What You Need to Understand About the Nuclear Sector Before You Invest in Uranium - Part 2

Global uranium shortage covers 80-90% reactor needs as $900M US SMR investment and 397.6 GWe capacity drive Western supply chain restructuring.

- Structural uranium supply deficits persist as mine development timelines stretch 7-10 years while reactor demand growth accelerates through Small Modular Reactor deployment and lifetime extensions.

- Geopolitical fragmentation from Russian uranium sanctions and Kazakhstan production cuts is forcing utilities to abandon spot market reliance in favor of long-term contracting at premium prices.

- Western energy security policies are creating jurisdictional premiums for North American and allied uranium producers, fundamentally altering traditional cost-based valuation frameworks.

- Small Modular Reactor programs receiving $900 million in U.S. Department of Energy funding signal demand acceleration beyond current International Atomic Energy Agency projections.

- Critical infrastructure control including In-Situ Recovery facilities and licensed mills provides strategic advantages as reshoring initiatives prioritize supply chain resilience over cost optimization.

The Strategic Mineral Imperative Reshaping Uranium Markets

Global energy security concerns are fundamentally transforming how Western governments approach uranium supply chains. The designation of uranium as a critical mineral across multiple jurisdictions reflects a strategic shift from market-driven procurement to security-focused sourcing strategies. This transformation extends beyond traditional supply and demand dynamics to encompass geopolitical alignment, supply chain transparency, and infrastructure sovereignty.

The U.S. Inflation Reduction Act allocated substantial funding for domestic critical mineral development while the CHIPS and Science Act prioritizes supply chain resilience. Similar initiatives across Canada, Australia, and European Union member states demonstrate coordinated Western efforts to reduce dependence on potentially adversarial suppliers. These policy frameworks create structural advantages for uranium producers operating within allied jurisdictions.

Recent supply chain disruptions have exposed the vulnerability of globally integrated fuel cycles. Russian uranium import restrictions, implemented as part of broader sanctions regimes, removed approximately 20% of U.S. reactor fuel supply. Simultaneously, Kazakhstan's production guidance cuts and Niger's political instability following military coups have created multiple simultaneous supply shocks across different geographical regions.

Market Structure Evolution & Price Discovery Mechanisms

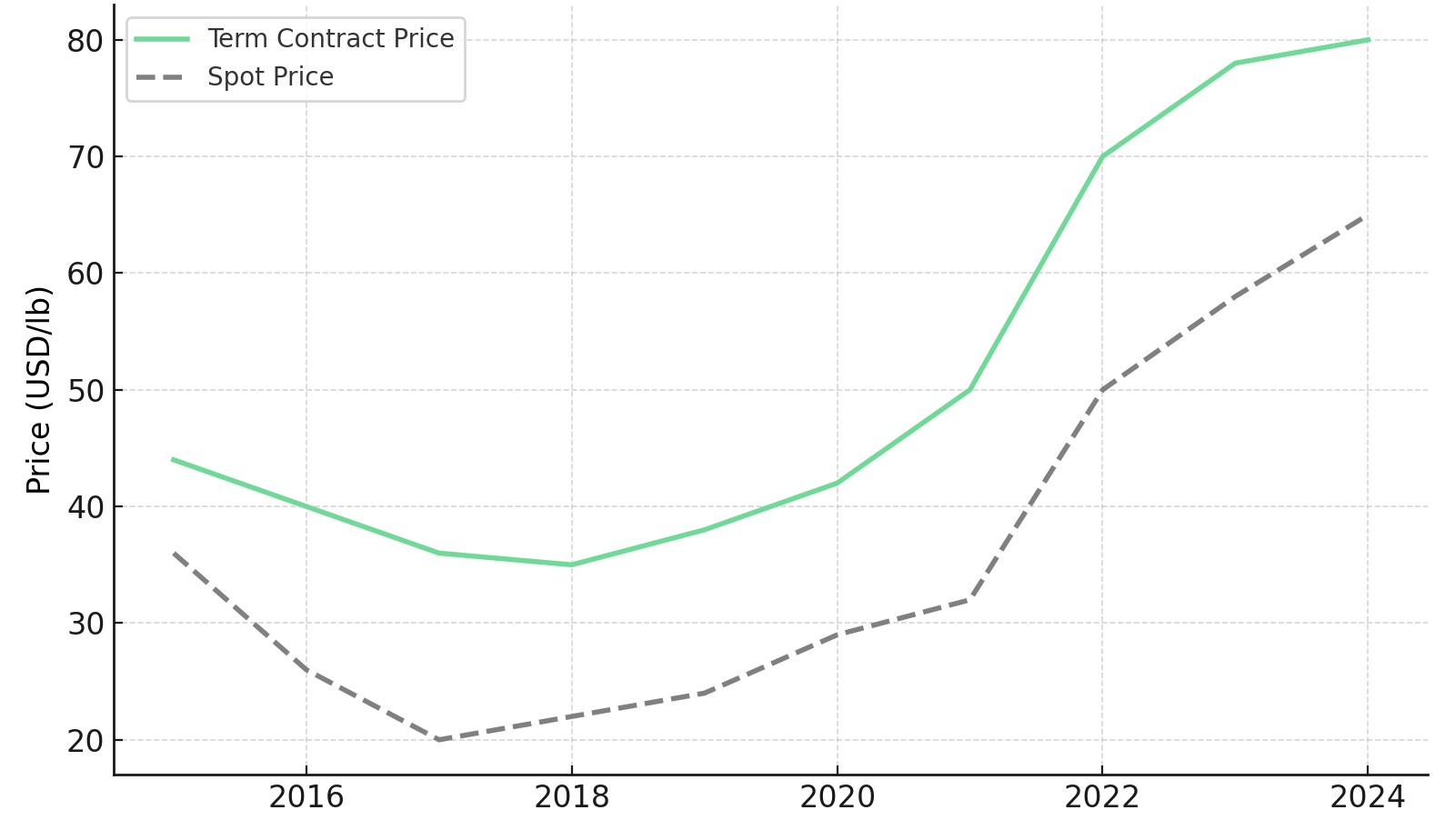

The uranium market is transitioning from spot price discovery to term contract-based pricing mechanisms. Utilities historically relied on spot markets for marginal supply requirements while maintaining long-term contracts for baseline needs. Current market conditions are forcing a complete reversal of this strategy as spot market liquidity remains constrained and price volatility increases.

Term contracting at $70-80 per pound represents a significant premium to historical pricing levels, reflecting not just supply scarcity but also jurisdictional risk premiums and delivery certainty values. This pricing structure incorporates geopolitical stability assessments, permitting timeline certainty, and infrastructure access considerations that extend well beyond traditional mining cost structures.

The shift toward strategic sourcing is evident across Western utility procurement strategies, with companies prioritizing supply chain transparency and jurisdictional alignment over pure cost optimization. This fundamental change in procurement methodology creates sustained competitive advantages for producers operating within allied jurisdictions while establishing structural pricing premiums that persist beyond traditional commodity cycles.

Structural Supply Deficits & Infrastructure Constraints

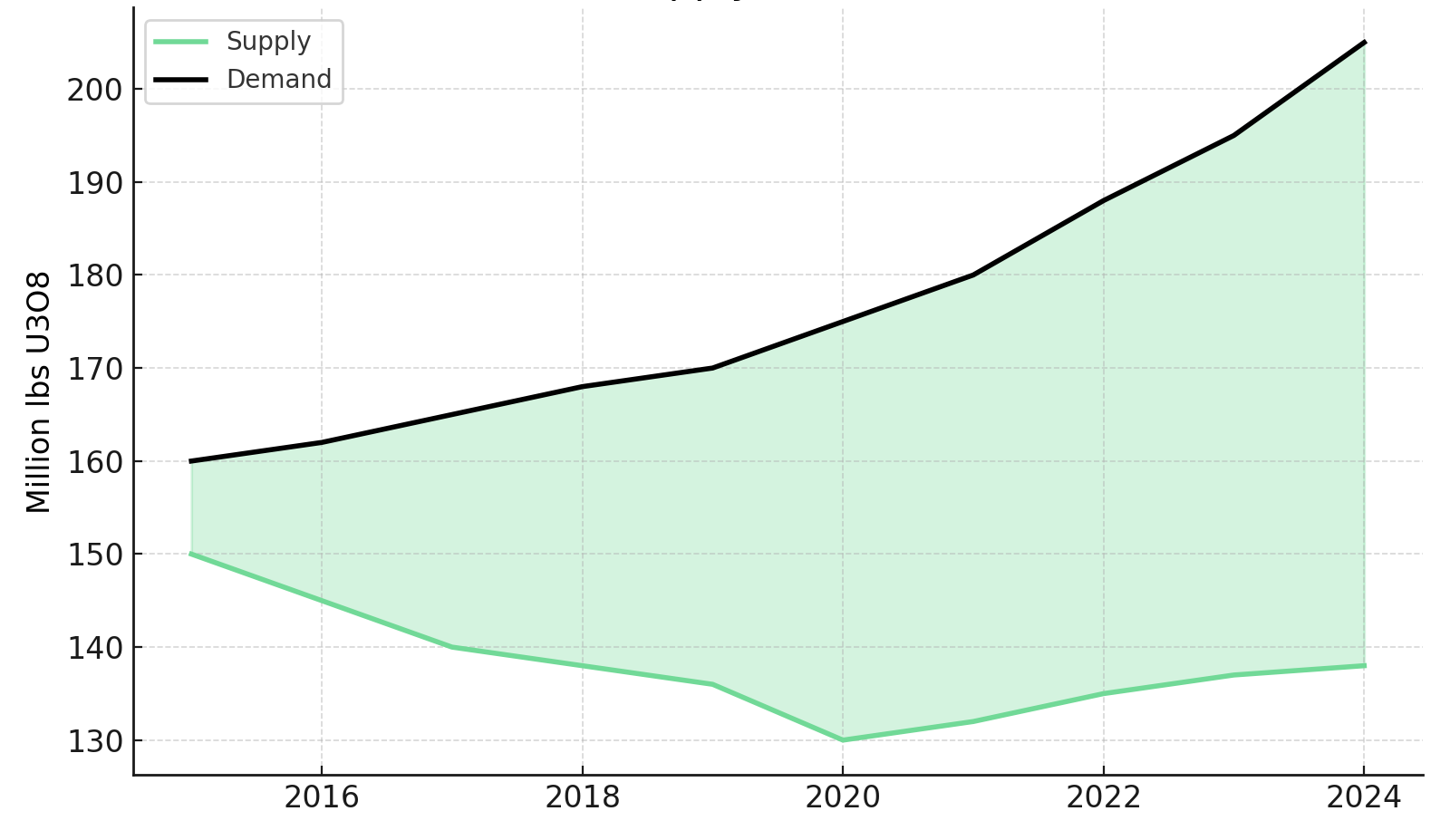

Global uranium mine supply currently satisfies only 80-90% of annual reactor fuel requirements, creating a persistent structural deficit requiring secondary supply sources, including government stockpile releases, recycled reactor fuel, and downblended weapons material. This supply gap has existed for over a decade but is becoming more acute as secondary sources diminish and reactor demand increases.

New uranium mine development requires extensive lead times encompassing exploration, resource definition, environmental permitting, construction, and commissioning phases. Recent project examples demonstrate 7-10 year development cycles even in favorable regulatory environments. This temporal mismatch between supply response capability and demand growth creates fundamental market tightness that supports higher pricing levels.

The concentration of global uranium production within a limited number of large-scale operations increases supply chain vulnerability to operational disruptions, regulatory changes, or geopolitical tensions. Kazakhstan's Kazatomprom controls approximately 25% of global mine supply while Canada's Athabasca Basin contributes high-grade production from a geographically concentrated area.

Processing Capacity Bottlenecks & Conversion Constraints

Uranium mining represents only the initial stage of a complex fuel cycle requiring multiple processing and conversion steps before reactor-ready fuel fabrication. Processing capacity constraints at conversion facilities, particularly for uranium hexafluoride production, create additional supply chain bottlenecks beyond mine-level production limitations.

The limited number of operational uranium mills and conversion facilities creates processing bottlenecks that can constrain effective mine supply even when ore production capacity exists. Energy Fuels operates the White Mesa Mill in Utah, representing the only operational conventional uranium mill in the United States, creating potential processing constraints for domestic production expansion while simultaneously providing strategic infrastructure control.

In-Situ Recovery operations require specialized Central Processing Plants that represent significant infrastructure investments with multi-year permitting and construction timelines. Companies controlling multiple ISR facilities benefit from operational synergies, shared infrastructure costs, and production flexibility that enables optimization across different uranium price environments.

Jurisdictional Risk Assessment & Investment Capital Allocation

Traditional uranium valuation models focused primarily on resource quality, operating costs, and commodity price sensitivity. Current market conditions require comprehensive jurisdictional risk assessment incorporating political stability, regulatory certainty, permitting timeline predictability, and geopolitical alignment with major consuming markets.

Tier 1 jurisdictions including Canada, United States, and Australia command significant valuation premiums reflecting not just political stability but also regulatory frameworks that support long-term investment planning. These jurisdictions offer established mining codes, transparent permitting processes, and legal systems that protect property rights and contract enforcement.

The regulatory environment in favorable jurisdictions provides operational certainty that translates directly into project economics and investment attractiveness. William Sheriff, Executive Chairman of enCore Energy, details the regulatory advantages available in premium jurisdictions:

"Our South Dakota project got Fast 41… Fast 41 gives you a much more certain and much more acceptable timeline to get through all of your filing… It gives us credibility as well with the federal regulators."

Financial Health & Strategic Positioning

Projects located in higher-risk jurisdictions may offer attractive economics based on resource quality and operating cost projections but face capital allocation constraints due to perceived political and regulatory risks. Institutional investors increasingly incorporate Environmental, Social, and Governance criteria into investment decisions, favoring operations in jurisdictions with established regulatory frameworks and stakeholder engagement processes.

Control over critical infrastructure assets including licensed processing facilities, permitted mine sites, and transportation corridors provides strategic advantages that extend beyond traditional resource ownership. These infrastructure assets offer processing capacity, regulatory certainty, and operational flexibility that can generate value through multiple commodity cycles and market conditions.

The strategic value of jurisdictional positioning extends beyond operational considerations to encompass market access and customer alignment. Philip Williams, Chief Executive Officer and Director of IsoEnergy, articulates the portfolio diversification benefits:

"We're a diversified explorer, developer and near-term producer with uranium projects in the top three jurisdictions in the world, Canada, the United States and Australia."

Small Modular Reactor Deployment and Demand Growth Projections

Small Modular Reactor technology represents a paradigm shift in nuclear power deployment strategies, offering enhanced flexibility, reduced capital requirements, and accelerated construction timelines compared to traditional large-scale reactor projects. SMR programs across multiple countries are receiving substantial government funding and regulatory support, indicating strong policy commitment to this technology pathway.

Current global nuclear capacity stands at 397.6 GWe across 439 operational units, with an additional 70.8 GWe under construction. The U.S. Department of Energy allocated up to $900 million for domestic SMR deployment while President Biden's executive order targets increasing U.S. nuclear capacity from 100 GWe to 400 GWe by 2050. These ambitious targets require unprecedented nuclear construction rates that would significantly increase uranium fuel requirements beyond current consumption levels.

