Ceasefire Expectations Drive Brent Crude 10% Lower as Markets Reassess Inflation and Equity Risks

Oil prices plunged over 10% as markets priced a potential US-Iran ceasefire, but the rally depends on a political approval that has not yet occurred.

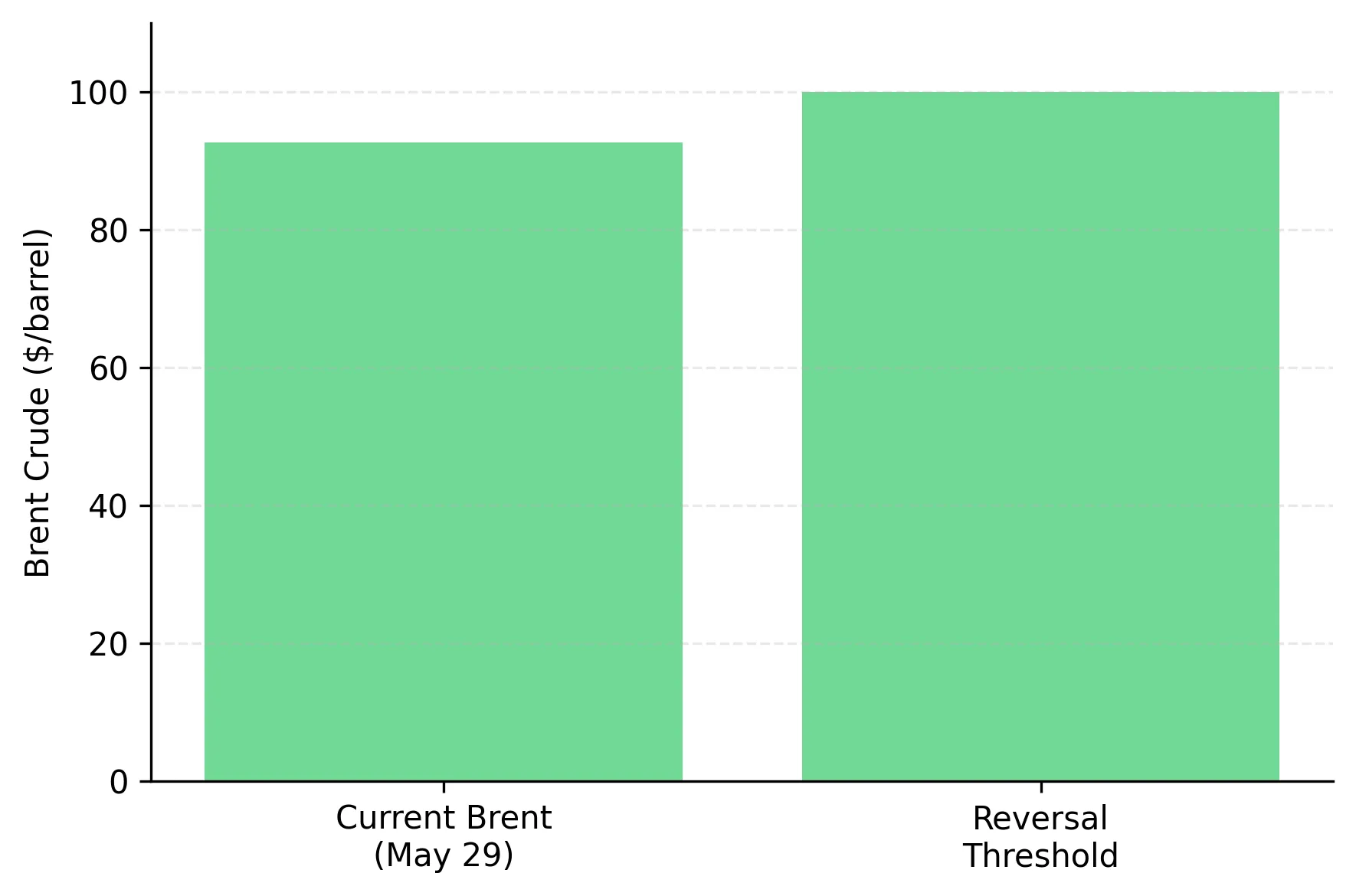

- Brent crude fell to $92.69 per barrel on May 29 after reports that a proposed US-Iran ceasefire could reopen the Strait of Hormuz, reducing the risk of disruption to roughly 20% of global oil trade.

- The decline left Brent more than 10% lower for the week as traders reduced the probability of a Strait of Hormuz supply disruption.

- Euro area inflation held at 3% in April, above the European Central Bank's 2% target, leading markets to price a 91% probability of a 25-basis-point rate increase on June 11.

- The agreement still requires approval from US President Donald Trump, leaving the ceasefire and the reopening of the Strait of Hormuz unconfirmed.

- If the agreement fails, oil prices could rebound as traders reprice Strait of Hormuz disruption risk, increasing fuel costs and inflation across oil-importing economies.

US-Iran Ceasefire Expectations & Record Highs in Global Equities

Global stocks reached record highs on May 29 after reports that the US and Iran had reached a ceasefire agreement that could reopen the Strait of Hormuz, reducing concerns about oil supply disruptions. Brent crude fell about $1 to $92.69 per barrel and more than 10% for the week, while the S&P 500 held near its record close of 7,563.63 as investors priced lower oil supply risk.

The selloff reflects lower expectations of disruption in the Strait of Hormuz, not an increase in actual oil shipments. Jason Wong, senior market strategist at BNZ, said traders were removing the premium they had added for the risk of supply disruptions. Oil prices have fallen because traders expect supply risks to decline, not because export volumes have increased.

Strait of Hormuz Supply Risk & Brent Crude Price Volatility

The Strait of Hormuz carries about 20% of global oil consumption, making disruptions to shipping a key driver of oil prices. During the conflict, traders pushed oil prices higher to reflect the risk that shipments through the Strait of Hormuz could be disrupted. Reports of a ceasefire reduced disruption concerns, sending oil futures lower before any increase in physical supply occurred.

The ceasefire has not been approved, leaving its implementation uncertain. The agreement still requires approval from President Trump before it can take effect. Oil prices are reflecting expectations that the agreement will be approved, not a ceasefire that has already taken effect. Any delay or rejection could force traders to rebuild the supply-risk premium removed during the past week.

Lower Oil Prices & Delayed Impact on Inflation & Energy Costs

Markets can reprice oil within hours, but physical energy supply takes longer to respond. Refinery operations, shipping contracts and fuel inventories can take weeks to adjust after a change in supply expectations. Even if the ceasefire is approved, lower oil prices may take weeks to reduce fuel and transportation costs for businesses and consumers.

Investors should watch the euro area inflation release on June 2 because it will show whether lower oil prices are feeding through to consumer prices. A lower inflation reading would support the view that falling oil prices are reducing cost pressures across the euro area. A higher reading would suggest lower oil prices have not yet reduced consumer and business costs.

Input Costs & Profit Margins Across Energy-Intensive Sectors

Falling oil prices have the largest near-term impact on sectors where fuel is a significant operating cost. Airlines, transportation companies, chemical producers and energy-intensive manufacturers benefit when oil prices fall because fuel and feedstock costs decline. Energy producers face lower revenue when oil prices fall because they receive less for each barrel sold.

Retail investors should focus on how companies manage higher energy costs rather than trying to predict the outcome of ceasefire negotiations. The key question is whether a company can maintain profit margins if oil returns to $100 per barrel. Companies with diversified supply chains, low debt and the ability to raise prices are better positioned to protect profits if oil prices rise again.

Investors cannot know whether or when the ceasefire agreement will be approved. Because oil prices depend on a single approval decision, investors should avoid building portfolios around a specific ceasefire timeline. Diversified portfolios are less exposed to a failed ceasefire than concentrated bets on lower oil prices.

Brent Crude at $100 & Reversal Risks for Inflation and Equities

The recent rally in equities and decline in oil prices depends on Brent crude remaining below $100 per barrel. If Brent remains below $100 per barrel and ceasefire talks continue, lower fuel costs could support corporate margins and reduce pressure on central banks to keep interest rates higher for longer.

A collapse in ceasefire negotiations or renewed threats to shipping through the Strait of Hormuz would challenge the recent decline in oil prices. Either event could push Brent back toward $100 per barrel, increasing fuel costs, raising inflation and reducing profit margins for energy-intensive businesses.

Investors should track Brent crude prices, official updates on ceasefire approval and the euro area inflation release on June 2. Euro area inflation was 3% in April. A reading above 3% would suggest lower oil prices are not yet reducing consumer costs, while a lower reading would support the view that fuel costs are feeding through to inflation.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed