AI Infrastructure & Electrification Drive Structural Copper Demand

AI, EVs, and grid expansion are driving structural copper demand as supply constraints tighten, creating a long-term deficit and investment opportunity.

- Copper has repriced as a structural infrastructure metal for the AI and electrification economy, with prices recently exceeding $14,500 per tonne intraday in early 2026 and stabilizing above $13,000 per tonne, reflecting tightening supply and durable demand growth.

- Artificial intelligence data centers, electric vehicle adoption, and power grid expansion are accelerating copper consumption simultaneously, with S&P Global forecasting global demand growth from approximately 28 million tonnes in 2025 to more than 42 million tonnes by 2040.

- Supply growth remains structurally constrained by declining ore grades, permitting timelines averaging 15 to 17 years from discovery to production, and weakening discovery pipelines, with only 5% of major copper deposits found in the last decade.

- Advanced development projects in stable jurisdictions with completed feasibility studies, environmental approvals, and credible cost structures are gaining strategic importance as the primary mechanism to bridge the looming supply gap.

- The opportunity lies in identifying companies across the development and exploration pipeline that can convert geological resources into economically viable copper production within the timeframe of accelerating demand.

Copper's Structural Repricing in the Age of Electricity & Artificial Intelligence

Copper’s resurgence in global markets is not simply another commodity rally. It reflects the convergence of several structural forces including electrification, artificial intelligence infrastructure, and geopolitical competition for critical minerals.

In January 2026, copper briefly surged to $14,527 per tonne, one of the strongest rallies in modern trading history. Prices have since stabilized above $13,000 per tonne, well above historical averages.

The demand drivers differ from previous cycles. Electric vehicles require roughly four times more copper than internal combustion vehicles, while renewable energy systems rely heavily on copper wiring and transmission infrastructure. The rapid expansion of AI hyperscale data centers has also introduced a new source of demand. According to J.P. Morgan, a single large AI data center can require up to 50,000 tonnes of copper, with total data center demand projected to reach 475,000 tonnes annually by 2026.

Demand Growth Is Accelerating Faster Than the Mining Industry Can Respond

Projected copper demand growth is extraordinary. According to S&P Global, global consumption could rise from about 28 million tonnes in 2025 to more than 42 million tonnes by 2040, a roughly 50% increase. This growth is driven by three overlapping trends: transport electrification, renewable energy expansion, and rapid growth in AI-driven digital infrastructure.

The International Energy Agency estimates the broader critical minerals sector will require $500 to $600 billion in new investment by 2040 to meet these needs. Copper sits at the center of this transition because its conductivity, durability, and recyclability make it essential for large-scale electrical systems.

Supply constraints are becoming the bigger issue. Copper production growth has slowed as the industry faces declining ore grades, more complex deposits, and rising development costs. Average global copper grades have fallen about 40% since 1991, forcing producers to process far more material to produce the same metal. At the same time, the discovery pipeline has weakened, with only about 5% of major copper deposits discovered in the past decade.

Supply Constraints: Why New Copper Mines Are Harder to Build Than Ever

Copper demand growth is widely recognized, but the industry’s ability to deliver new supply is constrained by geological, financial, and regulatory challenges that are unlikely to ease quickly.

Declining ore grades are increasing operating costs and capital requirements, especially for large sulphide projects that require costly concentrators and smelters. Permitting timelines in many jurisdictions often exceed a decade, while environmental and social licensing requirements continue to tighten. As a result, the average copper project now takes about 17 years from discovery to production, meaning today’s price signals may not translate into new supply until the mid-2030s.

Merlin Marr-Johnson, Chief Executive Officer of Fitzroy Minerals, an exploration-stage company advancing copper projects in Chile, describes the supply-side reality as a market-defining constraint:

"Production growth within Chile, and globally, is difficult. It is a mature industry struggling to maintain production, with vast amounts of money being spent simply to sustain output. As demand remains strong, metal prices will need to rise."

These constraints are particularly evident in the concentrate market, where smelter treatment and refining charges have fallen sharply. In early 2026, the annual benchmark between a major Chilean miner and Chinese smelters settled at $0 per tonne, the lowest level on record, signaling that smelters are competing aggressively for limited concentrate supply. These dynamics reinforce the importance of capital-efficient projects capable of entering production within the timeframe of peak demand growth.

