Brent Jumps on Hormuz Tensions, but 95.8% Refinery Utilization Limits Any Fuel Supply Response

Brent surged on Hormuz tensions, but US refineries running at 95.8% capacity limit fuel supply growth, keeping diesel and refining margins under pressure.

- Brent crude rose 3.8% to $78.86 per barrel and US crude rose 4.11% to $74.36 per barrel after renewed US-Iran missile and drone strikes and Tehran's claim that it had closed the Strait of Hormuz raised concerns over Gulf oil flows.

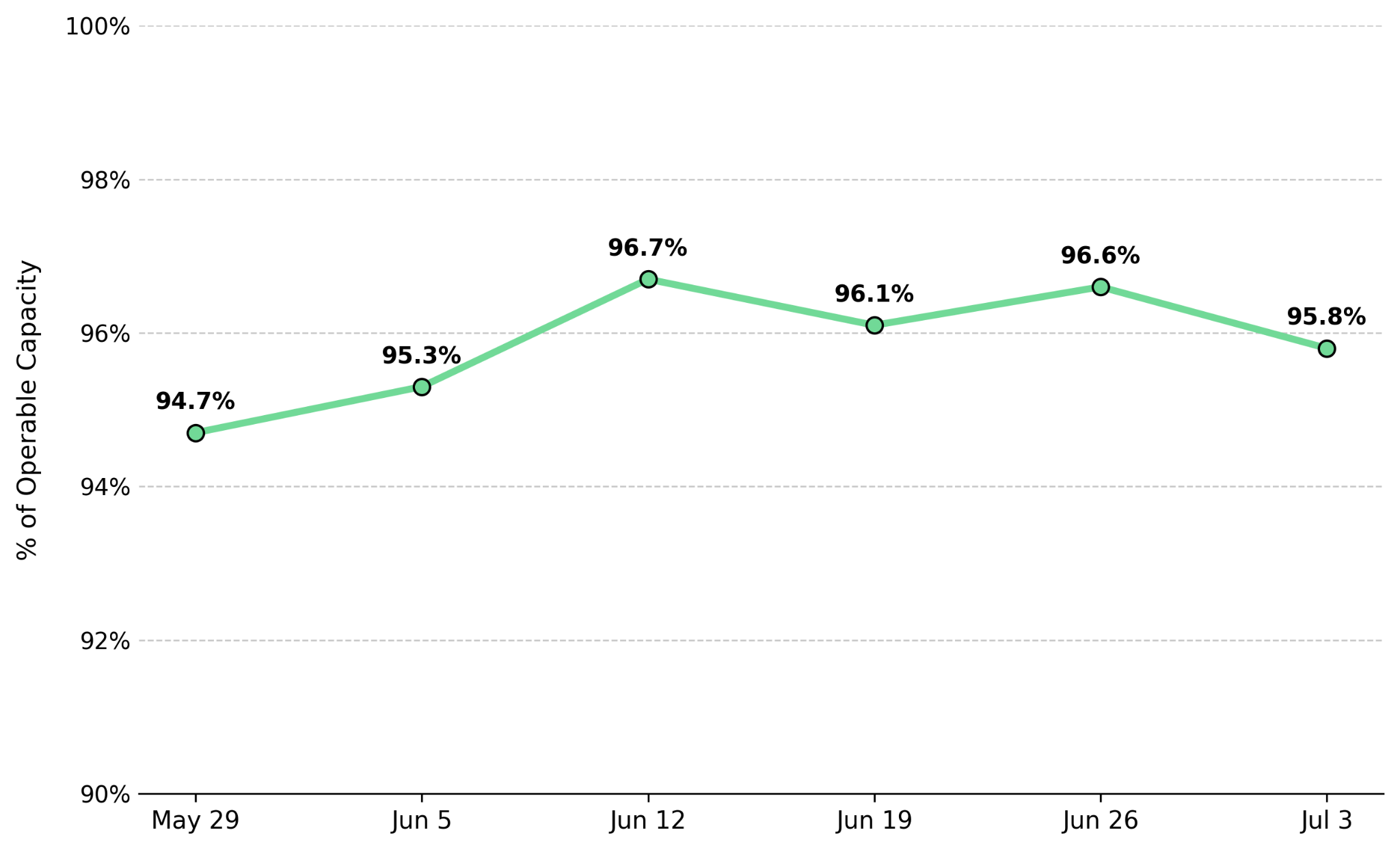

- US refineries processed 17.0 million barrels per day at 95.8% of operable capacity, up from a four-week average of 94.4% in the same period of 2025, leaving little spare processing capacity to increase fuel output if crude supplies tighten.

- US distillate fuel inventories fell 5.0 million barrels to 12% below the five-year seasonal average, while crude oil imports averaged 11.4% below the same period in 2025 over the previous four weeks, reducing the supply buffer ahead of any prolonged Hormuz disruption.

- National average retail diesel fell $0.090 to $4.578 per gallon but remained $0.839 above year-ago levels, leaving pump prices positioned to rise if the Hormuz-driven crude rally persists.

- US officials said about 20 vessels were escorted through the Strait of Hormuz, but ship-tracking data showed little transit activity, leaving the reported disruption unconfirmed despite the sharp rise in oil prices.

Hormuz Tensions Push Brent Higher as Markets Price Supply Risk Ahead of Confirmed Disruption

Brent crude rose 3.8% to $78.86 per barrel and US crude rose 4.11% to $74.36 per barrel after renewed US-Iran missile and drone strikes and Tehran's claim that it had closed the Strait of Hormuz. The rally erased most of Brent's decline from its recent low of $70.14 per barrel in a single session, reflecting a renewed geopolitical risk premium. US officials said about 20 vessels were escorted through the strait, but ship-tracking data showed little transit activity, indicating oil prices had risen faster than confirmed disruption to shipping.

Officials said about 20 vessels were escorted through the Strait of Hormuz in the past 24 hours, but ship-tracking data showed little transit activity, leaving shipping disruption unconfirmed. The mismatch indicates oil prices have moved ahead of confirmed supply disruption, with the market pricing the risk of a prolonged closure rather than verified changes in oil flows.

The market reaction spread beyond oil into equities, bonds, and gold. Global stocks fell, government bond yields rose, and gold dropped 1.5% to about $4,060 an ounce as higher yields outweighed geopolitical demand for non-yielding assets. The 2-year Treasury yield rose to 4.2393%, its highest level since February 2025, while Fed funds futures priced 39 basis points of additional tightening by year-end ahead of Fed Chair Kevin Warsh's first congressional testimony. Higher discount rates reduce the value of development-stage mining projects, while lower gold prices show that rising oil prices do not automatically lift the broader commodity market.

Higher Crude Prices Hit a 95.8% Refinery Capacity Ceiling, Keeping Fuel Supply Constrained

Refinery capacity, not crude availability, limits US fuel supply. US refineries processed 17.0 million barrels per day at 95.8% of operable capacity, up from a four-week average of 94.4% in the same period of 2025. Despite operating near full capacity, distillate fuel production fell to 5.2 million barrels per day and distillate inventories dropped 5.0 million barrels to 12% below the five-year seasonal average. With little spare refining capacity, the Hormuz disruption can raise fuel costs but cannot increase fuel supply.

Lower crude imports further limit supply flexibility. US crude oil imports averaged 5.4 million barrels per day over the previous four weeks, 11.4% below the same period in 2025. With imports already below last year's level and refineries operating near full capacity, any prolonged Hormuz disruption would tighten fuel supply rather than increase production.

Political De-escalation Could Restore Oil Flows While Refinery Constraints Cap Fuel Supply

Jefferies economist Mohit Kumar said political incentives could support a negotiated agreement before the US midterm elections. He told Reuters, "We could have a patch that would enable oil to flow through and put a lid on oil prices." Even if oil flows recover, refineries operating near full capacity would limit any increase in fuel production, leaving higher crude availability with little immediate effect on product supply.

In the base case, a negotiated agreement ahead of the US midterm elections keeps Brent near current levels, but refinery utilization remains at 95.8% and distillate inventories stay 12% below the five-year average unless crude imports recover. In the bear case, lower confirmed tanker movements would tighten crude supply further. With imports already 11.4% below year-ago levels and little spare refining capacity, higher crude costs would translate into tighter fuel supply rather than higher fuel production.

June CPI is the next key data release. A headline inflation rate of 4.2% could reflect lower gasoline prices before the recent rise in crude oil pushes fuel costs higher, making any improvement in inflation temporary if oil prices remain elevated.

Higher Oil Prices Tighten Refining Margins While Raising Mining Operating Costs

Refiners and midstream operators face the greatest margin pressure from higher crude costs. With refineries operating at 95.8% of capacity and distillate inventories 12% below the five-year average, higher crude prices squeeze refining margins because refiners cannot increase fuel output enough to offset rising feedstock costs.

US crude imports averaged 11.4% below year-ago levels over the previous four weeks, limiting refiners' ability to replace Gulf supplies if the Hormuz disruption continues. Retail diesel stood at $4.578 per gallon before the latest crude rally reached pump prices. With diesel already $0.839 above year-ago levels, further price increases would raise operating costs for miners that rely on diesel-powered haul trucks and generators.

The available data do not yet confirm whether the Strait of Hormuz disruption will prove temporary or prolonged because ship-tracking data has not verified a comparable change in tanker movements. Confirmed tanker traffic and refinery utilization are the key indicators to watch because they measure whether supply constraints are worsening or easing.

Tanker Traffic & Refinery Utilization Will Show Whether Fuel Supply Constraints Are Easing

Brent at $78.86 per barrel reflects expectations of a prolonged Strait of Hormuz disruption, even though ship-tracking data has not confirmed a comparable reduction in tanker traffic.

A negotiated agreement that restores normal tanker traffic through the Strait of Hormuz would remove much of the current geopolitical risk premium, potentially pulling Brent back toward its recent low of $70.14 per barrel.

June CPI and the EIA's next Weekly Petroleum Status Report are the key releases to watch. They will show whether refinery utilization remains near 95.8% and whether the 12% distillate deficit begins to narrow, providing the clearest indication of whether fuel supply constraints are improving.

Analyst's Notes

Subscribe to Our Channel

Stay Informed