China's progress with the HTR-PM demonstration project featuring two 210 MWe steam turbines and the under-construction ACP100 'Linglong One' at 125 MWe demonstrates SMR commercial viability. Russia's RITM-200 program for floating power units expands potential deployment scenarios while creating competitive pressure for Western SMR development.

Exploration Outlook & Resource Development Plans

SMR deployment schedules suggest meaningful uranium demand increases beginning in the late 2020s with acceleration through the 2030s. However, utilities associated with SMR projects are already entering long-term uranium procurement contracts to secure future fuel supply, creating immediate demand pressure rather than waiting for reactor commissioning dates.

The exploration implications of expanding nuclear demand create opportunities for discovery and resource development in underexplored geological districts. Troy Boisjoli, Chief Executive Officer of ATHA Energy, describes the exploration potential in emerging uranium corridors:

"We need more tier-one scale uranium systems. We believe that what we see right now, we're at the likelihood of this continuing to build upon itself, into a system like we're talking about."

The modular nature of SMR technology enables more predictable fuel requirements and potentially different uranium specifications compared to traditional large reactor designs. High-grade deposits become increasingly valuable as utilities seek to minimize fuel cycle costs and maximize energy density in compact reactor designs optimized for distributed deployment scenarios.

Geopolitical Supply Chain Bifurcation & Western Realignment

The global uranium market is evolving into distinct supply chains aligned with geopolitical blocs rather than operating as a unified global commodity market. Western markets are systematically reducing dependence on Russian uranium while building alternative supply chains through allied jurisdictions and friendly nations.

This bifurcation creates parallel pricing systems where Western-aligned uranium commands premium pricing compared to globally traded material. Utilities in NATO countries and allied nations prioritize supply chain security and geopolitical alignment over pure cost optimization, fundamentally altering competitive dynamics within different market segments.

The strategic alignment between uranium producers and Western government policy objectives creates opportunities for projects that might otherwise face jurisdictional challenges. Stephen Roman, President and Chief Executive Officer of Global Atomic, illustrates the policy-level engagement occurring:

"The administration right up to Secretary of State Marco Rubio knows about our project… We are primarily supplying US utilities and they're probably taking 90% of our offtake contracts at the moment."

Market Volatility, Currency Effects, & Investment Risk Controls

Enhanced supply chain transparency requirements emerging from Western governments mandate detailed documentation of uranium origin, processing history, and transportation routes. These requirements favor producers operating within allied jurisdictions while creating compliance burdens for complex international supply chains.

Chain of custody documentation and material traceability systems add operational complexity and costs but provide competitive advantages for producers capable of meeting enhanced transparency standards. Utilities increasingly require detailed supply chain documentation to satisfy regulatory requirements and internal governance standards.

For institutional investors, exposure to projects in stable, dollar-linked jurisdictions provides natural foreign exchange hedging while mitigating sovereign risk. Operations in countries with fragile governance structures may require discounted valuation multiples despite attractive project economics, as evidenced by high-return projects that struggle to access capital markets due to jurisdictional concerns.

Operational Urgency & Technical Efficiency in Production

The uranium industry faces immediate challenges in bringing production to market, emphasizing high-grade resources, rapid development capabilities, and technical operational excellence. Companies demonstrating superior operational efficiency and production acceleration capabilities command premium valuations as utilities prioritize supply security over cost considerations.

Higher ore grades provide natural hedging against inflationary cost pressures while improving project economics and reducing processing requirements. Companies with access to high-grade deposits benefit from operational flexibility and cost advantages that become increasingly valuable in supply-constrained markets.

