Full Funding & Committed Build: The Re-Rating Case for i-80 Gold

i-80 Gold’s US$4.9B Nevada portfolio trades at a discount due to execution risk, not structural issues, with funded construction and seven catalysts to 2027.

- The five-asset Nevada portfolio carries a total after-tax net present value at a 5% discount rate (NPV5%) of US$4.9 billion at US$3,000 per ounce gold, with per-asset values ranging from US$373 million at Granite Creek Underground to US$2.3 billion at Mineral Point Open Pit across operating, construction, and development stages.

- A first quarter 2026 recapitalisation retired approximately US$165 million in legacy debt obligations and, combined with a May 2025 equity raise, Convertible Senior Notes, a Gold Prepay Facility, and a Franco-Nevada royalty financing, assembled total available capital exceeding US$1.0 billion, funding Phase 1 and Phase 2 development without a requirement for additional equity.

- A full notice to proceed was issued to Hatch Engineering in the first quarter of 2026, following board approval and completion of an AACE Class 3 engineering study across approximately 14,000 cost line items, which commits i-80 Gold to Lone Tree construction and initiates the transition from third-party toll milling at a 55% to 60% payability factor to owner-operated processing at approximately 92% gold recovery.

- Lone Tree is expected to generate US$150 million to US$200 million in net cash flow per year once operational at US$3,000 per ounce gold, anchoring Phase 1 production of 150,000 to 200,000 ounces per year and a phased build-out targeting approximately 600,000 ounces per year by the early 2030s.

- The remaining discount reflects unresolved Environmental Impact Statement (EIS) processes, estimated at approximately 3 years each for Granite Creek Open Pit and Cove Underground; a defined 7-catalyst sequence running from the second quarter of 2026 through late 2027 provides time-bound, observable checkpoints against which execution progress can be assessed.

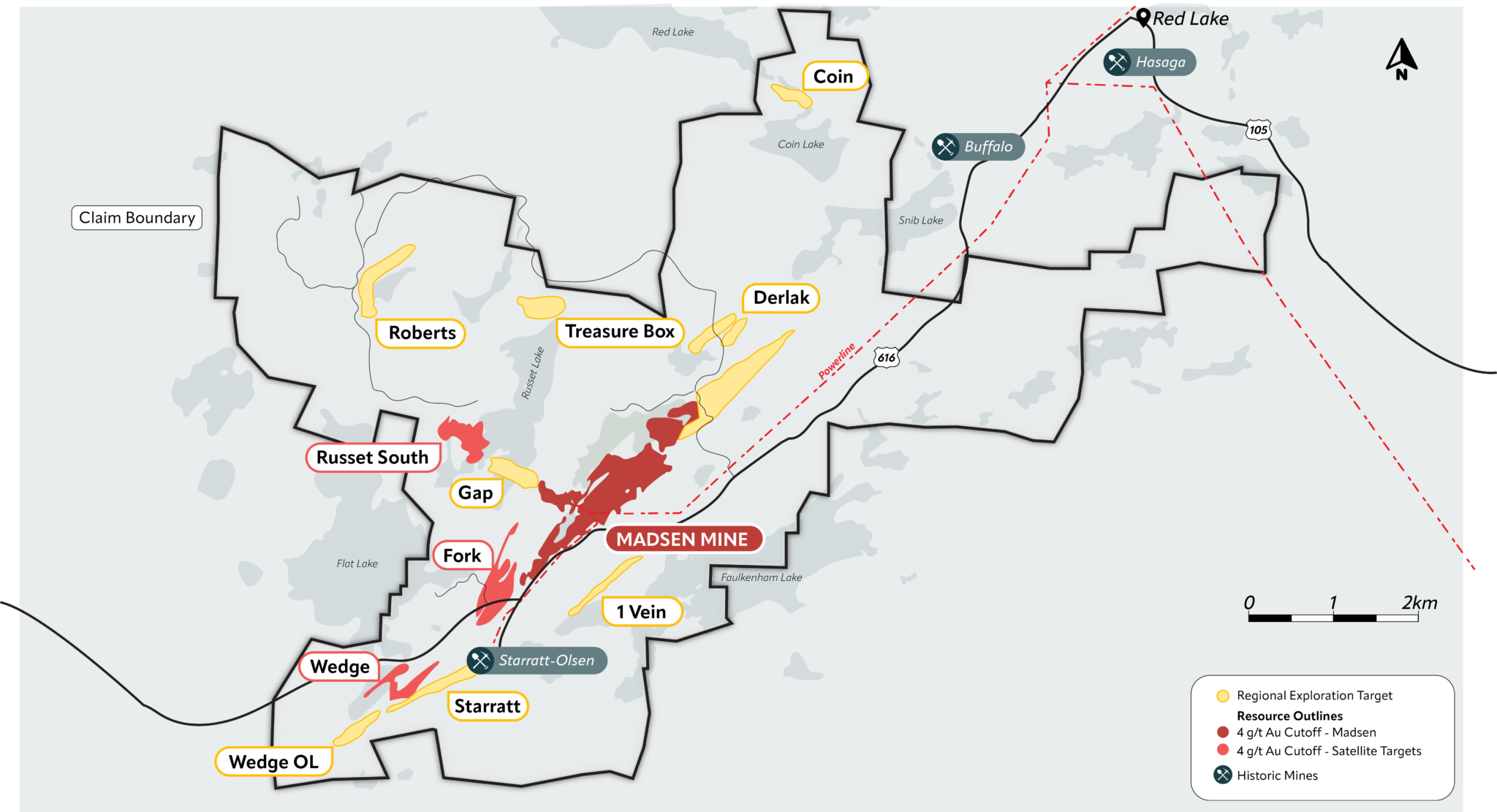

Portfolio Scale & NAV

Nevada ranked first globally for mining investment attractiveness in the 2025 edition of the Fraser Institute Annual Survey of Mining Companies. i-80 Gold (TSX: IAU) holds five assets within that jurisdiction, spanning operating, construction, and development stages, with a combined after-tax net present value at a 5% discount rate (NPV5%) of US$1.6 billion at a base-case gold price of US$2,175 per ounce and US$4.9 billion at US$3,000 per ounce gold and US$35.00 per ounce silver.

Per-asset valuations reflect the portfolio's phased structure. Granite Creek Underground, the Phase 1 operating asset in ramp-up, carries an NPV5% of US$155 million at the base case and US$373 million at the US$3,000-per-ounce assumption. Archimedes Underground, under construction, is valued at US$127 million to US$644 million, with an internal rate of return (IRR) of 81% at the upside price. Cove Underground adds US$271 million to US$626 million at an IRR of 54%; Granite Creek Open Pit contributes US$421 million to US$926 million at an IRR of 52%. Mineral Point Open Pit, the Phase 3 asset, is the portfolio's single largest component, ranging from US$614 million to US$2.3 billion, reflecting both the asset's scale and its long development horizon.

The resource inventory underpinning those figures spans high-grade underground assets at the near term and large-tonnage deposits at the far end. Archimedes Underground holds 436,000 ounces at 7.6 grams per tonne gold Indicated and 988,000 ounces at 7.3 grams per tonne gold Inferred, targeting approximately 100,000 ounces per year over a 10-year mine life. Granite Creek Underground carries 261,000 ounces of gold at 10.5 grams per tonne, Measured and Indicated (M&I), targeting approximately 60,000 ounces per year over 8 years. Mineral Point holds 3.4 million ounces of gold at 0.48 grams per tonne and 104.3 million ounces of silver at 15.0 grams per tonne, Indicated, with a production target of approximately 280,000 gold equivalent ounces per year over 17 years.

Capital Structure & Financing

The financing uncertainty that constrained the investment case through much of 2024 and early 2025 has been resolved through a sequenced series of transactions. In May 2025, i-80 Gold completed an equity raise of approximately US$300 million through a public offering and a private placement. That was followed by Convertible Senior Notes of approximately US$288 million at 3.75% due 2031, a US$250 million Gold Prepay Facility arranged with National Bank and Macquarie Bank, and a US$250 million Franco-Nevada royalty financing carrying a 1.5% life-of-mine Net Smelter Return stepping up to 3.0% in January 2031 across all properties, with US$50 million of those proceeds specifically allocated to advance Mineral Point in 2026. An Orion Mine Finance Silver Purchase and Sale Agreement for silver streaming remains in place.

The first quarter 2026 recapitalisation retired approximately US$165 million of legacy debt, comprising existing convertible debentures, an Orion Gold Prepay Agreement, and a Convertible Loan. Current debt stands at US$175 million, with US$63 million cash on hand. Total available capital secured exceeds US$1.0 billion, and the company is fully funded through Phase 1 and Phase 2 development plans without requiring additional equity. Separately, the initial US$150 million drawdown under the Gold Prepay Facility is structured for repayment through the delivery of approximately 40,000 ounces of gold over 30 months commencing in January 2028. Management has indicated intent to transition the prepay facility into a corporate revolver to fund Mineral Point.

Lone Tree Construction & Processing Economics

The board granted a positive construction decision for Lone Tree in the first quarter of 2026, supported by an AACE Class 3 engineering study covering approximately 14,000 cost line items. Total estimated capital cost is approximately US$430 million, including capital spares and approximately 12% contingency. The full notice to proceed was issued to Hatch Engineering concurrent with that decision.

Chief Operating Officer of i-80 Gold, Paul Chawrun, described the transition from the limited notice to proceed issued to Hatch in August 2025 to the full board-approved instruction:

"We did indicate that we had a limited notice to proceed back last August with Hatch, and what that means is that we're basically moving ahead with the construction part of the project to get the detailed engineering put together, the execution plan, and so now we've provided Hatch engineering with a full notice to proceed with board approval and we're actually moving the execution plan ahead from what we had indicated before."

The construction decision removes the previously primary structural question in the investment case. What remains is execution risk, a materially different category. The transition from third-party toll milling, which applies a 55% to 60% payability factor to refractory material, to owner-operated processing with an average gold recovery of approximately 92% results in a difference in recoverable gold per tonne that holds across a range of price assumptions. The payback period on the approximately US$430 million capital cost is estimated at 12 to 24 months.

Production Profile & Cash Flow Mechanics

Chawrun outlined Lone Tree's projected output and expected annual cash generation:

"We'll have the Lone Tree plant producing gold by the end of 2027 with a bit of a ramp-up in 2028, and in the range of about 150,000 (depending on the grade) to maybe 160,000 ounces per year at good margins. So if you take a look at the gold price now, I think we estimated somewhere around 150 to 200 million net cash flow per year once it operates at somewhere in the range of $3,000 gold."

That US$150 million to US$200 million in projected net annual cash flow from Lone Tree anchors the Phase 1 portfolio production profile of 150,000 to 200,000 ounces per year. Phase 2 targets 300,000 to 400,000 ounces per year; Phase 3 targets approximately 600,000 ounces per year by the early 2030s. The phased structure means the Lone Tree cash flow event in 2028 becomes the initial internal capital source for Phase 2 and Phase 3 development, reducing the company's reliance on equity markets at each subsequent stage.

Permitting, Feasibility & Proof Requirements

Three categories of open requirements underpin that residual gap. The first is permitting. The Environmental Impact Statement (EIS) process for Granite Creek Open Pit and the EIS for Cove Underground are each estimated to take approximately 3 years. Lower Archimedes permitting, a nearer-term requirement, is estimated to be completed by mid-2027. These timelines are outside the company's direct control and may be extended.

The second is feasibility conversion. Feasibility studies for Granite Creek Underground and Cove Underground are expected in the second quarter of 2026; an Archimedes Underground feasibility study is expected in the first quarter of 2027; and a Pre-Feasibility Study or Feasibility Study for Mineral Point is targeted for the first half of 2027, though timing is under review. Until those studies are complete, the NPV5% figures for the corresponding assets rest on less definitive engineering.

The third category is resource conversion. Inferred resources across the portfolio carry geological uncertainty and cannot have economic considerations formally applied until upgraded to M&I or reserve status. Commodity price volatility, groundwater management uncertainties at Granite Creek, construction cost overrun exposure at Lone Tree, and the terms of any future capital requirements are additive financial and technical risks. None of these risks is eliminated by the recapitalisation or the construction decision. They are the substantive basis for the remaining discount.

Catalyst Sequence & Re-Rating Conditions

What distinguishes the current investment case from the pre-recapitalisation period is the existence of a dated, observable milestone sequence. Seven catalysts run from the second quarter of 2026 through late 2027. Lone Tree demolition commences, and Lower Archimedes infill drilling initiates in the second quarter of 2026. First gold from Upper Archimedes is targeted for the third quarter of 2026. Lone Tree main construction commences in the second half of 2026.

The US$100 million accordion feature on the Gold Prepay Facility is expected to be executed in the first half of 2027. Lower Archimedes permitting is estimated to be completed by mid-2027. First gold pour at Lone Tree and wet commissioning are targeted for late 2027, with production ramp-up into the first quarter of 2028.

Chawrun set out the expected timeline for Mineral Point's construction and production:

"I believe we've estimated 2029 for the initiation of construction for Mineral Point, with 2032 for gold production. This is part of what this capital raise provides for us: to do the drilling, get that done sooner, and to start the EIS process sooner, and that hasn't happened yet because it takes a little bit of time, but that would allow us to accelerate the timeline for Mineral Point by anywhere from one to two years."

Each catalyst in the sequence is independently verifiable against a time-stamp. A feasibility study delivered on schedule converts an NPV5% figure from a Preliminary Economic Assessment (PEA) into a bankable estimate; a first gold pour at Lone Tree converts a construction timeline into a cash flow event. Neither of those benchmarks existed in dated form prior to the recapitalisation and full notice to proceed. They do now, and each milestone met reduces the factual basis for the remaining discount.

The Investment Thesis for i-80 Gold

- The AACE Class 3 engineering study at Lone Tree and the full notice to proceed issued to Hatch Engineering convert the US$4.9 billion after-tax net present value at a 5% discount rate at US$3,000 per ounce gold from a projection contingent on a construction decision into a figure against which a funded, board-sanctioned build programme is now being executed.

- The first quarter 2026 recapitalisation retired approximately US$165 million in legacy debt and, in combination with over US$1.0 billion in total available capital, eliminated the financing uncertainty that previously served as a structural basis for the valuation discount, leaving future equity dilution as the residual financial risk rather than the primary one.

- The full notice to proceed issued to Hatch Engineering represents a board-sanctioned, capital-committed transition from toll-milling economics at a 55% to 60% payability factor to owner-operated processing at approximately 92% gold recovery, a change in per-ounce economics that is quantifiable and independent of short-term gold price assumptions.

- The transition from structural uncertainty to execution risk changes the nature of the valuation gap: execution risk is addressable against a dated catalyst sequence, whereas structural uncertainty is not, and the seven catalysts identified between the second quarter of 2026 and late 2027 provide a framework against which progress can be monitored and discounted in real time.

- The approximately three-year Environmental Impact Statement timelines for Granite Creek Open Pit and Cove Underground, and the requirement to convert inferred resources to Measured and Indicated and reserve status across multiple assets, constitute the substantive basis for the remaining discount and are not eliminable by management action in the near term.

- The US$150 million to US$200 million in expected annual net cash flow from Lone Tree at US$3,000 per ounce gold, once ramp-up is complete in 2028, would establish an internal funding mechanism for Phase 2 and Phase 3 development that reduces reliance on equity markets at each subsequent construction decision, a structural shift in capital allocation that is not yet priced into the current enterprise value.

TL;DR

i-80 Gold entered the second quarter of 2026 having resolved the two uncertainties that most clearly justified its discount to portfolio net asset value: financing capacity and the Lone Tree construction decision. The first quarter 2026 recapitalisation retired approximately US$165 million in legacy debt, and total available capital exceeding US$1.0 billion removes the requirement for additional equity through Phase 2 development. The full notice to proceed issued to Hatch engineering commits i-80 Gold to a construction path that, if executed on schedule, targets a first gold pour at Lone Tree in late 2027 and approximately US$150 million to US$200 million in annual net cash flow at US$3,000 per ounce gold. The residual discount is now anchored in EIS timelines of approximately 3 years each for Granite Creek Open Pit and Cove Underground, as well as in the engineering conversion work required to advance inferred resources toward reserve status. Whether that discount closes against a total after-tax NPV5% of US$4.9 billion depends on execution against a seven-catalyst sequence that is, for the first time, both dated and fully funded.

FAQs (AI-Generated)

The recapitalisation retired approximately US$165 million in legacy debt and, combined with equity, notes, a Gold Prepay Facility, and Franco-Nevada royalty financing, assembled over US$1.0 billion in available capital. The practical effect is that the company no longer requires additional equity to fund Phase 1 or Phase 2 development, removing the financing uncertainty that previously constituted a structural basis for the valuation discount and recharacterising the remaining gap as execution risk.

The US$1.6 billion to US$4.9 billion range reflects the sensitivity of large, lower-grade open-pit assets to changes in the gold price. Mineral Point Open Pit's after-tax NPV moves from US$614 million at US$2,175 per ounce to US$2.3 billion at US$3,000 per ounce, accounting for the majority of the portfolio-level variance. High-grade underground assets, while showing a narrower relative range, remain material contributors at both price assumptions.

Current third-party toll milling applies a 55% to 60% payability factor to refractory material from i-80 Gold's Nevada operations. Lone Tree owner-operated processing targets approximately 92% average gold recovery, a materially higher recoverable gold per tonne processed. At the steady-state scale, that recovery differential is the primary mechanism by which the projected US$150 million to US$200 million in net annual cash flow is generated.

The primary risks are Lone Tree construction cost overruns or schedule delays, EIS timelines that could each run approximately 3 years for Granite Creek Open Pit and Cove Underground, and the geological uncertainty inherent in converting inferred resources to M&I and reserve status across multiple assets. Commodity price volatility and the potential terms of any future capital requirements are additive financial risks that the funded position mitigates but does not eliminate.

The late 2027 first gold pour is the point at which the Lone Tree construction decision converts from capital expenditure to cash generation. At steady-state operation in 2028, the facility is expected to produce 150,000 to 160,000 ounces per year and generate US$150 million to US$200 million in net cash flow annually at US$3,000 per ounce gold, providing an internal capital base for Phase 2 and Phase 3 development and reducing the company's dependence on external equity markets at each subsequent construction stage.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed