Analyst's Notes: Arizona Metals Corporation

Get industry analysts' take on the latest mining company press releases, and its effect on you - the investor.

Executive Summary

Arizona Metals Corporation (“AMC”) (TSX:AMC) is a resources company with two exploration projects in Arizona, USA. This note principally reviews the Kay Mine project.

There has been a steady flow of largely good news from Kay Mine and the share price has risen to give a market capitalisation of C$478 M.

Surprisingly, the Crux Investor analysis dug up more questions than answers on the project. Crucial information on the geometry of the mineralised material is poorly ordered and hard to decipher. The mineralisation might stack up and have real economic potential. Or it might not.

Concerns centred on the geometry of the mineralisation and the way the information is presented. There are many assayed but unreported drillholes and Arizona Metals plots its drilling results on simplified projections which can be misleading.

Technical reports note the geology is complex and structurally controlled, but this complexity is not fully reflected in the outward-facing marketing materials. The project is still at a very early stage of understanding, with no defined resources yet and no metallurgical test work done beyond basic mineralogical studies.

When Crux Investor views Arizona Metals alongside a company like Skeena Resources the differences are stark. Both companies are developing VMS deposits in north America, and the companies have similar market capitalisations, of C$479 M and C$456 M respectively.

This is where the similarities end. Arizona Metals has a lot of unanswered questions and no resource estimate. Skeena Resources has open pit reserves of 3.85 million ounces at 4.0 gt AuEq, a Feasibility Study hot off the press, and an estimated after tax NPV5 of C$1.4 billion.

Crux Investor would like Arizona Metals to provide sufficient information to enable investors to make an informed decision about the company. More information on geology, metallurgy, and economics please. Until then, Crux Investor would rather own Skeena Resources.

Introduction

Arizona Metals Corporation (“AMC”) (TSX:AMC) is a resources company with two exploration projects in Arizona, USA. Kay Mine is a polymetallic project centred on an area of historic mineralisation and Sugarloaf Peak is a gold exploration project. The company listed on the Toronto Stock Exchange in August 2019 via a reverse takeover of Croesus Gold Corporation (“Croesus”).

Soon after taking control of Croesus, AMC started drilling campaigns on its two projects.

Slow news from Sugarloaf Peak

By any measure news flow from Sugarloaf Peak has been slow. AMC is yet to publish metallurgical results on samples taken during 2020 drilling (Arizona Metals Corp. Interim Management’s Discussion & Analysis – Quarterly Highlights For the Three and Six Months Ended June 30, 2022 Discussion dated: August 29, 2022. Page 4). Given that good news travels fast and bad news does not, the inference is that Sugarloaf Peak metallurgy is bad. Accordingly, this note principally reviews the Kay Mine project.

Good news from Kay Mine

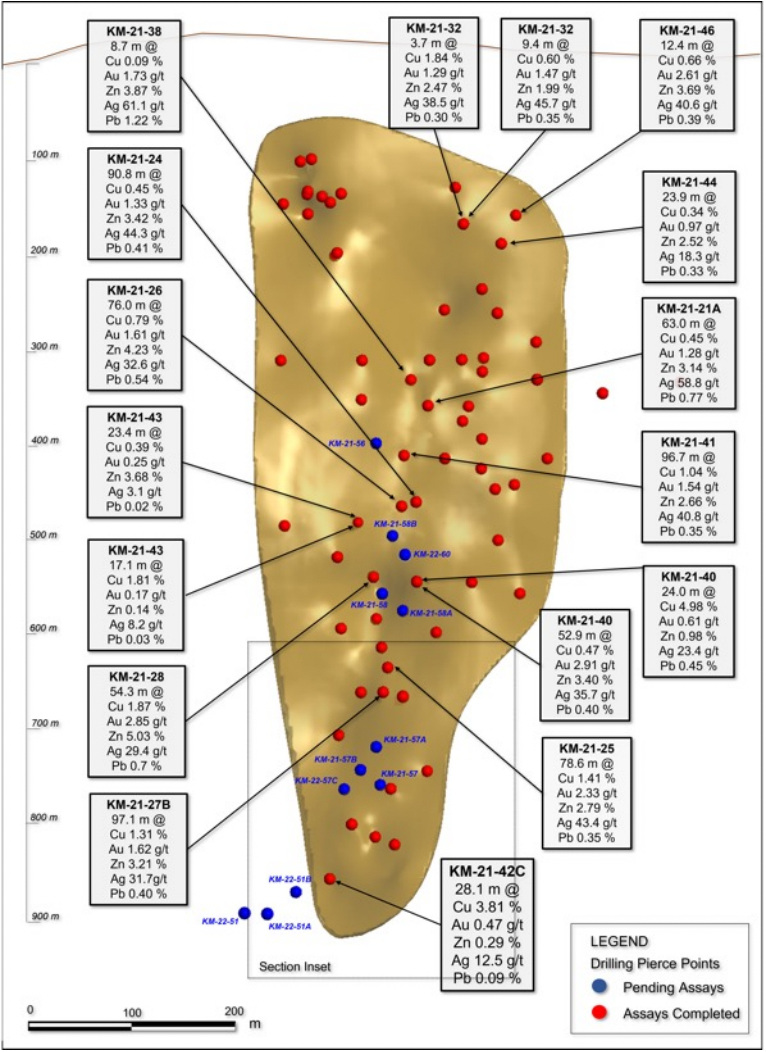

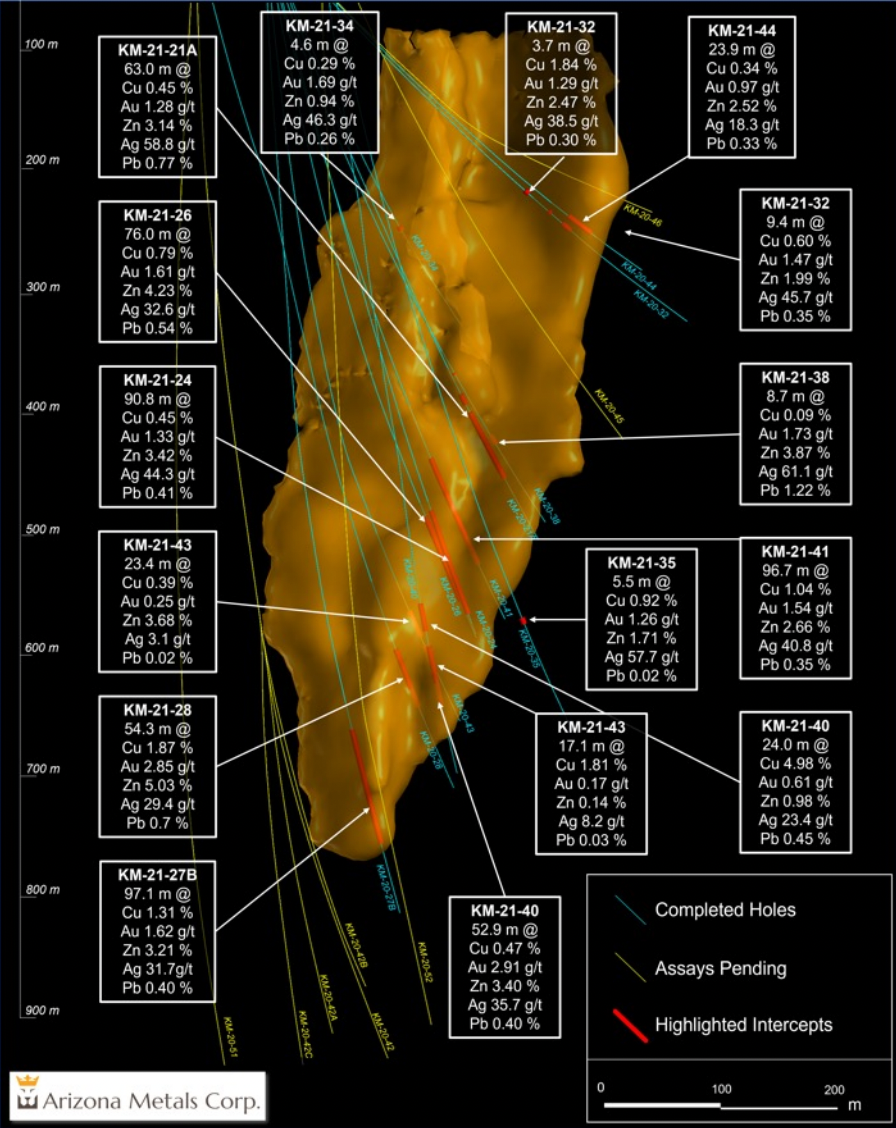

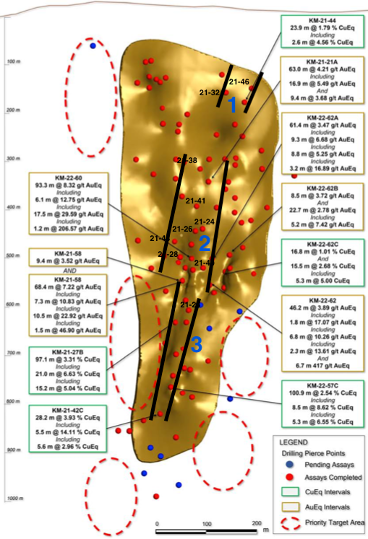

There has been a steady flow of largely good news from Kay Mine. The Company regularly releases news releases highlighting stellar intersections of high-grade material over good thicknesses. A recent drilling headline, for example, was 100.9 m at 2.5% CuEq; 61.4 m at 3.5 g/t AuEq; and 46.2 m at 3.9 g/t AuEq in three separate holes.

Glossing over the fact that TSX guidelines do not permit exploration results being reported in metal equivalents, these are Good Results. The market has responded to three years of this, with the share price having risen from ~20c in early 2020, to current levels of C$4.26, via a high of C$6.71 in early 2022.

Arizona Metals has a market capitalisation of C$478 M.

More questions than answers

Crux Investor was initially impressed with the Kay Mine project and decided to investigate further. Surprisingly, the investigation provided more questions than answers. Digging deeper into the projects gave the Analysts a headache. The way the information is presented makes it very hard to understand the real potential of the asset.

Crucial information on the geometry of the mineralised material is poorly ordered and hard to decipher. The mineralisation might stack up and have real economic potential. Or it might not. Here are some of the key concerns.

Cigar shapes and structure

Why is the key language of the NI 43-101 Technical Report (released 23 June 2021, effective date 21 May 2021 - found on SEDAR and not the company website) not fully reflected in the outward-facing marketing materials? The NI 43-101 describes the mineralisation as forming in “generally cigar to tabular shapes that pinch and swell” (NI 43-101, Technical Report, Kay Mine, page 19, paragraph 1).

Furthermore, a mapping expert hired to provide an in-depth analysis of the mineralisation wrote “Sulphide lenses are likely to be affected by steep-plunging tight folds, with the lenses being thinned and boudinaged in fold limbs and thickened in fold hinges” (Technical Report, page 36, paragraph 1).

Boudins

In layman’s language this means that mineralisation is likely to occur in rope-like pipes that may be discontinuous (occurring in boudins). Boudins in French are blood sausages, and under certain conditions rocks can be deformed into what looks like a string of sausages when exposed at the surface.

The photograph (below) is a textbook example of boudinage. If the mineralisation at Kay Mine occurs in boudins, then it could be easy to overestimate the volume of mineralised rock unless care is taken to map out the zones of greater and lesser thickness.

Hinge and Flank are very different

A key feature of the geology at Kay Mine is intense folding. Folds have hinges and limbs (or flanks). As the mapping expert hired by Arizona Metals points out, hinge zones have good potential for grade x thickness; flank zones do not (NI 43-101, Technical Report, Kay Mine, page 36, paragraph 1).

It would be most helpful if the Company could, in words and pictures, show the ‘hinge zones’ and the ‘flank zones’.

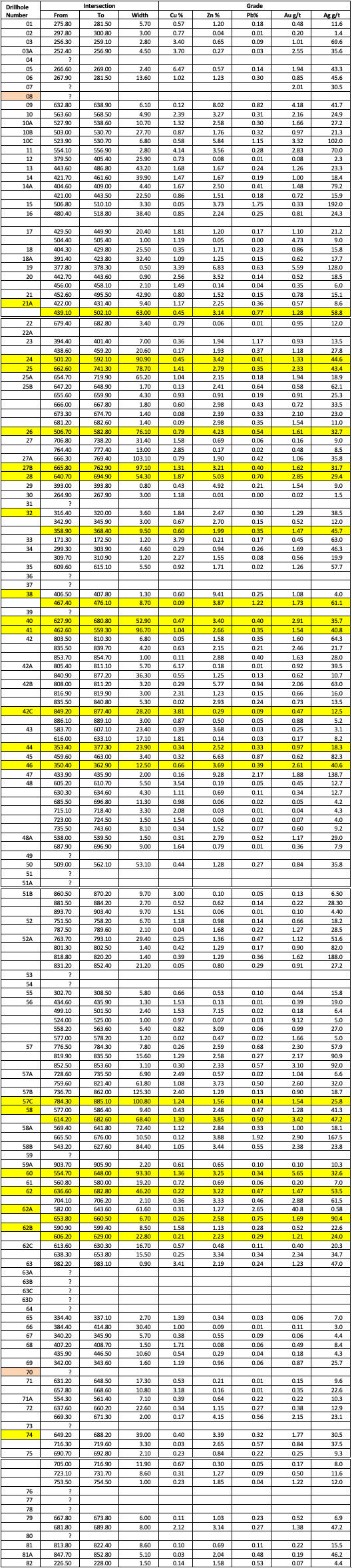

In fact, a review of the drillhole results confirms very large variations in mineralised widths. Crux Investor has performed spot checks on results of holes drilled away from the area with the best results.

There is often a sudden drop in intersection width, eg to 9.7 m in hole 22-51 B.

The best intersections occur in zones with narrow strike extent and which plunge steeply to the north. These observations tie up well with the concept of steeply dipping cigar-shape bodies. Curiously, the NI 43-101 describes them as having one orientation (229° - NI 43-101, Technical Report, Kay Mine, page 6, paragraph 4) but the images provided by Arizona Metals imply a different orientation (roughly north):

More information please!

Unreported Holes

Why do so many drillholes remain unreported despite having been assayed?

Did the 23 unreported full-length drillholes intersect flank zones, not hinge zones? Are the intersections thin, or low grade? Perhaps the intersections are both thin and low grade?

Given that bad news travels slowly (or is not released at all), the implication is that the unreported holes are bad news. The market needs to know. It would be most helpful if the Company could, provide drillhole data for all holes.

Projections are misleading

Why are there so many projected cross-sections, and so few actual cross-sections? Viewers of British television may know the brilliant logos for Channel 4 which only form a perfect "4" when viewed from the front. When viewed from any other angle, the individual components can be seen to be quite separate and in a different plane to every other component.

Here's a clip to illustrate this. The Technical Report talks about eighteen (18) discrete sulphide bodies (NI 43-101, Technical Report, Kay Mine, page 20, paragraph 3) and yet the Company shows just two main bodies (slide 13 of the Corporate Presentation).

Arizona Metals plots its drilling results on a single longitudinal section and on a composite cross section. These projections give the impression of an uninterrupted mineralised body 350 m across, 200 m thick, and with >800 m vertical extent.

Crux Investor feels that like the Channel 4 logo example, viewing Kay Mine mineralisation from the front is misleading. Projecting the thickest portion of the body onto a plane is not an accurate reflection of the average thickness of that body.

It is hard to reconcile the complexity of the geology as highlighted in the technical reports and seen in drill results with the simplicity of the geology as presented in publicly available material.

It would be most helpful if the Company could provide clarity on the data. An easy way to do this would be to show a series of close-spaced parallel cross-sections rather than projecting all cross-sections onto a single plane. More information please!

Drilling Problems

Arizona Metals evidently has trouble permitting new drill platforms. Plans show only three drill pads where drilling returned good results (slide 26 of the Corporate Presentation). This leads to inefficient drilling with hole azimuths not parallel to strike. And the deeper holes are increasingly oblique to mineralisation (NI 43-101, Technical Report, Kay Mine, page 26, Section 7 "Deposit Types").

The apparent problems in creating new drill pads will limit flexibility and increase cost, take longer, and potentially add errors to the data.

Mineralogically Challenging?

Mineralogy and metallurgy are other areas of concern. Kay Mine is a volcanogenic massive sulphide ("VMS") deposit which typically have a complex variety of mineralogical properties (NI 43-101, Technical Report, Kay Mine, page 26, Section 7 "Deposit Types").

This means that the metallurgy of VMS deposits is often very challenging. Metal recoveries can be low and concentrates can have levels of deleterious elements (e.g. As or Sb) that could make the product unmarketable, or result in penalties.

Obtaining a clean concentrate at good recoveries is far from a given. Much metallurgical testwork needs to be done on any VMS deposit. Will the rock upgrade to a clean concentrate at reasonable recoveries?

The consultants seem to think that Kay Mine mineralisation “should be amenable to conventional mineral processing” (NI 43-101, Technical Report, Kay Mine, page 22, paragraph 2).

As positive as the overall conclusion may be, proper metallurgical test work is required. The studies to date show that the typical grain size of the sulphide minerals is between 25 μm and 250 μm (NI 43-101, Technical Report, Kay Mine, page 23, paragraph 5), and that sphalerite and chalcopyrite are "interstitial to intergrown with pyrite" (NI 43-101, Technical Report, Kay Mine, page 23, paragraph 2).

The fact that the grain size is down to 25 μm and the minerals intimately intergrown suggests that at least fine grinding will be needed to achieve proper liberation.

No resources (yet)

Where is the resource estimate work for Kay Mine? There is no fresh resource at Kay Mine. Work in the 1970s estimated 5.8 Mt of mineral potential (NI 43-101, Technical Report, Kay Mine, page 12, paragraph 1). With the limited information available Crux Investor sees the possibility for 6 Mt of mineralised material.

Meanwhile, Arizona Metals is now moving on to drill the Central Zone west of Kay Mine. Perhaps the Company is feeling the laws of diminishing returns at Kay Mine?

The holes testing down-dip extensions of Kay Mine will clearly intercept the mineralisation at great depth and at increasingly oblique angles.

Valuation Mismatch

Consider the similarities and differences between Arizona Metals and Skeena Resources. Both companies are developing VMS deposits in north America, and the companies have similar market capitalisations, of C$479 M and C$456 M respectively.

This is where the similarities end. Arizona Metals has a lot of unanswered questions and no resource estimate. Skeena Resources has open pit reserves of 3.85 million ounces at 4.0 gt AuEq, a Feasibility Study hot off the press, and an estimated after tax NPV5 of C$1.4 billion.

Conclusion

Crux Investor would like Arizona Metals to provide sufficient information to enable investors to make an informed decision about the company. More information on geology, metallurgy, and economics please. Until then, Crux Investor would rather own Skeena Resources.

Cobre Limited Update

At the end of August Crux Investor published an Analyst’s Notes about Cobre Limited (“Cobre”). Cobre is exploring for copper in Botswana and the Analysts’s Notes report was positive about recent developments.

So positive in fact, that the Executive Summary concluded with the words “Crux Investor considers Cobre an attractive, albeit speculative, investment” and “One or more of the authors of this report own shares in Cobre Limited.” The share price at the time was 51c, and Cobre is currently trading at 13c.

The optimism was based on background data plus good-looking drill core backed up with decent X-ray Fluorescence (“XRF”) assays. To quote from the Analyst’s Notes, “Although no laboratory assays are yet available, hand-held…XRF…measurements taken…have given attractive results between 0.1 % Cu and 5% Cu over downhole sections of 59 m in NCP07, 25 m in hole NCP08, 15 m in NCP09 and 13 m in hole NCP10.”

XRF is a fantastic technology that is increasingly present in exploration camps and mine sites. XRF tools are easy to use, and results are available in almost real time anywhere. However, the results do not always match laboratory analyses, and this can cause problems - as Cobre discovered.

There can be a host of reasons for mismatches between XRF results and traditional quantitative techniques. The upshot is that Companies do not usually publish XRF data, preferring to use it for internal uses only.

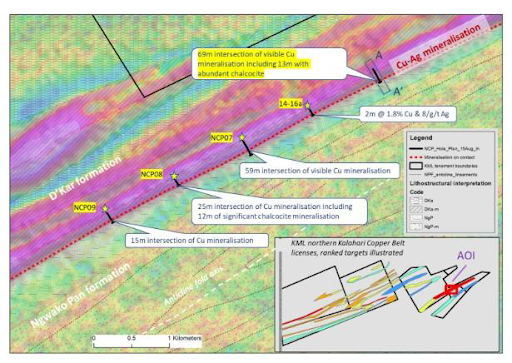

Consider the following two maps. Map 1 (below) was created using visual and XRF information, on 16 August 2022.

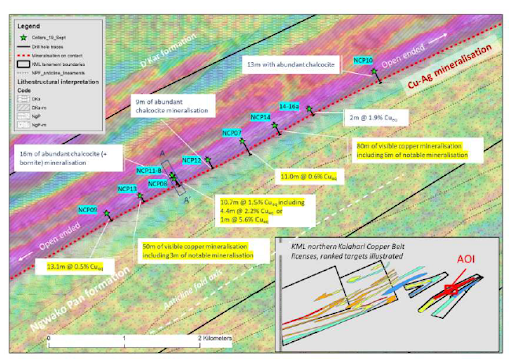

Map 2 (below) covers the same area but incorporates laboratory assay data for some drill holes and was published on 21 September 2022.

Note the comment in Map 1 at drill hole NCP08 that reports “25 m intersection of visual copper including 12 m of significant chalcocite”. When the assays were published this translated into 10.7 m @ 1.5% Cu equivalent, as shown in Map 2. Calibration has been improved. It now seems that “significant chalcocite” translates into about 1-1.5% copper equivalent. But investors will always need to see the full assay results to know for sure.

Cobre has faced the harsh consequence of poor expectation management. The share price has fallen from a high of 60c on 22 August to current levels of 13c. The hoary trading maxim runs “buy the rumour, sell the fact”.

Hopes were high, fuelled by photographs of core and good XRF data. The facts were less compelling. The market is unforgiving, and subsequent news (30 August) reporting “a broad 78 m zone of copper mineralisation which includes 16 m of abundant chalcocite (and bornite)” has not supported the share price in the aftermath of the assay results released on 21 September.

Overall, Cobre still has proof of concept for the exploration model, even if it is a long way from making a commercial discovery. There remains enormous potential within the project area given the hundreds of kilometres strike length with similar geology.

For market confidence in Cobre to return, the Company must deliver consistent good grades in assays, probably with decent widths of >1% copper. Laboratory assays for three holes were released on 21 September. Of these three, only one has an average grade of 1.3% Cu (and 18 g/t Ag) over the high-grade interval with the other two holes grading 0.4% Cu and 0.5% Cu.

The episode offers some key learnings:

- Laboratory assays are crucial. Wait for the assay data from accredited laboratories

- XRF is a brilliant tool for resource companies but has little place in public market releases

- Exploration success is all about consistency of good results. Resource discovery is a process, not a single point in time. The ‘discovery’ drill hole is usually only identified in retrospect.

If you are a Family Office investor, or an Institutional investor, and you would like the full report behind this article, please contact matthew@cruxinvestor.com

Analyst's Notes

Subscribe to Our Channel

Stay Informed