Resource quality improvements through exploration and development can provide significant economic advantages in higher uranium price environments. Mark Chalmers, President and Chief Executive Officer of Energy Fuels, quantifies the operational benefits:

"Right now there's a lot of people struggling with the ramp ups of their projects and struggling with their costs.In our case, there have been increases in cost. But one of the best ways to combat that was with higher grade and that's what we're seeing at the Pinyon Plain"

Industry Structural Challenges & Market Inefficiencies

The uranium market continues to face structural inefficiencies that create both challenges and opportunities for market participants. Delivery failures and production shortfalls have become recurring themes across multiple development projects, highlighting the complexity of bringing uranium projects to commercial production.

Market pricing mechanisms often fail to reflect the true cost of marginal uranium production, creating disconnects between spot prices and the capital requirements for new mine development. These structural inefficiencies create opportunities for well-positioned producers while highlighting the risks associated with development-stage investments.

The industry's track record of execution challenges creates skepticism among investors and utilities regarding project delivery capabilities. Philip Williams, Chief Executive Officer and Director of IsoEnergy, addresses the industry-wide execution issues:

"The actual real price of getting that marginal pound of production out of the ground is much higher than anyone thinks."

This execution risk premium creates competitive advantages for companies with demonstrated operational capabilities, established infrastructure, and proven management teams. Market participants increasingly differentiate between resource potential and production capability when making investment and procurement decisions.

The Investment Thesis for Uranium

- Long-term structural supply deficits persist due to extended mine development timelines while reactor demand growth accelerates through SMR deployment and existing reactor lifetime extensions creating sustained market tightness.

- Geopolitical supply chain bifurcation drives systematic shifts toward Western-aligned uranium producers as utilities prioritize supply security over cost optimization creating sustained pricing premiums for allied jurisdiction production.

- Critical infrastructure control including licensed processing facilities and In-Situ Recovery operations provides strategic advantages and operational flexibility across multiple market cycles while generating toll revenue streams independent of commodity pricing.

- Jurisdictional risk assessment frameworks favor Tier 1 mining jurisdictions offering political stability, regulatory certainty, and strategic alignment with major consuming markets creating structural valuation premiums for quality assets in preferred locations.

- Small Modular Reactor programs receiving substantial government funding signal uranium demand growth beyond current International Atomic Energy Agency projections with utility procurement beginning immediately to secure future supply creating near-term demand pressure.

- Capital allocation increasingly favors operational readiness and execution certainty over pure resource quality creating valuation premiums for permitted assets, established producers, and companies with demonstrated development capabilities in supply-constrained markets.

Implications for Portfolio Construction

Uranium investment opportunities exist across multiple segments including producing operations, advanced development projects, and exploration companies with strategic land positions in proven districts. Each segment offers different risk-return profiles and exposure to various macro themes driving sector fundamentals while providing diversification benefits within commodity-focused portfolios.

Near-term producers benefit immediately from current supply tightness and rising term contract prices while providing operational leverage to sustain higher uranium pricing through existing production capabilities and infrastructure control. Advanced development projects offer exposure to production growth and project execution while exploration companies provide discovery optionality and resource expansion potential in proven uranium districts with established geological frameworks.

The sector's transformation from cyclical commodity exposure to strategic resource positioning creates investment opportunities that extend beyond traditional uranium price appreciation to include infrastructure value creation, strategic asset control premiums, and geopolitical alignment benefits that support sustained premium valuations across multiple market cycles and regulatory environments.

TL;DR

Global uranium markets are undergoing fundamental restructuring as Western governments treat nuclear fuel as strategic infrastructure rather than a commodity. Structural supply deficits persist with mines covering only 80-90% of reactor demand while new projects require 7-10 years to develop. Geopolitical tensions from Russian sanctions and Kazakhstan production cuts force utilities into long-term contracts at premium prices, abandoning spot market reliance. Small Modular Reactor programs receiving $900 million in U.S. funding signal accelerating demand beyond current projections. Western energy security policies create jurisdictional premiums for North American producers while critical infrastructure control through processing facilities provides strategic advantages. The transformation from cyclical commodity to strategic resource creates investment opportunities extending beyond price appreciation to include supply chain positioning and energy security premiums.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed