Analyst's Notes: How to Read Drill Results & Numbers to Watch Out for

This week, the Analysts have chosen to focus on understanding drill results, using 5 companies as examples, focusing more on what's NOT said than actually is said.

We are committed to helping investors come to grips with the resources sector and learn how to interpret news releases made by companies. In these Analyst’s Notes we illustrate how news from companies affects the investment case for the stock, and how it can affect peers as well. The topics are selected based on what the analysts think is both relevant and informative to you, the investor.

Before making comments, please ensure you have read the whole article and the FAQs at the bottom.

This week, we have chosen to focus on understanding drill results, using 5 companies as examples.

Reading Drill Result Announcements

When writing a News Release, publicly quoted companies are under a legal requirement to follow certain rules. On the TSX, for example, under the NI 43-101 Disclosure Rule, news releases reporting technical information have to be:

- Balanced and not misleading

- Understandable to a reasonably informed investor

- Consistent in its use of standardized terms and definitions

- Based on reasonable assumptions which are clearly explained

- Unbiased and identifies the potential risks and uncertainties

- Signed off by a professional (QP) who takes responsibility for the information

While that is all well and good, companies also go to great lengths to present the information in the best light. This means that the executive summary (the front page) will emphasise the positive, and highlight the good bits, while the less positive, or negative elements (included to give the whole picture) of a news release will be tucked away in the unglamorous nether regions towards the back.

There is an art and a craft about news releases, and messaging, which has spawned a whole industry - namely Public Relations and Investor Relations. Communication is a skill and it is entirely appropriate for highly technical companies in the resources sector to pay for consultants to help on their marketing strategy and communication plans, including news releases.

What this does mean, however, is that investors and analysts need to be versed in how to read these news releases. The Company will always want to control the narrative as best as possible, so that it fits in with a broad messaging plan that the Company will have drawn up.

It is not enough for readers to understand what IS being said, in today’s market investors and analysts need to be able to interpolate and interpret what IS NOT being said.

In this weeks Analyst's Notes, we have set out a number of aspects that should be given extra attention when reviewing drill results. You will see that this exercise today is particularly focused on what IS NOT being said. Examples that catch our attention are:

- Only highlights from selected drill intersections are given – and the omission is that not all the drill hole results above an informative cut-off point are included

- Gaps in the numbering of drillholes listed

- Cross sections for the best holes only

- Holes with poor results omitted from cross-sections

- Drilling hole(s) very close to a previous hole with very good intersection

- Projecting the strike extent of a shoot

- Not explaining when an intersection width is much wider than true width

- Smearing of short high-grade intercepts over much larger intersections

- Conversion of polymetallic grades in a grade equivalent using a low assumed metal price for metal equivalent, or ignoring relative off-mine costs

In the rest of this report we will have a look at case studies for most of the above examples where great care is required when interpreting drilling results in news releases. A few names will crop up in the following sections, but this is NOT a recommendation on the company as a whole. The examples chosen here are not necessarily the worst offenders nor a fatal flaw in an investment case, but they are to some extent Red Flags that we notice and we will continue to monitor. Indeed, we hope and expect that the Companies are themselves monitoring these challenges of what to omit and what to include, and that they are generally looking for ways to mitigate whatever risks the geology presents. It is also worth mentioning that the examples selected by us are also a function of convenience, as a limited number of press releases covered most of the points and made life easier for the analysts.

1. Presentation of Highlighted Results

In an effort to present the key news in a succinct summary on the front page, the best drill results are often included in a highlights table. This is fine, as long as the News Release goes on to provide a complete set of results, with information about the collar location, azimuth and dip of each hole for which results have been received.

2. Gaps in Drill hole Numbering

A good way for readers to verify that no holes have been left out is to check the numbering of the holes and whether, or not, there are gaps in the numbering. If there are, these could be the results of the company having had to abandon a hole because of drilling problems (but this should be specifically disclosed), or if the sample preparation and assaying was not done chronologically and results still outstanding. However, the ‘results outstanding’ reason should fall away after a few weeks.

Even a company as good with comprehensive reporting as Great Bear Resources Limited (“Great Bear”) (TSX:GBR), which has on its website a spreadsheet with all drillholes results and with re-drilled holes identifiable with the drillhole number + “A”, has some omissions for LP Fault zone drilling: for example holes 113, 114, 179, 195, 207, 214, 216 and 222. The hole numbers 224-239 without assays are probably still awaiting results.

Great Bear do a great job on communication and marketing, and it is commendable to include the drill hole database on the website. We would certainly like more companies to follow suit.

And it can be a subjective matter of opinion as to what constitutes material disclosure. The TSX describes “Material Information” as any information relating to the business and affairs of an Issuer that results in or would reasonably be expected to result in a significant change in the market price or value of any of the Issuer’s Listed Shares. Not only that, but it goes on to state that material information includes Exploration results & developments (Positive or Negative).

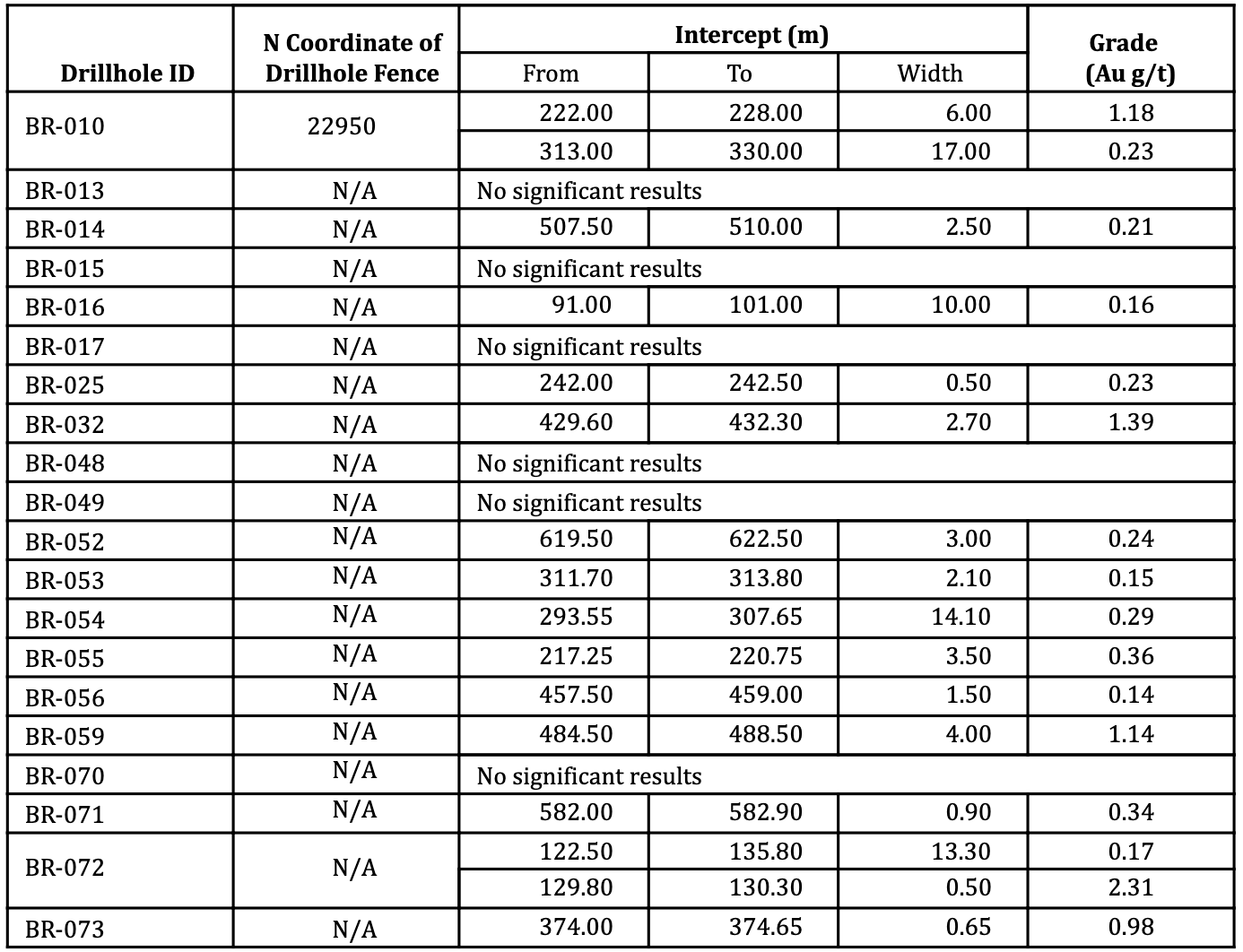

This leads us onto News Releases where some holes are omitted. Again using Great Bear data, which may seem a bit unfair because the company is so good at sharing information. It just makes it easier to see where there are omissions from news releases. Table 1 shows the holes drilled during the second half of 2019 at the LP Fault Zone and omitted from the press releases (3 Sep, 30 Sep, 10 Oct, 30 Oct, 16 Dec).

The table shows that all these holes had either very low grade or very short intersections, which in themselves is important. It is information that will colour expectations of continuity at the LP Fault zone and will be incorporated in any resource model. If the company is being transparent (a Good Thing), it would probably benefit it to be fully transparent to avoid misunderstanding along the way (a less Good Thing). To be clear, Great Bear did eventually provide the information, but not at the time in the News Release, which is where it would ideally have been included.

3. Providing Cross Sections for the Best Holes Only

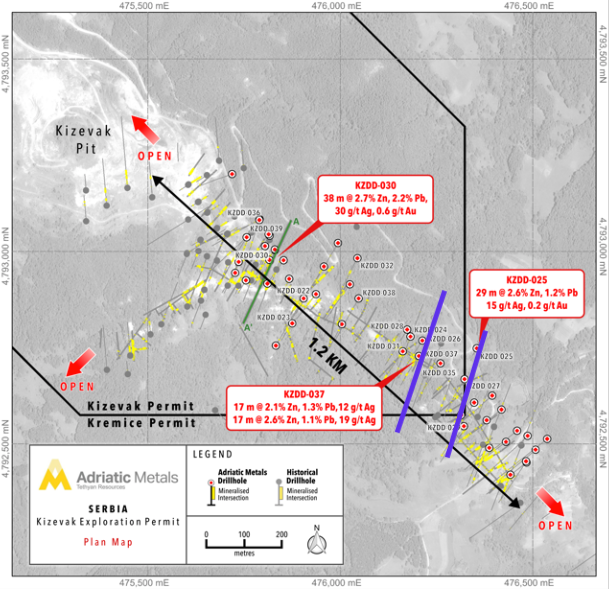

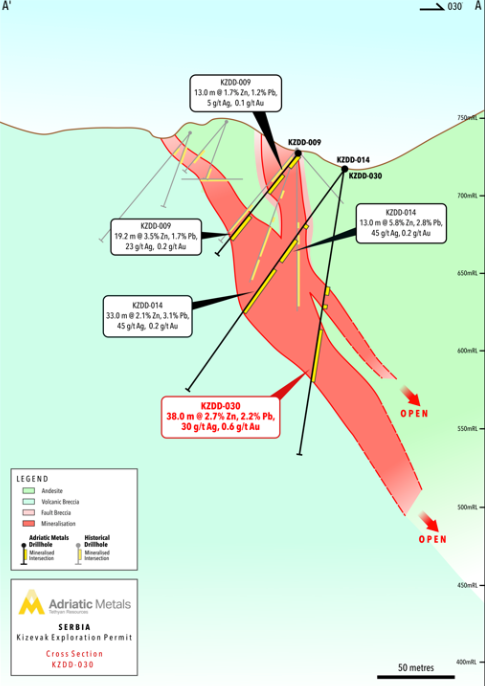

While it is tempting to show cross sections that include the best hole in a deposit, it is perhaps even more powerful when companies show restraint and show a cross-section that is truly representative of the ore-body. A recent example of a company indulging in an exuberant choice of cross section is Adriatic Metals Plc (Adriatic Metals) (ASX:ADT, AIM:ADT1, FSE:3FN) releasing results on 27 January 2021 for their Kizevak prospect in Serbia.

Figure 1 shows the drill collar location at the prospect with the results for holes 25, 30 and 37 highlighted. On the map there is a green trace for the cross section presented in the press release, reproduced in Figure 2.

The cross section published by Adriatic Metals illustrates that hole 30 is well supported by other holes along the cross-section trace. That is all well and good.

If you now go back to the map (Figure 1), we have drawn in purple the traces of two other hypothetical cross sections that Adriatic Metals could have provided to put holes 37 and 25 in context as well. If that had been done, however, hole 37 would have included hole 26 with individual intersections of around 5 m or less with grades of around 1% Zn, 0.5% Pb and less than 4 g/t Ag. The best intersection is 5.5 m @ 2.1% Zn, 1.2 % Pb and 14 g/t Ag.

The cross section for hole 25 would have included holes 27 (wide intervals of 20 m and 17 m with 1.1%-1.7% Zn, 0.4%-0.9% Pb and 5-10 g/t Ag, and hole 29 (no significant results). These additional cross sections would have presented a more complicated picture of the deposit than perhaps the Company wanted to share. Yes, we know that messaging is important, but in a good company such as Adriatic Metals (which has abundant geological potential), we feel that a more representative take of Kizevak would be the better way to go. We would rather companies trusted readers with the full picture, even if the front page of a news release only contains the simpler message.

4. Drilling Holes Very Close to a Previous Hole with Very Good Intersection

Geologists, project managers, and Company executives can all get caught in a position where good news is needed to ensure projects still get funded and grab the attention. What better way to grab the attention than by drilling well-mineralised holes? Of course, there are several valid reasons for wanting to drill closely-spaced holes, such as wanting to increase confidence in the resource base, or to understand structural control on the distribution of mineralisation. That is all well and good.

What does need to be avoided, however, is a tendency to keep coming back to the same spots when management need to plug a news gap. As an eagle-eyed investor you will want to understand why closed-space drilling is being done.

Nighthawk Gold Corporation (“Nighthawk”) (TSX:NHK), for example, has been exploring the Indin Lake property in Northwest Territories, Canada, since 2012. The property includes the Colomac project where historically 0.53 million ounces (“Moz”) gold has been mined at an average grade of 1.66 g/t.

In 2012 Nighthawk released its first mineral resource statement of 1.45 million ounces (“Moz”) gold in 42.6 million tonnes (“Mt”) at an average grade of 1.05 g/t Au. This increased in 2013 to 2.1 Moz Au in Inferred Resources. Since 2012 the company has spent C$86 million exploration, mostly drilling extension at depth. It has been hard going with the latest mineral resource statement dated July 2020 having 1.67 Moz in Indicated Mineral Resources at a grade of 2.01 g/t Au and 0.38 Moz in Inferred Resources at a grade of 2.03 g/t Au. The relatively high overall grade is due to inclusion of 1.46 Moz of underground resources at an average grade of 2.16 g/t Au. Good luck mining this grade economically underground. As mentioned above this upgrade in mineral resources has taken about eight years with a total cash outlay of C$86 million.

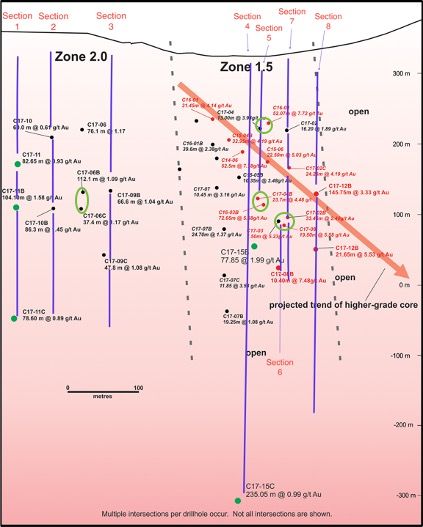

Given the obvious difficulties in finding exciting results the company seems to have found itself under pressure to maintain a flow of positive news in the form of good drilling results. As we know, the simplest route to good drill results is to drill preferentially close to previously known good results. Figure 3, which shows a longitudinal section along the strike of the Colomac deposit, illustrates this nicely.

The bar scale for the illustration shows that the total strike extent shown is 600 m. Within this strike extent there are two sections, Zone 1.5 and Zone 2.0 with collectively approximately 350 m strike extent and where all drilling took place. However, instead of testing the zones in a regular unbiased pattern with the dots (indicating the Drillhole pierce points through the deposit) at regular intervals, there are clusters of pierce points. We have indicated a number of these clusters by green circles or ovals.

The spacing of pierce points go down to approximately 10 m (e.g. C17-03 and C17-08). Again, this is not a fatal flaw in itself, it is simply a Red Flag that investors should want to understand? Why are those holes being drilled so close? There may be a perfectly good reason, or it may be because the project is, well, flagging a bit.

5. Projecting the Strike Extent of Grade Shells, and Mineralising Zones

Another difficulty can arise when shells are generated with computer software, which look impressive and resemble the margins of a defined resource, but are not actually resource grade shells. A couple of diagrams from Great Bear illustrate this nicely. The Isometric view of the Dixie Limb and the Hinge Zones show, for example, the Hinge Zone to be approximately 300 m long. The second diagram, zooming in a bit, shows that the mineralised zone is comprised of much smaller plunging shoots, probably no more than 50 m across. The mineralisation shading look like grade shells of defined Inferred resources, but they are not Inferred resource grade shells.

The geology of Dixie Limb and the Hinge Zones is highly complex, and we are always keen to see resource models, grades and tonnes before getting too carried away with continuity and projecting zones of mineralisation. As the Recommendations section of Great Bear’s technical report on the Dixie project state,

"the primary focus … is to determine and establish strike extents, depth potential, and controls to high grade mineralization”

and...

“Great Bear should consider contracting an experienced resource modeler who could provide guidance on the drill spacing that will be required in order to evaluate the Property’s total gold potential.”

and...

“The continued development of the geological model of the zones as well as continued development of the geological map are considered highly important to the project’s growth.”

Which we interpret as saying, keep drilling, keep trying to understand the geology, and when possible put a resource model together (but you’re not there yet). And we also feel that the diagrams that Great Bear publishes do not help readers understand the complexity of the controls on mineralisation at Dixie. In short, the diagrams show greater continuity than has been properly established, which we see as a Red Flag and something to be monitored.

Figures 4 and 5 are an isometric presentation of drill results at the Dixie Limb and Hinge Zones of the Dixie project of Great Bear.

6. Mineralised Intercepts Much Longer than True Width

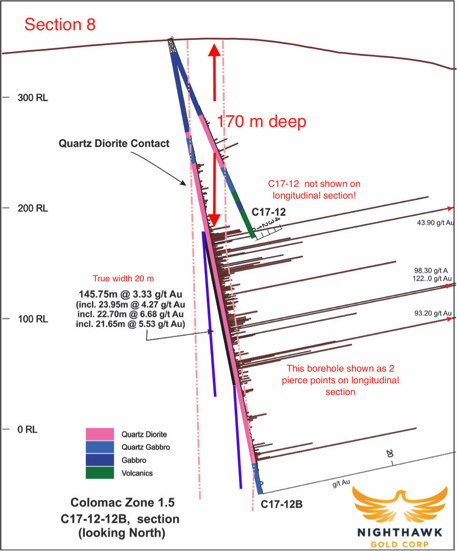

Companies do need to take care when publishing intersections where drilling is sub-parallel to structure or mineralisation. It is unfair to put the onus on the reader who will always be at a knowledge disadvantage to the author of a news release. To illustrate this point we return to the drill results provided by Nighthawk. Figure 6 shows Cross Section 8 at Colomac, the location of which is shown in Figure 3.

The following is apparent from this section:

- The impressive intercept of almost 146 m at 3.33 g/t Au is a lot less impressive when its true width of approximately 20 m is taken into consideration.

- Nighthawk has collared close to the target horizon and with a steep angle sub-parallel to the dip, resulting in a very oblique interception angle. The company’s statement in its new releases that intersections are “close to perpendicular therefore true widths are approximately 80% of core lengths” is therefore surprising, to put it mildly.

- Results of Drillhole C17-12 close off the mineralisation upwards, indicating that the depth to the top of the deposit here is 170 m deep. Any mining by open pit means would require a very high strip ratio.

7. Smearing of Short High-Grade Intercepts

Dealing with gold in drill results is always difficult, and especially so with high-grade gold. The well-established method is to apply a top-cut to the anomalously high grades found in narrow structures, so that the single (unpredictable, higher grade) intersection does not have undue influence over a wider, lower grade intersection. The reason is to avoid ascribing a too-high grade to a too-large block, and therefore skewing the overall tenor of a resource.

When companies do not apply a stringent top-cut to grade, and instead average out high grades from narrow intercepts, then this is called smearing. It is easily done, but that does not mean that it is good practice. Smearing projects to the reader that the tested target has a continuity and consistency that is not really there.

Figure 7 are enlargements of parts of certain cross sections through the silver block model of the Silver Sand project of New Pacific Metals included in the NI 43-101 report for the Mineral Resources estimation.

Note that the high-grade blocks (in red) are defined by smearing the short, high grade intersections (in red) along the Drillhole trace. Note also that high grade intersections in one drill hole have been carried all the way across to the adjacent Drillhole despite no such high-grade intersections being present in the other drill hole.

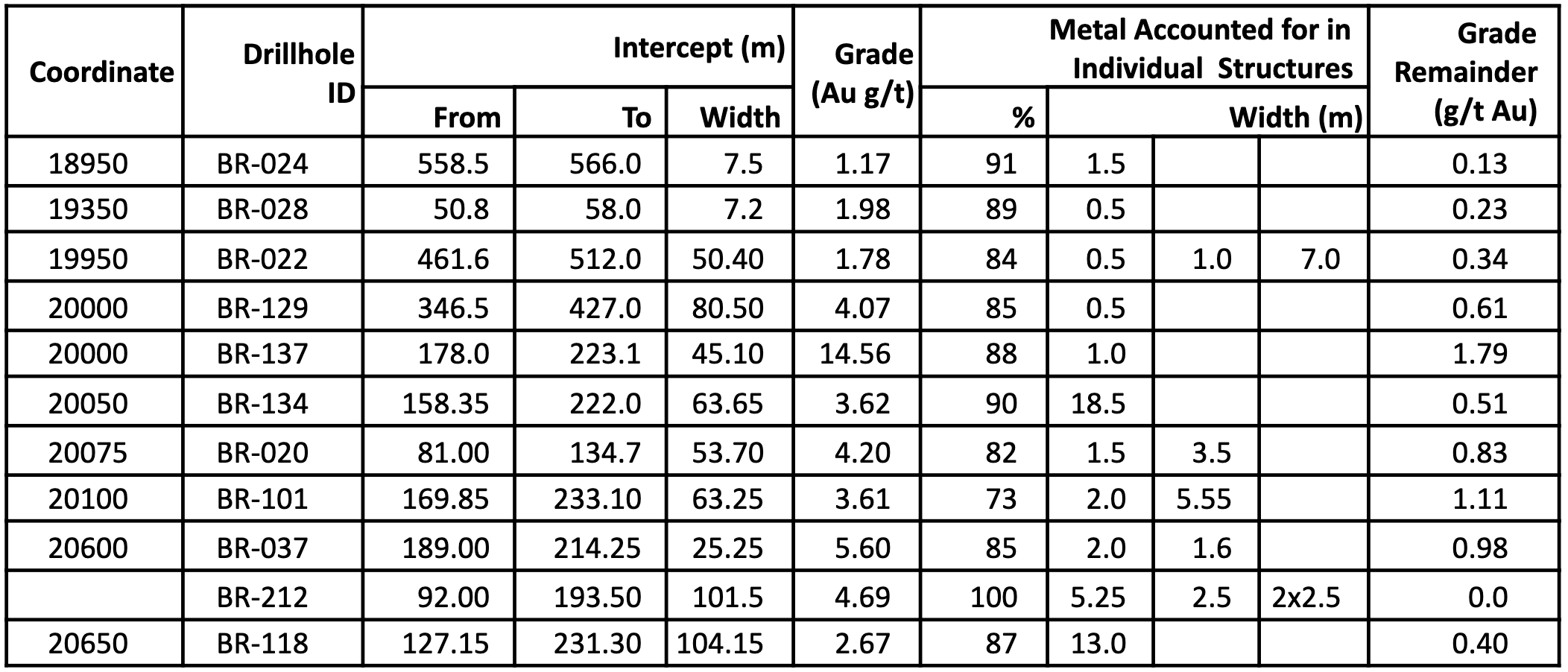

We repeat that the treatment of gold across narrow structures in drill results requires a great deal of discipline in how it is reported and communicated. We are not expecting perfection from every company, but if the geology is complex, then we do expect a full discussion on the subject from the reporting Company. Returning to Great Bear, have a look at the Drillhole results in Table 2 below for the LP Zone for drill fence coordinates up to 20650N. Note that these are not especially high grades.

The table shows that the grade of the remainder of the intersections can sometimes be so low that it would struggle to pay for its processing cost alone. Smearing of gold grades across wider intersections is definitely a Red Flag that needs monitoring, as it can affect the entire resource model.

8. Conversion of Polymetallic Grade in Grade Equivalent

Reporting the grade equivalent grades of polymetallic deposits is fraught with difficulty. The challenge is to incorporate a number of factors, where the data may not yet be available. Again, much of this can be navigated with clear explanation of methodology. Improvements are, however, expected over time as various ‘modifying factors’ of economic extraction are applied to the calculations. For example, in the first report, the grade equivalent figure for a drill result may just be an arithmetic calculation.

By the time a properly constrained resource is established, however, much more will be known about metallurgical recoveries, and potential smelter charges and penalties, so that the company in question will have a better understanding of what the payable metal of an intercept may be.

To illustrate this point, we refer to Discovery Metals Corporation (“Discovery Metals”) (OTCQX:DSVMF) (TSX:DSV). The main deposit, Cordero, is a silver deposit, with other associated metals and in drill releases the company notes underneath the intercept table that “AgEq calculations for reported drill results are based on USD $16.50/oz Ag, $1,350/oz Au, $0.85/lb Pb, $1.00/lb Zn. The calculations assume 100% metallurgical recovery and are indicative of gross in-situ metal value at the indicated metal prices.,”

Interestingly when it comes to how the AgEq calculations are done in the resource itself, Discovery Metals does publish a lot of information on recovery, and treatment charges. This is important because the metallurgical losses, will be particularly high for gold (60%), and high for Pb (16%) and Zn (28%). Ignoring the treatment charges that are incurred for treating lead and zinc concentrates in which the silver and the gold occur is important because the charges severely reduces the value contributions of these metals. Interestingly, for the PEA and the resource calculations that contributed to the PEA, Discovery Metals (or their consultants) used a very conservative AgEq approach, including all real-world costs. For the subsequent News Releases, however, Discovery Metals has used a far less rigorous (conservative) approach to arrive at a AgEq grade that is very flattering and not particularly useful. Red Flag alert!

Finally, by applying a low silver price of US$16.5/oz, Discovery Metals increases the relative importance of the by-products expressed in silver equivalent with the reader then bound to apply the spot silver price to the total quoted, thereby overestimating the attractiveness of the numbers in Drill Results news releases. When the real world recoveries, realisation costs, and metal prices outlined in the Discovery Metals PEA are applied, the average silver-equivalent grades are considerably lower than the figures that Discovery Metals uses in drill results.

What to do next

Eager for more Analyst content, or looking for consistent returns for more confident investing?

That's where we come in. Crux Investor is an investing app for busy people.

You’ll receive a single stock recommendation each month, curated by industry experts and presented in a clear and focused one-page memo. You’ll also receive access to a platform full of programmes that will allow you to grow your financial knowledge, overall, all at your own pace.

Crux Investor is for anyone interested in saving time while investing with confidence. It's an ideal resource for the novice that needs guidance and is tired of throwing money away with guesses and gambles. But it's also a perfect fit for the experienced investor that wants a faster and more efficient way to arrive at the perfect stock or significantly increase their knowledge.

Finally, you can afford the analysts the big funds use. No more gambling, no more guesswork. Instead, save time, slay stress, and start investing with confidence by joining Crux Investor today.

If you are a Family Office investor, or an Institutional investor, and you would like the full report behind this article, please contact matthew@cruxinvestor.com

Analyst's Notes

Subscribe to Our Channel

Stay Informed