160% Cobalt Rally Signals Higher Battery-Metal Valuations as Resource Nationalism Tightens Supply

Government supply controls are driving battery-metal prices, boosting valuations and financing access for projects in stable jurisdictions.

- Battery metals in 2026 are being driven more by government supply controls than by electric-vehicle demand, as the Democratic Republic of Congo, Indonesia, and Zimbabwe use export quotas and processing mandates to restrict cobalt, nickel, and lithium supply and support prices.

- Congo's quota framework caps 2026 and 2027 cobalt exports at about 96,600 tonnes per year, roughly half of 2024 levels, helping lift cobalt metal about 160% from its February 2025 low to above US$56,000 per tonne.

- Stable, Western-aligned projects can command higher valuations and lower financing costs as supply controls increase policy risk in major producing countries.

- The main risks are weaker project economics, financing that fails to close, and a breakdown in supply discipline that lowers metal prices.

Government Supply Controls Become the Primary Driver of Battery-Metal Prices

For most of the past decade, battery-metal prices were driven primarily by expectations for electric-vehicle demand. Lithium, cobalt, nickel, and graphite prices largely reflected expectations for electric-vehicle adoption. Battery metals rallied in 2021 and 2022, then fell in 2023 and 2024 as new supply from China, Indonesia, and the Democratic Republic of Congo pushed prices back toward pre-pandemic levels. Many investors concluded that mine supply could outpace demand for years.

Battery-metal prices in 2026 are being supported by government supply controls rather than stronger end demand. Export bans, quotas, royalties, and processing mandates are now major drivers of battery-metal supply and pricing. Major cobalt, nickel, and lithium producers are restricting exports and processing routes to support prices and government revenue.

When governments restrict supply, jurisdiction and fiscal terms have a greater influence on project valuations. Country risk, permitting certainty, and fiscal stability can affect both valuation multiples and financing costs. The following sections examine how supply controls affect project valuations, financing, and capital allocation.

Government Supply Restrictions Reshape Cobalt, Nickel & Lithium Markets

The shift toward supply-driven pricing is most visible in cobalt, nickel, and lithium, where a single jurisdiction controls a large share of global supply. In each case, government policy changes rather than stronger demand drove the price move.

Congo Halves Cobalt Exports & Drives a Supply Deficit

The Democratic Republic of Congo supplies roughly three-quarters of the world's mined cobalt, giving its export policy significant influence over global cobalt supply. In February 2025 it imposed an export ban, then in October 2025 replaced it with a quota system that caps 2026 and 2027 exports at about 96,600 tonnes per year, roughly half of 2024 levels.

Cobalt metal has risen about 160% from its February 2025 low to above US$56,000 per tonne. First, cobalt is primarily a by-product of copper and nickel mining, so producers cannot quickly increase cobalt output when prices rise. Second, actual hydroxide shipments have run near one-third of allocated volumes because of permitting and logistics constraints, while Fastmarkets still projects a 2026 cobalt deficit of about 10,700 tonnes.

Indonesia & Zimbabwe Tighten Nickel & Lithium Supply

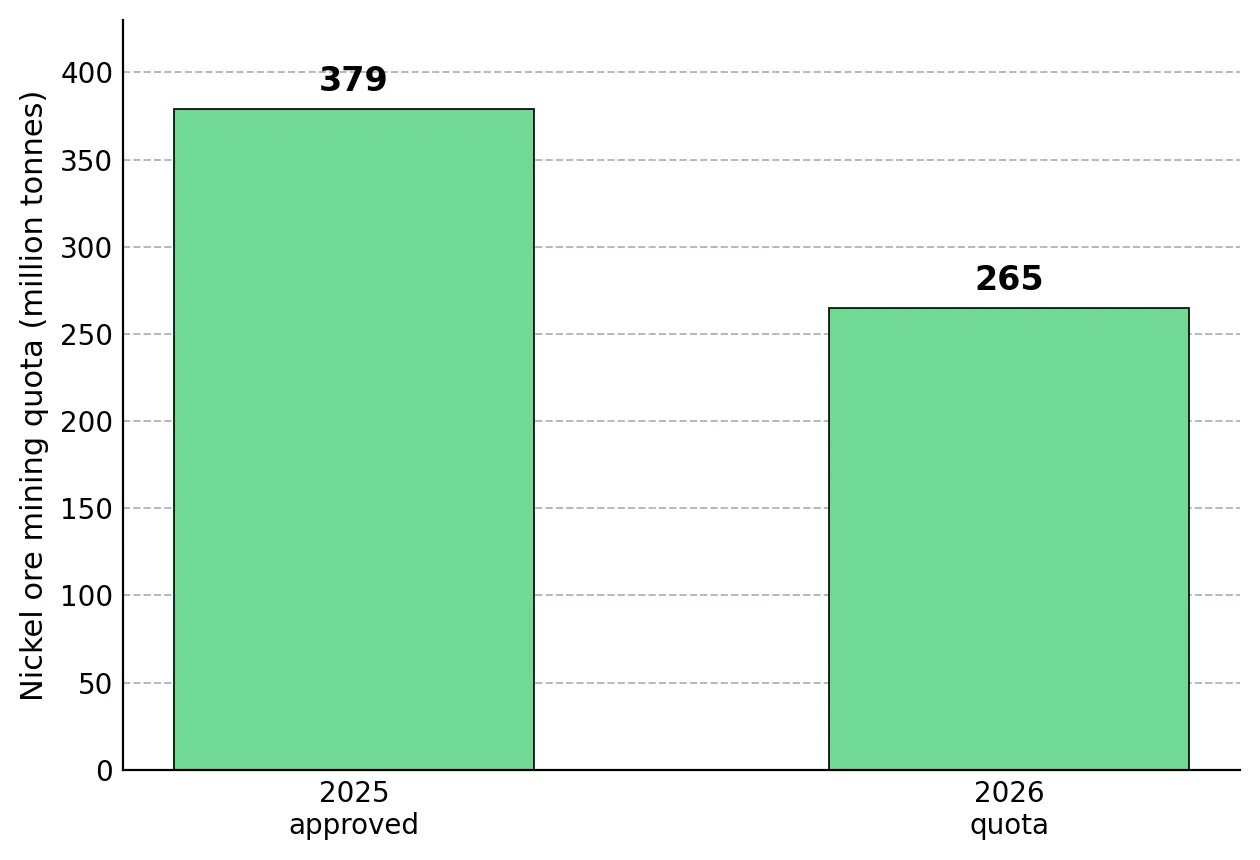

Indonesia, which accounts for the majority of global mined nickel supply, has also used quotas to restrict output. Its 2026 mining quota, known as the RKAB, was set at 260-270 million tonnes of ore versus 379 million tonnes approved for 2025, a reduction of about 30%. The quota reduction helped lift nickel prices to US$18,500-US$20,000 per tonne, although high inventories continue to limit further gains. Zimbabwe has taken a similar approach in lithium, imposing export quotas and signaling a future ban on concentrate exports to encourage domestic processing.

Supply controls in major producing countries increase the value of nickel projects in stable jurisdictions. Canada Nickel's Crawford project is one of the few non-Indonesian nickel sulphide projects targeting production before the end of the decade. Nickel sulphide ore generally requires less processing than Indonesian laterite ore, which can improve project economics. The limited number of advanced Western nickel projects supports their strategic value.

Mark Selby, Chief Executive Officer of Canada Nickel, describes how the limited number of advanced Western nickel projects could increase their value as Indonesia restricts supply:

"There's 200 gold stories, there's 150 silver stories, there's 100 copper stories, but there really are only a half a dozen nickel stories that have had meaningful advancement."

Stable Jurisdictions Command Higher Valuations & Lower Financing Risk

Sovereign supply controls increase the value investors place on projects in stable jurisdictions. Projects in countries using quotas and export restrictions face higher policy risk than projects in stable jurisdictions. Policy changes in countries using quotas or export controls can alter project economics, while projects in stable Western jurisdictions can attract higher valuations and lower financing costs. Investors often assign higher EV-per-pound valuations and place greater weight on NPV8 and IRR estimates for projects with lower jurisdictional risk.

Operating Assets in Stable Jurisdictions Command a Financing Advantage

Operating assets in stable jurisdictions provide the clearest example of how jurisdiction can affect valuation and financing risk. Energy Fuels is building an integrated, ex-China rare-earth supply chain spanning the United States and Australia, running from mining through separated oxides and, via its scheme with ASM, ultimately to alloys. Its Phase 2 rare-earth separation project carries a US$1.9 billion NPV8, a 33% IRR, and US$410 million of initial capital expenditure, and would lift the company to a separation scale comparable to Lynas. By processing monazite, which contains both light and heavy rare earths, at its White Mesa mill in Utah, Energy Fuels positions itself as a heavies-capable alternative to peers reliant on bastnaesite feedstock.

Energy Fuels advances the rare-earth project while uranium production funds the build-out, with offtakers seeking ex-China supply. This has translated into tangible financing terms: a Goldman Sachs convertible priced at three-quarters of a percent and closed within a week, roughly US$1 billion of deployable capital, and a re-rate to a roughly US$5 billion market capitalisation as investors came to view the company's roughly US$2 billion funding package as achievable. Current cash flow comes from uranium production, which bridges the company to the larger rare-earth opportunity.

Beneficiation Policies Make Processing Strategy a Key Project Variable

Resource nationalism can support projects in stable jurisdictions while increasing regulatory risk for developers operating inside countries pursuing beneficiation policies. Lifezone Metal's Kabanga project in Tanzania is one of the world's highest-grade undeveloped nickel sulphide deposits, but current discussions with the government create uncertainty around future processing requirements and export terms. Lifezone currently generates revenue from its Simulus recycling platform, which recovers platinum, palladium, and rhodium from spent catalytic converters, rather than from nickel production.

Lifezone's processing technology is aligned with the in-country beneficiation requirements increasingly sought by resource-rich governments. Its hydrometallurgical process is designed to enable lower-emission in-country processing than conventional smelting, which could support compliance with local processing requirements. Project economics and development timelines remain dependent on the outcome of ongoing discussions with the Tanzanian government.

Ingo Hofmaier, Chief Financial Officer of Lifezone Metals, describes how discussions with the Tanzanian government could influence future downstream processing requirements:

"In our feasibility study it's concentrated export only, and we're currently in discussions with the government about what the conditions would be to build something further downstream."

Financing Structure Becomes a Competitive Advantage for New Projects

Resource nationalism can increase fiscal and sovereign risk for new projects, raising the returns required by lenders and equity investors and increasing the cost of capital. Financing terms therefore become an important differentiator between developers. Flow-through shares can lower the effective cost of equity financing for Canadian exploration and development projects.

Strategic Capital Targets Western Critical-Mineral Supply Chains

Government agencies and strategic investors are directing capital toward critical-mineral projects in stable Western jurisdictions. Development-finance institutions, export-credit agencies, and industrial offtakers are supporting permitting and construction in these jurisdictions, improving project financeability and shortening development timelines. This capital is targeting supply chains where low-cost production remains heavily concentrated in a single country, creating supply-security concerns for Western governments and manufacturers.

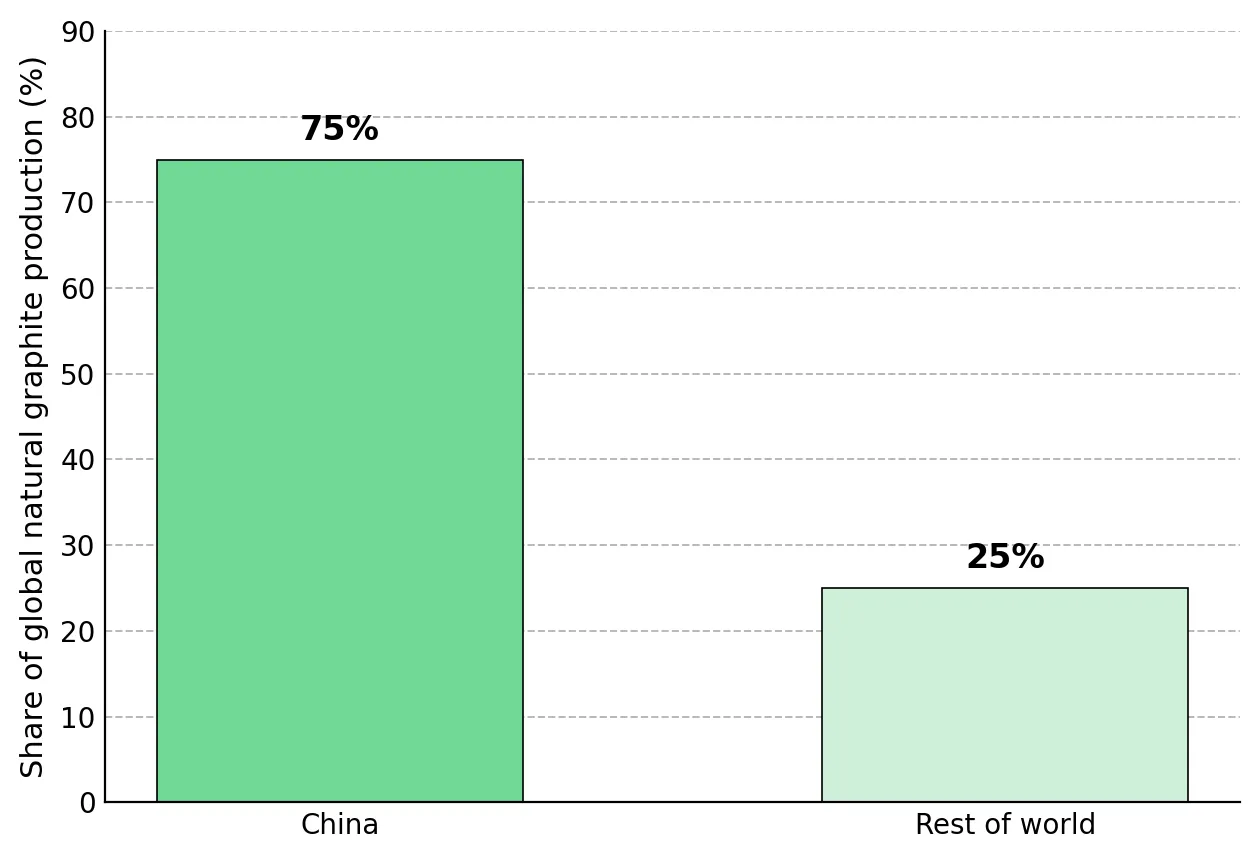

Graphite is one of the most concentrated battery-metal supply chains, with China producing about 75% of global natural graphite supply. Canada Nickel is targeting approval as the first project permitted under Canada's 2019 federal impact-assessment legislation, while Export Development Canada is in debt negotiations and Samsung is an offtake partner, supporting the project's financing options. Sovereign Metals' Kasiya project is expected to rank among the lower-cost graphite producers and includes a monazite by-product whose heavy-rare-earth content has attracted interest from U.S. agencies seeking non-Chinese supply. Both projects benefit from efforts by Western governments and manufacturers to diversify supply away from China.

Ben Stoikovich, Chairman of Sovereign Metals, explains why Western governments and strategic investors are seeking alternatives to Chinese graphite supply:

"China dominates low-cost production. China produces around 1.2 million tons per annum of natural graphite, i.e. about 75% of global supply at an average production cost of $257 a ton. The rest of the world simply cannot compete."

China's dominance of critical-mineral supply chains is directing government and strategic capital toward alternative sources, giving projects with predictable permitting and stable fiscal terms better access to financing.

The Investment Thesis for Battery & Critical Metals

- Sovereign supply controls in cobalt and nickel have supported prices, improving project economics and investor interest in assets located outside the jurisdictions imposing quotas and bans.

- Investors are assigning higher valuations to producers with secured permitting, lower regulatory risk, and operations in stable, Western-aligned countries.

- Beneficiation mandates can improve the development prospects of projects whose processing technology supports in-country refining rather than concentrating exports.

- Western supply shortages in heavy rare earths can increase the strategic value of projects with economically significant rare-earth by-products, even when those by-products contribute little to base-case project economics.

- Higher borrowing costs favour producers with self-funded balance sheets and developers that can reduce equity dilution through alternative financing sources.

- Strategic and development-finance capital is flowing to stable jurisdictions, improving access to funding for explorers and developers that can demonstrate permitting progress and secure offtake partners.

Battery-metal prices are increasingly being driven by government supply controls rather than electric-vehicle demand. When governments restrict supply through quotas, export bans, or processing mandates, investors place greater value on projects in stable jurisdictions with predictable mining and processing rules. Investors should place greater weight on jurisdiction, permitting certainty, and balance-sheet strength because these factors can improve access to financing and reduce development risk when supply controls support commodity prices.

TL;DR

Battery metals in 2026 are being driven more by government supply controls than by electric-vehicle demand. Congo's cobalt quotas, Indonesia's nickel restrictions, and Zimbabwe's beneficiation policies have tightened supply and supported prices, increasing the value of projects in stable jurisdictions. Investors are assigning higher valuations to producers and developers with secure permitting, lower regulatory risk, and stronger balance sheets, while strategic capital is flowing toward Western critical-mineral supply chains. The key risks are a breakdown in supply discipline, weaker project economics, and financing delays for development-stage companies.

FAQs (AI-generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed