US Copper Tariff Delay Diverges From What Markets Priced In, Leaving a 640,000-Tonne Ex-US Deficit

US tariff uncertainty redirected 900,000 tonnes of copper into US warehouses, tightening ex-US supply and favoring advanced copper projects.

- The US Department of Commerce missed its June 30 deadline to recommend a tariff on refined copper, keeping an exchange price premium of roughly US$400 per tonne in place as markets await a policy decision.

- An estimated 900,000 tonnes of copper have moved into US warehouses in 2026 as traders position ahead of a potential tariff, reducing available supply outside the US.

- Goldman Sachs revised its 2026 copper outlook from a 490,000-tonne global surplus in April to a 640,000-tonne deficit outside the US by June as tariff-driven stockpiling redirected metal into US warehouses.

- Major copper producers are producing below guidance, limiting the industry's ability to offset tighter supply outside the US.

- Copper developers and explorers advancing projects outside the US are best positioned to benefit from the US copper price premium.

Policy Uncertainty Sustains Copper Inventory Shifts & Regional Price Gaps

Section 232 of the Trade Expansion Act allows the US President to impose tariffs on imports deemed a national security risk, and the authority now underpins both existing copper tariffs and the ongoing refined copper review. Since 2025, a 50% tariff has applied to semi-finished copper products, including pipe, wire, and rod, while refined copper cathode, the primary input for wire mills, smelters, and fabricators, remains exempt. A Presidential Proclamation directed the Department of Commerce to determine whether refined copper cathode should face a phased tariff of 15% from January 2027, rising to 30% in January 2028. The recommendation was due by June 30, 2026, but the deadline passed without a public determination, giving importers more time to move copper into the US ahead of any tariff announcement and reducing available supply in other markets.

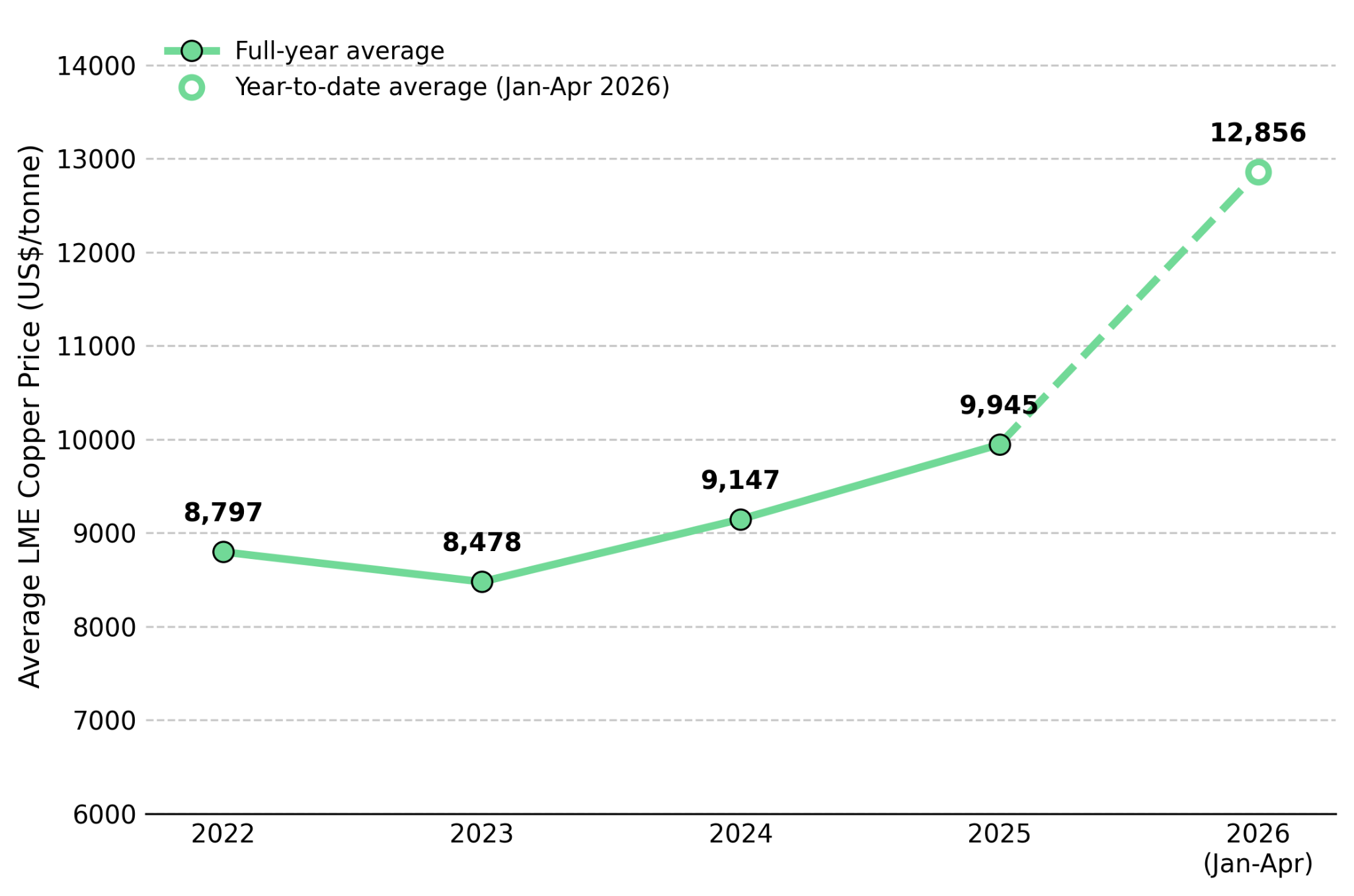

The clearest evidence of tariff positioning is the spread between COMEX and LME copper prices. The spread widened to roughly US$400 per tonne by early June, reflecting the premium buyers paid for US-delivered copper ahead of a potential tariff. The spread reflects trader positioning rather than a confirmed tariff decision and could narrow quickly if the proposed duty is not implemented.

Tariff-Driven Stockpiling Tightens Ex-US Copper Supply & Supports Regional Prices

When traders move physical cathode into COMEX-registered warehouses ahead of a potential tariff, that metal is withdrawn from LME and Shanghai-deliverable inventories. Total mined and refined copper supply does not change. Instead, inventories shift toward the US, leaving less immediately available copper for buyers in other markets.

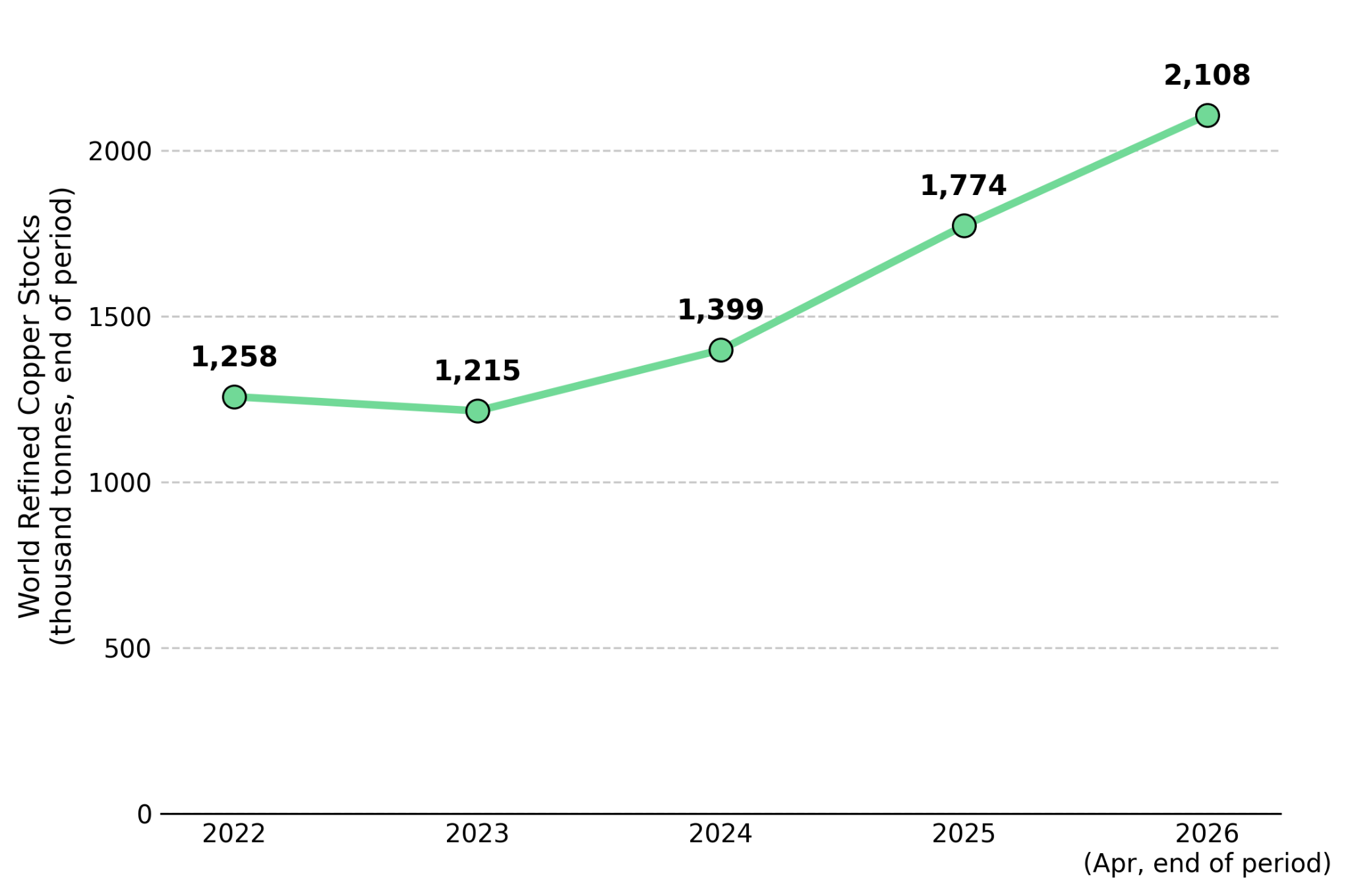

Goldman Sachs' forecast revisions illustrate how rapidly inventory transfers into the US reshaped copper market expectations, moving from a projected 490,000-tonne global copper surplus for 2026 in April to a 640,000-tonne deficit outside the US by June. The June forecast also projected a further 170,000-tonne deficit in 2027, alongside a 900,000-tonne increase in US inventories to roughly 1.8 million tonnes by year-end. The two-month forecast revision reflects the scale of inventory transfers into the US ahead of a potential tariff.

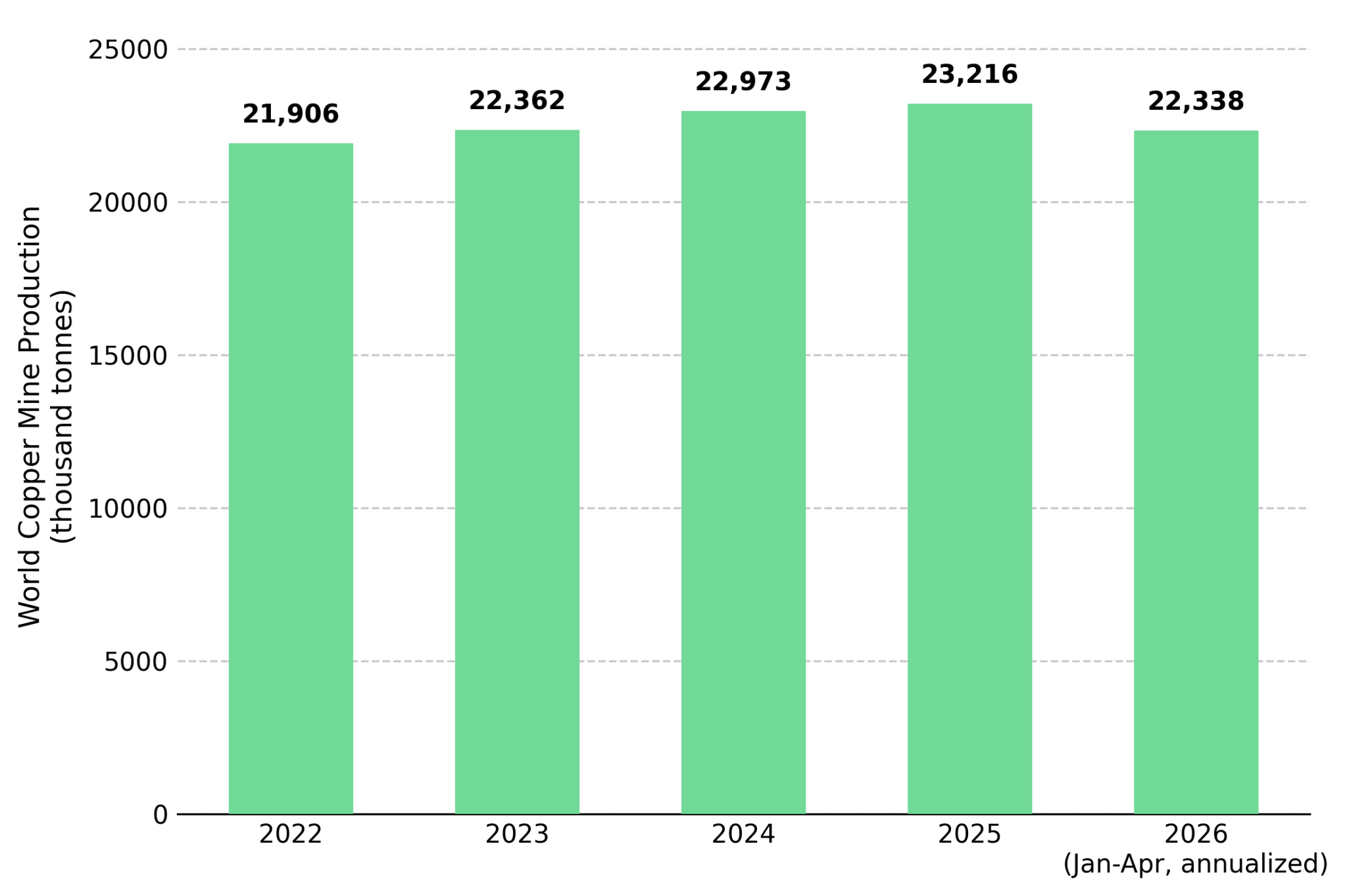

The inventory shift comes as major copper producers have limited capacity to increase supply. Codelco's El Teniente output fell 13% year over year, Anglo American's first-quarter production tracked below annual guidance, and the timing of a full restart at Freeport-McMoRan's Grasberg complex remains uncertain. Every tonne diverted into US warehouses leaves less copper available to smelters, fabricators, and project developers in other markets, supporting higher regional prices.

Ex-US Supply Tightness Accelerates Chilean Copper Development & Strategic Project Value

Chile is well-positioned to increase copper supply outside the US because its established smelting, electrowinning, and permitting infrastructure can support faster project development. Oxide deposits are processed through heap leaching and solvent extraction-electrowinning (SX-EW), producing cathode on site with lower capital requirements. Sulfide deposits require flotation and smelting but typically support larger, higher-grade ore bodies that can sustain longer mine lives.

Marimaca Copper is developing the Marimaca Oxide Deposit in Chile's Antofagasta region, with Proved and Probable Reserves of 179 million tonnes grading 0.42% copper for 748,000 tonnes of contained copper, targeting annual cathode production of 50,000 tonnes. Its first five years are projected to deliver an AISC of US$1.97 per pound against a base-case copper price of US$4.30 per pound, supporting robust project economics before any additional upside from tariff-driven price premiums. Hayden Locke, President and Chief Executive Officer of Marimaca Copper, highlights the strategic appeal of large Chilean copper projects:

"If you deliver a project with three to five million tonnes of contained copper in Chile's coastal belt, with access to infrastructure and Antofagasta, it would grab the attention of just about every major mining company in the world because they are all desperate for copper exposure."

Fitzroy Minerals is exploring the Buen Retiro project near Copiapó, where near-surface oxide mineralization includes a 59.0-meter intercept grading 1.73% copper and lies within 90 kilometers of three operating SX-EW plants, supporting lower development costs and faster commercial cathode production. Merlin Marr-Johnson, President and Chief Executive Officer of Fitzroy Minerals, outlines the long-term outlook for Chilean copper supply:

"BHP, the world's largest copper producer, says in its reports that Escondida will spend approximately US$5 billion, yet its production profile in 2030 is likely to be 1 million tonnes per annum. That's down 20% to 30% from where it is today. In the same report from August 2025, BHP says there will be zero growth from Chile between 2031 and 2040."

District Expansion & Brownfield Assets Strengthen Future Copper Production

Chile is not the only jurisdiction positioned to increase copper supply outside the US. Projects in Quebec and Canada's Yukon are leveraging existing infrastructure to shorten development timelines and bring additional copper supply to market more quickly.

Abitibi Metals is advancing the B26 polymetallic deposit in Quebec's Selbaie Camp, where the resource has grown 124% since 2023 to 25.3 million tonnes grading 2.1% CuEq. Its 10-year ROFR over SOQUEM's neighbouring Wagosic and Carheil properties supports a district-scale development strategy targeting 50 million to 100 million tonnes through a shared central mill, with a PEA targeted for the first quarter of 2027. The expansion strategy increases the project's long-term production potential while leveraging shared infrastructure to reduce future development costs. Jon Deluce, President and Chief Executive Officer of Abitibi Metals, emphasizes growing scarcity of large-scale copper development assets:

"Quebec is a very sought-after jurisdiction. Many multi-million-ounce-equivalent developers have been taken over in the last two years, and I don't think that M&A will stop. There are very few multi-million-ounce developers left in the market, while producers generating record cash flow are still behind the curve in replenishing their exploration and development pipelines."

Selkirk Copper is advancing exploration and resource-definition drilling at the past-producing Minto mine in Yukon, where an existing 4,100-tonne-per-day processing plant and underground infrastructure could shorten the path to production while reducing upfront capital requirements compared with greenfield developments. Its 50,000-meter Phase 2 drill program was 54% complete as of late June, supporting an updated MRE and PEA targeted for the second half of July 2026. Colin Joudrie, Director and Chief Executive Officer of Selkirk Copper, describes strong market demand for premium copper concentrate:

"It's a high-quality concentrate. The market likes this concentrate because it can be sold anywhere at any time. If we can get close to our mid-2028 restart objective, that would be exceptional in today's market. There isn't much supply available."

Early-Stage Copper Discoveries Expand Future Supply in the Vicuña District & South Australia

Further down the development curve, discovery-stage exploration in Argentina's Vicuña district and in South Australia makes a point worth stating plainly: some of the most consequential additions to the ex-US supply story are still years from a resource statement, let alone a construction decision.

Mogotes Metals is exploring the Albor discovery at its Filo Sur project in the Vicuña district, immediately adjacent to Lundin Mining and BHP's Filo del Sol deposit, placing it within one of the world's most active emerging copper districts. A recent intercept of 180.0 meters grading 0.98% CuEq from just 108 meters depth highlights the project's long-term resource potential but has not yet been incorporated into an MRE. Allen Sabet, Chief Executive Officer of Mogotes Metals, underscores copper's strategic value among major discovery targets:

"In terms of metals, it's clearly copper and gold. From a strategic perspective, copper is the most important because large-scale discoveries are much rarer."

Cobra Resources is advancing the Manna Hill project in South Australia within the same copper province as Olympic Dam, Prominent Hill, and Carrapateena, with up to 1,800 meters of planned diamond drilling to test a geophysical porphyry target. The project has not yet reached an MRE or disclosed economic studies, positioning it as a long-term exploration opportunity that could expand future copper supply outside the US rather than address today's supply deficit.

Policy, Demand & Mine Supply Could Undermine the Ex-US Deficit Thesis

If the Department of Commerce declines to impose a tariff or indefinitely defers its decision, the incentive to stockpile copper in the US would weaken, likely narrowing the COMEX-LME price spread toward historical levels. China accounts for roughly 55% to 58% of global refined copper consumption, making its second-quarter GDP and June trade data due July 14-16 an important test of whether demand is strengthening. Weaker-than-expected data would reduce support for higher ex-US copper prices regardless of the tariff decision. An earlier-than-expected restart at Grasberg would increase mine supply independent of US trade policy, reducing pressure on the ex-US copper market.

A refined copper tariff would reinforce the ex-US supply deficit, strengthening price support for advanced copper projects outside the US. If the tariff is deferred indefinitely or not implemented, inventories accumulated in the US would likely unwind, reducing support for higher copper prices outside the US. In either scenario, project quality, development stage, and the ability to deliver new supply remain the primary differentiators across the copper sector.

The Investment Thesis for Copper

- A policy-driven rather than demand-driven split between US and ex-US copper markets means COMEX prices may no longer reflect physical market conditions outside the US, increasing the importance of tracking regional supply, inventories, and project economics alongside headline exchange prices.

- Projects with defined reserves and economic studies retain value under the base-case copper price, while pre-resource discoveries offer greater upside if a widening ex-US deficit supports higher copper prices.

- Existing processing infrastructure, whether a nearby SX-EW plant or a past-producing mill, reduces development costs and timelines, allowing new copper supply to reach tightening ex-US markets more quickly.

- District consolidation strategies built around ROFRs and option agreements expand future resource potential and create district-scale development opportunities, increasing project value as the market prepares for a multi-year ex-US copper supply deficit.

- The Section 232 determination and upcoming Chinese demand data are the two principal catalysts for the ex-US copper thesis, with both expected within weeks rather than quarters, allowing key policy and demand assumptions to be tested over the near term.

- Producers, developers, and explorers operating in established mining jurisdictions face fewer permitting and political hurdles, improving their ability to convert stronger copper prices into project advancement and valuation gains.

A 640,000-tonne copper deficit outside the US does not mean global consumption has exceeded mine supply. Instead, it reflects policy uncertainty that has redirected roughly 900,000 tonnes of copper into US warehouses, tightening supply in other markets. Whether those inventories remain in the US or return to global markets will determine how long the resulting price support persists. The Department of Commerce's refined copper tariff determination is overdue and will either reinforce the current inventory imbalance or begin unwinding it within weeks of a decision. Until then, the investment case rests on inventory redistribution rather than a shortage of copper.

TL;DR

The delayed US refined copper tariff decision has redirected an estimated 900,000 tonnes of copper into US warehouses, creating a projected 640,000-tonne deficit outside the US without increasing global demand. As inventories tighten elsewhere and major producers struggle to raise output, advanced copper projects in established mining jurisdictions stand to benefit most from stronger regional pricing. Investors should monitor the Department of Commerce's tariff determination and upcoming Chinese demand data, as both could quickly reinforce or weaken the current market imbalance.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed