Brent's 6% Rally & Hormuz Blockade Risk Put $85-90 Oil in Focus for Energy-Intensive Miners

Hormuz shipping disruption and low oil inventories lift Brent, raising mining fuel cost risks while sanctions policy shapes the next supply outlook.

- Brent crude gained 6% to $76.34/bbl as renewed US-Iran airstrikes cut Strait of Hormuz ship traffic by 15% and pushed the waterway to a near-standstill.

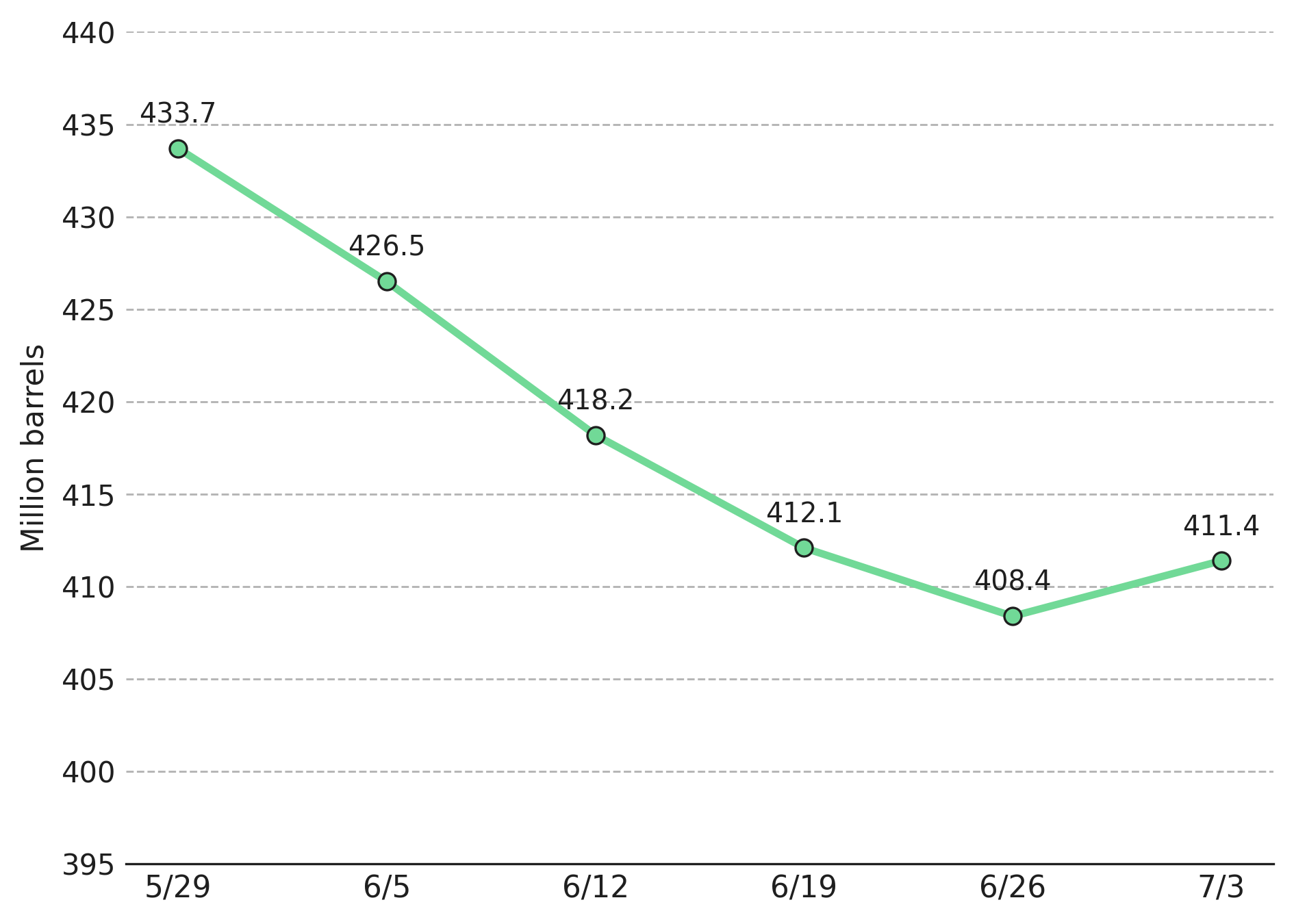

- US commercial crude inventories totaled 411.4 million barrels, 6% below the five-year average, before the Hormuz disruption escalated.

- US distillate fuel inventories totaled 103.6 million barrels, 12% below the five-year average, leaving a thin buffer against a sustained supply shock.

- David Goldwyn said a reimposed US blockade targeting Iranian crude would remove an estimated 1.5 million to 2 million barrels per day from the market.

- Ellen Wald said about 200 million barrels from previously trapped vessels were released under the prior US-Iran memorandum of understanding, equal to about two days of global demand and now largely consumed.

Military Escalation & Shipping Disruptions Extend Energy Cost Pressure

Renewed US airstrikes on Iran cut Strait of Hormuz ship traffic by 15% and pushed the waterway to a near-standstill as vessel owners assessed the escalating security risk. Brent crude gained 6% to $76.34/bbl for the week, while US West Texas Intermediate rose about 5% to $72.15/bbl.

Fighting resumed after a three-week ceasefire as Iranian forces struck US military infrastructure in Gulf states following US attacks on Iranian coastal and eastern provinces. Iran's strike on a Qatari LNG carrier exiting the Strait of Hormuz near Oman triggered the latest shipping slowdown. For mining operators setting quarterly fuel budgets, a conflict now in its fifth month raises the risk of sustained energy costs. The LNG carrier strike also extends shipping risk beyond crude to gas supplies that power Asian processing and smelting operations.

The disruption follows the expiration of the US-Iran memorandum of understanding, which allowed about 200 million barrels from trapped vessels to exit the Strait of Hormuz. Ellen Wald said the volume equals about two days of global demand and has largely been consumed. The EIA Weekly Petroleum Status Report showed US commercial crude inventories totaled 411.4 million barrels, up 3.0 million from the prior week but still 6% below the five-year average before the Hormuz standstill intensified.

Inventory Tightness & Reduced Supply Buffer Increase Oil Price Risk

In the base case, the US and Iran avoid a formal blockade, Iranian exports continue to risk-tolerant buyers, and Brent stabilizes between $72/bbl and $80/bbl, keeping mining fuel costs near current levels. In the bear case, US President Donald Trump reimposes the blockade, removing 1.5-2.0 million b/d of supply and increasing fuel costs for energy-intensive mining operations. A sustained supply loss would tighten physical oil supplies rather than inflate prices through geopolitical risk alone. The bear case would also strengthen gold demand, while higher energy costs compress margins across energy-intensive mining operations.

ClearView Energy warned that Iranian retaliatory strikes on Gulf producers could delay or halt production recovery, tightening global oil markets beyond the impact of a blockade alone. Vandana Hari said Hormuz shipping remains near a standstill, although confidence in renewed US-Iran diplomacy is limiting further gains in crude and near-term fuel costs for mining operations.

Trump said oil markets remain well supplied because vessels cleared the Strait of Hormuz and the disruption would be short-lived. Wald offered a contrasting view, saying Brent should already be trading above $80/bbl. Daniel Hynes said markets were reassured that the Trump administration avoided targeting Iranian energy infrastructure despite the broader escalation. For mining operators budgeting fuel costs, whether crude reflects geopolitical risk or confirmed damage to Iranian production will determine whether current prices become a ceiling or a floor.

Sanctions Policy & Iranian Exports Shape the Oil Supply Outlook

David Goldwyn said Iran will continue exporting crude despite the collapse of the US-Iran memorandum of understanding. Most shipments through the Strait of Hormuz come from Iran or countries with private arrangements with Tehran, allowing those flows to continue. A continued conflict alongside ongoing Iranian exports would limit the immediate supply impact and help contain fuel cost increases for mining operations.

Oil prices depend less on Iran's willingness to export than on the risk of a renewed US blockade. Goldwyn said a reimposed blockade would remove an estimated 1.5-2.0 million b/d from the market, increasing fuel cost risk for mining operations. A tighter sanctions enforcement could discourage buyers, restrict Iran's oil revenues, and delay a near-term diplomatic resolution.

Refining Constraints & Higher Fuel Costs Pressure Mining Margins

A blockade that keeps Brent above $85-90/bbl would raise fuel costs and compress margins at energy-intensive mining operations, including nickel HPAL facilities and copper smelters that price energy on quarterly benchmarks.

EIA data showed US refineries operated at 95.8% of capacity, leaving little spare processing capacity to absorb import disruptions. Mining operations relying on long-haul shipping through Asian ports face higher bunker fuel costs if the Strait of Hormuz disruption lasts more than two to three weeks. Widening diesel and distillate crack spreads signal tightening fuel supplies before confirmed disruptions, providing an early warning for mining fuel costs. Mining companies with the highest energy costs as a share of cash costs are likely to see margin pressure first.

EIA Inventory Trends & Oil Supply Tightness Guide the Next Price Move

Brent at $76.34/bbl reflects near-standstill Hormuz shipping and US crude inventories of 411.4 million barrels, 6% below the five-year average. Both factors must persist to support current oil prices. A formal US-Iran ceasefire or a new memorandum of understanding allowing non-Iranian vessels to resume Hormuz transits would reduce the current risk premium. The first agreement released about 200 million barrels from trapped vessels, much of which has been consumed, limiting the fuel cost relief a second agreement could provide to mining operations.

The EIA Weekly Petroleum Status Report is the key indicator of whether supply disruptions are reaching the physical oil market. The latest report, covering the week ending July 3, predates the Hormuz standstill and does not capture its physical supply impact. It showed crude inventories rising by 3.0 million barrels while distillate stocks fell by 5.0 million barrels to 12% below the five-year average. The July 10 report, due July 15, will be the first to reflect the Hormuz disruption. Consecutive crude draws and further distillate declines would confirm physical supply tightness, support Brent above $80/bbl, and move oil prices closer to the $85-90/bbl range where fuel costs begin compressing margins at energy-intensive mining and smelting operations.

Analyst's Notes

Subscribe to Our Channel

Stay Informed