Marimaca's Strategic Position Strengthens as Mercuria's Copper Grab Exposes Supply Fragility

Mercuria's 40,000-tonne copper withdrawal drove record $11,540/t prices. Marimaca Copper's permitted Chilean project offers validated economics and near-term supply potential.

- Mercuria's withdrawal of more than 40,000 tonnes of copper from LME warehouses on December 2 triggered a record price of $11,540/t, reinforcing structural supply tightness.

- Supply disruptions in Chile and Indonesia expose vulnerabilities that elevate the strategic value of new, near-term Chilean copper projects with environmental approval and validated economics.

- Marimaca Copper's Marimaca Oxide Deposit (MOD) is an advanced-stage Chilean project with a completed DFS (August 25, 2025) and environmental approval (RCA received November 2025), positioned to address market requirements for reliable new supply.

- At copper prices materially above DFS assumptions, Marimaca's project economics expand significantly, from a post-tax NPV8% of US$709M at $4.30/lb to US$1.1B at $5.05/lb, with a 39% IRR.

- The combination of global supply anxiety, premium copper pricing, and Marimaca's validated technical profile positions the project as a potential beneficiary of sustained market tightness and capital rotation into scalable, near-term copper developers.

A Copper Market on Edge & Why It Matters for Project Developers

The global copper market entered a state of heightened physical tightness following Mercuria Energy Group's large-scale withdrawal of more than 40,000 tonnes from London Metal Exchange warehouses on December 2. The move, executed through delivery cancellations to South Korea and Taiwan, coincided with a copper price spike to $11,540/t, the highest level in LME history. The withdrawal occurred against a backdrop of mine disruptions across Chile and Indonesia, amplifying concerns about near-term supply reliability.

This market configuration creates a strategic premium on de-risked development projects. When physical copper is removed from accessible inventories at scale, the implied signal is clear: traders anticipate sustained supply deficits that current production cannot adequately address. For project developers, this translates into higher incentive pricing, expanded financing windows, and increased buyer competition for new supply.

Marimaca Copper, advancing the Marimaca Oxide Deposit in Chile's Antofagasta region, represents a case study in how advanced-stage developers benefit from this environment. The project has received environmental approval (RCA in November 2025), completed a definitive feasibility study (August 25, 2025), and is targeting final investment decision in H2 2026, subject to completion of financing. Hayden Locke, President and Chief Executive Officer of Marimaca Copper, frames the resource growth opportunity:

"The first is that oxide intersection which was nearly 50 meters at 2% in a broader zone of 160 meters at 1%. That is a material extension to the oxide envelope and certainly higher grade than what our current interpretation of the block model is."

Mercuria's Copper Withdrawal & What It Signals About Market Structure

Mercuria's actions in the copper market reflected physical market dynamics rather than speculative positioning. The company cancelled more than 40,000 tonnes of LME copper for delivery on December 2, triggering immediate price volatility and a widening cash-to-three-month spread that reached $88/t on December 4, the highest since October 13. This backwardation structure signals looming shortages and creates conditions for potential short squeezes as inventories are physically removed from accessible locations.

The copper price spike to $11,540/t represents the highest level in LME recorded history. The move was driven by fundamental concerns about supply reliability as LME warehouse inventories declined and material destined for Asian markets was withdrawn. This configuration often precedes extended periods of elevated pricing, particularly when mine supply remains constrained by operational disruptions or underinvestment in new capacity.

Chile's role as a major copper producer means any operational shock within Chilean production is magnified through price-setting mechanisms. Recent disruptions, including labor negotiations, water access challenges, and permitting complexities, have reinforced investor sensitivity to Chilean supply volatility. This dynamic creates a premium on development-stage assets that offer supply predictability, environmental approval certainty, and proximity to established infrastructure.

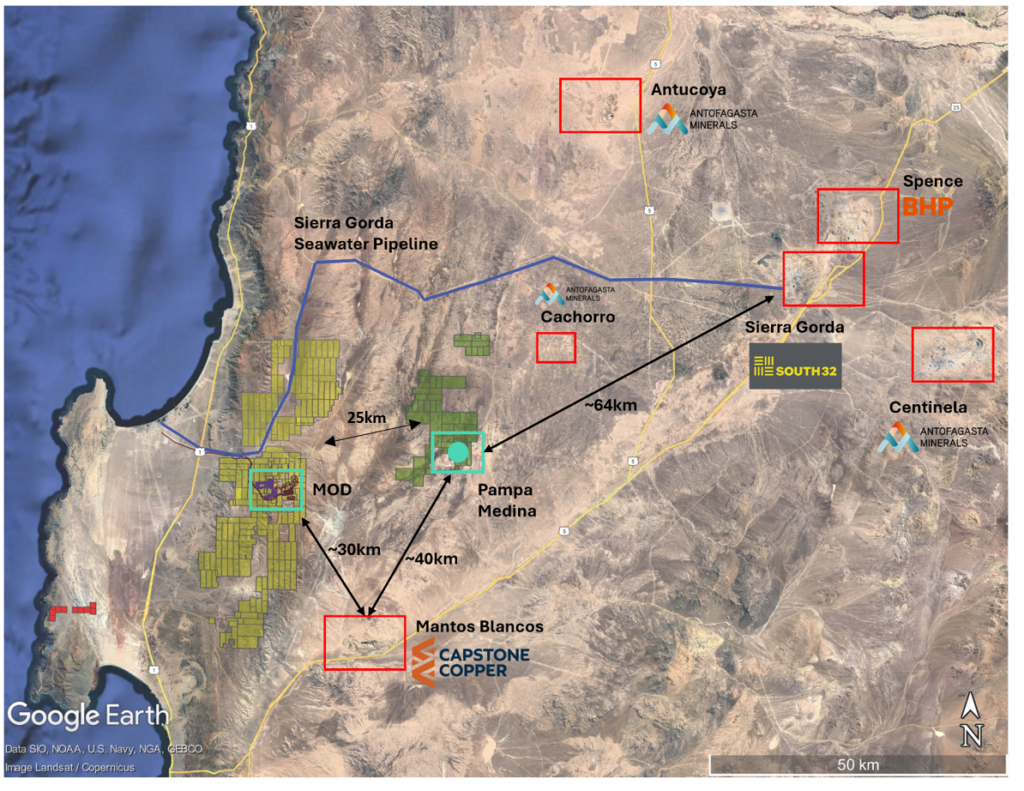

Chilean development-stage projects with completed feasibility studies and environmental permits are increasingly viewed as strategic hedges against supply disruptions at incumbent producers. Marimaca's position is reinforced by its location in the Antofagasta region, 25 kilometers from the Port of Mejillones, where proximity to port facilities, regional electrical infrastructure, and mining services reduces execution risk relative to greenfield projects in less-developed jurisdictions.

Chile's Supply Instability & the Emerging Premium on Low-Risk Development Projects

The copper market's response to Mercuria's withdrawal reflects a broader shift in how institutional investors evaluate copper exposure. Physical tightness accelerates capital flows toward projects that can deliver scalable production within defined timelines, disproportionately benefiting developers with completed feasibility studies, environmental approvals, and validated economics.

Chile is characterized as a Tier-1 mining jurisdiction, supported by decades of investment and regulatory frameworks. However, recent operational disruptions at Chilean copper operations have exposed vulnerabilities in global supply chains. Investors are increasingly differentiating between high-execution-risk jurisdictions and projects within established mining jurisdictions that offer permitting certainty.

Cost inflation typically slows development by eroding project economics. However, extreme price strength can accelerate financing interest by improving project returns and shortening payback periods. Projects with environmental approvals and completed feasibility studies become financeable candidates more rapidly in tight markets, as capital allocators seek exposure to copper scarcity through assets with permitting certainty, low technical complexity, and clear timelines to first cathode.

Marimaca's position is strengthened by its shareholder structure, which includes Greenstone Resources (21.6%), Assore Limited (18.9%), Ithaki Limited (13.6%), and Mitsubishi Corporation (3.9%), institutional investors with track records in mine financing. The company held zero debt and US$78.7 million cash as of September 30, 2025. Hayden Locke addresses the company's execution focus:

"My focus is now on when we go into the execution phase, who's going to lead that for us, what's our contracting strategy, who are we going to partner with."

Marimaca as a Case Study in De-Risked Chilean Development

Marimaca Copper's Marimaca Oxide Deposit represents an advanced-stage Chilean project positioned to benefit from sustained copper market tightness. The project's technical profile, environmental approval status, and validated economics differentiate it from earlier-stage exploration assets.

MOD is located in Chile's Antofagasta region, 25 kilometers from Mejillones. The project benefits from proximity to port facilities, regional electrical infrastructure (with planned power spur and line utilizing certified renewable electricity supply), and mining services availability. The project's RCA approval, Chile's comprehensive environmental authorization received in November 2025, substantially addresses a permitting barrier that has historically delayed Chilean developments.

The DFS, completed August 25, 2025, provides cost certainty and metallurgy confirmation. The project features a low strip ratio of 0.8:1, reducing waste movement requirements. The conventional heap leach and solvent extraction-electrowinning circuit produces Grade A copper cathode, avoiding concentrator complexity and smelting requirements. The project's Mineral Reserve stands at 178.6 million tonnes at 0.42% total copper for 748,000 tonnes of contained copper, supporting a 13-year mine life at steady-state production averaging 48,000 tonnes per annum of copper cathode.

Marimaca's environmental profile includes estimated 38% lower emissions intensity relative to traditional processing methods, recycled seawater supply secured from the Bay of Mejillones, and no use of continental or fresh water. Resource definition drilling remains ongoing at Pampa Oxide through Q3 2026. Hayden Locke emphasizes the exploration potential:

"We're now forming a view that it's going to be significantly more than that. It's really a complementary story first which is how do we go from 50,000 tons of cathode to 70,000 or more for an extended period of time."

The DFS delivered a post-tax NPV8% of US$709 million and an internal rate of return of 31% at $4.30/lb copper. At $5.05/lb copper, the NPV8% expands to US$1.1 billion with a 39% IRR and 2.2-year payback. The record LME copper price of $11,540/t ($5.23/lb) far exceeds both assumptions. Capital intensity of US$11,700 per tonne of annual production capacity positions MOD favorably relative to North and South American peers.

How Mercuria's Market Move Could Influence Marimaca's Financing Timeline

Mercuria's withdrawal signals expectations of sustained supply tightness, accelerating institutional interest in developers with clear pathways to production. Marimaca's position as a Chilean developer with environmental approval and a credible pathway toward FID in H2 2026 (subject to financing completion) aligns with this shift.

Institutional investors evaluating copper exposure increasingly prioritize projects with permitting certainty, validated economics, and modest capital requirements. Marimaca's financial position as of September 30, 2025, zero debt and US$78.7 million cash, provides a foundation for financing discussions. The company's shareholder structure, including Greenstone Resources, Assore Limited, Ithaki Limited, and Mitsubishi Corporation, reinforces credibility for capital syndication. However, there is no certainty that Marimaca will be able to raise funding when required, and any capital raising may result in dilution or other effects on share value.

Elevated copper price structures improve project returns and ease dilution risk. Marimaca's project economics at current copper prices support a range of financing structures, including streaming arrangements, offtake-linked prepayments, and strategic equity from industrial buyers seeking copper supply security. The company's financing process extends through Q3 2026 according to publicly disclosed work programs.

Comparative Positioning & Why Marimaca Screens Differently

Marimaca's capital intensity of US$11,700 per tonne of annual production capacity is positioned favorably relative to many North and South American peers. This cost structure reflects the project's low strip ratio, conventional heap leach processing, and proximity to infrastructure. Projects with lower capital intensity benefit in cost inflation environments, as their financing requirements remain manageable relative to project returns.

Marimaca's recycled seawater strategy addresses water access constraints that have affected other Chilean operations. The project's copper cathode production, with no smelting requirement, lowers emissions exposure. Ongoing drilling at Pampa Oxide provides resource expansion potential. The exploration program targets oxide extensions that could expand MOD's production profile beyond initial DFS assumptions.

The Investment Thesis for Marimaca Copper

- Structural supply deficits are intensifying as Mercuria's copper withdrawal underscores tightening inventories and reinforces long-term deficit models by CRU, Wood Mackenzie, and the International Copper Study Group.

- Jurisdictions with established mining frameworks and projects demonstrating advanced permitting status may attract disproportionate capital allocation as investors seek supply predictability.

- Low-capex, low-complexity projects benefit from price volatility as MOD's cost structure and heap-leach flow sheet provide leverage with manageable execution risk.

- Environmental approvals and infrastructure proximity materially reduce development timelines as Marimaca's RCA and location near Antofagasta increase financeability compared to projects lacking permitting certainty.

- High copper prices compress payback periods as projects with sub-3-year paybacks become compelling across institutional strategies from royalty funds to streaming providers and offtakers.

- Resource growth potential at advanced-stage projects creates valuation optionality as ongoing drilling at Pampa Oxide could expand production profiles beyond initial DFS assumptions.

- Chilean developers with established institutional shareholder bases benefit from capital syndication credibility as investors including Greenstone Resources, Assore Limited, Ithaki Limited, and Mitsubishi Corporation provide financing networks and operational expertise.

What Mercuria's Signal Means for Marimaca's Next Steps

Mercuria's large-scale copper withdrawal on December 2 reflects mounting physical tightness and rising concerns about supply reliability from major producers. When traders remove more than 40,000 tonnes of copper from accessible inventories, near-term supply constraints are expected to persist, requiring new production additions to address structural deficits.

Marimaca emerges as an advanced-stage Chilean project with completed DFS (August 25, 2025), environmental approval (RCA received November 2025), and a potential development pathway targeting FID in H2 2026, subject to completion of financing. The company's validated economics, capital-efficient profile, and proximity to infrastructure position it within the category of projects that may benefit from sustained market tightness and institutional capital rotation into near-term supply additions.

The investment implication is direct: as copper market tightness persists, advanced-stage projects with environmental certainty, validated economics, and credible development pathways may experience valuation uplift. Marimaca's positioning reflects this dynamic, though investors must recognize that project development carries inherent risks, including no certainty regarding eventual feasibility, financing completion, or achievement of production targets.

TL;DR

Mercuria's December 2 withdrawal of over 40,000 tonnes of copper from LME warehouses triggered record pricing of $11,540/t, exposing structural supply vulnerabilities. This market tightness elevates the strategic value of advanced-stage development projects with permitting certainty.

Marimaca Copper's Marimaca Oxide Deposit in Chile represents a de-risked opportunity: the project holds environmental approval (RCA received November 2025), a completed DFS (August 2025), and validated economics showing post-tax NPV8% expanding from US$709M at $4.30/lb copper to US$1.1B at $5.05/lb with 39% IRR. The company targets FID in H2 2026, subject to financing completion, positioning it as a potential beneficiary of sustained copper market deficits.

FAQs (AI-Generated)

Mercuria cancelled over 40,000 tonnes for delivery to South Korea and Taiwan on December 2, reflecting expectations of sustained physical supply tightness rather than speculative positioning. The move triggered record copper prices and widened backwardation spreads, signaling anticipated supply deficits.

Marimaca completed its Definitive Feasibility Study in August 2025 and received Chile's comprehensive environmental authorization (RCA) in November 2025. The company targets final investment decision in H2 2026, subject to completion of financing, with steady-state production of 48,000 tonnes of copper cathode annually over a 13-year mine life.

At $4.30/lb copper, the DFS shows post-tax NPV8% of US$709M with 31% IRR. At $5.05/lb, NPV8% expands to US$1.1B with 39% IRR and 2.2-year payback. The record LME price of $11,540/t ($5.23/lb) exceeds both assumptions, suggesting significant economic upside potential.

Marimaca offers low capital intensity (US$11,700/tonne annual capacity), a low strip ratio (0.8:1), conventional heap leach processing avoiding smelter complexity, recycled seawater supply, environmental approval certainty, and proximity to infrastructure near Antofagasta. The project also benefits from an institutional shareholder base including Mitsubishi Corporation.

Project development carries inherent risks including no certainty regarding financing completion, achievement of production targets, or eventual feasibility. Any capital raising may result in dilution or other effects on share value, and copper price assumptions may not reflect future market conditions.

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

Stay Informed