Market Volatility & Macro Cycles: Why Copper Prices Remain Sensitive to Global Policy

Despite strong structural demand drivers, copper remains sensitive to macroeconomic cycles. In early March 2026, copper prices temporarily fell approximately 2.7% to $5.74 per pound following a surge in the US dollar. Because copper is priced in US dollars, dollar strength increases costs for international buyers and can suppress short-term demand.

Recent dollar strength reflects several concurrent macro factors, including elevated geopolitical tensions, rising oil prices, and delayed expectations for Federal Reserve interest rate cuts. Higher interest rates increase the opportunity cost of holding non-yielding commodity positions, creating temporary downward pressure on prices.

Most analysts view these movements as cyclical volatility rather than structural weakness. The long-term demand drivers, including electrification, AI infrastructure, and grid expansion, remain intact. For long-term investors, short-term price dislocations driven by macro policy shifts may represent entry points rather than structural reversals..

Development Projects Gain Strategic Importance as Supply Tightens

As supply constraints intensify, advanced development projects are becoming increasingly important within the copper investment landscape. Projects combining strong project economics, low capital intensity, demonstrated permitting progress, and proximity to existing infrastructure are likely to attract sustained institutional attention as the supply gap widens.

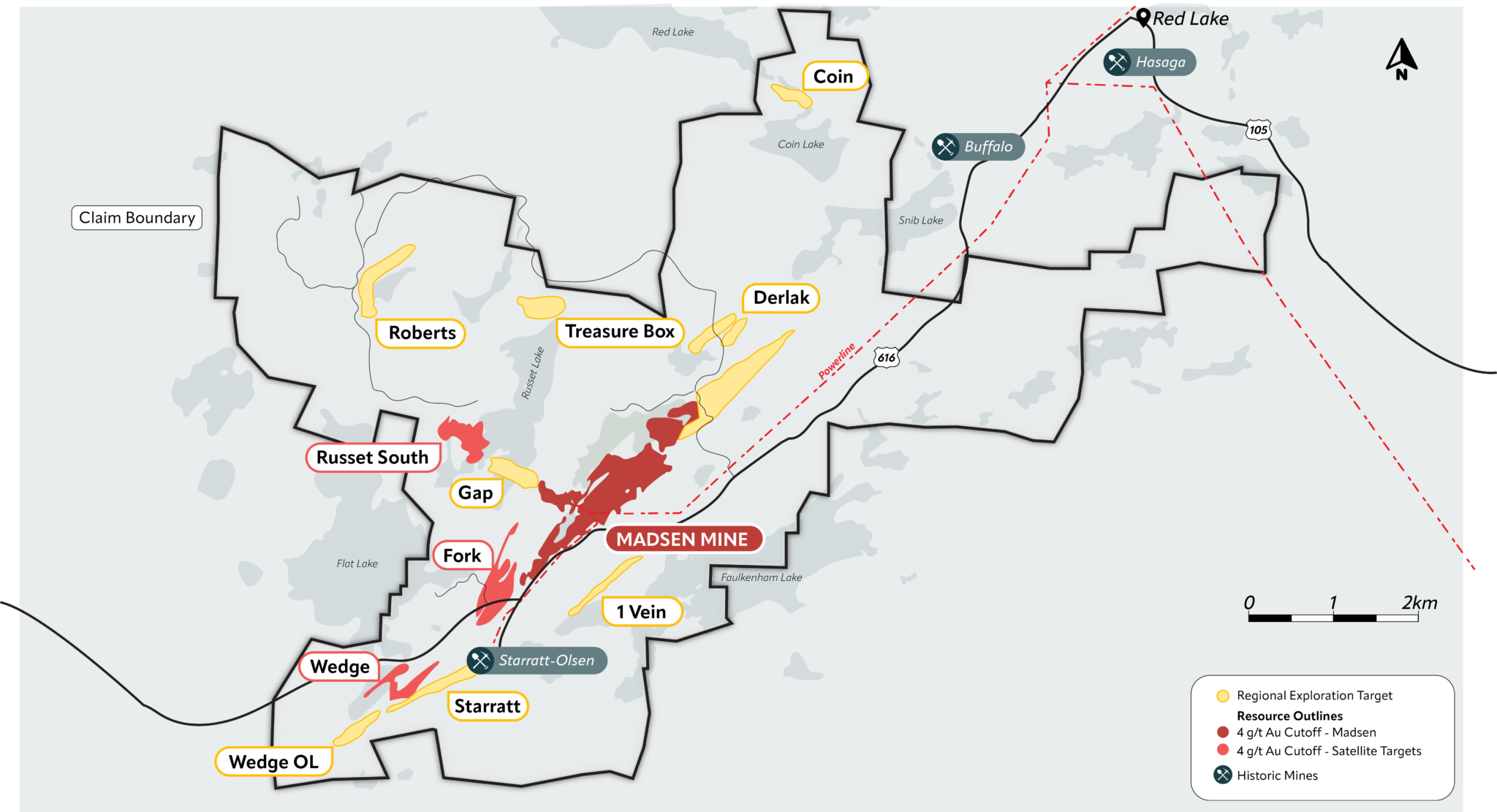

Marimaca Copper, a development-stage company advancing the Marimaca Oxide Deposit in Chile's Antofagasta region, offers a concrete illustration of this dynamic. The company has completed a Definitive Feasibility Study and received environmental approval in late 2025, two milestones that materially de-risk the development timeline and position the project for a construction decision.

The Definitive Feasibility Study outlines production of approximately 50,000 tonnes of copper cathode annually over a 13-year mine life, with projected C1 cash costs of $1.69 per pound and All-In Sustaining Costs of $2.09 per pound, placing the operation in the second quartile of the global cost curve. Post-tax net present value at an 8% discount rate is estimated at approximately $1.1 billion, with an internal rate of return of 39%. Capital intensity is estimated at approximately $11,700 per tonne of annual copper production capacity, which the company characterizes as industry-leading.

Hayden Locke, President and Chief Executive Officer of Marimaca Copper, explained the significance of the dual milestone achieved in 2025:

"The big items were that we delivered the DFS, which is really the final piece of the puzzle before we start transitioning into financing, and then detailed design and engineering for the Marimaca oxide deposit. The second part is that we are now permitted, so we’ve obtained our environmental approval, which is a huge milestone."

The project's proximity to the Port of Mejillones and access to renewable electricity and recycled seawater further strengthen its development profile by reducing logistics risk and aligning with evolving environmental, social, and governance expectations among institutional investors. Locke has also indicated that the exploration program surrounding the oxide deposit has the potential to add a further 25,000 tonnes per annum to the base case production profile, describing a drilling program where every single drill hole has intersected the target horizon, an unusually high success rate in exploration.

Exploration Pipelines Remain Essential to Long-Term Copper Supply

While advanced development projects can help bridge near-term supply gaps, exploration remains essential to sustaining copper supply beyond the current decade. New discoveries must ultimately replace declining production from aging mines, and the current discovery pipeline is insufficient to meet projected long-term demand.

Junior exploration companies play a central role in replenishing the development pipeline. Fitzroy Minerals is advancing multiple copper projects in Chile, including the Caballos and Buen Retiro projects. Recent drilling at Caballos intersected 176 metres grading approximately 0.47% copper equivalent, indicating the presence of a potentially significant porphyry-style system. Porphyry deposits, which are large disseminated copper systems often associated with molybdenum and gold, are responsible for the majority of global copper production and represent the primary discovery target class for major producers and acquirers.

Marr-Johnson frames the company's exploration thesis around the structural geology linking its assets to established producing deposits:

"We are really focused on our Buen Retiro flagship asset, which we believe has got major discovery potential. We have got the same geology that we can see of all of those three deposits within Buen Retiro."

The company has also commissioned a Mobile Magnetotelluric geophysical survey designed to map deep conductive structures that could host additional sulphide mineralization. A preliminary economic assessment is underway alongside a potential heap leach joint venture with Pucobre, which Marr-Johnson describes as a pathway to near-term, non-operated cash flow from a low-cost operation. Exploration nonetheless carries inherent risk: most targets never develop into economic mines, and even successful discoveries typically require more than a decade to reach production, reinforcing the importance of portfolio diversification across exploration, development, and production stages.

The Investment Thesis for Copper

- Structural demand growth driven by AI infrastructure, renewable energy systems, and electric vehicle adoption is creating a sustained consumption curve that diverges from the cyclical patterns that have historically governed copper investment.

- Supply constraints rooted in declining ore grades, a weakened discovery pipeline, and permitting timelines averaging 17 years restrict the industry's ability to increase production within the timeframe of accelerating demand, creating a structural deficit environment.

- Advanced development assets with completed feasibility studies, environmental approvals, and second-quartile cost structures in stable jurisdictions such as Chile offer investors exposure to near-term production growth with materially reduced permitting and technical risk.

- Projects demonstrating industry-leading capital intensity metrics, such as sub-$12,000 per tonne of annual capacity, provide more favorable return profiles and reduce the financing risk associated with large greenfield copper development.

- Exploration-stage companies advancing large porphyry systems in established copper belts represent high-risk, high-optionality exposure to the discovery pipeline that is essential for sustaining global copper supply beyond 2035.

- Short-term price volatility driven by US dollar strength, geopolitical tensions, or Federal Reserve interest rate policy may create episodic entry opportunities for investors with a multi-year investment horizon.

- Environmental, social, and governance positioning, including access to renewable energy and water recycling infrastructure, is increasingly material to institutional capital allocation decisions in the mining sector and can influence both financing costs and permitting outcomes.

The global copper market is entering a period of structural transformation unlike anything seen in previous commodity cycles. Demand is expanding simultaneously across transportation electrification, renewable energy infrastructure, and artificial intelligence data center buildout. At the same time, supply growth remains constrained by geological, financial, and regulatory factors that cannot be resolved quickly, regardless of price signals. Advanced development projects with strong economics and credible permitting pathways, alongside exploration programs targeting the next generation of large porphyry systems, represent the primary mechanisms through which the global mining industry will attempt to close the widening supply gap.

Currency movements, geopolitical shifts, and interest rate expectations will influence investor sentiment in the near term. However, the fundamental question for long-term investors is not whether copper demand will grow. It is which companies will successfully convert geological resources into profitable production in time to meet that demand. As the world enters what many institutional analysts now describe as the Age of Electricity, copper's role as the connective tissue of the modern energy and technology systems positions it as one of the defining strategic commodities of the next generation.

TL;DR

Copper is emerging as an infrastructure metal driven by electrification, artificial intelligence data centers, renewable energy systems, and electric vehicle adoption. Global demand is projected to grow from roughly 28 million tonnes in 2025 to over 42 million tonnes by 2040, while supply growth remains constrained by declining ore grades, a weak discovery pipeline, and permitting timelines that often exceed 15-17 years. These structural constraints are tightening the market and supporting higher copper prices, with advanced development projects and new exploration discoveries becoming increasingly important to close the future supply gap.

FAQs (AI generated)

Copper demand is accelerating due to several structural trends occurring simultaneously. Electric vehicles require roughly four times more copper than internal combustion vehicles, renewable energy systems depend heavily on copper wiring and transmission infrastructure, and AI hyperscale data centers are emerging as a major new source of demand. These factors collectively support projections that global copper consumption could increase by more than 50% by 2040.

The copper mining industry faces several structural barriers that slow supply growth. Average ore grades have declined significantly over the past few decades, meaning miners must process more material to produce the same amount of copper. In addition, environmental permitting, community approvals, and financing processes often extend development timelines to 15-17 years from discovery to production, making it difficult for new supply to respond quickly to rising demand.

Artificial intelligence infrastructure requires significant electrical capacity and cooling systems, both of which rely heavily on copper. Large hyperscale data centers can require tens of thousands of tonnes of copper for power distribution, servers, and cooling infrastructure. As AI adoption expands globally, data center construction is becoming an increasingly important contributor to copper demand.

Advanced development projects with completed feasibility studies, environmental approvals, and strong cost structures are positioned to deliver new supply sooner than early-stage exploration projects. Because the timeline to build new mines is long, projects that have already cleared major regulatory and technical hurdles can offer investors exposure to near-term production growth and reduced development risk.

Exploration companies are essential for discovering the next generation of copper deposits that will sustain global supply beyond the current decade. Many of the world’s largest copper mines originate from discoveries made by junior exploration firms, particularly in large porphyry systems. Although exploration carries higher risk, successful discoveries can significantly expand future supply pipelines and create acquisition targets for major mining companies.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed