Cartier Resources (TSX-V: ECR) - Valuing a Company’s Assets

Interview with Philippe Cloutier, President & CEO of Cartier Resources (TSX-V:ECR)

Founded in 2006, Cartier Resources Inc. is an exploration company focused on the Abitibi gold belt in Quebec, one of the best mining territories in the world. The company’s mission is to ensure growth and sustainability to benefit all shareholders and employees. It seeks to develop current and future assets into mineral production with a schedule consistent with its human and financial resources while respecting sustainable development practices.

Merlin-Marr Johnson caught up with Philippe Cloutier, President, CEO, and Director, Cartier Resources. Mr. Cloutier holds a B.Sc. in Geology and a certificate in Human Resource Management. He has over 25 years of experience in the mining exploration and development business. He previously worked for industry leads such as Noranda Inc, Aur Resources Inc, and Soquem. Mr. Cloutier played a lead role in the discovery and delineation of the Bell-Allard South Copper-Zinc Mine in Matagami, Quebec. Since September 2002, he served as a member of the Order of Geologist professional inspection committee.

Company Overview

Cartier Resources Inc. holds a portfolio of advanced-stage exploration projects in the Abitibi Greenstone Belt in Quebec, one of the most prolific mining regions in the world. The company is primarily focused on gold. It is headquartered in Quebec, Canada.

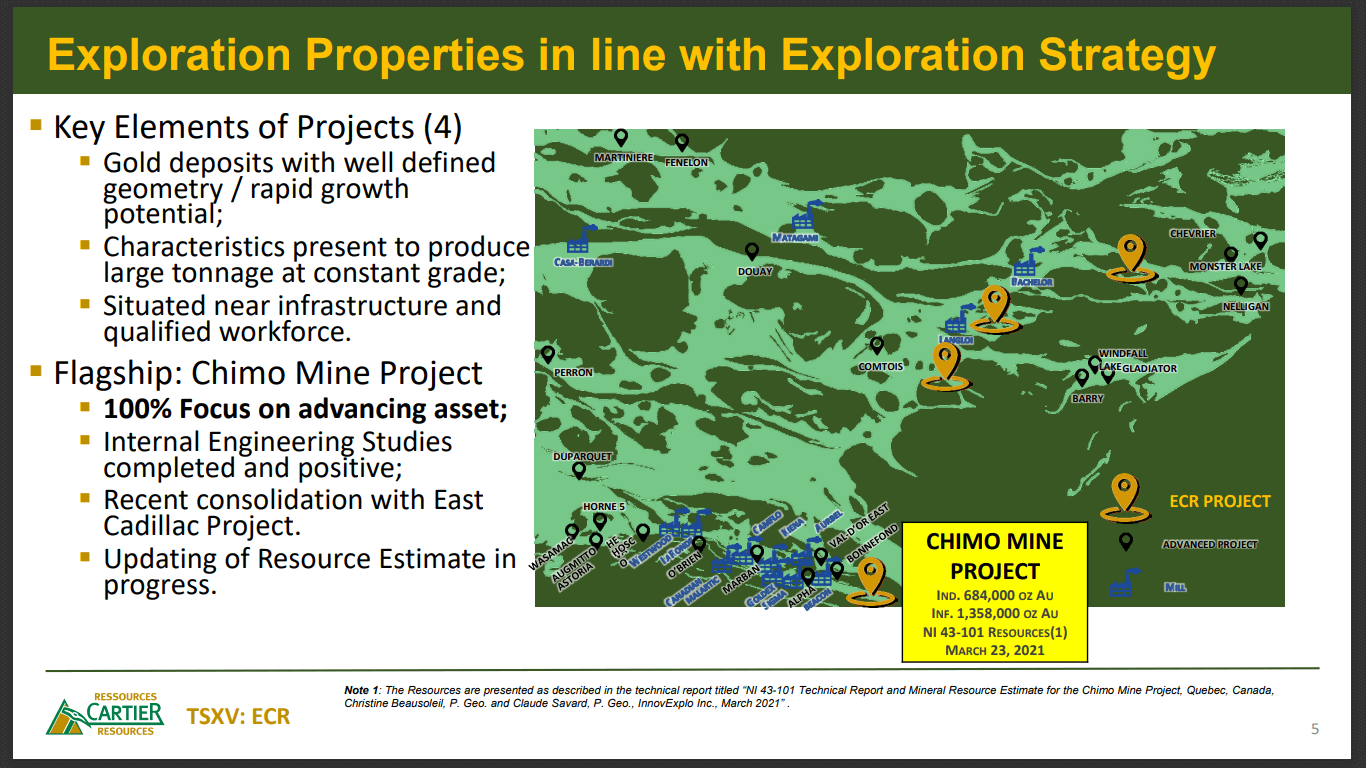

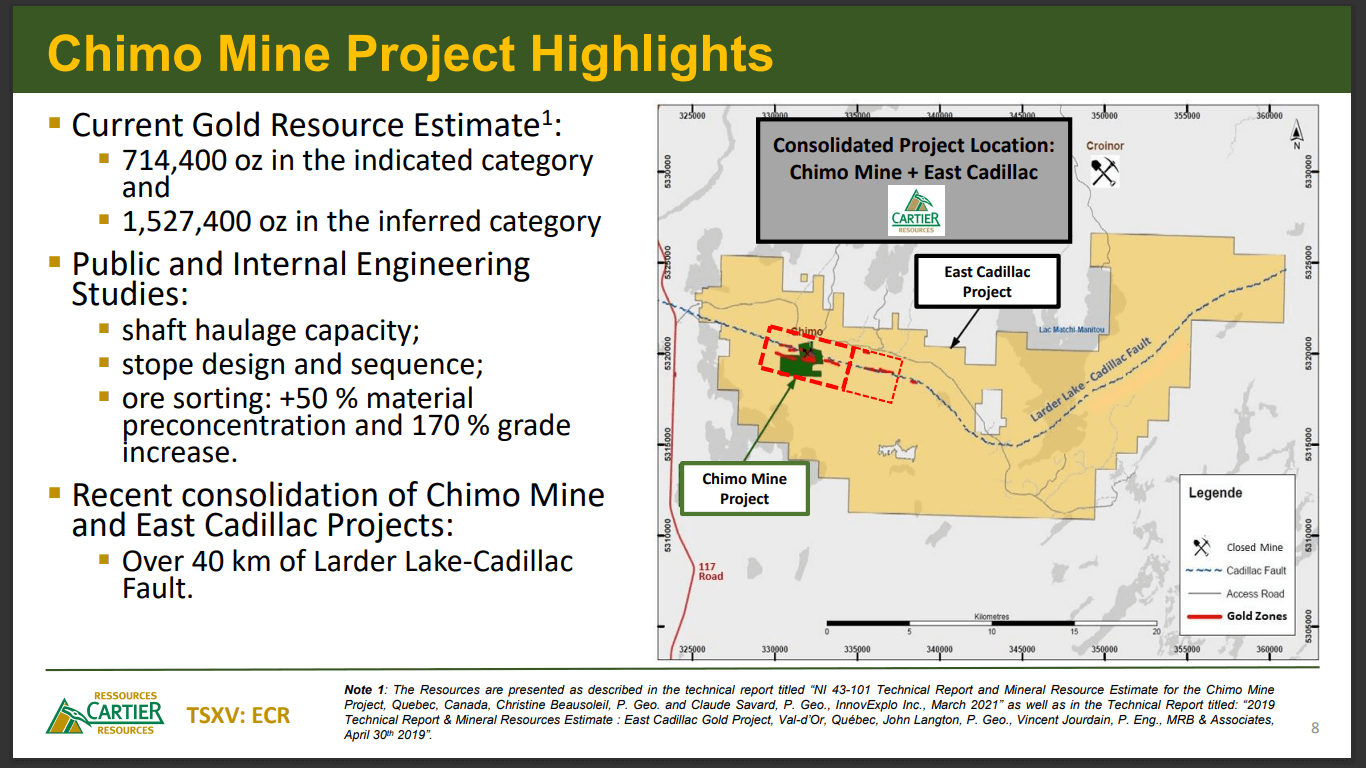

Cartier Resources’ flagship asset is the Chimo mine project, which spans almost 40km of the Larder Lake Cadillac fault. Recently, the company embarked on a 25,000m diamond drill program and published a fourth mineral resource estimate for the project. The company is also working on a PEA (Preliminary Economic Assessment).

The Shareholder Base

Currently, the company has 278M outstanding shares that comprise 17.7% ownership by Agnico Eagle Mines, 16.6% by O3 Mining, and between 8%-10% by Quebec Sovereign Fund’s management and board. In the long-term or 10-15 years, the retail ownership is about 26%, providing a 32% free float for the company.

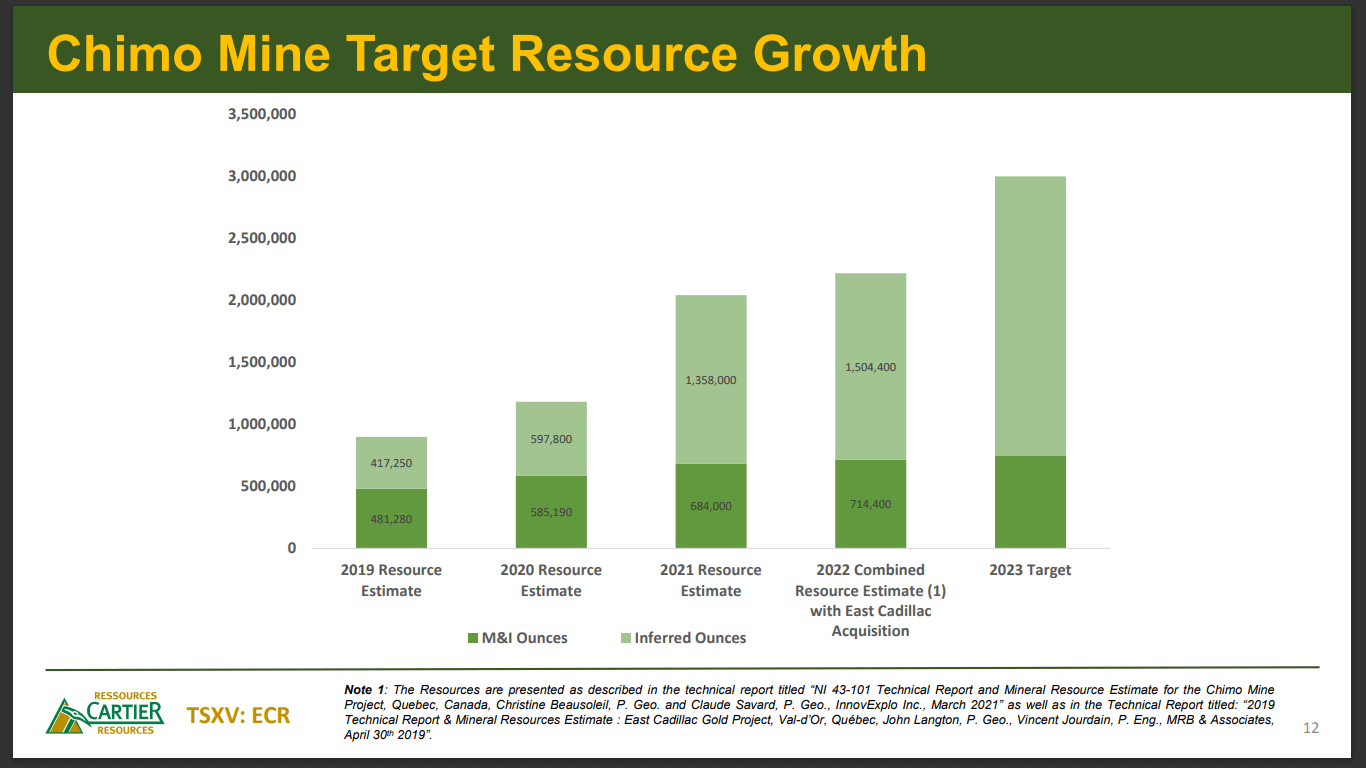

According to Cartier Resources, the 32% free float has turned around in the last few years. The company has been successful in constructing an entirely new demographic of shareholders, which is the result of its 2016 accomplishments. In 2012, during the ongoing financial crisis, the company was reoriented to focus on higher-level projects and more advanced exploration projects. As a result, the company bought 4 projects that featured historical deposits and resource estimates. One of the projects, the Chimo mine, ended up being the company’s flagship project. This project attracted Agnico Eagle who contributed $4.5M to the treasury in exchange for 19.9% of the company’s shares. This sponsorship attracted over $15M in 2017.

Between 2017 and 2020, Cartier Resources drilled 60,000m on the Chimo mine project and produced 3 resource estimates. In 2022, the Chino mine project was a smallish land position with a 2km strike length. The company was faced with property boundary issues. It was cognizant that the mineralization extended to the east, the west, and at depth. The mineralization eventually plunged onto the competitor’s ground at a depth of 2km. As a result, the company began working towards a partnership or consolidating the land position. In 2021, the company carried out exploration on a different project and produced the third resource estimate on Chimo. This development started the discussion towards mine consolidation.

The company was able to close the deal with O3 Mining in the Q1-early Q2 of 2022. In exchange for 100% ownership of O3 Mining’s land position, it was tendered 17.5% ownership of Cartier Resources. The payment was almost entirely made in shares, which are expected to be re-rated as the Chimo asset observes growth.

During this time, Agnico Eagle had been diluted to 13%, and it exercised an investor rights agreement with a participation rate. This led to the most recent $1.8M financing, which is essentially an exercise of Agnico Eagle’s participation rights. This enabled it to climb back to 17.7% ownership of Cartier’s shares.

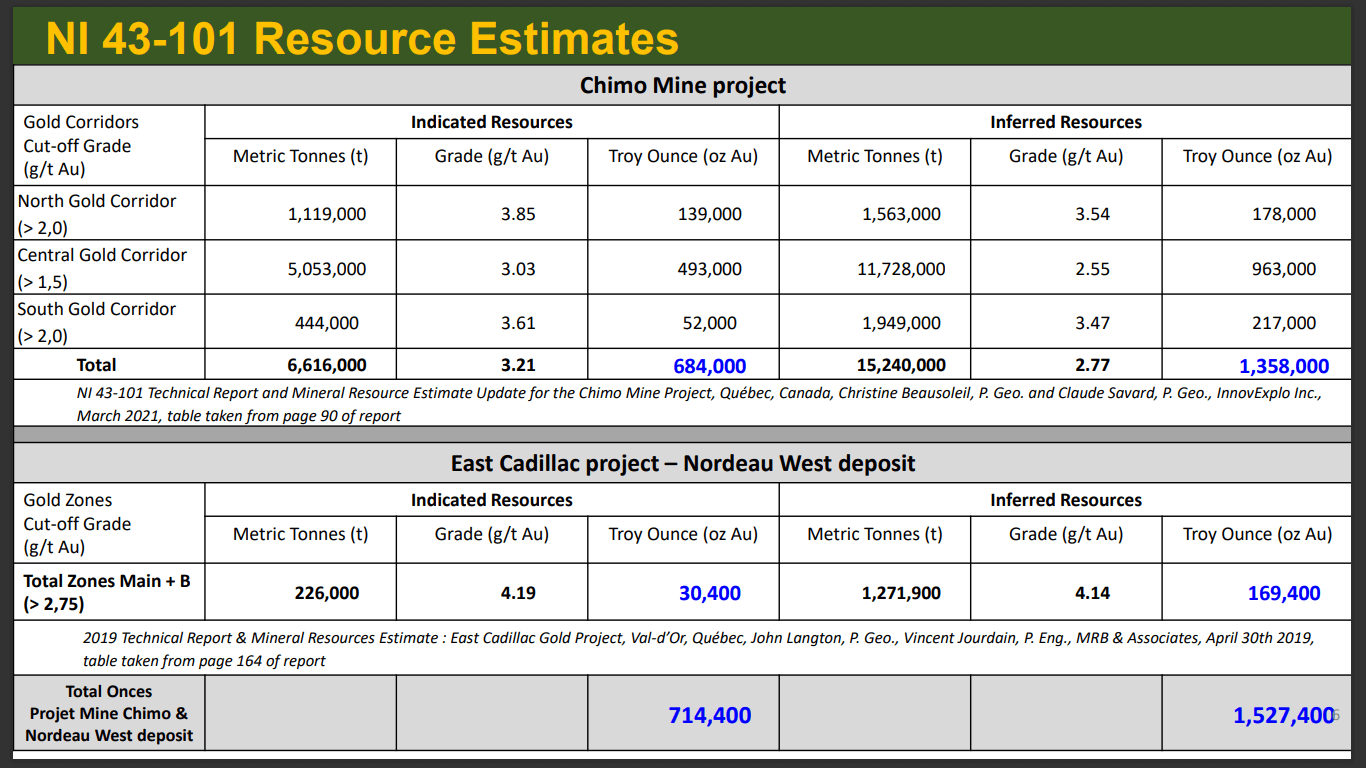

By mid-2022, Cartier Resources had $6.5M in cash flow. The company geared up to design the exploration program to further investigate the mineralization extension identified at the Chimo mine. At the same time, the company quoted the addition of the resource estimate on the Nordeau West which is located 450m east of Chimo mine’s infrastructure and the resource. These were added to the main resource.

IIROC (The Investment Industry Regulatory Organization of Canada) regulators mandate that in order for the resources to be added together, it needs to be produced by the same issuer. In this case, both resources were produced by two different issuers on different dates. Hence, at the end of August, the company provided a consolidated resource estimate of the Nordeau West deposit to the Chimo mine project’s gold system.

After adding the indicated resource, it features 720,000oz indicated gold and 1.633Moz gold in the inferred category. It is important to note that all the inferred ounces are within or near the Chimo mine past-producing infrastructures, shaft, and drifts. Once this was delivered, the company focused on the project’s PEA which was launched in November 2021. Since then, between 70M-80M company shares have changed hands due to various reasons including investor impatience, market conditions, and the fact that the funds are being repositioned onto different industries.

70M-80M shares account for almost 20% of the company’s float. This needs to be looked into as 40% of the float is in a tight spot. While there have been sellers, the company has also seen some astute, sophisticated buyers that understand that the company is undervalued. Cartier Resources is on the production path and it may take months to years in order to deliver the next value proposition.

The Market Landscape

Cartier Resources’ investors are interested in de-risking the project. Mining companies that went into M&A (Mergers and Acquisitions) years ago would focus on the ounce count, which takes away some of the risk factors. The funds are closely monitoring the company’s project. There is ongoing criticism when it comes to the project’s grades. The project’s grades are similar to the competition along the fault that is bulk-mined underground. This is not an issue for the company as it has already demonstrated that the mineralization is amenable to ore sorting. The company anticipates that the grade will be doubled by the time it is brought to the surface.

Notably, the company’s drill program is strictly focused on growing the resource base. At this time, it does not plan on conducting infill drilling. The company has a project with a highly-robust database, which lends to the de-risking component. The company has seen competition and examples of 25 years of mining innovation being put into practice locally, including underground vertical conveyors, ore sorting, bulk mining, and various metallurgical advancements.

The Young-Davidson mine, the Lower mine, the Alamos project in Matachewan, and the Odyssey project, which is a partnership between Yamana Gold and Agnico Eagle are all mining relatively low grades at a 1km depth. The company is looking at the conditions and is building it into the PEA. It is building in the risk-lowering elements in order to develop a robust PEA that will cater to the project’s local mining attributes. This will also provide a path for the company moving forward as it continues building ounces, de-risking the project, and moving closer to the production path. The company’s project is based on a tier-1 jurisdiction and provides favourable manpower access in a proactive fiscal and political jurisdiction.

Between 2017 and 2019’s drill operations, the company collected a sufficient number of representative samples that were sent to Steiner facilities in Kentucky that has ore sorting calibration techniques and a metallurgical lab in Quebec. Both independent tests came back with relatively the same conclusions: by mining the mineralization underground at Chimo, the ore sorting process can separate roughly 50% of the mined material into waste and ore, and enhance the material grade by about 170%.

The mineralization was identified using XRF (X-ray fluorescence) and optical methodology. Interestingly, the Chimo project has 6 different fasciae of mineralization present underground, two of which are in the quartz component that’s essentially free gold. The rest is variably interlocked in the arsenopyrite mineralization that is present underground in high-grades, medium-grades, and low-grades. Both XRF and Optical sensors are able to sort out the grades with high efficiency. If the company is able to take 50% of the material that was blasted and sorted as waste during primary crushing. The remaining 50% material won’t make it to the surface.

The company seeks to continue running tests. Optimally, additional crushing will provide better ore sorting, but the trade-off here is the extra cost that would need to be fine-tuned. Originally, the company was seeing the ore-crushing cells at the surface. For the PEA, the company is looking to blast roughly 5,000t/day but only haul about 2,500t to the surface. The remaining 2,500t will be used to backfill some of the stopes. The company seeks to use the shaft and the ramp capacity to exit about 2,500t/day material with grades higher than the ones indicated in the resource estimate.

This strategy also allows savings on hauling and transportation costs while also eliminating further environmental scarring at the surface. The company has plans to build a mill on-site to process the material. It is looking at a build-it-yourself strategy as toll milling will always continue to exist. Once the company has a mill in place, it could offer a processing facility to other producers which, in turn, would generate additional value.

The company is cognizant that the market is unappreciative of the finer details of ore sorting and different techniques. It is important to note that when a project is advanced, it caters to a different audience, which is the corporate world or the fund managers, both of which have the sophistication to appreciate the ore sorting techniques and strategy. Retail investors, on the other hand, do not appreciate the finer details of ore sorting. Even the fact that Quebec has hydroelectricity, which can make mining operations greener is lost on the retail audience. According to the company, the 70M-80M shares that were treaded and flipped over are expected to be recuperated by the tranche of retail investors.

Financial Considerations

Cartier Resources has the financial resources to continue advancing the project for at least another year and a half. It plans to continue building value and de-risking the project, namely on the drilling and resource aspects along with the PEA. This will help the company in getting to a better place. In a case where the markets continue to be negative, the company is open to taking a different approach.

The company anticipates that if the drilling and project advancing stops, investors will speculate that the project is stalled and will be attracted to the projects that continue to work. Also, if the company continues to operate while other operations have stopped working, it will free up news flow or the awareness capacity that can be generated. The company intends to continue working as the project has demonstrated clear indications of growth potential. The O3 Mining transaction is a testament to the project’s growth capacity. Now that the company is no longer restricted by the project’s boundaries, it can investigate the mineralization through continued drilling in the east, the west, and at depth. The project PEA will tackle the high-cost line items. Notably, PEAs are designed to showcase the project’s potential worth, ongoing work, and future plans.

The recent inflationary headwinds have hit mining projects, forcing companies to rethink the heavy-cost line items. The company will benefit from this as it plans to build all the new findings into the PEA. Since the Chimo asset already has a shaft, there are several ways to attack the deposit such as the use of vertical conveyors, ramps, building underground ore sorting facilities, and more. As the asset is located in Quebec, the company also has the option to develop a new fleet of electric vehicles and eliminate ventilation fan pipes since diesel is not being used as fuel. Building in better mining techniques, technologies, and metallurgical approaches helps the company benefit from what is being done on a local level.

Both Agnico Eagle and O3 Mining have the opportunity to put a member on Cartier Resources’ board. This right is by virtue of the investor rights agreement. Since 2016, neither company has elected a person for a position on the board. All three entities have had a strong working relationship since the very beginning, sharing detailed project information. Since the project has evolved considerably since it first began, Cartier Resources has levelled off the information asymmetry by providing the markets and competitors access to the data room by way of NDAs (Non-disclosure Agreements).

O3 Mining has a team member on the company’s board. Notably, the local juniors have been highly collaborative. The cross-pollination of ideas and different approaches to exploring the project can take an asset to a different level. Cartier Resources is cognizant of the benefits of sharing ideas and approaches.

Market Valuation

In order to measure market evaluation, Cartier Resources looks at its’ peers' ongoing activities. Some recent transactions include Monarch Mining Corp. with Yamana Gold for the Wasamac deposit and QMX Gold’s acquisition by Eldorado Gold. The company anticipates that the Eldorado-QMX deal was mostly done on a land package basis rather than an ounce count approach. The Yamana Gold-Wasamc deal had been relatively well-priced with a Feasibility Study, it was on an NPV (Net Present Value) metric. Cartier Resources would need to reduce the resource to an ounce metric to have a fair comparison in the same jurisdiction.

Using the PEA, the company is looking to compare the current M&A transactions on a new set of metrics. In the last 12 months, the inflation and runaway CapEx (Capital Expenditure) have caused gold price fluctuations and a rise in material costs. The company is looking to include all these changes in the PEA, however, the market conditions make it very difficult to properly price an asset. The company continues to advance the project, navigating the waters, and adjusting the sails as needed.

Cartier Resources has put together a property around a past-producing mine with a highly robust and extensive data set that has provided clear geological vectors that have profited the company’s exploration approach. It is important to note that the company’s drill success rate has been tremendous. It was able to develop a 2.3Moz resource with just under 60m of diamond drilling. This is a very small panel that is 3km in strike length that extends down to 1.5km at depth. The company now has a system that is in the 2,700oz/ vertical metre range, which is relatively robust. Now that the boundaries have been eliminated, the company can continue growing the project. The company anticipates that its drilling operations are as low-risk, high-reward as they can possibly get.

The PEA team is in active discussions with the exploration team and chaperoning engineers in order to get the best results in the situation. Since the current ounces have a lot higher value in the first 10 years of mining, the company does not plan on infilling the inferred resource to the indicated category.

The project PEA will provide the analysts and fund managers with a metric that can be used for company evaluation. For the company, the PEA will serve as guidance to continue advancing the project in the most optimal way. The company is on a pathway-to-production approach to advance the project. It is cognizant that the markets will continue to be difficult for juniors and seniors alike, as they have been for the past 3-4 decades.

The bull markets of the upticks are becoming shorter, while the downticks are becoming longer. As a result, the company is focusing on advancing the project in order to continue being relevant in the market. Cartier Resources seeks to be in a position that offers the best value for its project, either for a transaction or for continuous advancement. This would enable the company to either build the project on its own or by way of M&A activity.

For instance, if a group in the camp is currently mining 100,000oz-120,000oz/year, the acquisition of Chimo will enable it to extract the same amount while producing between 300,000oz-350,000oz on a yearly basis. The production metrics are expected to keep moving upward.

Targets 2022 and Beyond

Cartier Resources is anticipating partial drill results before Christmas. It is working diligently on the PEA which is expected to be completed by either Q4 2022 or Q1 2023. The PEA would be a robust and credible foundational document that will enable the company to keep moving forward. As per the company, people are shutting down drills on a local level. This serves as an opportunity for Cartier Resources as there will be more labs, machines, and personnel available.

Cartier Resources has $6M in current cash flow. The company isn’t looking to raise additional capital at the moment. Notably, the cash that is currently hitting the market is largely dilutive in nature. The company is drilling two solvent zones right now and it does not want to be in a position where it would need to take a decision to downsize or curtail the program.

In Canada, there is always a tax loss in selling during the flow-through season, which happens around October-November. As a result, there is an extraordinary amount of pressure on junior stocks in parts of the world during this time period.

The current market conditions are providing a lot of mining companies with the capacity to go out and hunt down some very good value propositions and investment opportunities. Cartier Resources continues to raise awareness and build value in the project, anticipating a market turn.

To find out more, go to the Cartier Resources website

Analyst's Notes

Subscribe to Our Channel

Stay Informed