US and Iran Ceasefire Lifts Copper to US$6/lb, But Smelter Margin Collapse Points to Tighter Supply Ahead

Copper recovers to US$6/lb on geopolitical easing, but negative US$77/t TC/RCs and China's sulphuric acid export ban signal tightening refined supply.

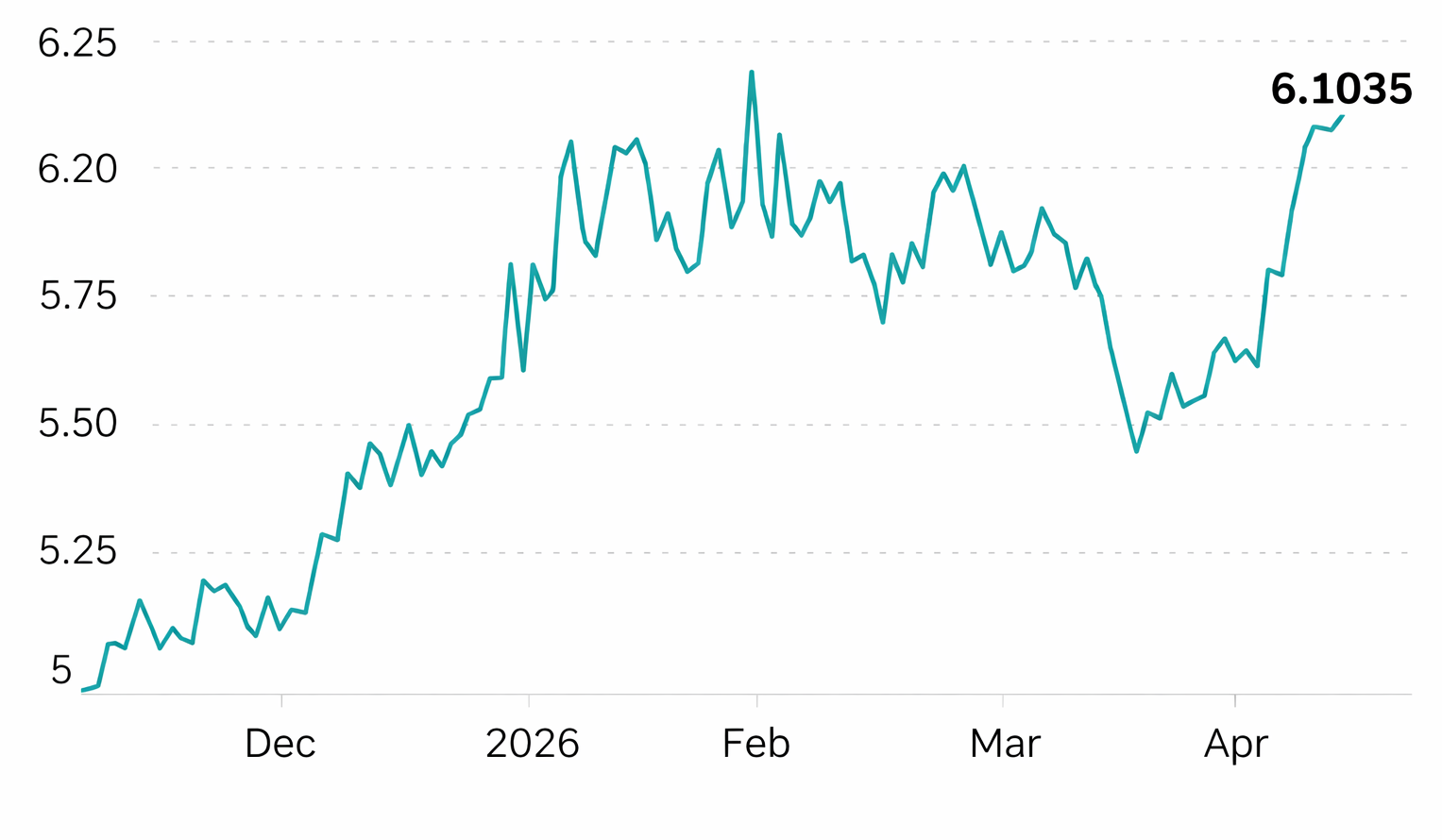

- Copper has recovered to approximately US$6/lb following an easing of US-Iran geopolitical tensions, but this price movement reflects a shift in macro sentiment rather than a change in the underlying supply-demand balance.

- China reduced total inbound copper shipments to 125,350 tonnes in February 2026, the lowest level since April 2011, as buyers stepped back from elevated prices and redirected exports into international markets, with January-to-February export volumes reaching 172,000 tonnes against 49,000 tonnes in the comparable prior-year period.

- Treatment and refining charges fell to negative US$77/t as of April 10, 2026, reflecting a structural imbalance in which global smelting capacity significantly exceeds available copper concentrate supply.

- Bloomberg reported that China plans to halt sulphuric acid exports starting in May 2026, removing a byproduct revenue stream that has subsidised loss-making smelter operations and, if sustained, would eliminate the economics keeping marginal capacity online.

- Smelter economics at negative US$77/t TC/RC, combined with a reported May 2026 Chinese sulphuric acid export ban, create a production cut mechanism that improves returns for development assets with permitted concentrate supply.

Geopolitical Easing & Copper's Price Response

The United States and Iran agreed to ceasefire terms in April 2026, removing the Strait of Hormuz disruption risk that had kept oil prices above what supply-demand conditions alone justified and, by extension, inflated near-term copper demand forecasts, driving copper's recovery to approximately US$6/lb without any change in concentrate availability or smelter economics. This sequence drew speculative and physical buyers back into the copper market, producing a rebound from the correction that followed copper's nominal all-time high of US$14,527/t on the LME in January 2026.

EVs, grid infrastructure, and renewable energy do not insulate against price corrections: the retreat from US$14,527/t in January 2026 to approximately US$6/lb by April confirms that overextended entry points carry drawdown risk regardless of long-term consumption drivers. Monthly Chinese import volumes, TC/RC levels, and exchange inventory trajectories are the primary indicators for benchmarking whether a given price level reflects underlying supply conditions.

China's Market Power: The Buyer's Strike That Reset Prices

China is the world's largest consumer of refined copper, and its behavior in early 2026 constitutes a structural signal rather than a cyclical anomaly. When prices surged toward the January 2026 high, Chinese buyers withdrew materially from international markets. Total inbound copper shipments fell to 125,350 tonnes in February 2026, the lowest reading since April 2011, and January-to-February import volumes declined 25% year-over-year. Simultaneously, Chinese exports of refined copper reached 172,000 tonnes in the January-to-February period, up from 49,000 tonnes in the same period of the prior year, as domestic producers redirected surplus into markets where international pricing remained more favorable.

This behavior reflects a deliberate strategy: avoid purchasing at elevated international prices, maximize utilization of domestic refining capacity, and deploy export volumes when the margin justifies it. China's February 2026 withdrawal, imports falling to 125,350 tonnes, the lowest since April 2011, demonstrates that at prices above physical equilibrium, the world's largest buyer reduces offtake with sufficient scale to reverse speculative momentum.

China's willingness to withdraw at elevated prices means that copper's effective ceiling is set by Chinese end-user economics, not by supply scarcity alone - and that positions sized against the structural thesis require a Chinese import data trigger to confirm demand resumption before adding exposure.

Inventory Build & Supply Chain Rebalancing

The scale of the current inventory build across Western and Chinese exchange systems provides quantitative confirmation of the market imbalance. LME copper inventories reached 385,275 tonnes as of March 2026, an eight-year high, while Shanghai Futures Exchange inventories reached 433,500 tonnes in early March 2026, surpassing the previous record set in 2020. Both figures are the result of the same sequence: reduced Chinese import demand, elevated domestic production, and export flows redirected to LME-registered warehouses as domestic inventory capacity filled.

The ICSG's October 2025 forecast projects that supply tightness slows refined output growth from 3.4% in 2025 to 0.9% in 2026, a deceleration that is not reversed by elevated exchange inventories. Chile's government stated in April 2026 that it is targeting copper output above earlier projections through permitting reform, a supply-side policy response that confirms the deficit is structural rather than cyclical, since governments accelerate permitting when they cannot close a gap through existing production.

The Smelter Margin Squeeze: A Critical Inflection Point

Treatment and refining charges represent the fees mining companies pay smelters to convert copper concentrate into refined metal. Spot TC/RCs fell to negative US$77/t as of April 10, 2026, reflecting an imbalance in which global smelting capacity far exceeds the available supply of copper concentrate. At this level, smelters are effectively subsidizing miners for the right to process their output, which is unsustainable without an offsetting revenue source. Chinese smelters have remained operational through this environment primarily because sulphuric acid, a byproduct of copper smelting, has commanded strong prices driven by demand from the battery sector and fertilizer production.

Bloomberg has reported that China plans to ban sulphuric acid exports starting in May 2026 to protect domestic fertilizer supply. If confirmed, restricted acid exports would increase domestic availability, compress domestic acid prices, and eliminate the byproduct margin that has sustained smelters through negative TC/RCs. The probable operational response would be production cuts or maintenance shutdowns, which would reduce refined copper output and provide a grounded basis for medium-term price recovery. Investors should note that this policy has not been confirmed by an official Chinese government statement, and the timeline and scope remain subject to change.

Development Assets: Capital Efficiency & Permitting Progress

Marimaca Copper is advancing a near-term oxide development project in Chile's Antofagasta Region. The Definitive Feasibility Study published on August 25, 2025 confirms a net present value at an 8% discount rate of approximately US$1.1 billion, an internal rate of return of 39%, and a payback period of 2.2 years, based on a copper price assumption of US$5.05/lb Cu using a three-month average COMEX spot price plus a US$0.10/lb cathode premium. Capital intensity is US$11,700/tpa Cu production and C1 cash costs are approximately US$1.69/lb. In November 2025, Marimaca received its Resolución de Calificación Ambiental covering the Marimaca Oxide Deposit, a de-risking milestone for the project's development timeline.

Hayden Locke, President and Chief Executive Officer of Marimaca Copper, describes the significance of the DFS completion and permitting milestone:

"We delivered the DFS, which is really the final piece of the puzzle before we start transitioning into the financing and then detailed design and engineering for the Marimaca oxide deposit. It confirmed what we already knew, which is industry-leading capital costs, very competitive operating costs, and industry-leading return on invested capital metrics."

The company is advancing toward a Final Investment Decision, with site early works pre-FID identified for 2026, subject to financing completion. Hayden Locke addresses the capital position supporting that process:

"We raised C$80 million from Australian, Canadian, and US investors, and it was really well-received, massively oversubscribed... We're very comfortable with our cash position. We don't have to think about raising money for the short to medium term."

Exploration Upside: The Scarcity Premium in High-Grade Discoveries

Abitibi Metals Corp is advancing its B26 copper-gold deposit in Quebec's Abitibi region, a jurisdiction ranked 22nd out of 68 globally on the Fraser Institute Annual Survey of Mining Companies 2025. The current resource estimate, with an effective date of January 1, 2026, and reviewed by Qualified Person Laurent Eustache, P.Geo, under NI 43-101, includes 12.96 million tonnes indicated at 2.08% copper equivalent and 12.34 million tonnes inferred at 2.20% copper equivalent.

Jon Deluce, Chief Executive Officer and Founder of Abitibi Metals, describes both the current resource and the geological factors supporting further expansion:

"Looking at the 13 million tonnes indicated at 2.1% copper equivalent, 12.3 million tonnes inferred at 2.2%, and the growth in this resource has come from inferred... Our thesis has been this could very well be a 30 to 50 million ton deposit."

Hybrid Development Models: Near-Term Cash Flow & Long-Term Upside

Fitzroy Minerals offers a differentiated exposure profile by combining a low-capital heap leach joint venture with longer-dated porphyry exploration upside. The Buen Retiro heap leach project is structured as a joint venture with Pucobre S.A., under which Fitzroy holds an option for 100% of the project subject to a 30% clawback option available to Pucobre contingent on minimum eligible expenditures, as confirmed in Fitzroy's April 2026 corporate presentation. This structure provides a near-term pathway to cash flow generation from oxide material with limited upfront capital. The Caballos project is characterized as a copper-molybdenum-gold-rhenium porphyry system in Fitzroy's April 2026 corporate presentation, with technical information reviewed by Qualified Person Dr. Scott Jobin-Bevans under NI 43-101, providing leverage to the structural concentrate deficit driving the smelter margin compression described above.

Conditions That Would Eliminate the Case for Refined Copper Supply Tightening

The primary demand-side risk is a global recession reducing industrial activity sufficiently to suppress copper consumption despite constrained supply. On the policy side, the sulphuric acid export ban has not been confirmed by a formal Chinese government statement; if the policy is delayed or reversed, the primary near-term catalyst for refined copper supply tightening is removed. Similarly, if TC/RCs recover materially without production shutdowns, the supply tightening mechanism does not activate. The thesis also weakens if LME and ShFE inventories continue to build despite smelter stress, indicating that demand weakness is more persistent than current data suggests. Monthly Chinese import volumes, TC/RC levels per Argus, and exchange inventory trajectories are the primary indicators against which investors should benchmark the ongoing validity of this thesis.

The Investment Thesis for Copper

- Smelter treatment charges at negative US$77/t as of April 10, 2026 per indicate that concentrate supply is structurally insufficient relative to global refining capacity, and a reported Chinese sulphuric acid export ban, if confirmed, would eliminate the byproduct revenue sustaining unprofitable smelters and create a mechanism for production cuts that tighten refined copper supply.

- LME inventories at an eight-year high and ShFE inventories above their previous 2020 record reflect a demand timing mismatch driven by China's price-sensitive buyer behavior rather than structural oversupply, and are expected to normalize as physical demand resumes at lower price thresholds.

- Development projects with strong DFS economics, such as Marimaca Copper's Marimaca Oxide Deposit, confirmed at a 39% IRR and US$11,700/tpa capital intensity at a US$5.05/lb copper base case, maintain viable returns across a wide range of price scenarios and improve further under supply tightening conditions.

- Heap leach joint venture structures provide near-term oxide cash flow at limited upfront capital while retaining porphyry exploration exposure, a model that captures both current refined copper economics and longer-dated leverage to concentrate deficit conditions without requiring full project capital commitment at either stage.

- Quebec ranks among jurisdictions where permitting risk is quantifiably lower: the Fraser Institute's Annual Survey of Mining Companies 2025 places Quebec 22nd out of 68 jurisdictions globally.

- Macro-driven price volatility across the January-to-April 2026 range creates entry points for investors with a disciplined view of cost structure, permitting status, and supply catalysts, but requires ongoing monitoring of TC/RC levels and Chinese import data as the primary falsification indicators.

Copper's recovery to approximately US$6/lb reflects a reduction in geopolitical risk rather than a change in supply-demand conditions. Treatment charges at negative US$77/t and the reported May 2026 sulphuric acid export ban combine to create a potential mechanism for refined copper supply tightening grounded in fundamentals rather than sentiment. China's price-sensitive behavior in early 2026 has confirmed that physical demand sets a practical ceiling on speculative price moves, while also confirming that demand remains robust and price-responsive at lower thresholds. Identifying where cost efficiency, permitted status, and resource quality align with that supply cycle will determine where durable value is created across the copper investments.

TL;DR

Copper's April 2026 recovery to approximately US$6/lb reflects US-Iran ceasefire sentiment, not a change in supply fundamentals. TC/RCs at negative US$77/t confirm concentrate supply is structurally insufficient relative to global smelting capacity, and a reported Chinese sulphuric acid export ban — if confirmed — removes the byproduct subsidy keeping loss-making smelters operational. China's February 2026 buyer withdrawal, with imports falling to 125,350 tonnes, the lowest since April 2011, confirms physical demand sets a practical price ceiling. Elevated LME and SHFE inventories reflect a demand timing mismatch, not structural oversupply. Development assets with permitted status, strong DFS economics, and defined concentrate supply are best positioned as refined copper supply tightens.

FAQs (AI-Generated)

The recovery reflects a geopolitical risk premium unwinding following US-Iran ceasefire terms in April 2026, which removed the Strait of Hormuz disruption scenario that had kept oil prices and industrial demand forecasts above fundamental levels. Concentrate availability, smelter economics, and Chinese import demand are unchanged.

Treatment and refining charges at negative US$77/t as of April 10, 2026 mean smelters are effectively paying miners for the right to process concentrate rather than earning a processing fee — an unsustainable position that historically precedes production cuts or maintenance shutdowns, which would reduce refined copper output.

Sulphuric acid, a byproduct of copper smelting, has provided the margin offsetting negative TC/RCs for Chinese smelters. A confirmed ban starting May 2026 would compress domestic acid prices, eliminate that offset, and remove the primary revenue source sustaining loss-making smelter operations — creating a direct mechanism for refined copper supply tightening.

No. LME inventories at an eight-year high and SHFE inventories above their 2020 record reflect China's deliberate withdrawal from elevated-price markets and tariff-driven redistribution of refined metal to COMEX warehouses — not a durable reduction in end-use demand. The ICSG's October 2025 forecast projects a 150,000-tonne refined copper deficit in 2026, driven by concentrate constraints that slow refined production growth from 3.4% in 2025 to 0.9% in 2026.

Monthly Chinese import volumes, TC/RC levels per Argus, and LME and SHFE exchange inventory trajectories are the primary indicators. A confirmed sulphuric acid export ban, TC/RC recovery without accompanying production shutdowns, or sustained inventory builds despite smelter stress would each require a reassessment of the supply tightening case.

Analyst's Notes

Subscribe to Our Channel

Stay Informed