Breaking News: Wind and Solar Potentially Aren't Climate Cure-Alls

The flaws and myths of renewable energy and why they will never be the whole solution to climate change.

Despite the hype, wind and solar power potentially aren't the climate cure-all that people think. After his breakdown of the promising future for coal, Fergus takes us deeper into his energy thesis, taking on the renewables industry.

Fundamental Flaws of Wind and Solar

Reliability

Perhaps the most obvious criticism of renewables is their intermittent nature, or as Fergus calls them “unreliable”. Solar panels clearly don’t work when it's dark and wind turbines don’t turn when it isn’t windy, but the problem goes far deeper than this.

Solar energy is fundamentally at odds with our energy usage patterns, being offline when we’re making dinner and watching tv after work. On overcast days when we’re more likely to be inside production levels fall, and that’s nothing on the scale of capacity issues caused by snow.

Even the ambitious plans for huge desert solar arrays face repeated cleaning to remove sand from the panel surfaces.

The real issue with solar, however, is seasonality. In the Northern Hemisphere during winter, when the earth is angled away from the sun, there is a 50% decrease in solar power production. The only solution to this requires either twice the number of panels, half of which will be excess capacity in the summer, or having back-up power stations that will remain idle for half the year.

Wind power experiences similar issues and also requires supplementation by other energy sources to account for unpredictable down time.

Due to the very nature of their design, renewables like solar and wind fail to provide energy security, leading to a reliance on backup power stations, which ultimately contradict the very purpose of installing renewables.

Energy Density

Human development has been framed by the energy density ladder, with each rung more energy dense than the last: transitioning from wood, to coal, onto oil and gas, before arriving at nuclear power. For Fergus Cullen solar and wind power represent a step in the wrong direction:

“We’ve actually gone backwards…orders of magnitude backwards”

Moving back down the energy ladder means we will have to build far more power generators, requiring far more materials and far more space, in exchange for less energy.

A study by the UK Department of Energy and Climate Change found that to replace Hinkley Point C, a nuclear power plant in Somerset, it would require 130,000 acres of solar farms or 250,000 acres of onshore wind farms, an area roughly the size of Hong Kong.

Considering that Hinkley Point C takes up just 450 acres, the alternatives require between 280-550 times more space for the same capacity.

Fergus also cites a study which found that the operational lifespan of most wind turbines is significantly lower than the broadly accepted 20-25 years. The report by the Renewable Energy Foundation which analysed 3000 wind turbines in the UK and Denmark found that on average they lasted for just 12-15 years.

So wind power not only requires far more resources and space but it also needs replacing regularly, when compared to the operation lifetime of the average nuclear plant of between 30-40 years, the difference is stark.

To make matters worse, wind turbine blades are currently unrecyclable, and typically end their lives in landfill.

Consequently, solar and wind power represent inefficient and broadly uneconomic alternatives to conventional sources of electricity.

Storage

The unpredictable nature of wind and solar power makes energy storage a necessity to stop the lights going out. However, according to Fergus, current battery technology is too expensive and ineffective to provide a scalable solution to this problem.

The Hornsdale Power Reserve lithium-ion battery that serves the Hornsdale Wind Farm in South Australia, was the largest battery in the world at time of construction in 2017.

.jpeg)

The Hornsdale battery currently provides 129MWh of storage, but Fergus argues that this isn’t the whole picture. Of the 129MWh just 30MWh, less than a quarter, is actually used for energy storage with the remaining 99MWh being required to stabilise the energy fluctuations from the wind farm.

30MWh in reality represents just 3 hours of power storage, not even enough to sustain power demand for a brief period of still weather.

Then we get to the cost; the Power Reserve battery is currently priced at A$90million, making it more expensive than the actual wind farm, which came in at A$89million.

To make matters worse, a 2020 expansion, which increased storage by just 1.5 hours, cost another $71 million, taking the overall battery cost to 1.8 times that of the entire wind farm.

In the words of Fergus Cullen “4.5 hours of stage is not going to cut it at all”, especially not at those prices.

The Developing World

Bloomberg NEF is predicting that by 2050, China’s energy mix will be 48% solar and wind, whilst India will top 55%, Fergus wholly disagrees.

“With no wind and the seasonality of solar, I don’t see how that can ever happen”

Considering that 97% of population growth is set to occur in developing nations over the next few decades it is very unlikely that renewables will be able to scale quickly enough or affordably to satisfy growing demands.

“If you don’t get buy-in from developing countries, it’s largely irrelevant what developed countries do”

While in the West, subsidies and government grants have underpinned the drive toward solar and wind power, developing countries are unlikely to have either the money nor the willingness to spend enormous amounts on inefficient electricity generation.

Once combined with the higher electricity costs associated with renewables, they quickly cease to be an option for the developing world.

If renewables remain as uneconomic as they are then Fergus believes that coal is the most likely candidate for electricity generation in the developing world.

You can read more about Fergus’ coal investment thesis here: Why Coal is Still Important and How Your Investment Portfolio Should Reflect That.

Myth Busting

Fergus breaks down the most important myths associated with the renewables argument:

Capacity Is Not Generation

A huge myth Fergus seeks to tackle is “the apples-for-apples comparison of renewables to baseload”, 1GW of nuclear power can’t simply be replaced by 1GW of wind or solar due to one overlooked reason, capacity factors.

The energy capacity of a power source is not the same as the amount of power it actually produces, for example, nuclear power has a typical capacity factor of 90% so 1GW of capacity translates to 900MW of generation. By contrast, wind sits at 20-40% and solar is even less with just a 10-25% capacity factor, with 1GW of capacity producing 200-400MW and 100-250MW respectively.

To replace 1GW of nuclear capacity you would need between 2.5-5 wind farms or 4-10 solar farms, with 1GW of capacity each.

Fergus even claims that the capacity factors of renewables, as low as they are, are actually misrepresentations, as the data is taken from solar and wind farms which have been built in optimal locations. Fergus considers this to be similar to the high-grading methods used in the shale industry.

A prime example of the impact of capacity factors would be Japan’s decision to decommission their offshore wind farm in Fukushima Prefecture. Despite being well placed for wind power and with aims to achieve a 30% capacity factor, the project failed, with capacity factors fluctuating between 4-36%.

Japan has since chosen to keep coal as one of their key baseline electricity sources, with plans to build 22 new high-efficiency coal plants by 2025.

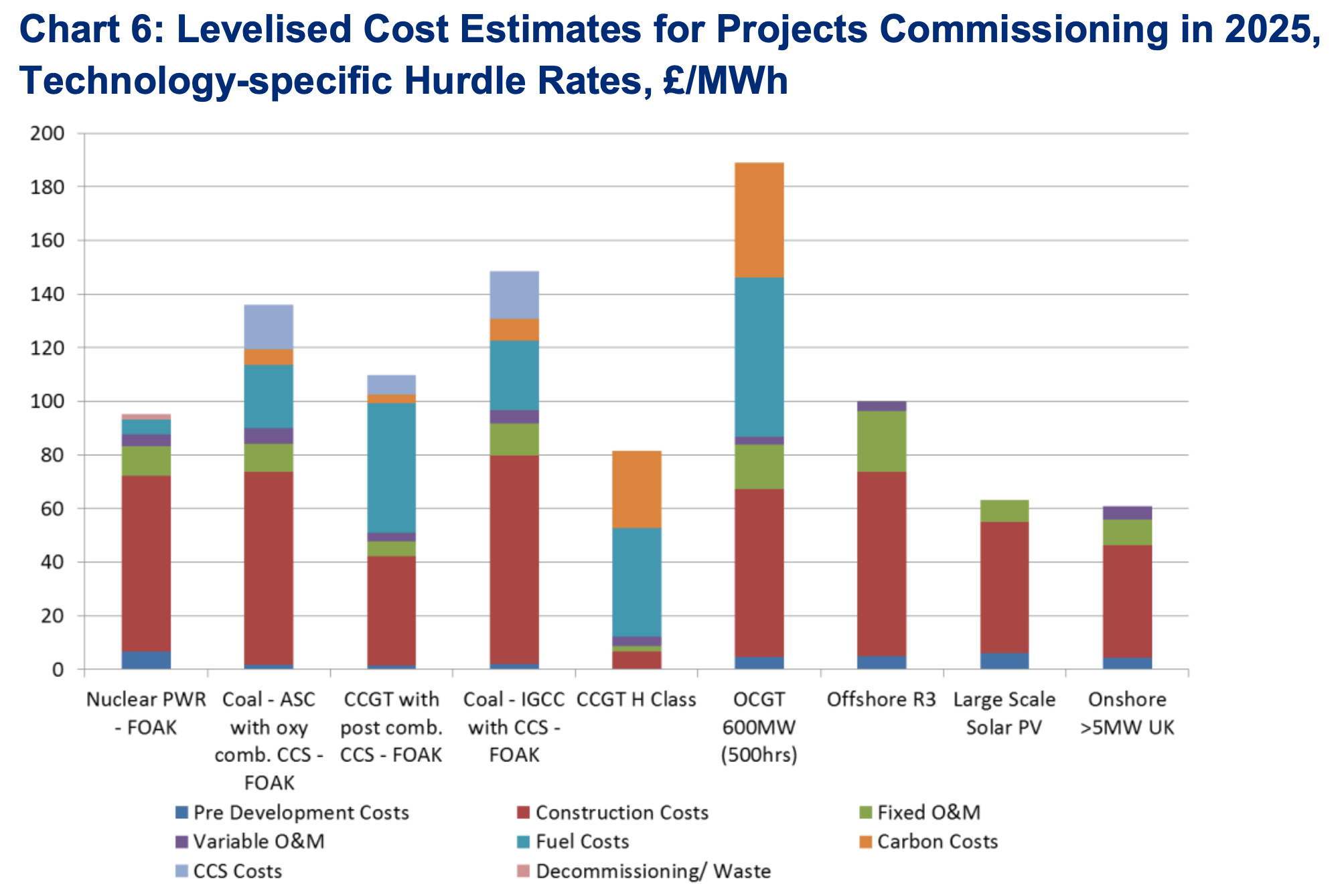

Levelized Cost of Energy - A Misleading Metric

Arguments for renewables tend to rely quite heavily on the Levelized Cost of Energy, a metric which supposedly accounts for all the costs associated with a particular energy type, from development and construction all the way to decommissioning.

The chart below covers the UK government estimates for LCOE in 2025 in £/MWh, and it clearly shows that large scale solar and onshore wind power are significantly cheaper than the alternatives.

However, Fergus Cullen believes that LCOE is incredibly misleading as it fails to account for the integration costs of switching to renewables.

“This is like quoting someone the cost of the flight and leaving out the pilot and half the fuel”

There are three main costs that aren’t included in LCOE:

- The infrastructure required to handle the fluctuating power levels associated with renewables. Even the infrastructures of the most developed countries aren’t up to the task, with Fergus citing the US energy grid, which is already well past its life expectancy and has been graded D+ by the American Society of Civil Engineers.

- The need for back-up power stations to handle the unpredictability of renewable energy. Either new power plants will need to be constructed or existing stations will need to be upgraded to react to supply fluctuations, instead of providing a constant base level.

- For Fergus, the main issue with LCOE is storage, which is wholly unaccounted for, and without storage, renewables cannot compete with conventional energy sources.

Suspicious Success Stories

Despite their reputations as renewable success stories, Germany and Denmark are struggling to implement their green policies.

Germany

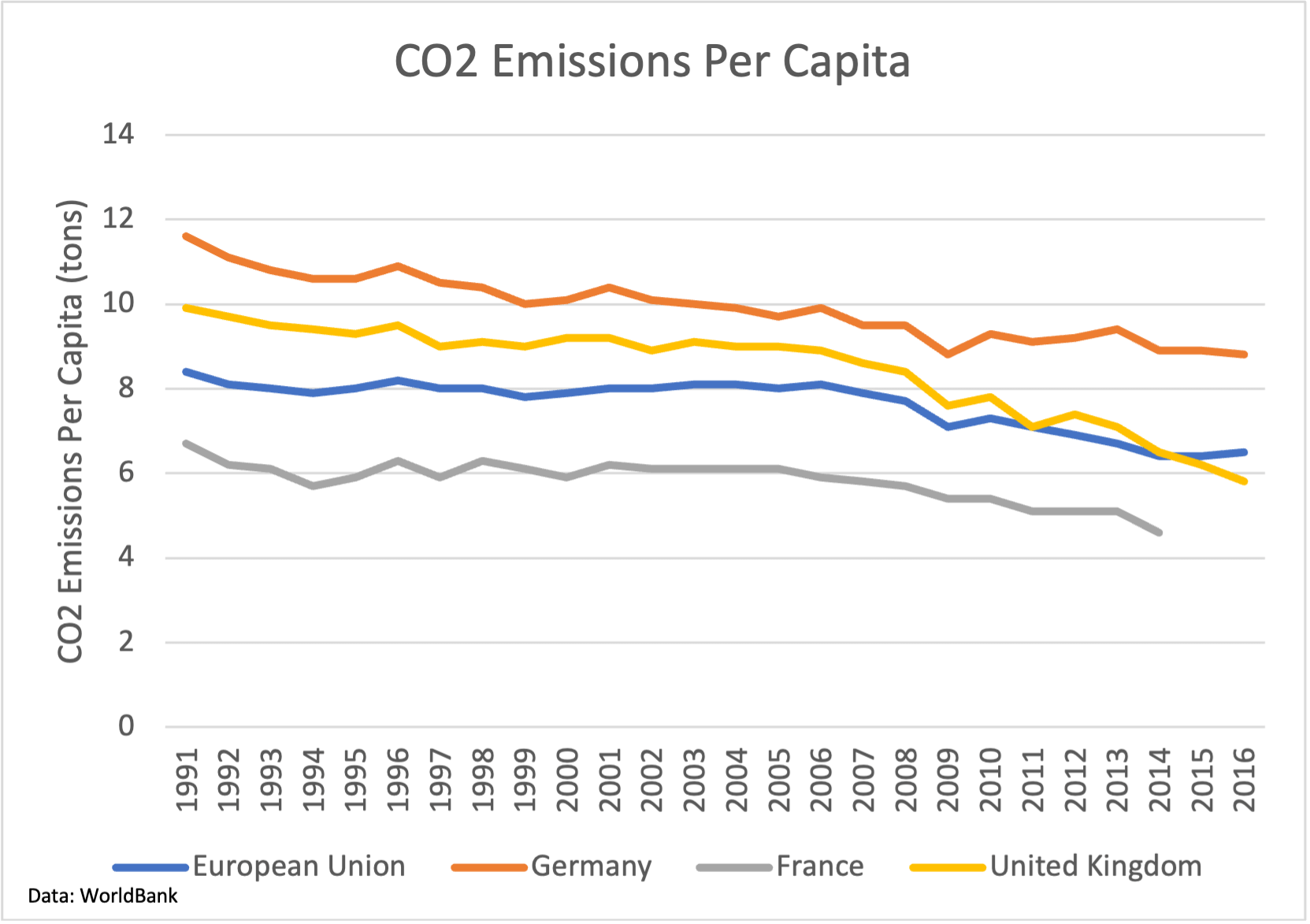

Despite 42% of Germany’s electricity coming from renewable sources, the country has failed to significantly reduce its carbon emissions per capita and still ranks far higher than other Western European countries like the UK and France and the EU average.

Germany also experiences the second highest electricity costs in Europe, second only to Denmark. However, it is worth noting that over half of this cost is from taxes and other surcharges. Roughly 20% of the electricity cost comes from the renewables surcharge, which supports the expansion of renewable energy.

The transition to renewables has been repeatedly hampered by conservationists and local associations resisting the construction of onshore wind turbines.

Germany has targets to add 4GW of wind power to their energy mix annually, however just 1.5GW was achieved in 2020 and it has been predicted that Germany will have a net loss of wind capacity growth in 2021. This net loss can be attributed to the slow rate of adoption and the decommissioning of existing wind farms.

Germany has also had to rely on energy imports to stabilise its energy grid, particularly from France, which generates the majority of its energy from its fleet of nuclear reactors.

So far, Germany has been beset by difficulties, with mounting resistance to onshore wind, rising electricity prices, and a lack of energy security, in exchange for CO2 emissions which are still higher than countries with a comparable level of development.

Denmark

Denmark is often held up as a model country for clean electricity generation, with almost 60% being produced by wind power which is undoubtedly an impressive achievement. However, it is only possible because Denmark can import electricity from its neighbours to make up for its fluctuating power supply.

Fergus emphasises that at certain times, Denmark imports as much as 50% of its electricity needs, particularly from Norway, which has a reliable hydroelectric baseload.

Denmark’s model is fundamentally flawed as it is reliant on electrical imports from countries with more consistent energy sources. This model very simply cannot be scaled.

Fossil Fuels, ESG, and Investor Activism

The question remains, however, if renewable energy is so inefficient and uneconomic, why have energy giants like Shell (LSE:RDSA) and BP (LSE:BP) shifted so heavily toward green energy?

Fergus believes that investor activism and ESG (Environmental and Social Governance) mandates are the cause.

He highlights the recent actions of BlackRock and several other investor activist groups against ExxonMobil’s management, due to beliefs that the oil giant was not committed to action against climate change. Fergus sees this as a prime example of companies being forced into renewable energies that are against their best interests.

“By sheer shareholder force, the management can’t toe the line of the actual business”

However, this extends much further than just BlackRock, with the Norwegian Sovereign Wealth Fund, the California Public Employees' Retirement System, Vanguard, and many other funds targeting fossil fuel businesses.

Fergus believes, however, that this turn toward solar and wind power by large fossil fuel companies is permanent, as opposed to the greenwashing by Shell and BP in the late 1990s. With BP committing to selling $25bn of its oil assets by 2025, regardless of a post-COVID oil market recovery, at a record low in the market whilst simultaneously buying into renewables which are trading at a premium.

“They’re going to get burned by what they’re doing, they need to be doubling down on fossil fuels because it’s going nowhere”

Is there hope? Molten Salt Reactors

After a pretty gloomy outlook for renewables there is hope for a cleaner energy future.

Small Modular Reactors (SMRs) and Molten Salt Reactors (MSRs), according to Fergus, may be the future.

“I think it will be a gamechanger if we can get them adopted”

MSRs use fluoride salts as a coolant, instead of water, and dissolve the fissile material into the molten salt rather than using fuel rods. Fergus highlights several key benefits of this type of reactor:

Efficiency

Conventional reactors can only use 3-5% of the fissile material in a fuel rod as they decay quickly, meaning they often need replacing which produces a great deal of highly hazardous waste. In MSRs the fuel is dissolved into the fluoride salts allowing it to remain within the reactor for far longer, resulting in far more of the fissile material being expended. This higher proportion of fuel use results in far less dangerous waste. Conventional nuclear waste remains hazardous for up to 10,000 years, by comparison MSR waste only remains radioactive for 200-300 years.

Safety

MSRs are considered “walk away safe” as there is no risk of meltdown. Should the reactor overheat then the freeze plug (as shown on the diagram) would thaw resulting in the fuel salts being drained into dump tanks where they cool and solidify, becoming safe. MSRs also operate at atmospheric pressure, unlike water-cooler reactors, so in the case of a breach there is no risk of an explosion or of radioactive material being released by a huge cloud of steam.

Nuclear Waste

MSRs actually consume nuclear waste, providing a partial solution to the world’s radioactive waste problems. As just 3-5% of the fuel in a conventional fuel rod is expended the remaining fissile material can be converted into fuel for an MSR.

Applications for the Developing World

Due to their relatively simple design, with few moving parts and without the need for pressure containment systems, MSRs lend themselves well to mass production. If combined with SMR technologies these reactors could be scaled to the size of a shipping container for easy distribution across the developing world. As MSRs are “walk away safe” they require very little infrastructure and expertise to run, making them perfect for regions without modern energy grids.

Public Perception

MSRs will help to break the stigma surrounding nuclear power as they represent a significant shift in technology. The impressive safety features associated with MSRs will help to allay public fears and shift attention away from nuclear disasters like Chernobyl or Fukushima which could not occur with an MSR.

Hydrogen Generation

As MSRs produce both a great deal of heat as well as electrical energy they offer the potential for large scale, cheap hydrogen production. A trial found that by using 78% heat energy and 22% electrical from an MSR, hydrogen could be produced at just $2/kg.

Trader Ferg’s Angle

Regardless of your opinions on solar and wind power, any roll out will require a huge amount of raw materials, for Fergus this is where investors can take advantage of the trend toward renewables.

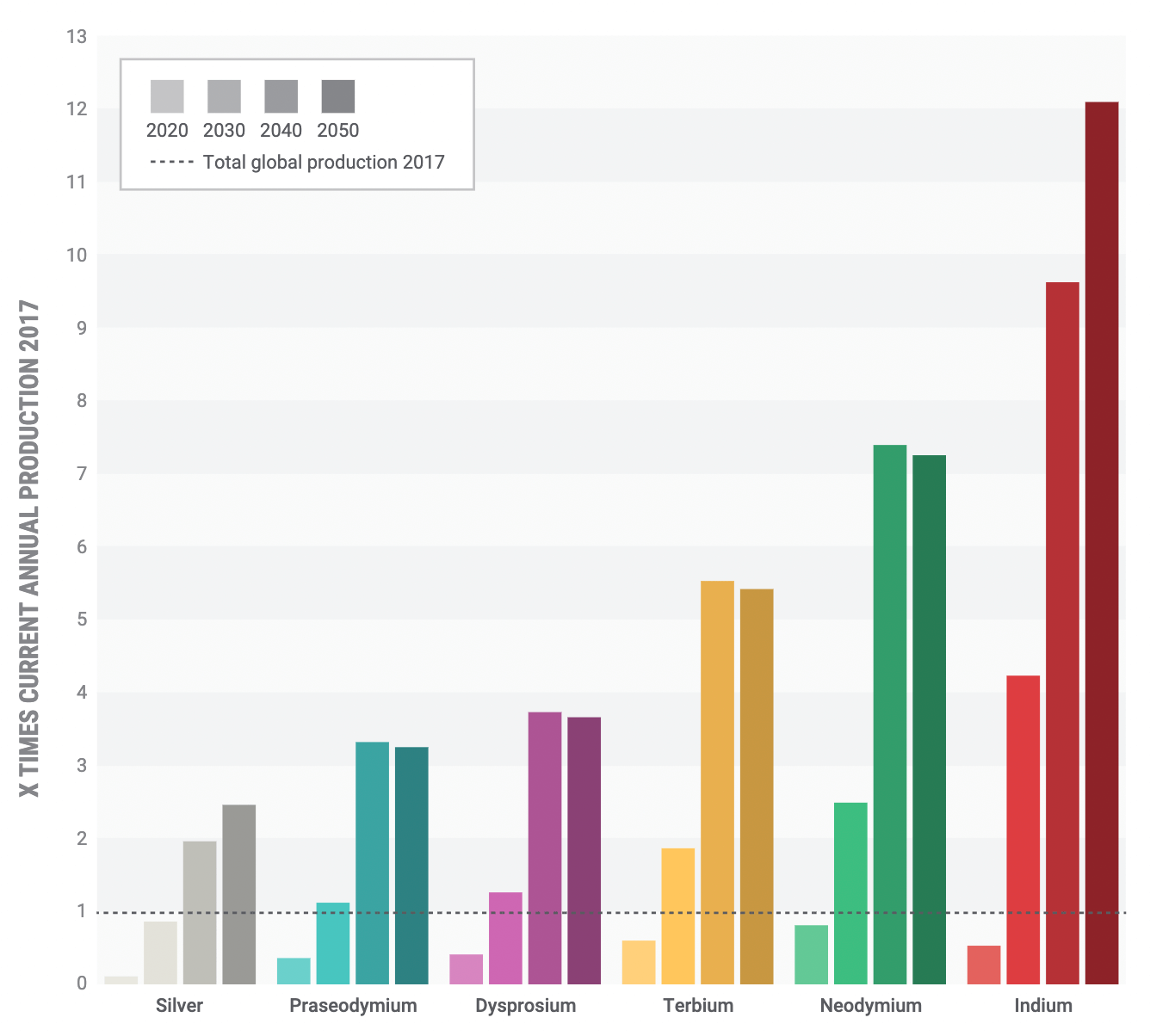

Rare Earth Elements (REEs) are where Fergus sees a great deal of potential. A report commissioned by the Dutch government in 2017 analysed the demand for metals from current renewables mandates for solar and wind power and the results are glaring:

- The demand for neodymium, an REE typically used in magnets and critical for direct drive wind turbines, is set to rise to over 7 times the annual production in 2017.

- Terbium, also used in direct drive magnets, will see demand outstrip the 2017 supply by 5.5 times.

- While not an REE, demand for indium is expected to soar to over 12 times the annual production in 2017.

This report has been corroborated by the World Bank, which estimates cumulative neodymium demand by 2050 for wind turbines alone could reach between 225,000-400,000 tons, depending on the uptake of direct drive technology.

Electric vehicles (EVs) are also set to have a huge impact on demand, Fergus cites a report which found that for the UK alone to reach its 2050 EV targets it would require 2 times the worlds annual cobalt production, almost the entire neodymium supply, 75% of the lithium supply, and 50% of annual copper production.

However, Fergus cautions against investing in battery metals, like lithium and cobalt, as it is still uncertain as to which battery technology will emerge as dominant. He has prior experience of the unpredictability of this market as he bought into the cobalt spike in 2018, shortly before Tesla announced that it would be removing cobalt from its battery mix.

Fergus has limited his battery metal exposure since, keeping each battery metal at 2% or less of his portfolio.

For Fergus REEs make the most sense, especially when combined with uranium production, as is the case with Energy Fuels (NYSE:UUUU).

You can read more about Fergus’ views on REEs here: The Middle East Has Oil, China Has Rare Earths.

What to do next

Eager for more Ferg content or looking for consistent returns for more confident investing?

That's where we come in. Crux Investor is an investing app for busy people.

You’ll receive a single stock recommendation each month, curated by industry experts and presented in a clear and focused one-page memo. You’ll also receive access to a platform full of programmes that will allow you to grow your financial knowledge, overall, all at your own pace.

Crux Investor is for anyone interested in saving time while investing with confidence. It's an ideal resource for the novice that needs guidance and is tired of throwing money away with guesses and gambles. But it's also a perfect fit for the experienced investor that wants a faster and more efficient way to arrive at the perfect stock or significantly increase their knowledge.

Finally, you can afford the analysts the big funds use. No more gambling, no more guesswork.

Instead, save time, slay stress, and start investing with confidence by joining Crux Investor today.

Analyst's Notes

Subscribe to Our Channel

Stay Informed