Copper Prices Hold Firm Despite a Fivefold Refined Surplus, Shifting the Focus to China's Demand Growth

China's refining boom drove a fivefold copper surplus, but prices remain elevated as future direction depends on whether demand catches up with supply.

- The world refined copper market posted a 239,000-tonne surplus in the first four months of 2026, nearly five times the 47,000-tonne surplus a year earlier.

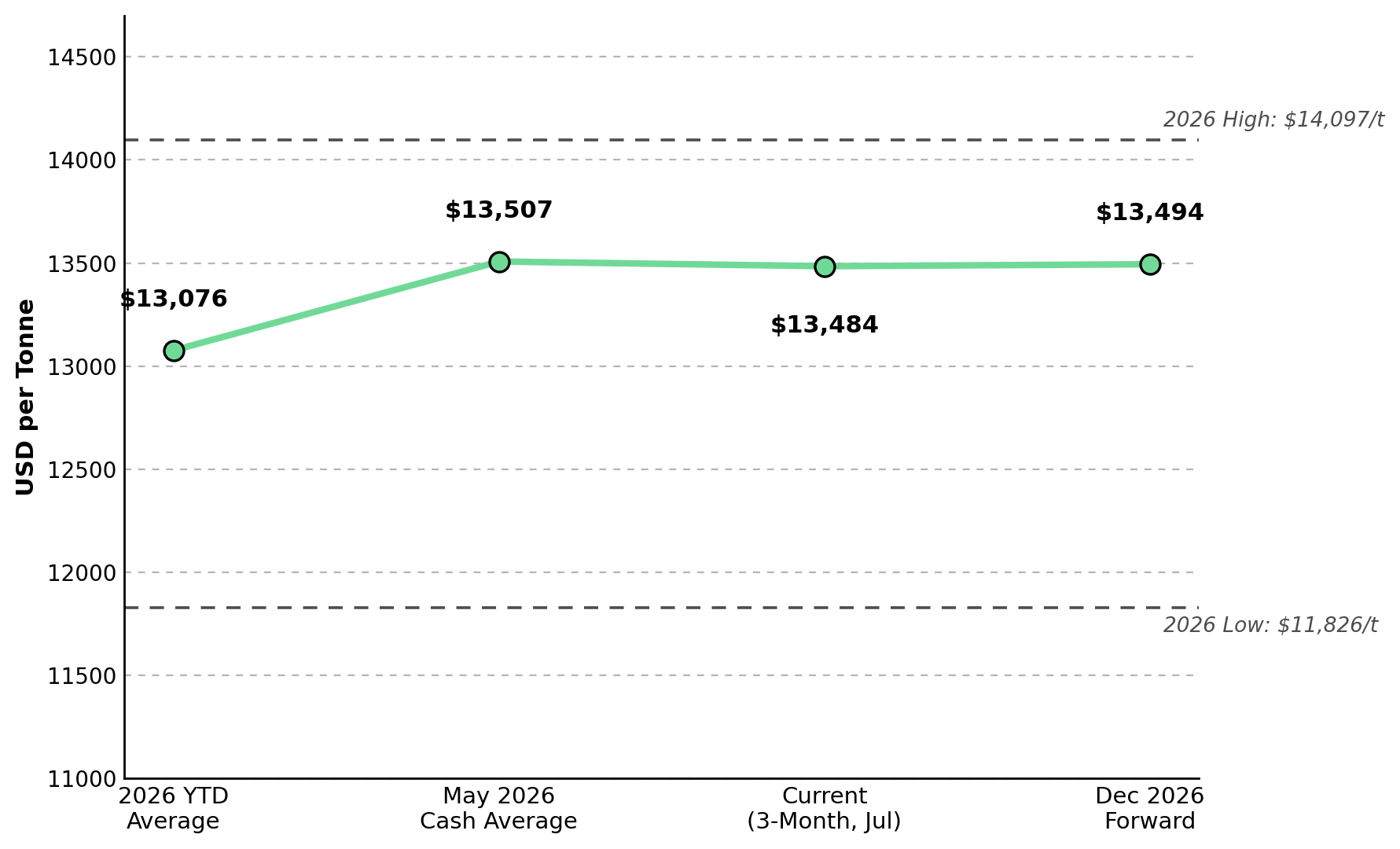

- LME three-month copper closed at $13,484.50 per tonne, with the forward curve in a mild contango from $13,453 to $13,494 per tonne through December 2026.

- Combined LME, COMEX, and SHFE copper inventories reached 1,144,966 tonnes at the end of May 2026, up 54% or 400,851 tonnes from the end of 2025 and the highest level since January 2003.

- China's refined copper production grew 7.4% in the first four months of 2026, offsetting Chile's 7.9% mine output decline, the 40% cut in Grasberg concentrate production, and the DRC's 33% concentrate decline.

- Chinese net refined copper imports fell 25% even as apparent demand grew 2.4%, indicating domestic smelters met more of China's demand instead of relying on imported refined copper.

Mine Supply Disruptions Support Copper Prices While Refined Supply Builds

Preliminary ICSG data showed world copper mine production fell 1.4% in the first four months of 2026, yet LME three-month copper closed at $13,484.50 per tonne, in line with the May cash average of $13,507.13 per tonne and 32% above the 2025 annual average. Concentrate production at Indonesia's Grasberg mine fell 40% in the first four months of 2026 after a severe mud rush disrupted operations. Chilean mine output fell 7.9%, led by lower production at Candelaria, El Teniente, Escondida, Los Pelambres, and Spence.

China's refining expansion prevented mine supply disruptions from tightening the copper market. World refined copper production rose 4% to 9.711 million tonnes in the first four months of 2026, while refined usage increased 2% to 9.471 million tonnes, creating a 239,000-tonne surplus. Despite that surplus, copper still trades 32% above its 2025 average, suggesting prices continue to reflect an earlier supply-disruption narrative rather than current market fundamentals.

China's Refining Growth Outpaces Mine Supply Losses While Copper Surplus Widens

China's 7.4% growth in refined copper production more than offset mine supply losses, explaining why the market moved into surplus despite disruptions at major mines. China and the DRC account for about 60% of global refined copper production, and their combined 7.6% output growth added more refined copper than the supply losses from Grasberg and Chile. Chinese net refined imports fell 25% even as apparent demand grew 2.4%, showing domestic smelters supplied most of the additional demand. Global secondary refined copper production from scrap grew 6.8%, with most of the increase coming from China, adding further supply to the market.

Chile's decline in refined copper production did not tighten the global market because China's refining growth replaced the lost output. Chile's electrolytic refined copper production fell 26% and SX-EW output declined 3.4%, reducing low-cost refined copper supply. China's secondary refined copper production replaced that lost output, keeping refined supply elevated and limiting the scope for a sustained price recovery.

Copper Inventories Reach a 23-Year High While Demand Becomes the Next Price Driver

Combined LME, COMEX, and SHFE copper inventories reached 1,144,966 tonnes at the end of May 2026, up 400,851 tonnes, or 54%, from the end of 2025 and the highest level since January 2003. Rising inventories show refined copper production continues to outpace demand. Consistent with that surplus, the LME forward curve remains in a mild contango from $13,453 to $13,494 per tonne through December 2026, indicating the market expects adequate near-term supply rather than an immediate shortage.

Whether copper prices rise or fall now depends on the balance between Chinese demand growth and refined copper production. In the base case, Chinese apparent demand growth rises from 2.4% to 5% or more, supported by grid investment, EV production, and AI data center construction, reducing the 1,144,966-tonne exchange surplus over two to three quarters and lifting LME copper toward its 2026 high of $14,097 per tonne. In the bear case, Chinese refined production continues growing 7.4% while apparent demand remains at 2.4%, pushing exchange inventories above their highest level since January 2003 and driving LME copper toward its 2026 low of $11,826 per tonne.

Copper Surplus Increases Cost Pressure While Production Efficiency Drives Relative Performance

If copper prices weaken, producers with lower operating costs should be better positioned than higher-cost peers. Lower production at Escondida, El Teniente, Los Pelambres, Candelaria, and Spence increased unit costs by spreading fixed expenses across fewer tonnes. Chile's electrolytic copper production fell 26%, leaving fewer tonnes over which to spread fixed smelter costs. By contrast, Mongolia's Oyu Tolgoi underground project increased production 29%, improving operating efficiency as copper prices remain 32% above the 2025 annual average despite the refined market surplus.

The key differentiator is production cost. Producers that require LME copper above $12,500 per tonne to break even face greater downside risk if the refined copper surplus expands. Oyu Tolgoi's 29% production increase improved operating efficiency, while lower output at Escondida and El Teniente raised unit costs by spreading fixed expenses across fewer tonnes. As a result, Oyu Tolgoi is better positioned than higher-cost Chilean operations if copper prices weaken.

Chinese Demand Growth & Copper Balance Will Set the Next Price Trend

LME copper remains at $13,484.50 per tonne even as the forward curve stays in a mild contango and exchange inventories sit at their highest level since January 2003, indicating prices remain supported despite ample refined supply. Copper has averaged $13,075.57 per tonne this year, 32% above the 2025 average, reflecting earlier supply disruptions at Grasberg and in Chile. As the refined copper surplus grows, future price direction will depend more on demand growth than on mine supply disruptions.

The key question for the second half of 2026 is whether China's refined copper production continues growing faster than demand. If production growth slows while demand remains steady, the refined copper surplus should begin to narrow. The indicator to watch is the gap between Chinese refined production growth and apparent demand growth in each ICSG bulletin. If demand growth exceeds production growth for two consecutive reporting periods, the surplus should continue shrinking and LME copper could move toward the $14,097 base-case target.

The monthly ICSG Copper Bulletin, published with a two-month reporting lag, will provide the clearest signal of where copper prices are headed next. A world refined copper surplus below 40,000 tonnes per month for two consecutive reporting periods would indicate the surplus is shrinking and support higher copper prices. A surplus above 100,000 tonnes per month for two consecutive reporting periods would indicate excess supply is continuing and support the bear case for LME copper to move toward $11,826 per tonne.

Analyst's Notes

Subscribe to Our Channel

Stay Informed