Copper All-Time High: Will Nickel Beat its 2007 Skyrocket?

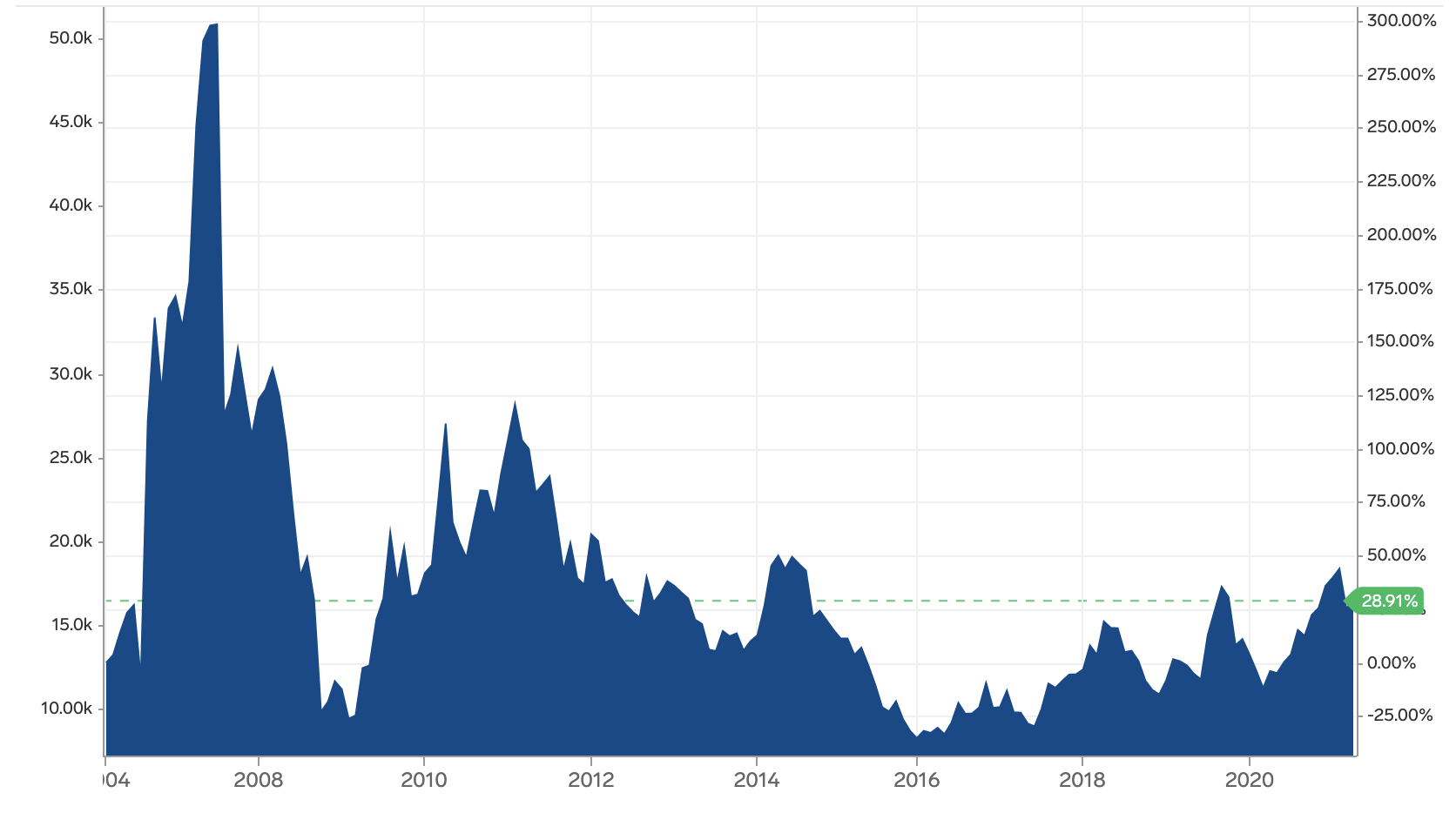

The Copper price has reached an all-time high; and with the increasing demand for physical high-purity metals, experts are hoping that Nickel is slowly creeping up towards its 2007 price of $50000 per tonne.

The Copper price has reached an all-time high; and with the increasing demand for physical high-purity metals, experts are hoping that Nickel is slowly creeping up towards its 2007 price of $50000 per tonne.

A couple of days ago Nickel got back through $8/lb. We had the big Xinjiang drubbing, now 2-months ago, but prices have now gone back up through about $8.10/lb - $8.15/lb. Getting closer to $18,000/t driven by concerns about inflation.

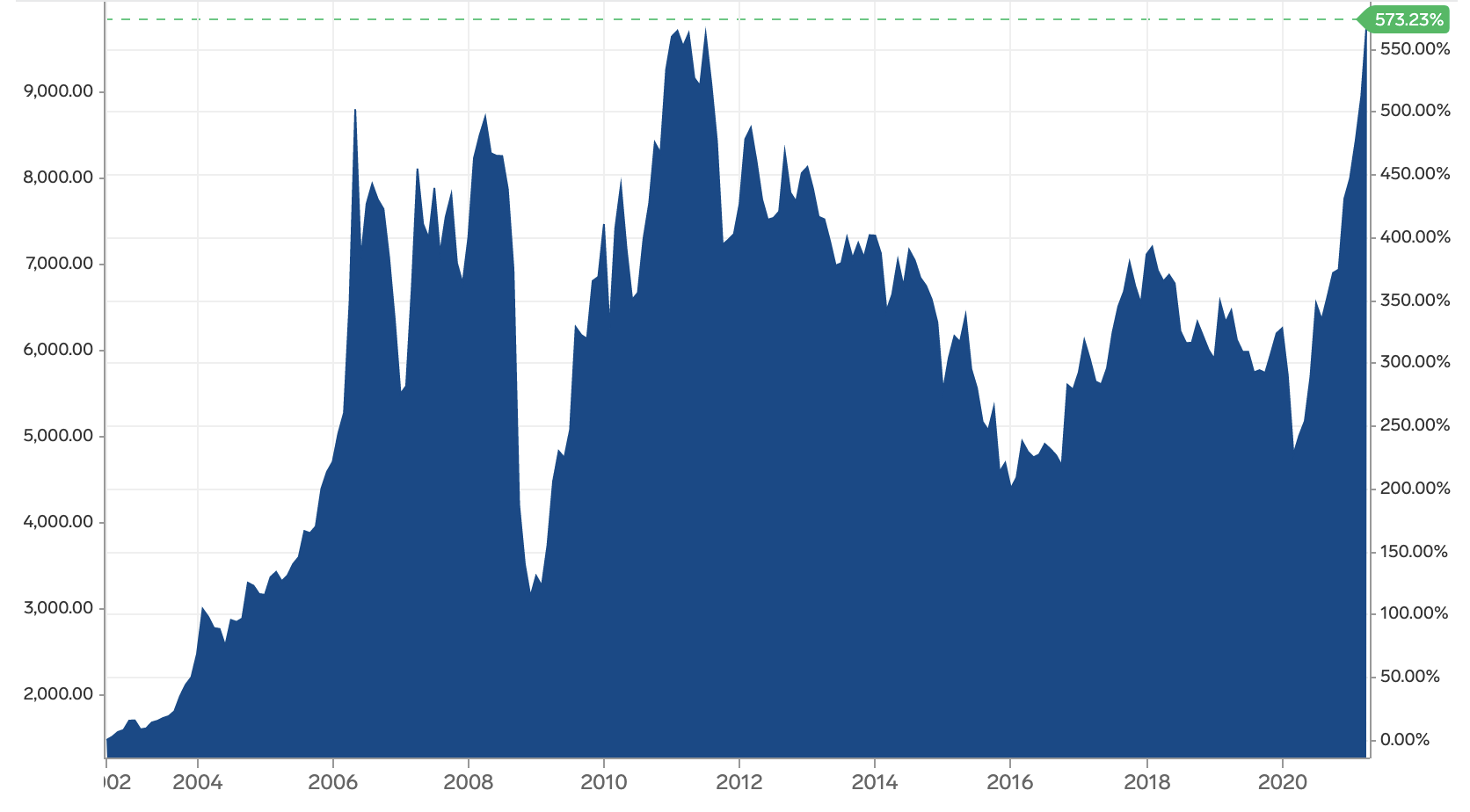

The Copper price too is ripping. Copper is back up over $10,000/t or $4.50/lb, and getting within a few cents of the all-time high for Copper. There are industry players saying it’s going to happen in the next 12-months.

Physical Nickel Demand

Talking to industry players about physical Nickel, it seems the demand is there. They are cleaning out the inventories of the high-purity metal that they had at the end of last year. Product is flowing, and one of the good ways that the physical side of the business gets some sense of where the real demand is, a lot of contracts will have a range.

There’s a minimum and maximum volume that they can take. A lot more people are taking closer to the max volume than the average.

It’s a good sign from the physical side, and we’re seeing some pretty decent physical demand from the battery side of the business. People are looking for briquettes to dissolve, but there are not many of those to be had.

Yellen Not Concerned About Inflation… Yet

There is a tipping point in every economic rebound where opinion becomes a little bipolar. We’re seeing tremendous growth, which is going to be great for profitability and stock market’s highs. And that growth and profitability is going to push the market higher.

However, you also get the flip side of it where it can create inflationary pressures, interest rates need to rise. And if interest rates rise, the market is going to tank.

We’re in this seesaw battle right now where we’ll see the seesawing for the next 3 or 4-months at least until we see a clear narrative that say either, ‘yes, we can get this big bump in growth and profitability without a lot of inflationary pressures’; or ‘oh no, we are actually seeing inflation spill out into a broader part of the investor base and interest rates are going to have to start to move higher from close to 0 in most markets’.

Yellen, who has been fairly dovish through most of her central banking career, was hinting that there are some inflationary risks lurking around that gave the market a kick in the teeth in the early part of last week.

So, look out for this seesaw battle back and forth for the next few months, and make decisions about your investment portfolio and cash position accordingly.

Will production actually happen?

Given these market uncertainties, you need to ask yourself whether the companies that you are invested in are capable of getting into production or is it just a momentum play.

If the latter, you need to have a view about when you start taking your profits off the table and start moving them into fundamental plays ie: companies that have a genuine chance of actually getting into production.

You need to be honest with yourself when answering this question. As the old investing adage goes, when the tide goes out, you don’t want to be naked...

China Flexing Their Muscles

A big piece of news out of China is that in the past week is the government has removed some tax rebates on Steel products. That sounds a little esoteric for some people, but it is pretty important. It signals a couple of key things.

- They’re trying to dampen demand for Iron Ore because now Steelmakers and Stainless-Steel makers can’t export a bunch of their products out of the country. They’re going to be less likely to buy that marginal tonne of Iron Ore and continue to push prices higher.

- This is the second major move downstream, where the Chinese made their first big move about 10 or 12-years ago, is that they not only eliminated the tax rebate but also put export duties on various products.

What the Chinese don’t want to happen is they bring in raw material, use up a lot of air and water to create a lot of pollution, and then export that to a third country that has the benefit of using that downstream product.

This elimination of the tax rebate means we’re going to see a lot less Chinese exports of various Steel products and various Stainless-Steel products, which should mean you see a bigger demand pop from the rest of the world as they fill the gap, by those exports pulling back.

How important is the Carbon footprint?

It also helps the argument against a class 1 versus class 2 narrative. The bigger question going forward will be, is China or India willing to have higher levels of pollution versus Western world supply chain, with less tolerance of Carbon environmental footprint of the materials that are being used.

Chinese company Lygend started trial production in Indonesia. These are the first wave of the HPAL projects. Back in 2018 when Xinjiang talked the market down the first time. It was about how they were going to have 150,000t - 200,000t of HPAL projects online by now and then with the capacity to do many more, and they were going to do it with half the capital cost of how Western companies could do it. The reality is that they’re all about 1 to 1.5-years late.

The tricky part with HPAL projects isn’t necessarily getting them started, although that tends to take longer and more money. It’s actually getting up to capacity. It’s good that Lygend got this far. We’ll see how quickly they climb up the ramp-up curve.

Past Chinese experience in PNG with Ramu which took 4 or 5-years for CMCC to ramp up. It is a place where they basically built a little Chinese beachhead on the north shore of PNG and even in that environment, it still took them 4 to 5-years to get up to current capacity. That’s going to be the next hurdle that these plants are going to have to get past.

Retread Projects v The Real Deal

With Nickel now a favoured metal, it’s not surprising we’re starting to see a bunch of new stories pop up where people are talking about how they’ve picked up a new property, started doing geophysics, and have some really exciting anomalies and will be drilling soon. Thus it has ever been, so let’s make sure we don’t get caught out.

Things to look for include: have these people ever actually discovered anything in their past or have they just run companies that haven’t really delivered anything and sucked cash out of the shareholders’ pockets?

You’re going to get some of those guys there.

Also, they will spin that property as new and you’ll have to read into the detail to see if it has actually been explored 3 or 4 times and if they’re just looking at it for the fifth time, and this time hopefully it’ll be fifth time lucky, they’re going to find some Nickel other than one of the other companies.

That does happen.

I shouldn’t say that we should automatically dismiss it, but unless they have a really new angle or a new piece of technology. For instance, if it was last explored in the 1970s and they think there are some EM targets at depth, that’s a technology that’s advanced pretty dramatically but if they looked at it 7-years ago, that’s a little trickier.

The other key piece is, look at the pace at which they’re advancing it. If the company is really confident about what they have then they’re going to move aggressively to push it.

Broader Market Activity

Ardea

Has a big Aussie Laterite project, but they’ve also picked up a Sulphide project. Assays, like in many parts of the world, are slow getting out so lots of people are putting out more of a description of the mineralisation as opposed to actual assays. 'It was narrow'. 'It was a couple of metres but a chunk of it was semi to massive Sulphide, which generally should show +1% Nickel'.

If you get a hole in a new target that’s got any kind of semi-massive to massive Sulphides in, that’s always a good sign. The next question is how thick is it and over what extent are they able to drill it off? But that first hole with a little bit of higher grade in there is always good.

Bitterroot

Is a company exploring in Michigan, where the Lundin’s Eagle Mine is. It was narrow, a fraction of a metre, but they did get a piece that was 2.7% Nickel, so it looks like it’s got the potential to have some higher grade.

Obviously, it needs to be much thicker than that to make it work, but the system itself can generate those kinds of Nickel grades.

Legend Mining

Has done some decent step-outs on a target. They have worked the south and north end of a structure with some distance in between the area they’d been drilling before. Some of their other drilling had been relatively narrow step-outs and these are pretty courageous step-outs relative to the drilling they’ve done before.

These look good as they’ve got several metres of semi-massive to massive Sulphide in both holes so assays pending on that front, but it’s good to see some lateral extent that’s there.

Palladium One

Has hit a zone near Thunder Bay, a new discovery with some nice high-grade intervals from the first set of holes. In terms of drilling, this was well spaced.

They drilled 14 holes over a good strike length on the target. 11 of them hit massive or semi-massive Sulphides, so pending assays, they gave some pictures of the core and not huge widths but very good grades. We’ll see how they continue to develop that.

Talon Resources

Has put out some more results. They’ve got multiple targets they’re working on now. Some good, lower-grade intervals over 30m - 40m of width containing anywhere from 2m - 5m of multi percent, 3% - 5% Nickel, which is good to see, with associated Copper and Cobalt.

We are starting to see some good exploration results from some junior companies and a pipeline of new Nickel targets and anomalies.

What to do next

Eager for more Mark Selby content, or looking for consistent returns for more confident investing?

That's where we come in. Crux Investor is an investing app for busy people.

You’ll receive a single stock recommendation each month, curated by industry experts and presented in a clear and focused one-page memo. You’ll also receive access to a platform full of programmes that will allow you to grow your financial knowledge, overall, all at your own pace.

Crux Investor is for anyone interested in saving time while investing with confidence. It's an ideal resource for the novice that needs guidance and is tired of throwing money away with guesses and gambles. But it's also a perfect fit for the experienced investor that wants a faster and more efficient way to arrive at the perfect stock or significantly increase their knowledge.

Finally, you can afford the analysts the big funds use. No more gambling, no more guesswork. Instead, save time, slay stress, and start investing with confidence by joining Crux Investor today.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed