Flagship Minerals' Completes Isidora Metallurgical Programme with New Canadian Copper Asset to Portfolio

.jpg)

Flagship Minerals adds BC copper project, exits lithium, and advances its 2.1Moz Isidora gold project in Chile toward a 2026/27 resource update.

- Flagship Minerals has acquired the Whipsaw Copper Project in British Columbia, adding a Tier-1 jurisdiction copper option alongside its 2.1 million ounce Isidora Gold Project in Chile.

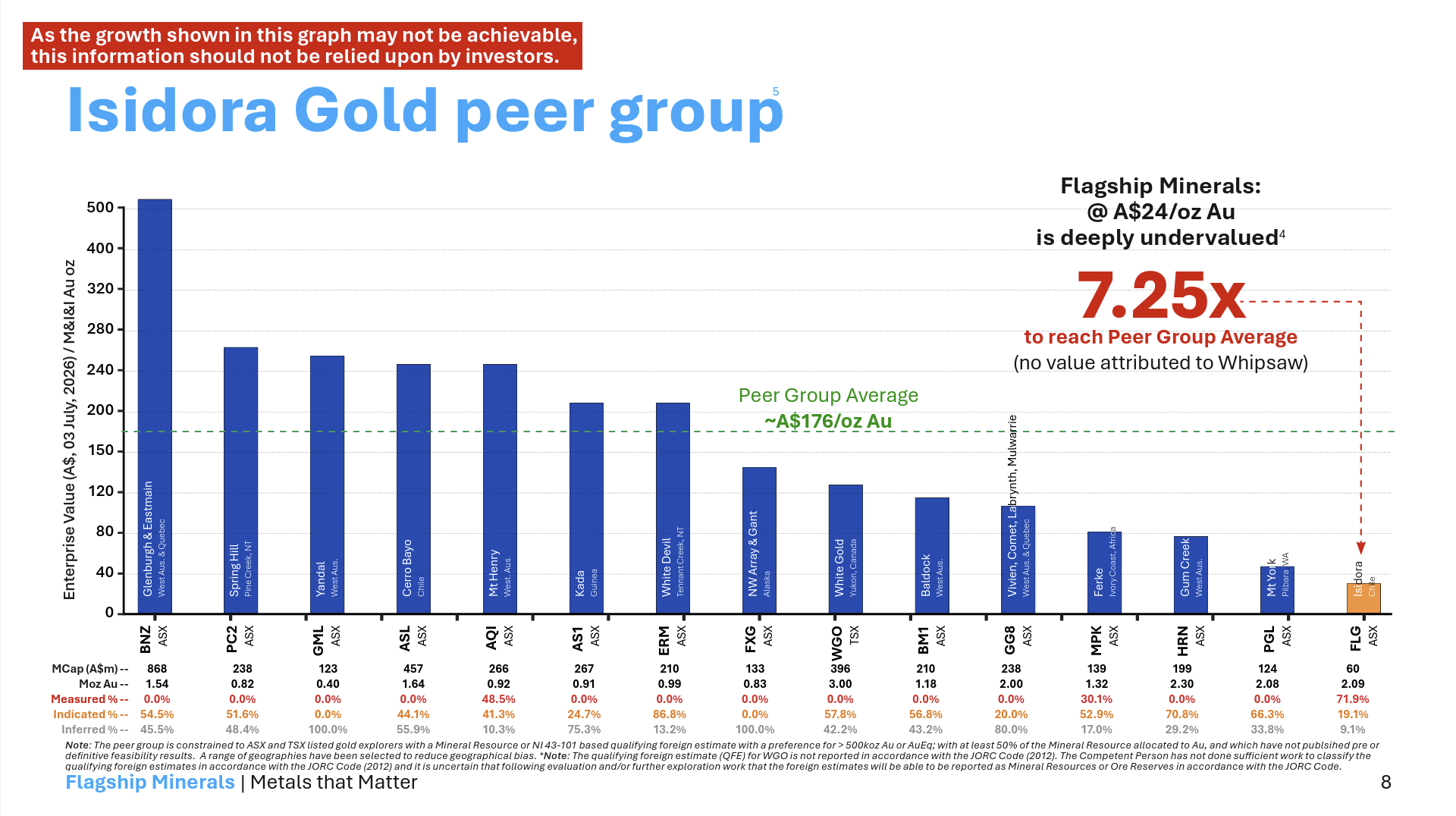

- Managing Director Paul Lock says Isidora trades at roughly A$24-25 per resource ounce against a peer average near A$176, a gap he attributes largely to dilution risk rather than asset quality.

- Flagship has completed its planned metallurgical drilling and trenching programme at Isidora and is now running infill and extension drilling targeting an updated resource in late 2026 or early 2027.

- The divestment of the RK Lithium Project for $4 million (~A$5.8 million) cash completes Flagship's transition to a dedicated gold and copper explorer and developer.

- Whipsaw carries a JORC Exploration Target of 0.51 to 1.02 billion tonnes at 0.2-0.4% copper equivalent with Flagship weighing further drilling against a potential spin-out into a standalone ASX-listed vehicle.

Junior gold and copper developers are increasingly judged on more than a single flagship asset - investors want a growth pathway and optionality that doesn't rely on one drill result. Flagship Minerals (ASX:FLG) has spent the past month reshaping itself around exactly that idea, adding a large-scale copper option in Canada, completing a key stage of test work at its Chilean gold project, and exiting its lithium interests entirely. Managing Director Paul Lock discussed the rationale behind each move and where the company goes from here.

A Two-Commodity Growth Story Takes Shape

Flagship's strategy has shifted noticeably over the past two months. Back in May, the company's investment case rested almost entirely on Isidora, a single Chilean gold asset working through resource expansion. Since then, Flagship has acquired a large copper option in British Columbia, signed a binding agreement to exit its Thai lithium interests and completed a metallurgical milestone at Isidora - three moves that, taken together, amount to a deliberate repositioning as a dedicated gold and copper explorer and developer.

Lock frames this as disciplined rather than opportunistic. Flagship's stated strategy is twofold: advance Isidora toward production readiness, and secure additional gold or copper opportunities with scale, long mine life and strong development potential in established jurisdictions. Whipsaw was selected specifically because it offered certainty without requiring Flagship to fund a speculative, ground-up exploration programme - the asset already carries decades of historical drilling, geophysics and geochemistry, meaning Flagship is paying for a defined target rather than a blank slate.

Isidora Gold's Path to Feasibility

Metallurgical Programme Complete, Resource Update Targeted on 2026

Flagship's flagship asset remains the Isidora Gold Project in Chile's Maricunga gold belt, which carries a mineral resource estimate of 115.2 million tonnes at 0.56g/t gold for 2.1 million ounces. The resource splits into 84.26Mt at 0.56g/t (1,505koz, 71.9%) measured, 21.07Mt at 0.59g/t (399koz, 19.1%) indicated, and 9.86Mt at 0.60g/t (190koz, 9.1%) inferred, using cut-off grades of 0.16g/t for oxide, 0.27g/t for transitional and 0.31g/t for sulphide material.

The company has now completed a metallurgical drilling and trenching programme comprising four large-diameter (PQ) metallurgical holes for a combined 600.5m and five trenches totalling 600m. Drilling and trenching intersected numerous zones of visually apparent mineralisation. Core processing is nearing completion, with samples headed to a testing laboratory in Chile.

That material will support a "pilot-scale" test programme built around a 300-400 tonne bulk sample, subjected to dump leach test work focused on leach kinetics, gold recoveries and reagent consumption. With the metallurgical rig work finished, Flagship has moved the drilling programme on to infill holes targeting inferred and unclassified mineralisation within the current pit shell, to be followed by extensional drilling around the 2026 pit shell and confirmatory drilling of historical RC holes. The company is targeting an updated mineral resource estimate for late 2026 or early 2027.

Water, Permitting and Community Engagement

Beyond the resource and metallurgical work, three factors will determine how quickly Isidora can move toward a construction decision: water, permitting, and community support. Water supply is the most commonly cited technical risk for projects in the high-altitude Maricunga belt. Neighbouring producer Rio2 trucks water approximately 160km from near Copiapo at sea level up to its Fenix mine site at roughly 5,000m elevation, and still achieves bottom-third-of-the-cost-curve economics. Lock indicated Flagship has been running its own water studies and believes it has found a solution that would materially derisk the project.

On permitting, Flagship's baseline flora and fauna studies have found no material issues to date, and the company points to Chile's current Kast government as having signalled intent to accelerate approval timelines relative to the previous Boric administration, under which Fenix obtained its own permits. Flagship is drawing directly on Fenix's permitting experience as a template for structuring its own applications. Environmental studies began in December 2025 and are expected to conclude around the first quarter of 2027, feeding into a basic mine plan that will support both the environmental submission and the prefeasibility study running in parallel.

On the social side, Lock described community engagement as a priority since the project's earliest stages, including efforts to involve local workers in Flagship's own workflows, and said a more formal announcement on community relationships is likely later in 2026. Flagship is targeting PFS for early 2027.

Interview with Paul Lock, Chairman & MD of Flagship Minerals

A Tier-1 Option Next to Copper Mountain

On 18 June 2026, Flagship announced the acquisition of the Whipsaw Copper Project in British Columbia, located roughly 160km east of Vancouver and just 17km west of Hudbay Minerals' operating Copper Mountain mine, which runs a 45,000-tonne-per-day plant. The project carries a JORC (2012) Exploration Target of 0.51 to 1.02 billion tonnes at 0.2-0.4% copper equivalent (0.14-0.23% Cu, 86-147ppm Mo, 1-2ppm Ag and 0.01-0.02ppm Au) across a mineralised system extending approximately 3.7km in strike length and up to 1.2km in width, which remains open.

Lock framed the acquisition as a way to give shareholders exposure to copper without diverting management focus or capital from Isidora, pointing to a smaller ASX-listed copper porphyry developer in Peru as a rough valuation anchor:

"There's a company called AusQuest with a copper porphyry in Peru. The reason I raise this company is it has a market cap of $80 million. And I'm looking at Whipsaw going: 'Out of the gates the project should be worth at least 80 million bucks' - That's my theory anyway."

Whipsaw's Deal Structure and What Comes Next

The Whipsaw transaction is deliberately structured to limit Flagship's near-term cash commitment. The total option fee is A$6.5 million, of which A$350,000 (a A$100,000 non-refundable HOA payment plus a A$250,000 option agreement payment) has already been paid, alongside a A$500,000 payment due in cash or shares within 15 days of signing. The remaining A$5.65 million is payable in near-equal semi-annual instalments over 24 months - split A$3.65 million cash and A$2 million in shares with tranches due in December 2026, June 2027, December 2027 and June 2028. Beyond the option fee, a A$5 million milestone payment falls due only if Flagship delineates a 300Mt resource at 0.40% CuEq, and the deal carries a 2% net smelter royalty, half of which Flagship can buy back for A$3 million.

Importantly, Flagship has management control over Whipsaw from day one and carries no minimum annual expenditure or drilling requirements under the option, .meaning it can walk away from future payments without further obligation, at the cost of forfeiting the project and prior payments made. The company has proposed a follow-up programme of 15 diamond drillholes for approximately 4,500m, designed to test the continuity of mineralisation between the four modelled domains and to test depth extensions beneath the deepest historical intercept (359m, in hole 2005-07).

Funding the Build-Out: Exiting Lithium and Tungsten Talks

Flagship has also stepped back from non-core commodities to fund its two-asset strategy. The company signed a binding Sale and Purchase Agreement to sell its RK Lithium Project comprising the RK and BT lithium prospects held via Flagship's Siam Industrial Metal Co. Ltd subsidiary, and the KT lithium prospect held via Pan Asia 2 Metals (Thailand) Co. Ltd - to a Thai-based syndicate led by privately held Pendulum Auto Co., Ltd, for $4 million (~A$5.8 million) cash. Roughly 50% of the payment was received the week of the announcement, with the remainder due by mid-July 2026.

Flagship confirmed it is also in high-level discussions to sell its 100%-owned Khao Soon Tungsten Project, described as one of the largest undeveloped tungsten projects in southeast Asia. Taken together, completion of both divestments would finish Flagship's transition to a pure-play gold and copper explorer and developer, a strategic shift the company had flagged as its direction of travel. In the interview, Lock echoed the rationale directly:

"[The sale] brings in a substantial amount of cash. It's a lot cash up front that allows us to do the work we need for the rest of this year."

This removes the need to raise dilutive equity capital in the near term while both Isidora's PFS work and Whipsaw's technical review are underway, a materially different funding position than if Flagship had needed to tap the market at current, heavily discounted share price levels.

Valuation Gap and the Dilution Question

Lock argues the market has yet to reflect Isidora's scale, pointing to a self-published peer curve of ASX and TSX-listed prefeasibility-stage gold developers with resources above 500,000 ounces, which averaged approximately A$176 per resource ounce as of early July 2026. Against that, Lock estimated Flagship's own implied enterprise value at roughly A$24-25 per ounce - an eight-times gap he attributes primarily to the market's caution around future dilution rather than any issue with the underlying asset.

"We are incredibly undervalued at this point. The biggest worry for me ultimately, on valuation, is dilution when you raise money. So we don't want to be down here for too long."

Lock, who holds close to a fifth of Flagship's shares, said the priority for any capital raised - beyond general marketing to shareholders - would go toward completing the prefeasibility study, which he believes is largely funded already given the volume of work already under way. He was more circumspect on Whipsaw's contribution to that valuation gap, noting the asset's value is not yet reflected on the balance sheet at all, but that management believes it "holds significantly more value" once the drilling-versus-spin-out decision is made and communicated to the market.

Lock has been explicit that if Whipsaw doesn't attract the valuation he expects, the company retains the option to spin it out rather than let it dilute focus from Isidora. That optionality - two commodities, two jurisdictions, two distinct catalyst paths - is central to how Flagship wants to be assessed by investors going forward, rather than as a single-asset story dependent on one gold price cycle.

Investment Thesis for Flagship Minerals

- Twin-commodity optionality: A 2.1Moz advancing gold project in Chile paired with a large, low-cost-entry copper Exploration Target in a Tier-1 Canadian jurisdiction, diversifying the catalyst base beyond a single asset.

- Near-term catalysts at Isidora: Metallurgical test work results and an updated mineral resource estimate (targeted late 2026/early 2027) both feed directly into the prefeasibility study.

- Low near-term cash commitment on Whipsaw: Option structure defers the bulk of consideration over 24 months with no minimum spend obligations, preserving capital for Isidora.

- Non-core divestment funds the build-out: US$4 million lithium sale (plus a potential tungsten sale) removes distraction and adds cash without shareholder dilution.

- Valuation gap versus peers: Management's own peer curve implies significant re-rating potential if the gap narrows as the PFS and updated MRE de-risk the project.

- Structural decision pending on Whipsaw: Watch for confirmation on further drilling versus a spin-out decision - this will materially affect how the asset is valued and by whom.

- Water solution disclosure: A formal announcement on Isidora's water strategy would remove one of the project's most-cited technical risks.

Macro Thematic Analysis

Flagship's pivot mirrors a broader shift among junior developers toward pairing an advancing gold asset with copper optionality, as generalist and specialist capital alike position for a widening copper supply gap even as near-term project economics remain gold-led. Large-scale, low-grade porphyry systems in established, infrastructure-rich jurisdictions - precisely the profile Whipsaw fits, sitting adjacent to an operating mine in British Columbia - are increasingly viewed as scarce, optionality-rich assets even before a maiden resource is declared. As Flagship put it in its acquisition announcement:

"Whipsaw provides Flagship's shareholders with exposure to one of the strongest long-term commodity themes in the market. As global copper grades decline and new discoveries become increasingly difficult to find, we believe large-scale copper projects in Tier-1 jurisdictions will become increasingly valuable."

For investors, the read-through is that companies able to add credible copper exposure to an already-funded, de-risking gold story - without diluting shareholders to do it - may command a structural premium as the copper investment case broadens beyond specialist funds into the generalist mining audience.

TL;DR

Flagship Minerals has reshaped its portfolio around gold and copper: it acquired the large-scale Whipsaw Copper Project in British Columbia in June, completed a metallurgical drilling and trenching programme at its 2.1Moz Isidora Gold Project in Chile, and sold its RK Lithium Project for US$4 million to fund the build-out without dilution. Managing Director Paul Lock argues Isidora trades well below peer valuations and that Whipsaw, structured with deferred payments and no minimum spend, offers low-cost copper optionality next to Hudbay's operating Copper Mountain mine. Catalysts ahead include an updated Isidora resource targeted for late 2026/early 2027, a prefeasibility study, a water-solution announcement, and a decision on Whipsaw's drilling versus spin-out path.

FAQ (AI-generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed