What You Need to Understand About the Nuclear Sector Before You Invest in Uranium - Part 1

Uranium supply deficits, policy shifts, and SMR demand are reshaping nuclear markets. Utilities abandon spot purchasing for premium long-term contracts.

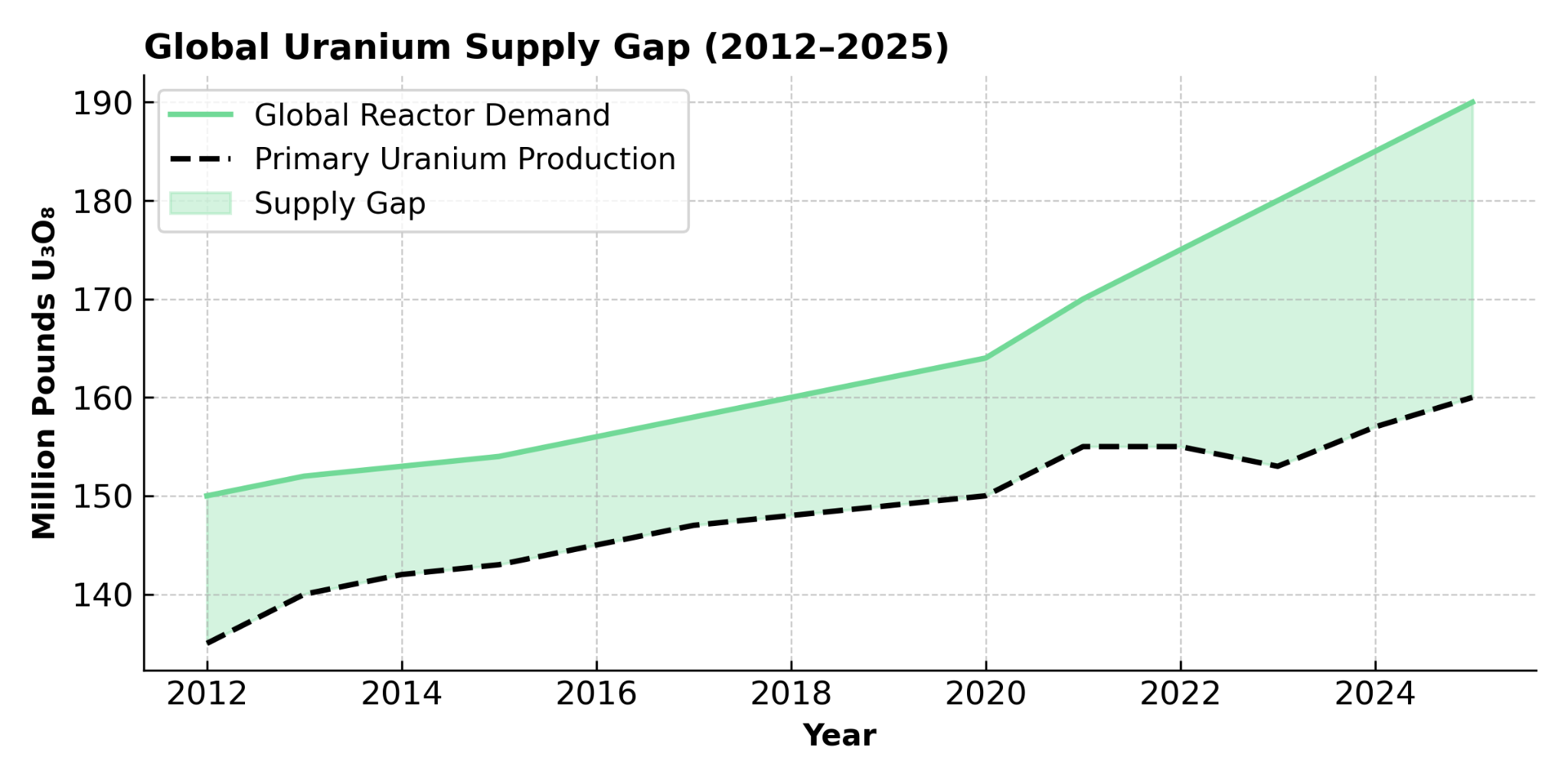

- The supply-demand imbalance in uranium is intensifying, with global production covering only 80-90% of reactor demand; Kazatomprom’s 20% production cut and political instability in Niger have effectively removed about 30% of reliable supply capacity from the market.

- Policy segmentation is fragmenting markets, as the Russia–Ukraine conflict accelerates Western efforts to regionalize nuclear fuel supply chains, creating premium pricing for producers in Tier-1 jurisdictions and pushing utilities away from spot purchases toward long-term agreements.

- A demand wave for Small Modular Reactors is building, as SMRs transition from concept to commercial deployment and tech giants like Microsoft actively seek nuclear power for data centers, adding new demand vectors beyond traditional utility baseload requirements.

- Inventory dynamics are shifting, since historical secondary supply sources such as inventory drawdowns, re-enrichment, and downblending, which once fulfilled 10-15% of reactor demand, are diminishing, forcing greater reliance on primary production amid constrained mining capacity.

- Investment capital is increasingly flowing to production-ready assets, with uranium spot prices around $59.50/lb in mid-2025 driving institutional focus toward companies that have near-term production visibility, proven management teams, and operations in stable jurisdictions that command valuation premiums.

The Nuclear Renaissance: Demand Fundamentals

The global nuclear landscape has fundamentally shifted from post-Fukushima decline toward expansion-driven growth. In 2024, the world's nuclear power plants supplied 2,667 TWh of electricity through 398 GWe of operable capacity. More significantly, 69 reactors are currently under construction in 2025, representing the strongest construction pipeline in decades.

This capacity expansion reflects nuclear power's strategic positioning in the energy transition. Nuclear energy avoided over 68 Gt of CO2 emissions between 1971 and 2022, providing 47% of the USA's low-carbon electricity and one-third of the European Union's clean power in 2023. The base-load characteristic of nuclear generation creates predictable fuel demand patterns, differentiating it from intermittent renewable sources that require grid balancing solutions.

SMR Technology & New Market Applications

Industry forecasts for Small Modular Reactors through 2040 utilize both bottom-up approaches for defined SMR projects and top-down modeling for generic SMR concepts. Only Light Water Reactor SMRs are considered for commercial deployment within the forecasting period, encompassing four major applications: electricity generation, hydrogen production, replacing coal-fired plant generation, and off-grid remote site power.

Colin Healey, Chief Executive Officer of Premier American Uranium, points to why technology firms are leaning into nuclear:

“Tech companies want to deliver their products in the most green, emission-free way possible, and they see nuclear as the solution, safe, green power at a large scale with incredible uptime.”

Tech sector interest represents a paradigm shift in nuclear demand patterns. Microsoft's active pursuit of nuclear power for data centers signals that technology companies are moving beyond renewable energy certificates toward 24/7 carbon-free electricity solutions. This creates new demand vectors outside traditional utility procurement cycles, potentially accelerating SMR deployment timelines and adding demand elasticity to uranium markets.

David Cates, President and Chief Executive Officer of Denison Mines, highlights Microsoft’s public endorsement of nuclear as a critical signal:

“We've seen the developments with Microsoft in terms of supporting nuclear energy to supply power to their data centers. The fact that they're joining and publicly joining the WNA is icing on top of the stories that have already occurred.”

Supply-Side Constraints & Geopolitical Fragmentation

The uranium supply landscape is characterized by structural deficits that have persisted since 2018. Primary uranium production currently fulfills only 85% of global reactor demand, down from approximately 90% between 2012 and 2017. This deterioration reflects both demand growth and supply-side disruptions that have removed reliable production capacity from the market.

Kazatomprom's approximately 20% reduction in 2025 production guidance, lowering midpoint output to 14 million pounds U3O8, represents the most significant supply shock in recent years. Combined with political instability in Niger, a jurisdiction contributing substantial global uranium output, these events have effectively removed nearly 30% of global supply from reliable production status. This supply fragility is forcing utilities to abandon just-in-time purchasing strategies in favor of securing long-term contracts, often at premiums to spot pricing.

Gavin Chamberlain, Chief Executive Officer of Bannerman Energy, underscores how uncertainty dominates utility discussions:

“The issue for us has been the lack and the difficulties in supply… The demand side of things speaks for itself. Most of the discussions have been around can the supply actually meet their targets”

Regional Market Segmentation

Geopolitical instability from the Russia-Ukraine conflict has accelerated a shift toward regionalized nuclear fuel supply chains. Recent analysis specifically examines regional demand and supply dynamics in the context of potential market segmentation driven by government legislation and utility risk management policies.

The United States has designated uranium as a critical mineral, banned Russian uranium imports, and invested in domestic enrichment capacity. This policy framework creates structural demand for Western-origin uranium while fragmenting previously globalized fuel cycle relationships. As Phil Williams, Chief Executive Officer of IsoEnergy, explains the strategic value of jurisdictional diversification:

'We're diversified explorer developer and near-term producer with uranium projects in the top three jurisdictions in the world, Canada, the United States and Australia”

Secondary Supply Dynamics

Secondary supply sources, including inventories, recycled materials, ex-military stockpiles, enrichment underfeeding, and depleted uranium re-enrichment, have historically provided 10-15% of reactor requirements. However, these sources face "market mobility" constraints that limit their availability and timing in commercial markets.

Market analysis emphasizes that recycling of nuclear material depends largely on political rather than economic factors, creating uncertainty around secondary supply reliability. As historical inventory drawdowns diminish and geopolitical tensions constrain cross-border material flows, primary production must shoulder increasing responsibility for meeting reactor demand.

Market Structure & Pricing Mechanisms

Most uranium continues to trade through multiannual contracts based on utility requirements, with spot markets serving short-term procurement adjustments. Unlike commodities traded on terminal clearing platforms like the London Metal Exchange, uranium operates through bilateral relationships between traders, brokers, producers, and utilities.

The spot market's physical nature and limited liquidity create price volatility that reflects immediate supply-demand imbalances rather than long-term fundamentals. At ~$59.50/lb in mid-2025, spot uranium pricing remains well above most producers' all-in sustaining costs, creating strong incentives for production expansion while supporting utilities' shift toward long-term contracting.

Contract structures typically include location and price swaps, carry trades, and physical or monetary settlement options. The role of traders and intermediaries has expanded significantly, providing market liquidity while balancing location-specific requirements and mitigating supply risks for utilities.

For uranium miners, the ability to capture value depends on being positioned in production during upcycles rather than waiting on the sidelines. Matthew Gili, President of Ur Energy, stresses the importance of timing:

“The entities that make the real money are the ones operating when the price goes up. Not so much the companies or entities that are waiting for the price to go up to implement their construction program. Cycles don’t last long, you’ve got to be in production during the cycle.”

Conversion & Enrichment Bottlenecks

The nuclear fuel cycle encompasses mining, milling, conversion, enrichment, and fuel fabrication stages provided by specialist companies. Each stage represents a potential bottleneck that could constrain fuel supply regardless of uranium availability.

Conversion capacity, the process of converting uranium concentrates to UF6 for enrichment, has faced particular constraints as geopolitical tensions limit access to Russian conversion services. Similarly, enrichment capacity utilization varies significantly by region, with excess capacity in some jurisdictions offset by supply chain fragmentation in others.

These fuel cycle bottlenecks create additional complexity for uranium investors, as uranium concentrate demand ultimately depends on downstream processing capacity. Companies with integrated fuel cycle exposure or toll processing agreements may capture additional value from these structural constraints.

Fuel Cycle Economics & Cost Structure

Nuclear fuel represents a unique cost dynamic compared to fossil fuel plants, typically accounting for less than 20% of total operational costs in nuclear facilities versus up to 80% in fossil fuel-fired plants. This low fuel cost sensitivity provides nuclear operators with considerable economic resilience during uranium price volatility, while simultaneously creating inelastic demand characteristics that benefit uranium producers during supply constraints.

The fuel cycle's complexity extends beyond simple extraction, encompassing front-end processes (mining through fuel fabrication) and back-end activities (temporary storage, reprocessing, recycling, waste disposal). Each stage requires specialized infrastructure and expertise, often distributed across multiple countries. A single fuel assembly might involve uranium mined in Australia, converted in Canada, enriched in the UK, and fabricated in Sweden, illustrating the international interdependence that creates both efficiency opportunities and supply chain vulnerabilities.

This geographic dispersion necessitates sophisticated logistics coordination, as nuclear materials represent only a small fraction of worldwide cargo while requiring detailed advance planning and compliance with International Atomic Energy Agency transport regulations established in 1961. The regulatory framework's maturity contributes to nuclear transport's excellent safety record, though it adds complexity and lead times that reinforce utilities' preference for long-term contracting over spot market dependence.

Lumpy Demand Patterns & Inventory Dynamics

Uranium demand exhibits distinctly "lumpy" characteristics rather than continuous consumption patterns, with most reactors refueled at intervals of one year or more. This creates predictable but concentrated procurement cycles that can generate significant spot market volatility when multiple utilities simultaneously enter the market.

The approximately two-year lead time from uranium concentrate purchase to fuel loading in reactors creates substantial working capital requirements and inventory management challenges. Utilities maintain large fuel inventories relative to immediate reactor requirements, providing operational flexibility while creating opportunities for inventory-driven market manipulation during supply disruptions.

These demand characteristics favor uranium suppliers capable of providing consistent, contracted supply rather than relying solely on spot market transactions. Companies like Energy Fuels benefit from this dynamic through existing long-term uranium sales contracts with deliveries scheduled from 2025 to 2030, providing revenue visibility that supports higher equity valuations. The lumpy demand pattern also creates opportunities for financial market participants, including exchange-traded funds and financially settled futures contracts that allow investors to hold uranium inventories directly, adding liquidity while potentially amplifying price volatility during supply-demand imbalances.

Company Positioning & Investment Implications

Investors are increasingly prioritizing uranium companies operating in stable, Tier-1 jurisdictions with clear regulatory frameworks and operational visibility. This preference reflects heightened awareness of geopolitical risks following supply disruptions in Niger and sanctions on Russian nuclear materials.

ATHA Energy positions itself as a large-scale exploration company in the Canadian uranium sector, and holds the largest exploration land position in Canada, encompassing over 7 million acres across premier uranium districts including the Athabasca Basin.The company's 10% carried interest in NexGen Energy and IsoEnergy lands provides additional exposure to major development projects while diversifying exploration risk.

Production Readiness & Cash Flow Visibility

With uranium markets tightening, institutional capital is flowing toward companies with near-term production capabilities rather than early-stage exploration plays. Energy Fuels demonstrates this appeal through active operations at three conventional uranium mines and processing at the White Mesa Mill, the only operating conventional uranium mill in the USA.

Mark Chalmers, Energy Fuels' Chief Executive Officer, describes the company's strategic positioning:

"Energy Fuels is a unique company where we are a critical mineral company building a critical mineral hub that is built around the uranium industry as the largest producer of uranium in the United States."

The company's diversification into rare earth elements provides additional revenue streams while leveraging existing infrastructure and regulatory permits.

ISR Technology & Cost Advantages

In-Situ Recovery represents a lower-cost, environmentally advantaged uranium extraction method compared to conventional mining. enCore Energy positions itself as America's leading In-Situ Recovery firm, operating three licensed Central Processing Plants in South Texas with combined resources of 30.94 million pounds in Measured & Indicated categories.

Executive Chairman William Sheriff articulates the company's capital discipline:

"As enCore pushes forward on its aggressive uranium extraction plans in South Texas, we continue to execute on our stated ongoing non-core asset divestment strategy: Non-core assets that can provide value and reduce shareholder dilution."

Development-Stage Assets & Financing Challenges

Companies advancing development-stage uranium projects face complex financing environments amid geopolitical uncertainties. Global Atomic's Dasa Project in Niger exemplifies these challenges, with construction 75% complete despite regional political instability.

The project's robust economics, including a 57% after-tax IRR at $75/lb uranium pricing, demonstrate the potential returns from well-positioned development assets. However, jurisdictional risks require careful evaluation of political stability and regulatory continuity when assessing development-stage investments.

The Investment Thesis for Uranium

- Structural uranium supply shortfalls of 10–20% are creating pricing power for producing companies, with spot prices at $59.50/lb supporting strong operating margins across most cost curves.

- Utilities’ shift from spot purchases to long-term contracting allows producers to capture premium pricing while providing revenue visibility that supports higher equity valuations.

- Geopolitical fragmentation is driving capital toward Tier-1 jurisdiction operators such as ATHA Energy in Canada, Energy Fuels in the U.S., and IsoEnergy in Canada, the U.S., and Australia, creating valuation premiums over peers in higher-risk locations.

- Technology differentiation is becoming a competitive edge, with ISR operators like enCore Energy benefiting from lower capital intensity and environmental advantages, while integrated producers like Energy Fuels leverage processing infrastructure to capture additional fuel cycle margins.

- Companies with near-term production capability are positioned to benefit from Small Modular Reactor deployment acceleration and the tech sector’s adoption of nuclear beyond traditional utility demand patterns.

- Market volatility and development financing challenges favor companies with strong balance sheets, such as Energy Fuels with $210 million in cash and zero debt, and IsoEnergy with C$84.7 million in cash equivalents, over highly leveraged peers.

Why Policy-Tight Markets Reward Prepared Pounds

The uranium sector's transformation from post-Fukushima decline toward supply-constrained growth creates compelling investment opportunities for sophisticated investors willing to navigate complex geopolitical and technical factors. Structural supply deficits, policy-driven market segmentation, and emerging SMR demand are reshaping fundamental market dynamics while forcing utilities away from just-in-time purchasing toward premium long-term contracting.

Success in this environment requires careful evaluation of jurisdictional risk, operational capability, and financial strength rather than simply betting on commodity price appreciation. Companies combining Tier-1 jurisdiction exposure with near-term production visibility are best positioned to capitalize on the nuclear renaissance while managing the inherent risks of this specialized commodity sector.

TL;DR:

The uranium sector faces structural supply deficits as production covers only 80-90% of reactor demand, while Kazatomprom's production cuts and Niger instability remove 30% of reliable global supply. Geopolitical tensions from the Russia-Ukraine conflict are fragmenting nuclear fuel markets, forcing utilities to abandon just-in-time purchasing for premium long-term contracts with Western suppliers. Small Modular Reactors and tech company nuclear adoption are creating new demand vectors beyond traditional utilities. This environment favors uranium companies in Tier-1 jurisdictions with near-term production capabilities, strong balance sheets, and proven management teams, as investors prioritize operational visibility over exploration plays in an increasingly supply-constrained market.

FAQ's (AI-Generated):

Global uranium production currently fulfills only 85% of reactor demand, down from 90% historically, due to Kazatomprom's 20% production cuts and political instability in Niger removing nearly 30% of reliable supply capacity.

The Russia-Ukraine conflict has accelerated Western efforts to regionalize nuclear fuel supply chains, creating premium pricing for Tier-1 jurisdiction producers while fragmenting previously globalized fuel cycle relationships.

SMRs are smaller, more flexible nuclear reactors being developed for electricity generation, hydrogen production, coal plant replacement, and remote power applications, with tech companies like Microsoft actively pursuing nuclear power for data centers.

Companies with near-term production capabilities in stable jurisdictions (Canada, USA, Australia), strong balance sheets, and proven management teams are favored over early-stage exploration plays.

Nuclear fuel typically represents less than 20% of total operational costs versus up to 80% in fossil fuel plants, creating inelastic demand that benefits uranium producers during supply constraints.

Analyst's Notes

Subscribe to Our Channel

Stay Informed