Atlas Salt: North America's Next Major De-Icing Producer

Atlas Salt advances North America's first new salt mine in 30 years amid rising prices and supply constraints, targeting $920M NPV with 4 Mtpa production capacity.

- Atlas Salt is developing the Great Atlantic Salt Project in Newfoundland, Canada - North America's first new salt mine in nearly three decades - with 4 million tonnes per annum (Mtpa) nameplate production capacity targeting the import-dependent eastern seaboard de-icing market.

- The September 2025 Updated Feasibility Study demonstrates robust economics with after-tax net present value (NPV8) of $920 million, internal rate of return (IRR) of 21.3%, and average annual post-tax cash flow of $188 million over a 24.3-year mine life.

- Recent price increases by American Rock Salt ($25 per tonne) and persistent supply constraints underscore the structural deficit in North American de-icing salt supply, with the continent importing 8-10 Mtpa annually to meet demand.

- The project's Newfoundland location provides significant cost and logistics advantages, enabling salt delivery to Boston in 3 days versus 14+ days from Chile or Egypt, while leveraging established port, road, and electricity infrastructure.

- With environmental assessment completed, strategic partnerships secured with Scotwood Industries, Sandvik, and Hatch, and current enterprise value of $65.5 million versus after-tax NPV of $920 million, Atlas Salt offers substantial re-rating potential as the project advances toward production estimated by 2030.

Introduction: Winter's Essential Commodity Faces Supply Crunch

The December 2025 news that American Rock Salt raised commercial road salt prices by $25 per tonne amid early winter demand has focused renewed attention on North America's critical de-icing salt supply chain. Small businesses in upstate New York reported immediate margin pressure, with Girl Plower owner Gina Dandrea noting the increase directly impacts snow removal service economics. One contractor had already consumed 40 tonnes from private stockpiles by early December, indicating unusually early seasonal consumption.

This pricing pressure arrives against a backdrop of structural supply constraints. Cargill's historic Avery Island salt mine in Louisiana - producing since the mid-1800s - ceased operations in 2021, removing 2.5 million tonnes per year of domestic supply from the U.S. east coast de-icing market. The company's remaining New York and Cleveland salt assets have remained unsold since 2023 due to environmental concerns, with potential closure threatening to remove approximately 2 million additional tonnes annually. Meanwhile, American Rock Salt's facility in New York, which opened in 2001, remains the newest salt mine to commence operations in over 50 years at that time.

Against this supply-constrained backdrop, Atlas Salt Inc. (TSXV: SALT) is advancing North America's first new salt mine in nearly 30 years. The Great Atlantic Salt Project in Newfoundland represents a rare opportunity to add significant, long-life domestic salt production precisely as legacy mines face operational challenges and aging infrastructure issues. The convergence of rising prices, supply disruption, and decades without new capacity creates a compelling market entry point for Atlas Salt's strategically positioned asset.

Company Overview: Developing a World-Class Salt Resource

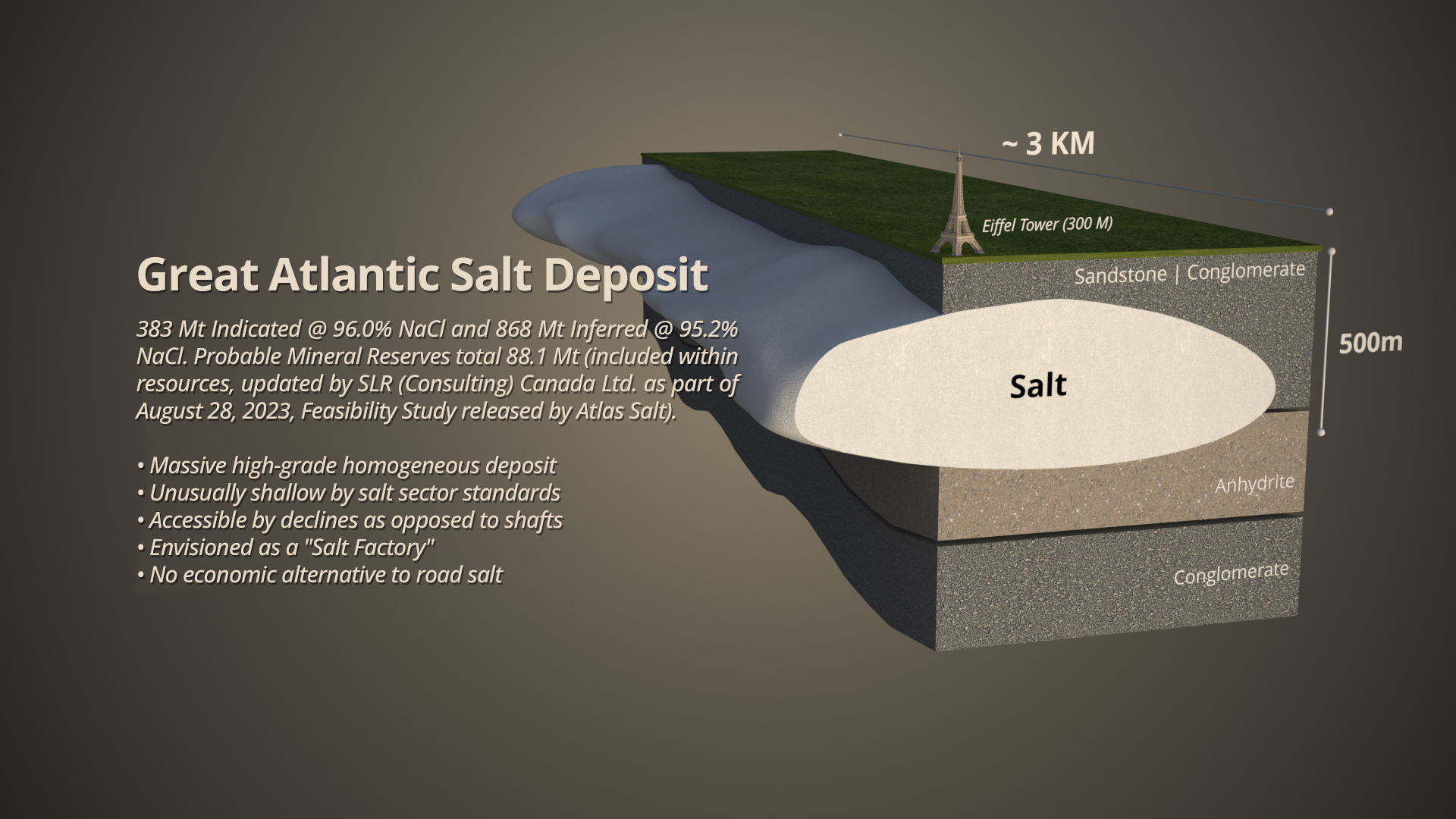

Atlas Salt controls one of North America's highest-purity salt deposits through its Great Atlantic Salt Project located near St. George's, Newfoundland. The company holds Probable Reserves of 95.0 million tonnes grading 95.9% sodium chloride (NaCl), with an additional 868 million tonnes of Inferred resources averaging 95.2% NaCl. The shallow deposit - accessible at approximately 180 meters depth - enables efficient mining via declines rather than costly shaft sinking, providing significant capital and operational advantages over legacy North American salt mines that typically operate 350 to 1,000 meters below surface.

The project benefits from exceptional geology characterized by homogeneous, high-grade salt with average thickness of 200 meters (ranging 68 to 340 meters). Resource modeling indicates tremendous continuity across the deposit, with significant concentrations of high-grade reserves exceeding 98% NaCl concentrated around the "pillow" shape within the broader salt horizons. This geological consistency supports efficient room-and-pillar mining with minimal grade variability and no chemical processing requirements. The operation relies entirely on physical screening and sizing underground.

Atlas Salt's management team combines deep mining development experience with salt industry expertise. CEO Nolan Peterson brings over 20 years in mine development, operations, and finance, having previously served as CEO of World Copper where he advanced over $1 billion in assets. Project Director and General Manager Andrew Smith contributes more than 10 years in underground mine construction, having led over $500 million in project builds as former Head of PMO at Dumas. Director Rowland Howe, a salt industry veteran, led Compass Minerals' Goderich mine to record production of 7.5 million tonnes per year, providing critical operational expertise specific to large-scale salt mining. This combination of mining development and commodity-specific operational knowledge positions the team to execute the project through construction and commissioning.

Key Development: Updated Feasibility Study De-Risks Project

Atlas Salt released its Updated Feasibility Study in September 2025, significantly improving project economics compared to the 2023 baseline study. The updated analysis shortened mine life to 24.3 years from 34 years, pulling forward production and cash flow realization while reducing reliance on longer-term price forecasts. Average annual production capacity increased over 60% to 4.0 Mtpa from 2.5 Mtpa, with after-tax NPV8 rising 66% to $920 million from $553 million despite a 5% reduction in life-of-mine average selling price per tonne.

The study incorporated feedback from Newfoundland's environmental assessment process, which released the project with conditions in April 2024 after only approximately two months of review. Engineering refinements included optimized production profiles, improved drift design, port and logistics enhancements, and integration of Sandvik battery electric mining equipment. The updated sales mix prioritizes higher-margin direct sales over bulk commodity sales, contributing to improved unit economics with net revenue per tonne of $109.40 and all-in sustaining cost (AISC) of $34.90 FOB Turf Point.

Capital expenditure estimates reflect current market conditions with pre-production costs of $589 million and life-of-mine sustaining capital of $609 million. Operating costs of $28.20 per tonne shipped benefit from the shallow deposit depth, established infrastructure access, and clean hydroelectric power availability in Newfoundland. Payback period of 4.2 years and post-tax IRR of 21.3% demonstrate robust project returns even at conservative base-case salt pricing of $81.67 per tonne, which sits below current spot pricing levels following recent industry increases. The economics improve substantially at higher price scenarios, with after-tax NPV8 reaching $1.5 billion at $89.84 per tonne pricing.

Strategic Significance: Addressing North America's Import Dependency

North America currently imports 8 to 10 million tonnes per annum of de-icing salt, primarily from Chile, Egypt, Mexico, and Caribbean sources. United States Geological Survey data shows 67.5 million tonnes of salt imported to the United States from 2020 through 2023, with Chile supplying 27%, Canada 29%, Mexico 14%, Egypt 8%, and other sources comprising 22%. This import dependency creates supply chain vulnerabilities, extended shipping times, and exposure to international logistics disruptions. These factors became particularly evident during 2024's early-season shortage that prompted American Rock Salt to implement weekend production shifts.

The Great Atlantic Salt Project's location in Newfoundland positions it to serve Atlantic Canada, Quebec, and the U.S. east coast - markets with combined annual road salt consumption of 11 to 16 million tonnes according to the project feasibility study. Shipping distance to Boston requires less than 3 days versus over 14 days from Egypt or Chile, reducing transportation costs, carbon footprint, and inventory requirements for customers. The operation's proximity to end markets minimizes the cost-insurance-freight (CIF) to free-on-board (FOB) spread that benefits overseas producers shipping to North American ports. This logistics advantage translates to estimated transportation cost savings of $10-15 per tonne compared to international alternatives.

Newfoundland's status as a Tier-1 mining jurisdiction enhances project attractiveness. The Fraser Institute ranked Newfoundland and Labrador as the 9th best mining jurisdiction globally in 2025 based on mineral potential and government policy alignment. The province hosts active development projects from major mining companies including Equinox Gold's Valentine Gold Project (via Calibre Mining acquisition), Eldorado Gold's joint venture with Tru Precious Metals, and FireFly Metals following a $100 million financing with BMO in June 2025. This mining-friendly environment provides regulatory certainty and established permitting processes that Atlas Salt has successfully navigated through its environmental assessment and Early Works Development Plan approval.

Current Activities: Strategic Partnerships and Financing Progress

Atlas Salt has secured three cornerstone partnerships that validate the project's commercial and technical viability. In August 2024, the company announced a Memorandum of Understanding with Scotwood Industries LLC targeting salt offtake volumes of 1.25 to 1.5 Mtpa. Scotwood, the largest distributor of packaged retail de-icing salt in the United States, provides immediate market access and validates Atlas Salt's ability to serve both bulk municipal customers and higher-margin retail distribution channels. This offtake agreement covers approximately 31-38% of planned nameplate production capacity, providing revenue visibility and supporting project financing efforts.

Equipment supply and financing arrangements with Sandvik, announced in September 2024, cover $73 million worth of mining equipment and engineering support. Sandvik, a global high-tech engineering group serving manufacturing, mining, and infrastructure industries, brings extensive experience in underground hard rock and soft rock mining operations. The partnership includes provision of battery electric vehicles for underground operations, supporting Atlas Salt's all-electric mine design powered by clean Newfoundland hydroelectricity. This configuration positions the operation among the lowest greenhouse gas intensity mines globally at just 950 tonnes CO2 equivalent per million tonnes of ore production, compared to industry averages exceeding 40,000 tonnes CO2e for gold operations and 80,000 tonnes CO2e for base metals.

"We are developing a world-class salt mine with nameplate production capacity of 4 million tonnes per annum, which will be the newest salt mine in North America in approximately 30 years. Our strategic location in Newfoundland, combined with close proximity to the import-dependent North American market, positions us to serve a critical infrastructure need while delivering compelling economics for our shareholders."

In November 2025, Atlas Salt formalized Hatch Ltd. as Lead Engineering Partner and Integrated Project Delivery Partner. Hatch brings proven experience delivering the world's largest soft-rock mines and maintains existing presence in Newfoundland through other mining projects. This partnership provides critical detailed engineering expertise as the project transitions from feasibility stage toward construction readiness. The company has also engaged Endeavour Financial for project financing, progressing toward securing the $589 million pre-production capital requirement through a combination of debt and potential strategic equity partnerships.

Market Context: Structural Deficit Meets Supply Disruption

The North American salt market fundamentals continue strengthening as aging infrastructure, environmental challenges, and lack of new production collide with steady demand growth. Fortune Business Insights forecasts the global salt market will expand at 4.2% compound annual growth rate through 2032, with de-icing applications remaining a core demand driver. United States Geological Survey data shows American Rock Salt's New York facility, the most recent major salt mine to open in North America (2001), remains an outlier. No comparable new production has commenced in the subsequent 24 years despite several legacy operations facing closure or operational challenges.

Recent transaction multiples demonstrate institutional appetite for salt assets. German-based K+S sold its Americas salt business, including Morton and Windsor Salt brands, to Stone Canyon Industries Holdings for $3.2 billion in 2020. This transaction represented 12.5 times 2019 EBITDA, providing a valuation benchmark that suggests significant value creation potential for new, long-life salt operations with lower cost structures. Stone Canyon subsequently consolidated additional North American capacity through acquisitions including the Kissner Group, positioning the private equity-backed company as a dominant regional producer. This consolidation trend underscores the strategic value of salt assets with long reserve life and favorable operating costs.

Current spot pricing trends support Atlas Salt's feasibility study assumptions. The Updated Feasibility Study utilized base-case pricing of $81.67 per tonne, reflecting conservative assumptions relative to recent price movements. American Rock Salt's December 2025 price increase of $25 per tonne represents a material percentage increase over historical norms, with industry sources citing contractual pressures and accelerated seasonal demand as primary drivers. Atlas Salt's sensitivity analysis shows after-tax NPV8 increasing to $1.5 billion at $89.84 per tonne pricing (+10% from base case) with IRR expanding to 25.0%, demonstrating significant operating leverage to continued price strength. Each incremental $10 per tonne above base case assumptions adds approximately $200-250 million to after-tax NPV.

The Investment Thesis for Atlas Salt

- North America's 8-10 Mtpa import dependency creates immediate absorption capacity for new domestic production as legacy mines face operational challenges and environmental constraints that threaten 4-5 Mtpa of existing supply.

- Current enterprise value of $65.5 million represents 0.07x after-tax NPV8 of $920 million, offering multiple re-rating opportunities as project advances through financing, construction, and first production milestones by 2030.

- Environmental assessment completed, Updated Feasibility Study released, Early Works Development Plan approved, and strategic partnerships secured with Scotwood (offtake), Sandvik (equipment/financing), and Hatch (engineering) substantially reduce execution risk.

- Newfoundland positioning enables 3-day shipping to Boston versus 14+ days from international sources, reducing logistics costs by $10-15 per tonne while accessing established port infrastructure and clean hydroelectric power that delivers industry-leading greenhouse gas intensity.

- Base-case mine plan excludes 868 million tonnes of Inferred resources averaging 95.2% NaCl, providing potential to extend 24.3-year mine life and increase 4 Mtpa production profile as mining progresses and additional resources convert to reserves.

- Recent $25 per tonne pricing increase by American Rock Salt and structural supply deficit support continued price strength; each 10% increase above $81.67 per tonne base case expands after-tax NPV8 by approximately $580 million with IRR increasing 380 basis points.

Atlas Salt's Great Atlantic Salt Project represents a compelling opportunity to gain exposure to North America's structurally undersupplied de-icing salt market through a de-risked development asset with robust economics and strategic location advantages. The convergence of rising salt prices, legacy mine closures, import dependency, and three decades without new North American production creates a favorable backdrop for project advancement. With environmental assessment completed, feasibility study demonstrating $920 million after-tax NPV, strategic partnerships in place, and experienced management executing toward production by 2030, Atlas Salt offers investors significant re-rating potential as the company progresses through development milestones. The current enterprise value of $72.3 million versus feasibility study NPV suggests substantial upside for investors willing to accept development-stage execution risk in exchange for leveraged exposure to a critical industrial mineral with non-discretionary demand characteristics and favorable long-term supply-demand fundamentals.

TL;DR

Atlas Salt is developing North America's first new salt mine in 30 years in Newfoundland, Canada, with 4 Mtpa production capacity targeting the import-dependent eastern seaboard de-icing market. The September 2025 Updated Feasibility Study shows after-tax NPV8 of $920 million, 21.3% IRR, and $188 million average annual cash flow over 24.3 years. Recent price increases ($25/tonne by American Rock Salt) and supply constraints (legacy mine closures removing 4.5+ Mtpa) strengthen market fundamentals for new domestic production. With environmental assessment completed, strategic partnerships secured (Scotwood offtake, Sandvik equipment, Hatch engineering), and current enterprise value of $72.3 million versus $920 million NPV, Atlas Salt offers significant re-rating potential ahead of production estimated by 2030. Key risks include construction execution, financing completion, and commodity price volatility, balanced by salt's non-discretionary demand and essential infrastructure role.

FAQs (AI-Generated)

The shallow 180-meter deposit depth reduces development costs and enables decline access versus costly shaft sinking, while 95.9% NaCl grade requires only physical processing without chemicals, generating AISC of $34.90 per tonne and after-tax IRR of 21.3%.

Newfoundland positioning enables 3-day shipping to Boston versus 14+ days from Chile or Egypt, reducing transportation costs by $10-15 per tonne while accessing established port infrastructure and clean hydroelectric power for industry-leading low greenhouse gas intensity of 950 tonnes CO2e per million tonnes production.

The company estimates first production by 2030, with immediate priorities including finalizing project financing through Endeavour Financial, securing additional offtake agreements, obtaining remaining operating permits, and commencing early works construction activities on the 4 Mtpa operation.

Primary risks include construction cost overruns beyond $589 million pre-production budget, financing completion challenges, permitting delays, commodity price volatility below $81.67 per tonne base case, and operational execution during mine ramp-up to nameplate 4 Mtpa capacity.

Atlas Salt's current enterprise value of $72.3 million represents 0.08x the after-tax NPV8 of $920 million, providing substantial re-rating potential as the project advances through financing, construction, and production milestones over the next five years toward 2030 first production.

Analyst's Notes

Subscribe to Our Channel

Stay Informed