassess asset quality through multiple lenses: infrastructure readiness, jurisdictional reliability, and ESG compliance.

Strategic copper projects with development flexibility, supportive policy environments, and operational visibility stand to benefit in this transformed landscape. In an environment where volatility creates opportunity and policy uncertainty demands adaptability, clarity of execution and jurisdictional advantages will define long-term investment returns. The copper market's new reality rewards preparedness over speculation, and strategic positioning over tactical trading.

Analyst's Notes

Subscribe to Our Channel

Stay Informed