Atlas Salt - Pioneering Sustainable Salt Mining in North America

Atlas Salt: North America's first new salt mine in 30 years. $920M NPV, 21.3% IRR, zero emissions. Trading at 8% of NPV. Full investment analysis & risks.

- Atlas Salt is developing North America's first new salt mine in nearly 30 years, targeting a $5.34 billion market where government and municipal customers provide recession-proof demand. Deicing applications account for 44% of North American salt consumption, while the chemical industry represents 30%, creating stable revenue streams with minimal price volatility.

- The Great Atlantic Salt Project delivers exceptional economics with a $920 million post-tax NPV, 21.3% IRR, and $188 million average annual free cash flow over 25 years. The shallow deposit enables lower-cost drift mine construction compared to traditional deep shaft mines, while the site's proximity to Turf Point deep-water port provides superior logistics through a three-kilometer conveyor system.

- The project will operate as 100% battery-electric with zero greenhouse gas emissions, creating competitive advantages as carbon pricing mechanisms evolve across North America. Full environmental assessment approval was secured in 2024 with early works permits in hand, eliminating major permitting risk that typically delays mining developments.

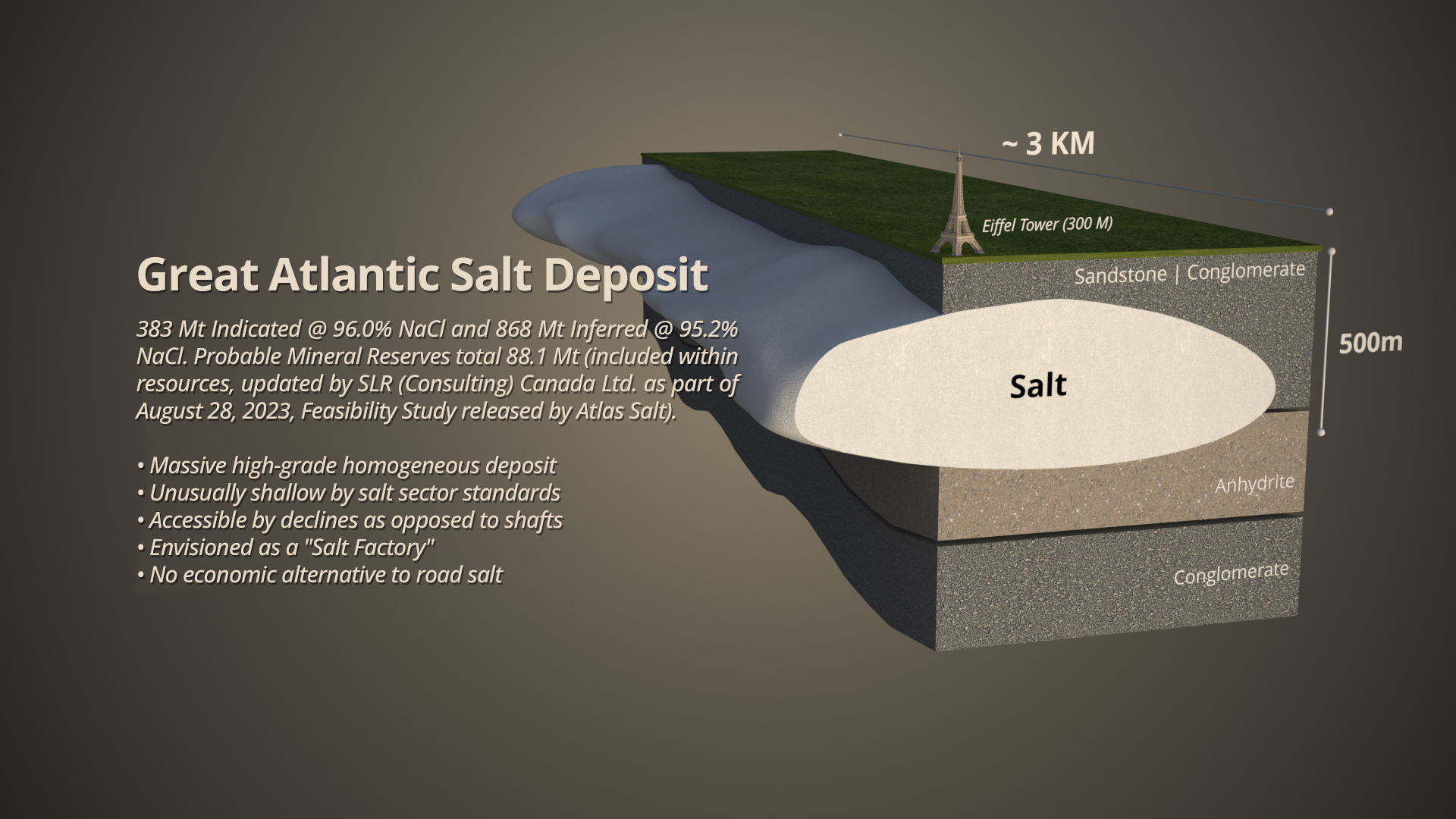

- Two completed feasibility studies confirm over 1 billion tons of salt reserves with no further metallurgical work required, positioning the project as shovel-ready with full community and Indigenous support. Sandvik has committed $70-80 million in equipment financing (15-20% of total capital needs), while Scotwood Industries, the largest US packaged deicing salt distributor, has signed an offtake MOU.

- The company maintains a clean capital structure with 108 million shares outstanding, $20.4 million net cash, and no warrant overhang. Current market capitalization of $65-75 million represents less than 10% of the project's $920 million NPV, suggesting substantial upside potential as construction financing advances and development milestones are achieved.

Introduction to Atlas Salt & the Great Atlantic Salt Project

Atlas Salt represents a rare investment opportunity in the industrial minerals sector, developing what will become North America's first new salt mine built in nearly three decades. The company's flagship Great Atlantic Salt Project is located on the west coast of Newfoundland, strategically positioned to serve the northeastern United States, Midwest, Ontario, Quebec, and Atlantic Canada markets with deicing salt, a commodity characterized by stable demand, minimal price volatility, and government-backed revenue streams.

The project's development timeline positions Atlas Salt to capitalize on a market that has seen virtually no new supply additions for a generation. While North American salt consumption remains robust at over 23.5 million tons annually in the United States alone, existing mines are aging infrastructure operating at depths of 500-600 meters or more, with higher operating costs and development challenges than Atlas Salt's shallow, high-grade deposit.

Nolan Peterson, who joined as CEO in June 2025, brings over a decade of experience in mine development and design, having been involved in three major mining projects through construction phases. Peterson's engineering background, combined with his MBA and CFA credentials, represents a significant shift toward commercialization for a company that had previously excelled at technical advancement but struggled with market communication. As Peterson explains, "This company is a very interesting story... Earlier in the company's history, it had very strong market success. It followed the Lassonde curve. It started in 2019 at about five cents Canadian. And then during COVID, the initial excitement of the project took that valuation to over $4 per share."

The subsequent share price decline, despite continued fundamental progress on engineering and permitting, created a disconnect between project value and market valuation that new management aims to correct. With two completed feasibility studies, full environmental approvals, strategic partnerships emerging, and early works activities now funded, the company appears positioned to begin unlocking value as it advances toward construction.

All Known Questions Answered, with Chief Executive Officer, Nolan Peterson

Key Advantages of the Great Atlantic Salt Project

The Great Atlantic Salt Project's competitive positioning rests on four fundamental advantages that collectively make it one of the most compelling undeveloped salt projects in North America: resource quality, jurisdictional strength, infrastructure proximity, and operational efficiency.

The deposit itself is described by management as shallow, high-grade, homogeneous, and thick - characteristics that directly translate into economic advantages. The shallowness is particularly critical, as Peterson emphasizes:

"The shallowness is the key here. This is what makes it all possible as a mine. Existing mines in North America, which are all over 25 to 30 years old, have been operating for many decades and they sit at great depth, five to 600 meters minimum for the most part. That necessitates development through a shaft mine."

This depth advantage enables Atlas Salt to pursue drift mine development, a horizontal angular structure into the ground, rather than the vertical shaft construction required at competing operations. The implications are significant: lower capital costs, shorter development timelines, and reduced operating expenses throughout the mine life. For investors, this translates into faster payback periods and higher returns on invested capital compared to traditional salt mine development.

The jurisdictional advantage cannot be overstated. Western Newfoundland ranks among the world's premier mining jurisdictions, offering political stability, established mining law, and supportive communities. The company has secured full community support, full Indigenous support, and completed environmental assessment approval in 2024. This regulatory clarity eliminates one of the primary risks that plague mining developments globally.

Perhaps most compelling is the infrastructure advantage. Atlas Salt's location is less than three kilometers from Turf Point, an existing deep-water port capable of handling 50,000-tonne Panamax vessels, which provides direct access to key markets via the St. Lawrence Seaway. As Peterson notes:

"When you're selling a bulk commodity product like salt, this is an industrial mineral, which is low margin and high tonnage. So you have to be close to your customers or close to an ability to get to your customers. And that's what we have."

The operational plan calls for a five-kilometer conveyor system connecting the mine to port, with underground crushing and screening eliminating the need for surface processing infrastructure. Less than two kilometers from Newfoundland Hydro's St. George's substation, the operation will be 100% battery-electric with zero greenhouse gas emissions, a claim Peterson is careful to distinguish from aspirational goals:

"This is not an aspirational goal. This is built into our plans right now. We'll have zero greenhouse gas emissions, making this a truly cutting edge mine development."

Economic Viability & Feasibility Studies

Atlas Salt has completed not one but two feasibility studies, demonstrating economic robustness across different scenarios and market conditions. The updated feasibility study released in Q3 2025, prepared by SLR, delivered materially improved results compared to the 2023 baseline study.

The financial metrics are compelling for an industrial mineral project. The post-tax NPV at an 8% discount rate stands at over $920 million, a figure that dwarfs the company's current enterprise value by more than 10x. The 21.3% post-tax internal rate of return exceeds typical mining project thresholds and reflects the project's robust economics even in conservative price scenarios.

What distinguishes Atlas Salt from many mining investments is the consistency of projected cash flows. The life-of-mine average annual free cash flow of $188 million represents steady-state production rather than front-loaded or declining profiles. Peterson emphasizes this stability:

"This is a steady state cash flow as well. This isn't volatile. This isn't spiking in the first few years. This isn't a long tail. This is every single year, steady demand. That's the nature of salt deposits. They're very robust, very stable, and they just make money constantly and consistently."

The reserve base of over 1 billion tons of salt supports the 25-year mine life outlined in the feasibility study, with an additional 50 years of resource potential beyond current reserves. All material has been confirmed through drilling programs, eliminating exploration risk. Critically, no further metallurgical studies or drilling programs are required, and the company does not need to raise capital for additional technical studies.

From an investor perspective, this de-risked profile is unusual. Most mining development stories at this market capitalization require significant additional capital for drilling, metallurgical work, or further engineering before achieving bankable status. Atlas Salt has crossed these thresholds, positioning it as a near-term development opportunity rather than a long-dated exploration bet.

The capital requirements for construction have been estimated in the feasibility study, with Sandvik, a globally recognized mining equipment supplier, having already committed $70-80 million in equipment financing. This represents 15-20% of total financing needs and validates the project's technical and commercial viability in the eyes of a sophisticated industry participant.

Understanding the North American Salt Market

Overview of the North American Salt Market

The North American salt market represents a $5.34 billion opportunity in 2025, with the United States accounting for approximately $4.71 billion of this total. Market dynamics are characterized by stable demand drivers, limited new supply, and regional rather than global pricing structures due to transportation economics.

Deicing applications constitute the largest market segment, representing 44% of North American salt consumption in 2023, compared to chemical industry use at 30% and other applications including food processing, water treatment, and agriculture accounting for the remaining 26%. The US produced an estimated 42 million metric tons of salt in 2023, making it the world's second-largest producer after China's 53 million metric tons.

Market growth projections indicate a compound annual growth rate of 2.0-2.4% through 2032 for the US market, reaching $4.91-5.39 billion by that date. The North American market overall is projected to expand at 5.1% CAGR, reaching $9.51 billion by 2034. While these growth rates appear modest, they reflect the mature, stable nature of salt markets, precisely the characteristic that makes them attractive for investors seeking consistent cash flow generation.

Regional market structures are critical to understanding Atlas Salt's positioning. As Peterson explains:

"Salt is a global industry. It's used all over the planet, every country on earth needs salt for many different applications, every country on earth produces salt to varying quantities as well, but what is the challenge is moving that salt around. So what you find is that there's a lot of regional markets more so than one global integrated market."

Transportation economics dictate that landlocked mines can typically service areas only 100-150 kilometers radius before becoming cost-prohibitive. Salt moving longer distances requires port access and vessel transportation. This creates natural monopolies within geographic regions and protects producers with superior logistics from distant competition.

Environmental Challenges & Market Dynamics

The deicing salt market faces increasing scrutiny regarding environmental impacts, particularly salt runoff contamination of waterways and damage to roadside vegetation. These concerns have prompted regulatory discussions about alternative deicing agents such as calcium magnesium acetate, though cost and effectiveness limitations have prevented widespread substitution.

Atlas Salt's zero-emission operating profile positions it advantageously as carbon pricing mechanisms evolve. Peterson notes:

"This is something that is becoming more common and more worked into pricing models as the market starts to evolve to account for greenhouse gas emissions, not only in North America, but in other jurisdictions like Europe as well, where this will help our salt be very competitive compared to foreign production."

The carbon footprint comparison is stark. Solar-evaporated salt produces approximately 1 kg CO2 per ton, mined rock salt typically generates below 10 kg CO2 per ton, while vacuum salt can reach 100 kg CO2 per ton. Atlas Salt's battery-electric operations powered by Newfoundland Hydro's renewable energy will deliver rock salt with minimal transportation distances to key markets, creating a compound environmental advantage.

Import dynamics also shape the market. Canada supplies 29% of US salt imports, followed by Chile at 28%, Mexico at 12%, and Egypt at 11%. These imports, primarily arriving via ocean freight, carry significant carbon footprints that increasingly factor into procurement decisions by environmentally conscious municipalities and government agencies.

Winter weather patterns drive deicing demand volatility, with El Niño weather patterns (warmer temperatures in northern states) reducing consumption while La Niña patterns increase it. However, over multi-year periods, deicing demand proves remarkably consistent. Mild winters in recent years have actually created inventory drawdowns at some operations, positioning the market for stronger pricing when normal winter patterns return.

Feasibility Study Insights & Financial Projections

The updated 2025 feasibility study, building on the 2023 baseline work, reflects conservative assumptions that enhance investor confidence in projected returns. Management deliberately chose to model the most conservative product (bulk deicing salt) in the most conservative market segments, avoiding reliance on higher-margin specialty salt products or premium pricing scenarios.

The $920 million post-tax NPV at 8% discount rate implies significant value creation potential. Using the current market capitalization of approximately $65-75 million as a baseline, the project would need to achieve less than 10% of its feasibility study value to justify current valuations. This provides substantial downside protection even if actual results fall short of feasibility study projections.

The 21.3% post-tax IRR compares favorably to typical mining project hurdle rates of 15-20% and significantly exceeds risk-free rates. For context, most industrial mineral projects struggle to achieve IRRs above 15%, making Atlas Salt's economics stand out within its peer group.

Capital intensity metrics warrant examination. While absolute capital cost figures have not been publicly disclosed in the transcript, the fact that Sandvik's $70-80 million equipment financing commitment represents 15-20% of total needs implies total capital requirements in the $350-500 million range. Against a $920 million NPV, this suggests capital efficiency superior to many larger-scale mining developments.

Operating cost advantages stem directly from the drift mine configuration and conveyor-based logistics. Underground crushing and screening eliminate surface processing costs, while the battery-electric equipment configuration avoids diesel fuel expenses that represent significant operating costs at conventional mines. Peterson emphasizes:

"There's no diesel consumption. There's no drilling and blasting. 100% battery electric operated. All of our mining is done underground. Crushing and screening is done underground. It's put onto a conveyor, taken to our transfer building, taken onto another conveyor that takes it down to our port."

The project generates over 200 full-time long-term jobs when including port operations, contributing significant tax revenues to Newfoundland and Canadian governments. These economic multiplier effects strengthen community and government support, which are intangible benefits that reduce political risk and smooth regulatory processes.

Sensitivity analysis, while not detailed in available materials, would typically examine salt price assumptions, production volume variance, capital cost overruns, and operating cost inflation. The conservative product choice (bulk deicing salt rather than higher-margin specialty products) and conservative market assumptions (no premium for environmental advantages) suggest feasibility study results incorporate substantial safety margins.

Operational Efficiency & Environmental Impact

The operational design of the Great Atlantic Salt Project prioritizes efficiency, environmental performance, and cost minimization through integrated logistics and electrification. The five-kilometer conveyor system from mine to port eliminates trucking costs and associated diesel consumption, creating both economic and environmental advantages.

Underground operations will utilize battery-electric mining equipment exclusively, a commitment that distinguishes Atlas Salt from virtually all operating salt mines in North America. Conventional operations rely on diesel equipment, generating greenhouse gas emissions and requiring ventilation infrastructure to manage exhaust. Battery-electric operations eliminate these requirements, reducing capital costs for ventilation systems and ongoing operating costs for diesel fuel and maintenance.

The environmental profile extends beyond zero operational emissions. As Peterson notes:

"There's no water retention. There's no cyanide usage. There's no sulfuric acid usage. There's no diesel consumption. There's no drilling and blasting."

The absence of explosives use reflects the soft, easily extracted nature of the salt deposit, further reducing operational costs and environmental disturbance.

Greenhouse gas emissions studies commissioned by the company document emissions equivalent to four Newfoundland households annually, a figure that excludes offsetting benefits from reduced foreign salt imports. When considering displacement of imported salt that currently travels via ocean freight from Chile, Egypt, and other distant sources, the net carbon impact becomes significantly negative.

Surface disturbance is minimized by the underground operation configuration and direct conveyor connection to port. The visible surface footprint, as Peterson describes it, encompasses only essential infrastructure.

Water usage represents another environmental consideration, though salt mining by its nature is less water-intensive than many mineral operations. The absence of tailings, acid rock drainage, or chemical processing further simplifies environmental management and reduces closure liabilities, factors that improve project economics and reduce regulatory risk.

The environmental advantages translate into commercial benefits as procurement practices evolve. Municipalities and state departments of transportation increasingly incorporate carbon footprint considerations into bid specifications. Atlas Salt's zero-emission profile, combined with reduced transportation distances relative to imports, positions it to command premium pricing or win contracts against higher-carbon competitors.

Corporate Development & Management Strategy

Atlas Salt's mid-2025 management transition signals a shift from technical development to commercialization. CEO Nolan Peterson brings over a decade of mine development experience across three construction-phase projects, plus MBA, CFA, and P.Eng. credentials. CFO Jeffrey Kilborn adds investment banking and capital markets expertise. Both address a critical gap: while previous management advanced feasibility studies and environmental approvals, they failed to communicate value effectively to markets.

This disconnect created an investment opportunity. The stock rallied from $0.05 at inception in 2019 to over $4.00 during COVID-era excitement, then fell to current levels around $0.69 despite completing two feasibility studies and securing environmental approvals. As Peterson acknowledges: "The company did not market the story well enough, did not work to make sure that the successes of the company were being broadcast to the industry, did not defend the share price enough, and the share price suffered."

The board provides operational depth. Rowland Howe, former general manager of the Goderich Mine, led that operation to record 7.5 million tonnes per year production. Bob Kelly, former VP at Teck Resources, brings 40+ years in operations and mine development. The chairman and founder, both lawyer and geologist, discovered the deposit and demonstrated initial viability.

Strategic partnerships validate the project. Sandvik's $73 million equipment financing commitment from a global supplier with rigorous due diligence standards signals confidence in project viability. The Scotwood Industries offtake MOU targeting 1.25-1.5 million tonnes annually connects Atlas Salt to the largest US packaged deicing salt distributor serving Walmart and Home Depot, with discussions ongoing to "firm up and expand the quantities." Selection of a lead engineering firm, expected to be announced, represents another de-risking milestone moving the project toward construction-ready status.

Capital Structure & Future Prospects

Atlas Salt maintains an attractive capital structure with 108.2 million shares outstanding as of October 31, 2025. The October 2025 Listed Issuer Financing Exemption (LIFE) offering raised $8.7 million Canadian without warrants, demonstrating management's commitment to protecting shareholder interests. This brings net cash to approximately $20.1 million, resulting in an enterprise value of approximately $69.0 million.

The absence of warrant overhang distinguishes Atlas Salt from typical junior mining companies, where in-the-money warrants create persistent selling pressure. Management explicitly highlights this:

"There are no warrants overhanging our company. This includes the financing that we just completed. It was a no warrant deal and we have a clean balance sheet."

Construction financing of $589 million represents the critical path forward. Traditional project financing from banks appears feasible given strong feasibility study economics and government customer base. Sandvik's equipment commitment provides foundation for additional vendor financing. Strategic partnerships with existing salt producers or industrial consumers offer another avenue, while government programs supporting low-emission mining could supplement the financing package.

There is a valuation disconnect. At $69 million enterprise value versus $920 million NPV, the market prices in substantial execution risk. Even if the project achieves 25% of feasibility study NPV, current valuations imply significant upside. The Lassonde curve framework suggests Atlas Salt sits in the "valley of death" period common to development-stage mining companies, positioned for re-rating as construction financing is secured.

Key risks include financing execution (inability to secure capital on acceptable terms), construction cost overruns, operational challenges, and salt price declines, though pricing has proven stable given market structure. The Scotwood relationship mitigates customer acquisition risk, while Newfoundland's strong mining support reduces political risk.

The Investment Thesis for Atlas Salt

- Compelling Valuation Disconnect: Current market capitalization of $65-75 million represents less than 10% of the $920 million post-tax NPV demonstrated in the updated feasibility study, creating substantial upside potential as financing is secured and construction advances. The 21.3% IRR significantly exceeds typical mining project hurdle rates.

- De-Risked Development Asset: With two completed feasibility studies, full environmental approvals secured in 2024, over 1 billion tons of reserves confirmed through drilling, and early works permits in hand, the project has eliminated the primary technical and regulatory risks that typically plague mining developments. No further metallurgical studies or drilling programs are required.

- Strategic Market Positioning: As North America's first new salt mine in three decades, Atlas Salt enters a market characterized by aging infrastructure, stable demand of 42 million tons annually in the US alone, recession-proof government customers, and minimal price volatility. The deicing segment (44% of market) and chemical industry use (30%) provide consistent, countercyclical demand drivers.

- Superior Infrastructure & Cost Structure: The shallow deposit enables lower-cost drift mine development versus traditional shaft mines, while the three-kilometer proximity to Turf Point deep-water port via conveyor system creates unmatched logistical efficiency. Zero-emission battery-electric operations eliminate diesel costs and position the company advantageously as carbon pricing mechanisms evolve.

- Strategic Validation & Financing Progress: Sandvik's $70-80 million equipment financing commitment (15-20% of total capital needs) validates project viability, while the Scotwood Industries offtake MOU with the largest US packaged deicing salt distributor provides market access. Recent $9 million no-warrant financing demonstrates management's commitment to protecting shareholder value.

- Experienced Management Transition: The June 2025 appointment of CEO Nolan Peterson (10+ years mine development experience, three construction-phase projects, MBA, CFA) and CFO Jeffrey Kilborn addresses previous weaknesses in market communication and capital markets expertise while retaining engineering capabilities. Board members include the former general manager of the world's largest underground salt mine.

- Key Risks to Monitor: Financing execution remains the critical near-term challenge, requiring $350-500 million in construction capital. Construction cost overruns or delays could impact returns, while operational performance once in production remains unproven. Salt price declines are possible though historically rare given market structure.

The Atlas Salt investment thesis centers on management's ability to bridge the gap between demonstrated project value ($920 million NPV) and current market valuation ($69 million enterprise value) through successful financing execution and construction commencement. Technical risks have been eliminated through two feasibility studies, environmental approvals, and engineering work. What remains is execution risk - securing $589 million in construction capital and delivering the mine as designed.

The risk-reward profile appears asymmetric. Downside scenarios, including financing delays or project setbacks, will likely keep shares range-bound with potential dilution from additional financings. Upside scenarios assuming successful construction financing could drive substantial re-rating. Even capturing 20-30% of NPV in market capitalization would represent 3-5x returns from current levels.

Investment timelines matter critically. Development-stage mining investments typically require 2-4 year holding periods before major value inflection points. Early works activities funded by recent financings should provide visible progress milestones over coming quarters, with construction financing representing the key catalyst likely in 2026.

The environmental leadership positioning creates optionality undervalued in feasibility studies. As carbon pricing expands and government procurement incorporates emissions considerations, zero-emission operations could command premium pricing or preferential contract access beyond base case projections.

Market opportunity is substantial. North American salt demand projected to expand from $5.34 billion in 2025 to $9.51 billion by 2034 represents 5.1% compound annual growth. Within this expanding market, deicing applications show stable demand driven by winter weather and growing road infrastructure, while 8-10 million tonnes of annual imports create displacement opportunity for domestic production. Government customers provide payment security rare in commodity markets, enhancing project bankability.

Macro Thematic Analysis

Atlas Salt's development aligns with broader North American trends toward supply chain resilience and environmental accountability. While salt lacks "critical mineral" designation, dependence on imports for 8-10 million tonnes annually of deicing salt creates vulnerability. Severe winter salt shortages can literally halt regional economies, giving the commodity strategic importance despite its ubiquity.

Environmental, social, and governance considerations increasingly shape commodity procurement. Transportation accounts for the largest component of salt's carbon footprint, making domestically produced salt with short shipping distances inherently lower-emission. Atlas Salt's battery-electric operations compound this advantage, potentially creating North America's lowest-carbon salt supply.

As Peterson emphasizes, environmental attributes carry commercial implications:

"This is something that is becoming more common and more worked into pricing models as the market starts to evolve to account for greenhouse gas emissions, not only in North America, but in other jurisdictions like Europe as well, where this will help our salt be very competitive compared to foreign production."

This strategic pivot in commodity markets means environmental performance increasingly influences purchasing decisions beyond simple cost considerations.

The technological leadership positioning matters beyond Atlas Salt. While many mining companies announce aspirational emission reduction targets for 2030 or 2040, Atlas Salt's day-one commitment to 100% battery-electric operations demonstrates feasibility and economic viability, potentially influencing broader industry adoption and regulatory expectations.

From a portfolio perspective, Atlas Salt offers defensive characteristics rare in mining equities. Salt demand proves remarkably insensitive to economic cycles, with government customer base and essential deicing operations creating revenue stability uncommon in commodity investments. This countercyclical profile complements more volatile mineral exposures in diversified portfolios.

TL;DR

Atlas Salt is developing North America's first new salt mine in three decades, targeting a $5.34 billion market with recession-proof government customers and 4 million tonnes per annum nameplate production capacity. The Great Atlantic Salt Project delivers exceptional economics with $920 million NPV, 21.3% IRR, and $188 million average annual free cash flow over a 24.3-year mine life. Environmental assessment approval was secured in April 2024 after only two months of review, while the shallow deposit at 180 meters enables low-cost drift mine construction versus traditional 500-600 meter shaft mines. Zero-emission battery-electric operations provide competitive advantages as carbon pricing evolves. With 108.2 million shares outstanding and $69 million enterprise value, the stock trades at less than 8% of feasibility study NPV, suggesting substantial upside as construction financing is secured and development advances toward estimated 2030 production start.

FAQ's (AI-Generated)

Atlas Salt will be North America's first new salt mine built in nearly 30 years, utilizing 100% battery-electric equipment for zero greenhouse gas emissions. The Great Atlantic Salt Project's shallow deposit enables low-cost drift mine construction versus traditional shaft mines, while its proximity to Turf Point deep-water port (less than 3 kilometers) provides superior logistics via conveyor system. The project has completed two feasibility studies showing $920 million post-tax NPV and 21.3% IRR, with full environmental approvals secured in 2024.

The North American salt market is valued at $5.34 billion in 2025, with the U.S. accounting for $4.71 billion. Deicing applications represent 44% of consumption (approximately 18.5 million tons annually in the U.S.), followed by chemical industry use at 30%. Atlas Salt targets the deicing segment primarily, selling to government agencies, municipalities, and state departments of transportation—customers that provide stable, recession-proof revenue streams with minimal price volatility.

The primary risk is financing execution—the company must secure $350-500 million in construction capital to advance the project. Construction cost overruns or delays could impact returns, while operational performance once in production remains unproven. Salt price declines are possible though historically rare given market structure. The company's current capital position of approximately $20.4 million funds early works activities but not full construction. Political or regulatory changes could affect the project, though current government support is strong.

The company has not publicly disclosed a specific production start date in available materials, but typical drift mine construction timelines range from 2-4 years following construction financing. With environmental assessment approval secured in April 2024, early works permits in hand, and $8.7 million raised in October 2025 for initial activities, visible development progress should emerge over the next 6-12 months. Construction financing remains the critical path item, likely requiring 6-18 months to complete against the $589 million initial capital requirement. Assuming financing closes in 2026, first production could potentially commence around 2030, though investors should expect timeline adjustments as the project advances through detailed engineering and construction phases.

Atlas Salt will operate as 100% battery-electric with zero operational greenhouse gas emissions, equivalent to four Newfoundland households annually. This compares to conventional diesel-operated mines that generate 10+ kg CO2 per ton of rock salt produced. The company's renewable energy connection through Newfoundland Hydro and short transportation distances to markets via port facilities provide additional carbon advantages over imported salt from Chile, Egypt, and other distant sources. The project requires no water retention, uses no cyanide or sulfuric acid, and involves no drilling or blasting due to the soft nature of the salt deposit.

Analyst's Notes

Subscribe to Our Channel

Stay Informed